SCHW - The Broyhill Q2 2023 Letter

2023-07-27 11:15:00 ET

Summary

- Broyhill Asset Management is a boutique investment firm guided by a disciplined value orientation. We operate outside of the fray and invest with a rational, objective, long-term perspective.

- Broyhill Asset Management is widening access to its flagship equity strategy for the first time.

- The portfolio's largest contributors to performance were Fomento Economico Mexicano, Fiserv Inc., and McKesson Corporation.

- The economic outlook is deteriorating, with recessionary indicators piling up, leaving equities vulnerable to a correction in the second half.

EXECUTIVE SUMMARY 1

After spinning out the investment team as an independent entity last fall, we are widening access to our flagship equity strategy for the first time. We discuss the careful growth in assets that has gotten us here and why we are excited about the near future for fundamental investors.

PERFORMANCE REVIEW

The portfolio's largest contributors to performance were Fomento Economico Mexicano ( FMX ), Fiserv Inc. ( FI ), and McKesson Corporation ( MCK ). The largest detractors to performance over the quarter were First Horizon Corp ( FHN ), Anheuser-Busch InBev ( BUD ), and Bayer ( BAYRY ).

PORTFOLIO COMMENTARY

Our top five equity investments are Activision Blizzard ( ATVI ), Philip Morris ( PM ), Fiserv ( FI ), Fomento Economico Mexicano ( FMX ), and Ambev SA ( ABEV ). New investments include The Charles Schwab Corporation ( SCHW ), Nintendo Co. ( NTDOY ), British American Tobacco ( BTI ), and PayPal Holdings ( PYPL ).

MARKET OUTLOOK

The economic outlook is deteriorating as recessionary indicators pile up. Yield curves are deeply inverted, commodity prices are non-confirming, and manufacturing activity is contracting. Despite these risks, stocks have rallied, driven by surging enthusiasm for AI technology, aggressive retail buying, and a resurgence of flows into equity funds. This combination leaves equities vulnerable to a correction in the second half. Meanwhile, the full impact of tightening monetary policy has yet to flow through the economy. Markets are likely to take notice when labor markets begin to crack, impacting consumer confidence and ultimately leading to more profit declines and job losses. This is the most dangerous part of the cycle.

BOTTOM LINE

The first half of the year was frustrating for fundamental investors but has created a lengthy and tasty menu of investment opportunities that have been largely ignored because they don't have "AI" attached to them. Given the increasing economic risks and elevated equity valuations, we remain conservatively positioned, deploying capital where the price already reflects more challenging times ahead. Our pipeline is full, and our enthusiasm for the portfolio and prospective returns is as high as ever.

| 1 Executive summary provided by ChatGPT and lightly edited by Broyhill Asset Management. |

INTRO

At Broyhill, capital preservation is in our blood, running through our veins since the family office was first founded nearly a half century ago. It's been an incredible journey marked by careful stewardship, lifelong learning, and the relentless pursuit of excellence. Now, after spinning out the investment team as an independent entity, we're thrilled to announce an exciting new chapter.

Our flagship equity strategy was solely available to a single family for a generation. In 2005, that family asked me to help spearhead their wealth conservation efforts, and since that time, we've relentlessly pursued this goal. Over the years, we've selectively brought on external investors, never trying to be all things to all people. We've never strived to be a one-size-fits-all, attract-every-dollar kind of investment firm. Instead, we recognize our strengths and work hard every day to optimize them. For investors unwilling to put their hard-earned nest eggs at high risk, we believe that a rational, independent, valuedriven, investment philosophy has never been more important than it is today.

We are now widening access to our flagship equity strategy for the first time. In the remainder of this letter, we'll provide an update on the portfolio's second quarter performance and review recent portfolio activity, which has been higher than normal, compliments of a rapidly growing opportunity set . We are excited about the road ahead and look forward to traveling it with you. Given the market backdrop, we can't think of a better time for a fundamental value investor to get started.

PERFORMANCE REVIEW

The Broyhill Equity portfolio fell 0.4% net of all fees and expenses in the latest quarter. Year to date, the portfolio has returned 10.9% net of all fees and expenses. For the portfolio's full history, please see the Broyhill Equity fact sheet by clickin g here . While our performance appears rather uneventful, the most recent quarter has been anything but, as markets and risk appetite swayed back and forth repeatedly. AI has been the sole driver of markets this year, creating the second tech bubble in years. It's been well documented that, except for a few stocks that have provided stellar year-to-date performance, the rest of the market has been roughly flat. Despite "missing out" on related bubble stocks, we had a strong start out of the gate. The portfolio gained 11.3% in the first quarter, outperforming global equity indices. April was pretty much a non-event for anything other than AI, followed by May, where just about anything that could have gone wrong in the portfolio went wrong in spectacular fashion. Thankfully, the portfolio rebounded nicely in June as the rally broadened, sentiment rose, and our investments caught a bid.

The largest contributors to performance over the quarter were Fomento Economico Mexicano (FMX), Fiserv Inc. (FI), and McKesson Corporation (MCK). The largest detractors to performance over the quarter were First Horizon Corp (FHN), Anheuser-Busch InBev (BUD), and Bayer (BAYRY). A brief recap on top contributors, along with a more detailed commentary on top detractors, is provided below as we gain more insight from sunshining our losses than celebrating our wins.

TOP CONTRIBUTORS

We are constantly amazed at how quickly sentiment swings from one extreme to the other, seemingly turning on a dime or on a single headline. Management at Fomento Economico Mexicano orchestrated a similar U-turn in sentiment when the company announced the results of its eagerly anticipated strategic review. Simply by selling off a few non-core assets and a single public investment, the company was able to convince investors to remove the "complexity discount," and the gap between the stock's price and its intrinsic value closed. Management at Fiserv continues to execute. Amid fears of a recession and lower consumer spending in the latter half of the year, Fiserv is positioned to add another year to its uninterrupted, 32-year track record of double-digit earnings growth. The stock's performance over the years has largely been driven by earnings growth as the market has yet to award FI with the premium valuation we believe it deserves. Following the first quarter's earnings, McKesson delivered a triple beat by beating consensus in the quarter, guiding next year EPS growth above consensus, and raising its long-term operating earnings growth. Investors were pleasantly surprised with what Deutsche Bank dubbed the "Rare Trifecta."

TOP DETRACTORS

In February 2022, Toronto-Dominion Bank ( TD ) offered $25 per share to acquire First Horizon Bank (FHN). A year later, the banks pushed the closing date back to allow more time for regulatory approval, a move good for a 20% decline in the stock. Weeks later, FHN fell another ~30% with the collapse of Silicon Valley Bank. We initiated our position in the heat of the crisis. With the stock already down in concert with banking peers, we believed the downside was limited and that the odds of TD walking away from the deal were even smaller, as the Canadian bank had its eyes on FHN and its southeastern footprint for years. We were wrong on both counts, as regulators made it clear they would not sign off on the deal, and shares fell well below our estimated downside as arbs blew out of the stock. We still believed the bank was undervalued, considering the increased tangible book value complements of a hefty break fee. However, we fully exited the position given continued uncertainty around the regional banking system and the likelihood of decreased normalized earnings power due to pending changes to capital requirements.

Problems at Anheuser Busch InBev ( BUD ) began on April 1 with Dylan Mulvaney's social media post, which ignited a fiery backlash amongst Bud Light customers across 'Merica. With volumes down sharply, and competitors gaining share at BUD's expense, operational deleveraging is set to weigh heavily on US margins amid peak demand pressure in the second quarter. Despite severe US headwinds (second-quarter operating profit maybe half of last year's levels), we still expect BUD to grow consolidated operating profit at a mid-single-digit rate for the full year. With current issues well understood and investor sentiment in the gutters, we see significant upside in a stock, which is approaching a double-digit FCF yield. With FX headwinds and rising input costs reversing course, increasing margins are likely to drive positive surprises into FY24 as continued deleveraging accrues more value to shareholders.

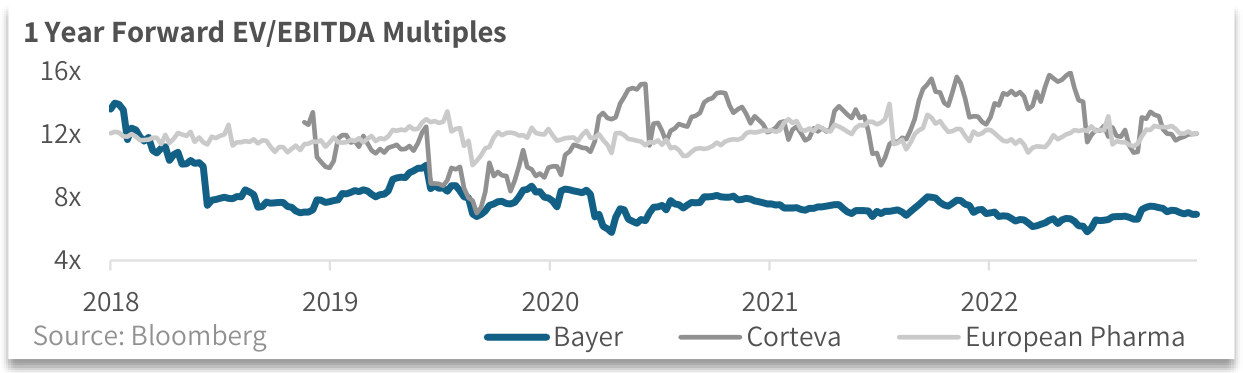

Bayer, the German pharmaceutical and life sciences company, is firmly in the running for our most frustrating investment. Following a steady increase in consensus estimates since bottoming in early 2021, numbers took a dive after the company's first-quarter earnings report. While the miss was relatively minor, the stock's reaction was not, suggesting that investors were already pricing in additional downgrades to guidance. The incoming CEO may reset the bar even lower after taking a good look under the hood, but we think there is more risk that the CEO, a Roche veteran, will give in to activist investors who are pressing to break up the conglomerate. [1] Should investors decide to sharpen their pencils and value Bayer's individual segments on a stand-alone basis, we believe the discount to peers would quickly disappear. Our base case sum of the parts estimates pegs the company's fair value at nearly twice current levels. Our longer-term upside estimates are materially higher.

1 Year Forward EV/EBITDA Multiples

{kind=link}

PORTFOLIO COMMENTARY

At quarter-end, our top five investments in alphabetical order were Ambev SA, Activision Blizzard, Fiserv, Fomento Economico Mexicano, and Philip Morris. Over the quarter, we made several new investments, fully exited two positions, and rebalanced our tobacco exposure. Increased volatility has provided plenty of opportunities to optimize exposure and increase the portfolio's expected returns. Since this year's (mini) financial crisis, when the regional bank index collapsed by 23.0% in three days, was the biggest driver of short-term volatility, let's begin there.

THE CHARLES SCHWAB CORPORATION

After the failure of Silicon Valley Bank (SVB), the market turned a critical eye to the financial sector. Institutional investors sharpened their forensic accounting pencils and hypothesized, "What would happen to Schwab should its depositors take their money and run?" While this is a helpful exercise, we believe the probability of a run on Schwab Bank is low. Schwab is not SVB. Its deposit base is sticky and fragmented; Silicon Valley's was not. Less than 10% of SVB's deposit base was under the FDIC insurance limit, and its core customers were rate-sensitive startups and venture capitalists with fickle cash needs. In contrast, ~80% of Schwab's deposit base is under the FDIC's limit and spread across millions of brokerage accounts that keep cash on hand for investment. Rather than spending our time replicating doomsday scenarios, we began by estimating the risk to Schwab's earnings power should it need to raise the rate paid on deposits in line with competitors. Even under this scenario, we believe our downside is limited. Longer term, we believe Schwab has multiple levers it can pull to monetize the ~ $7 trillion in assets trusted in its custody.

NINTENDO CO.

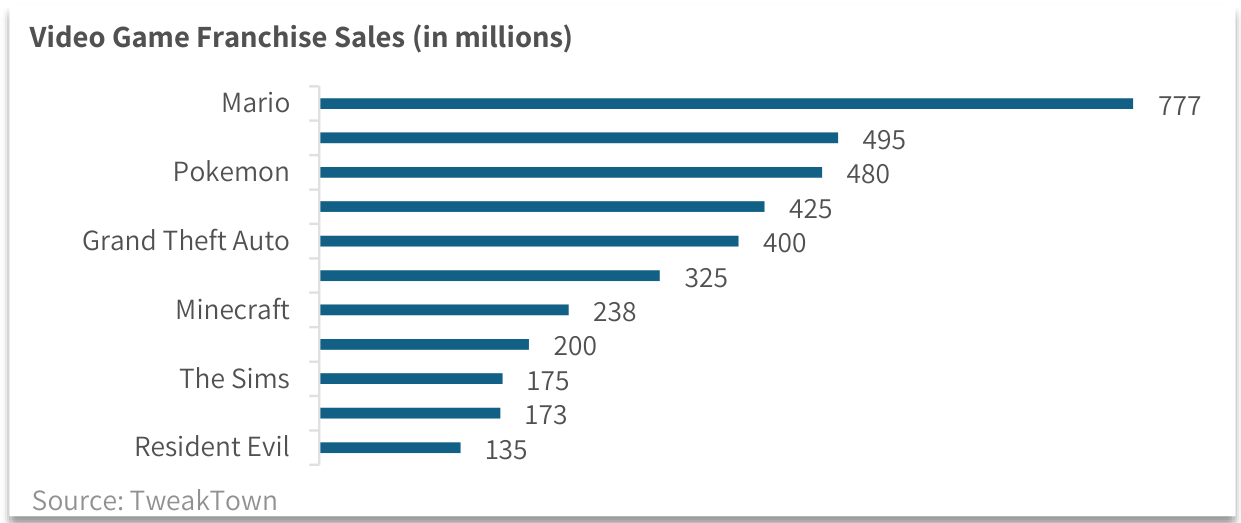

Nintendo has long suffered from self-inflicted opacity and what has been interpreted as a general disregard for shareholders or at least a less "western" view of shareholder capitalism. We have followed the company closely for years, looking for any hint that those views were shifting. We have long been intrigued by the company's creative culture and its iconic intellectual properties, both of which are nearly unparalleled in the media industry. The recent release of The Super Mario Brothers Movie, which blew away even the most optimistic expectations, the opening of the company's first Super Mario theme park in the US (following its inaugural opening in Japan and scheduled opening of its second US park), and the addition of the company's first American board member (founder and CEO of film producer Illumination) would seem to indicate that the winds are changing. Shares of Nintendo also appear set to enjoy a number of catalysts in the future, including the next generation Switch and a robust slate of new games, most recently demonstrated by the latest installment of The Legend of Zelda, which sold 10 million copies in its first three days, making it the fasting selling game of all time. Notably, Nintendo tops the charts with two of the three best-selling game franchises of all time. [2] We think shares are a long way from reflecting the company's increased earnings power, which has inflected higher alongside the transition to the Switch platform and increasing share of higher margin digital sales.

Video Game Franchise Sales (in millions)

{kind=link}

TOBACCO

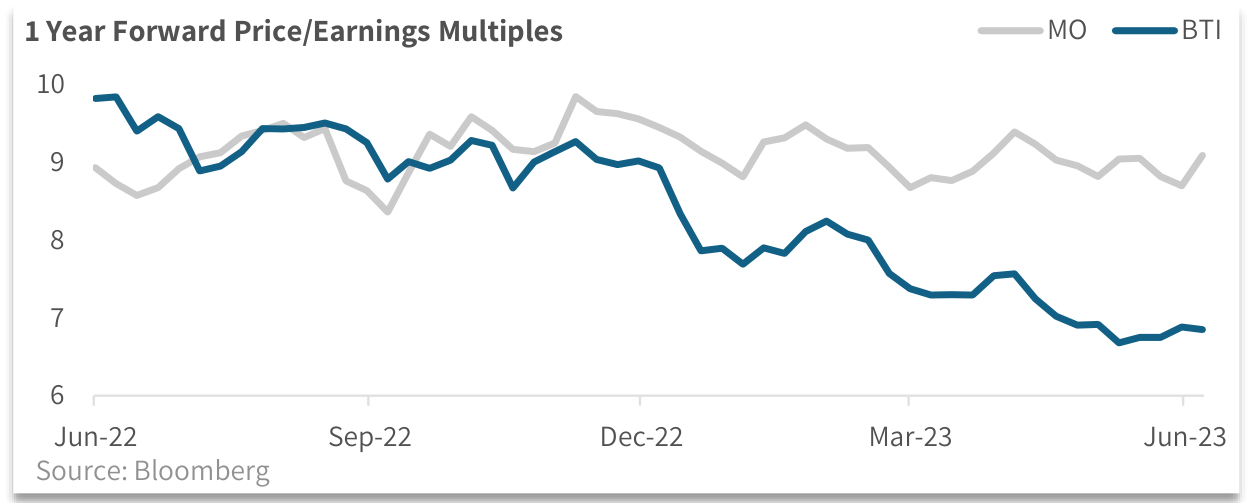

In our year - end letter to investors, we explained why we had reduced our investment in Altria and reinvested the proceeds to increase our position in Philip Morris. This quarter, we exited the position completely, swapping our exposure for British American Tobacco, as the valuation gap became too hard to ignore. Investors are rightly frustrated with the stock. In addition to the menthol ban, leadership change, and North Korea kerfuffle. BTI has mountains of debt piled on its balance sheet following the acquisition of Reynolds, which will limit options for capital allocation, namely more buybacks. While we'd love to see new management aggressively repurchasing stock at these prices - shares trade below 7x earnings - we don't think buybacks are necessary for the investment to work from here.

1 Year Forward Price/Earnings Multiples

{kind=link}

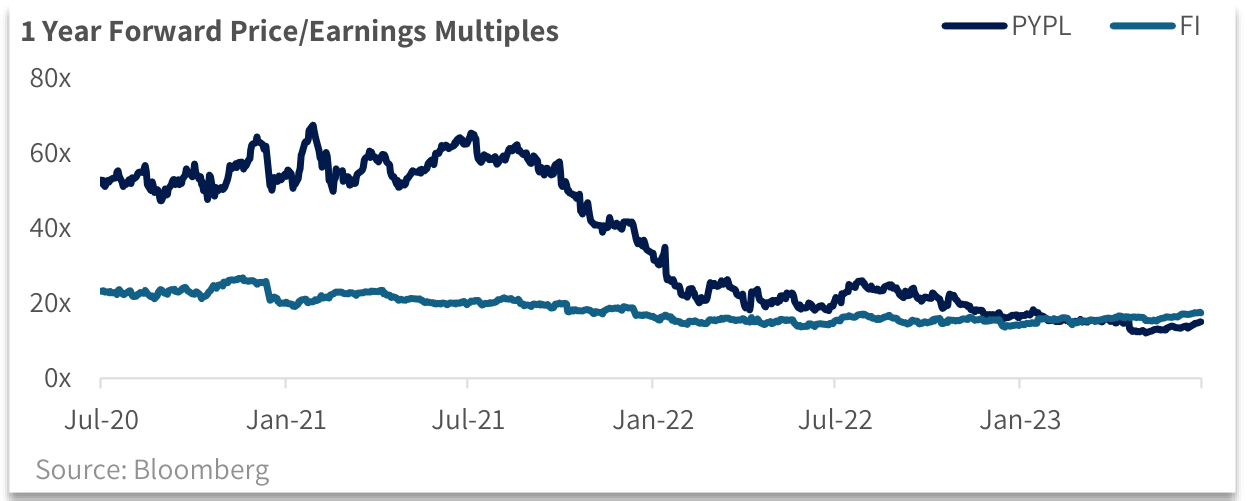

Our foray into the payments sector began a few years ago with an investment in Fiserv, which we detailed in ou r 2021 year - end letter t o investors. While Fiserv continues to execute as expected, and the stock's multiple has increased from recent lows of 14x to 16x earnings, shares still trade at a meaningful discount to the market. In the meantime, multiples across the "sexy, rapidly-growing disrupters" called out in our Fiserv thesis, have crashed like a house of cards in a hurricane. PayPal traded at nearly 70x earnings at its peak, or almost 3x the market's multiple. It now trades at a multiple below Fiserv, roughly two-thirds of the market's valuation. We didn't think 70x was the right price a couple of years ago, and we don't think 12x is the right price today. While the company has certainly had its share of missteps and miscalculations, we don't think the business is broken. Competition has increased as share gains at Apple Pay have accelerated, heightening an already fiercely competitive landscape. At the same time, CEO Dan Schulman's announced retirement has created a leadership void at the top. But a refocused management team under increased pressure from an activist investor to aggressively cut costs should drive accelerating free cash flow growth for the next several years. We have followed this company since our early investment in eBay, which was driven largely by the potential for a PayPal spin-off. We are happy to own it again at the current valuation.

1 Year Forward Price/Earnings Multiples

{kind=link}

MARKET COMMENTARY

Almost without exception, all periods of speculative excess in financial markets are assisted by easy money and brought to an end when interest rates start to rise once more.

- Milton Friedman, The Monetary History of the United States

After a brief hiatus, irrational exuberance has returned with a vengeance strikingly similar to the 19992000 and 2020-2021 periods! The most ridiculous stocks with the most unprofitable business models are leading the pack, with the most aggressive fund managers riding their coattails. Six months ago, it appeared that many of them would be closing shop, but after being bailed out by reignited animal spirits, they are back to raising eye-popping amounts of capital earning eye-popping fees. Some folks never learn.

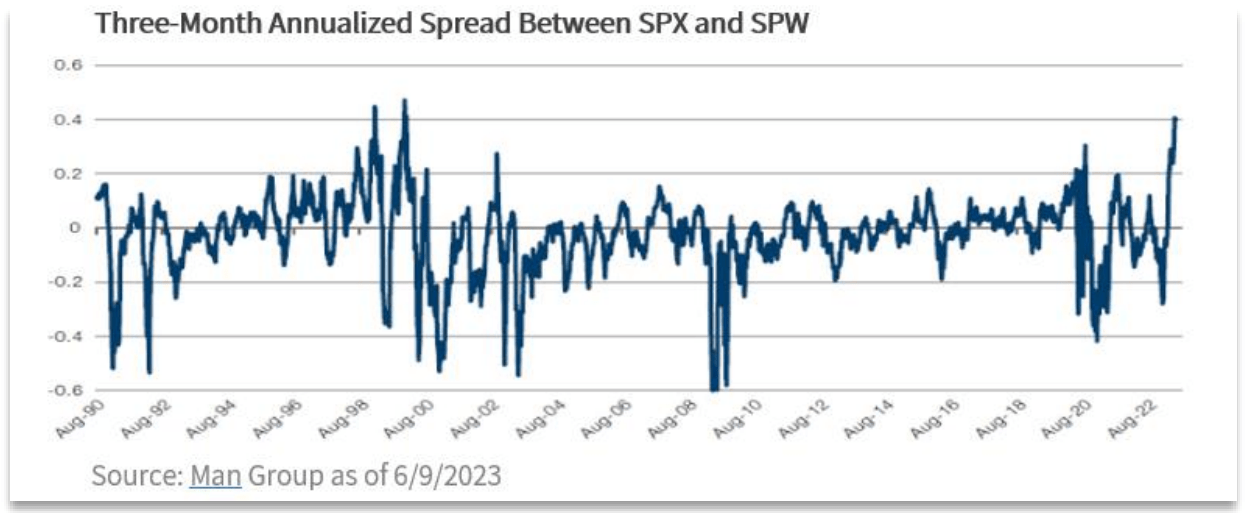

Meanwhile, market concentration has reached record levels last seen amidst the Nifty Fifty, preceding the 70s bear market. The only other times the spread between the cap-weighted and equalweighted index has been this great were in December 1999 and January 2000. [3] Monetary tightening proved to be the final straw for the market in 2000. We would be surprised if this setup didn't end the same way, with many market participants likely to suffer the same fate.

{kind=link}

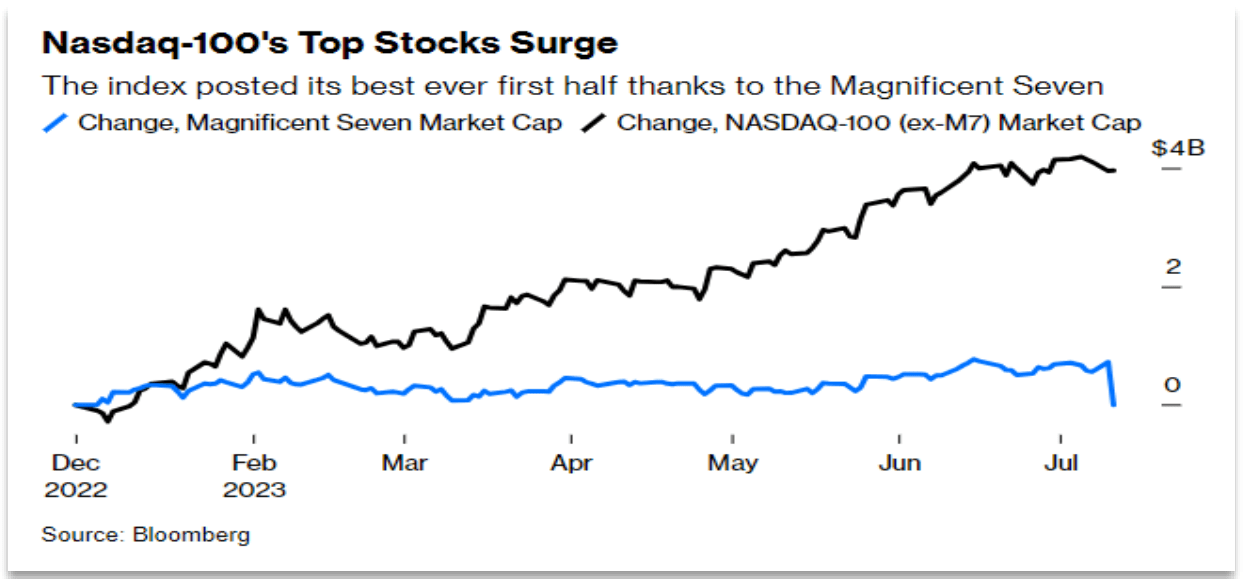

Nearly a quarter of companies in the Nasdaq 100 are once again trading at or above 10x sales . Following its best first-half performance in history, six of its largest members now make up more than half the index. Accordingly, Nasdaq has taken notice, announcing a "special rebalance" subsequent to quarter end. As it turns out, passive investing may not provide investors with the diversification they seek as more money flows into index funds and, ultimately, into the largest, most overvalued companies in that index. As the weighting of the top stocks in the index may be slashed by 40%, those passive flows will automatically follow suit, while active investors will have to decide if they want to sell these big names they were "forced" to own to minimize career risk. [4]

{kind=link}

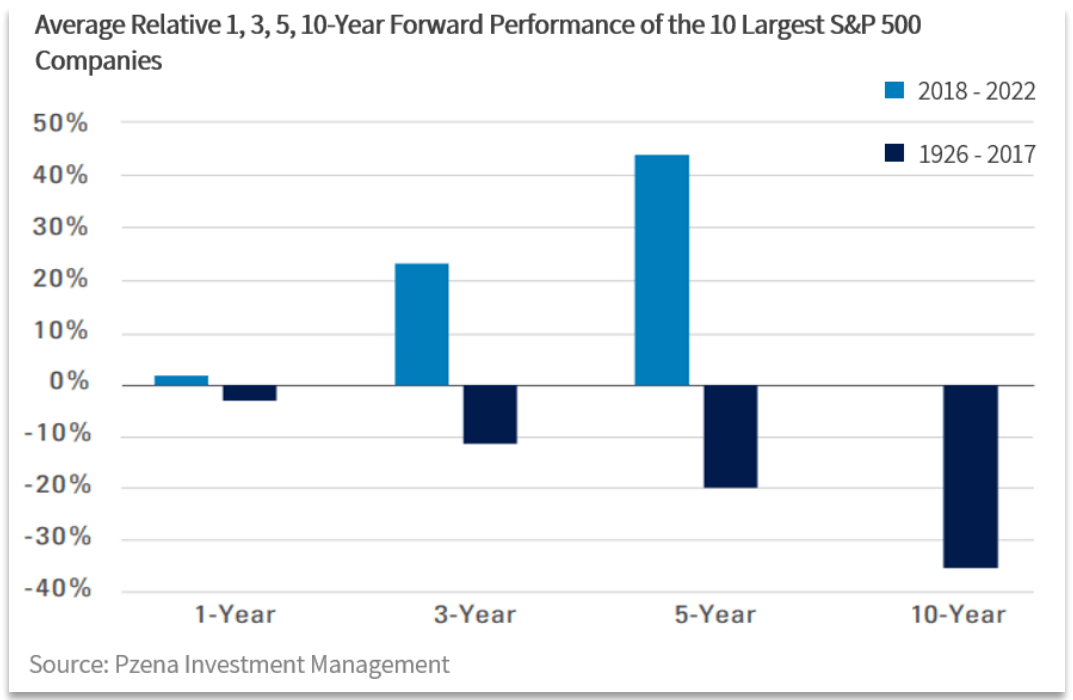

This year's rally has been one of the narrowest on record, as the name of the game has been "get me into the large tech names at any price." The top ten contributors to the market's performance are up almost 60% year-to-date. Historically, about half of their returns have come from earnings growth. This year, over 95% of that return has come from multiple expansion. Investors should take note: multiple expansion has never been a reliable or sustainable driver of long-term performance. Neither has owning the largest stocks in an index that have underperformed the market, on average, over every time period. We have seen similar levels of concentration in the not-too-distant past. It was among the most challenging periods for value investors on record. The upside, as we all learned, was that those with the patience and conviction to maintain discipline were well rewarded. To survive and thrive in this environment will require the same fortitude and common sense.

{kind=link}

Stocks have rallied despite a deteriorating economic outlook as AI Mania has reignited animal spirits. A quick scan of recent headlines tells you all you might need to know about current market sentiment. [5] [6] [7] [8] Investors are chasing stocks that have already re-rated sharply. AAII is at its most bullish reading since the recent peak along with several other measures of sentiment. Mutual funds have been aggressive buyers of stocks over the past month, as FOMO (Fear of Missing Out) outweighs economic concerns. These fund managers, however, are nowhere close to as aggressive as retail investors who recently doubled their single-stock options trading activity. And weekly flows into equity funds have spiked as investors have flocked back into the technology sector.

Such an abrupt increase in positioning suggests that investors have quickly capitulated, leaving equities more vulnerable to a correction in the second half.

{kind=link}

A year ago, central bankers promised to slam the breaks on the economy to tackle inflation. Despite these efforts, markets are higher today, and the most widely anticipated recession in history has yet to materialize. Earnings have surprised to the upside, and estimates have recently turned higher. Stocks are climbing the proverbial wall of worry. Perhaps the recession and bear market has already taken place - economic growth contracted for two consecutive quarters, in late 2021 and early 2022, and the earnings drawdown was comparable to previous recessions. So, one could certainly argue that markets have already discounted a recession. But it's not an argument one is likely to win.

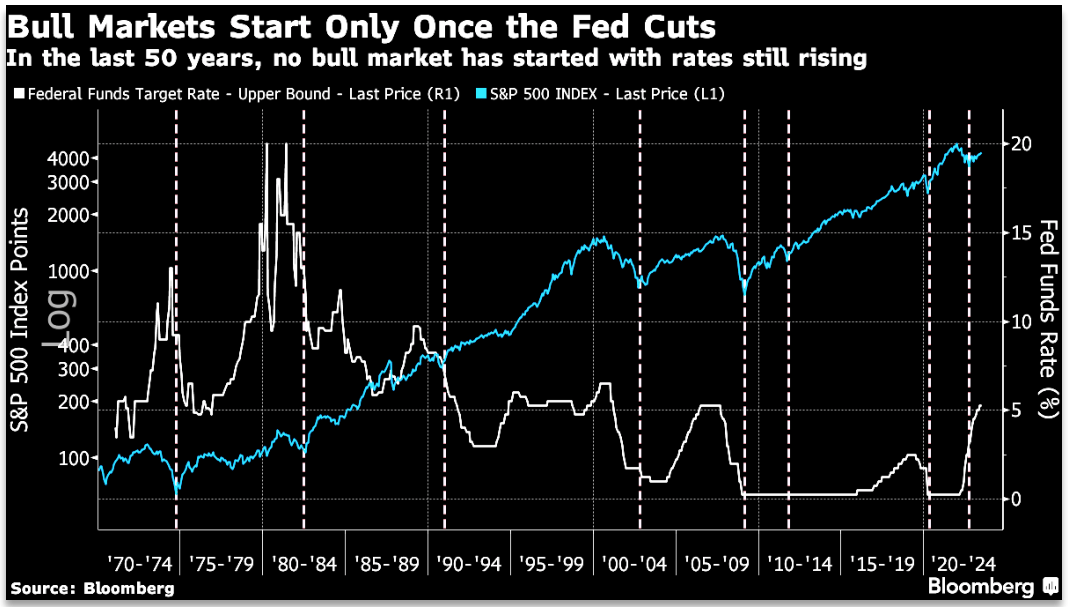

While we don't have a lot of confidence in our ability to forecast the exact timing or magnitude of recession, that doesn't mean we should ignore it. Instead, as in all aspects of investing, it's helpful and necessary to think probabilistically about the range of outcomes. If a downturn has been completely avoided, maybe last year's selloff was just an extreme response to extreme speculation, like

Black Monday in 1987. That seems like a stretch. Markets usually wait until the Fed has started cutting rates before bottoming (see chart below). So, if this is a new bull market, it would be the first to start while the Fed is still hiking. On the other hand, if a recession has only been delayed, it would be very strange if the low for stocks was already in before the economic downturn even began.

While neither of these scenarios is impossible, we believe that the lagged effects of the past year's extraordinary monetary tightening have yet to flow through the economy and financial markets. [9] Given increasing complacency amongst investors and stock prices, which already discount the bestcase scenario (a soft landing or no landing at all), the greatest risk would be any potential future other than the Fed perfectly sticking the landing.

{kind=link}

This seems like a poor bet. It's also contrary to the old market adage: don't fight the Fed. Central bankers often lie; ask them about the banking system, and the only acceptable response is, "Everything is fine." But when they tell you that they are determined to stomp out inflation and show you their intent by raising rates at the fastest pace on record, you better believe them! To that effect, Jay Powell has been unusually blunt this cycle, issuing stark warnings about the "pain" facing households and businesses as he jacks up rates to engineer a recession and slow inflation. [10]

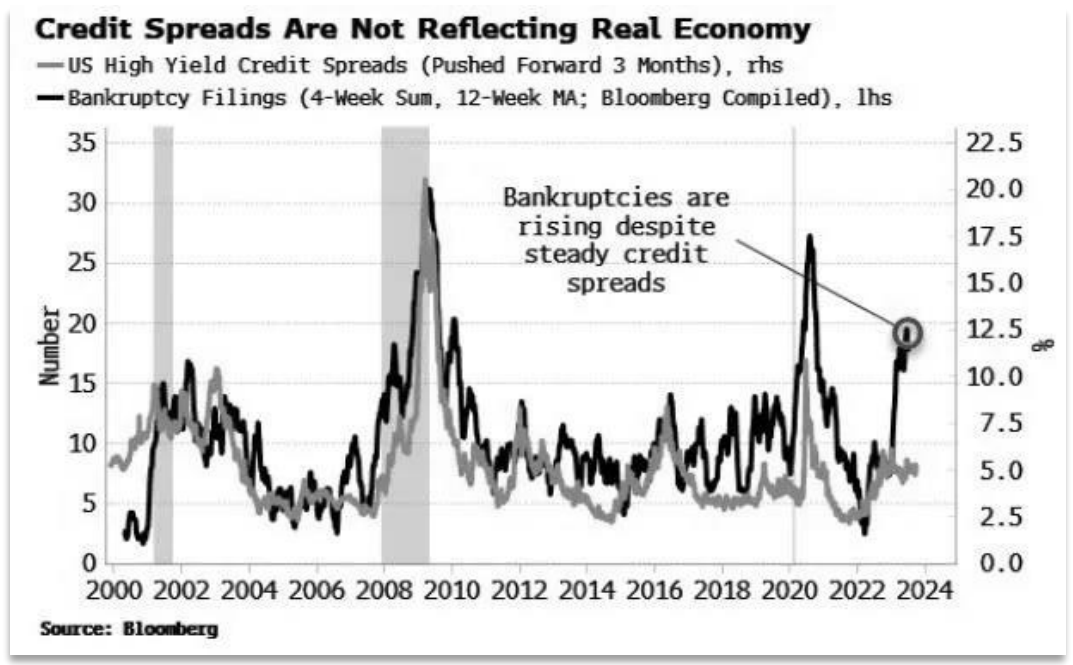

As such, investors should be careful not to read too much into the recent resilience of the economy and earnings. Optimism is keeping valuations at record levels, but monetary policy is already contractionary, and we were just promised "at least" two more hikes. Recent turmoil in the banking system and the ongoing commercial real estate implosion should drive increasing losses on bank loan sales, compounding the liquidity squeeze and tightening credit conditions even further. Historically, the bulk of credit tightening has come after the hiking cycle is complete, but we now have simultaneous tightening from the Fed and the banks for the first time in history.

Since coincident economic indicators have yet to catch up to the sharp decline in leading indicators, markets have refused to price in a recession. But recessionary indicators keep piling up and should intensify in the second half. Yield curves are deeply inverted. Inflation has rolled over. Commodity prices refuse to confirm the equity rally. And manufacturing activity is contracting. Meanwhile, investors are content to keep their heads in the sand as credit spreads blatantly ignore underlying credit conditions while bankruptcies continue to pile up.

{kind=link}

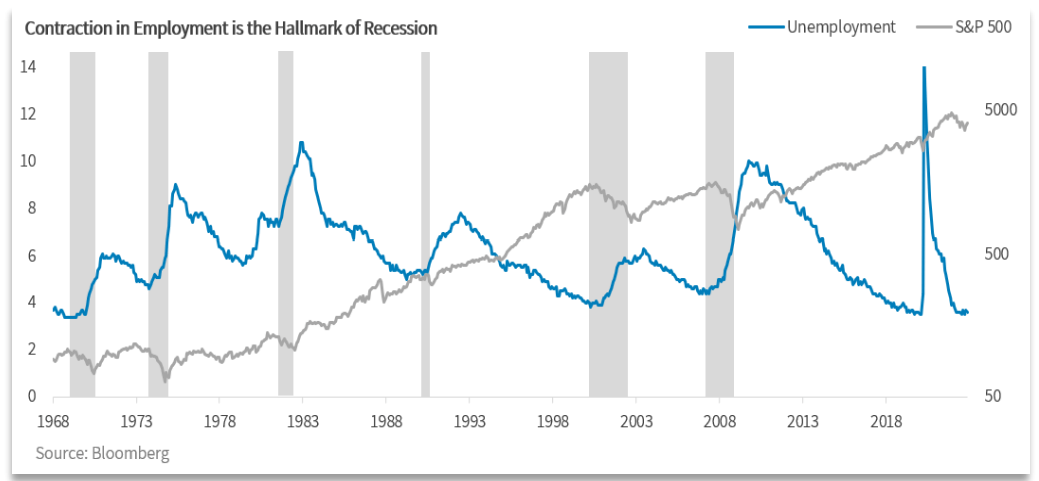

Making matters worse, the Fed is still hiking rates while earnings growth has already turned negative. This has never happened before. Tightening policy in what is already a profits recession is not exactly a positive for markets.

Investors remain hopeful, but such hopes have historically disappointed once labor markets began to crack. Notably, a contraction in employment is the hallmark of recession as it hits consumer confidence and reduces spending, leading to more profit declines and more job losses. This is where reflexivity kicks in, and it represents the most dangerous part of the cycle.

{kind=link}

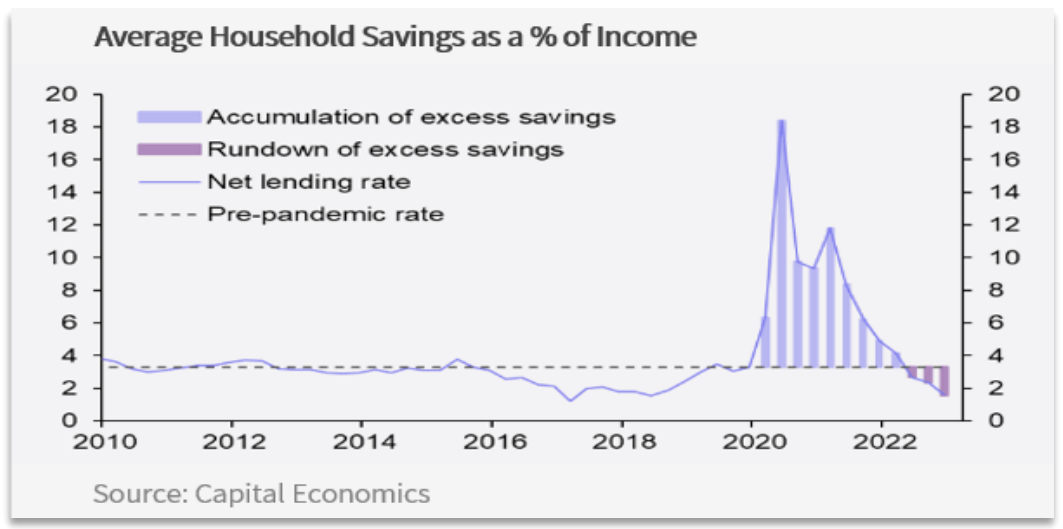

All cycles are different. But this cycle has been extraordinary thanks to the unique circumstances of the pandemic. Excess savings that built up during the lockdowns were then unleashed into the market, sending asset prices to cycle highs at a record pace. But those same consumers are starting to show signs of weakness, as excess savings have been depleted and will soon be exhausted, and households continue to splurge on credit card debt to sustain spending. For the average consumer, the bulk of savings has already evaporated (chart below). [11] Real discretionary spending has been declining for the better part of the past year, and renewed student loan payments are unlikely to help. [12] This is hardly the picture of a robust consumer.

{kind=link}

Against this backdrop, investors have largely given up on the most widely anticipated recession in history and now believe that the worst for corporate earnings is behind us.

Estimates have recently ticked higher in contrast to weakening economic activity, and markets have anxiously discounted accelerating earnings growth into year-end. We think this is a mistake and have grown increasingly cautious as the year has progressed while the rest of the street continues to ratchet up estimates. We expect a more challenging backdrop in the second half.

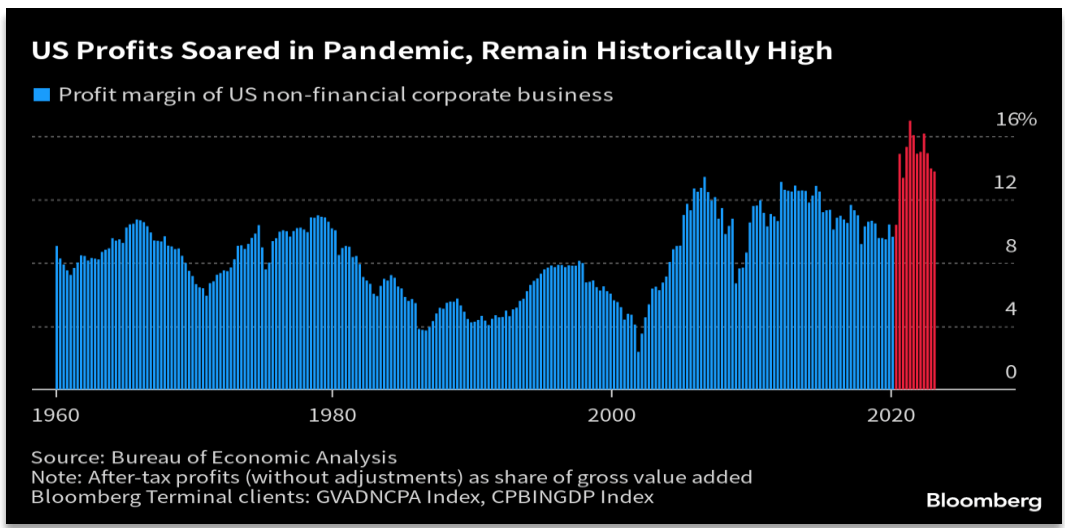

Most market participants understand the significant impact that unprecedented, stimulus-fueled demand had on consumer spending. But record profit margins are an often overlooked yet equally important consequence of trillions of dollars in pandemic deficits.

Margins were already elevated before the pandemic. Now they are just plain silly. It would be a mistake to assume those effects are permanent.

{kind=link}

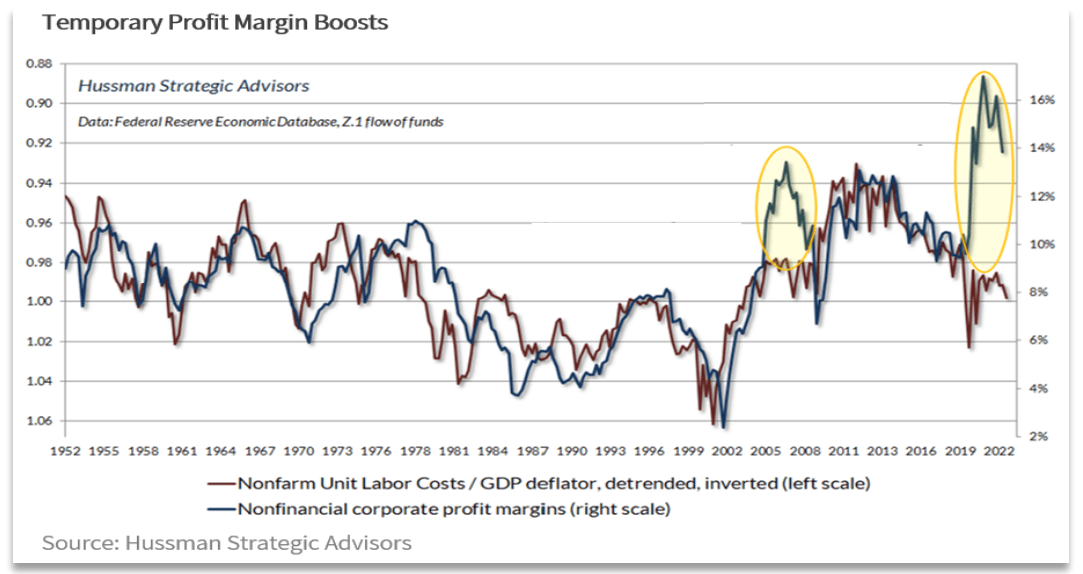

It would also be a mistake to assume that "new-age" technology has single-handedly and sustainably increased the normal level of corporate profitability. While there is no denying that corporate profits have remained higher than average in the age of the internet, Occam's Razor suggests there is a much simpler explanation. Plainly, two major macroeconomic tailwinds have accounted for nearly all of the increase. Notably, neither is permanent, and both appear set to reverse.

- First, low rates boosted profit margins as interest costs plummeted. Every 100 bps decline in corporate borrowing costs boosts margins by that same 100 bps. Given that higher rates impact margins with a lag, it's safe to assume profits will be materially lower in the next year. At current rates, implied profit margins are several points lower than current elevated levels. And margins typically undershoot in recessions, so a steeper drop shouldn't be ruled out.

- Second, profits move in the opposite direction of labor costs, which are the largest single expense on most income statements. Luckily for US corporations, labor costs have been depressed since the global financial crisis. Given the inverse relationship, it should come as no surprise that record low labor costs as a percentage of GDP sent profit margins to record highs.

This tight economic relationship can be seen for decades in the chart below, with two notable exceptions highlighted in yellow. In 2007-2008, profit margins were temporarily boosted as households used their home equity lines as ATMs. But once those ATMs ran dry, margins collapsed back to trend. We see an even greater gap today as pandemic subsidies boosted household balance sheets and corporate profits.

Increasing labor costs suggest that the current level of margins is unlikely to be sustained (see yellow circles in chart below).

{kind=link}

Centuries of history inform us that margins are mean reverting: what goes up must come down. It's reckless to assume otherwise. And it's more reckless to value equities on that assumption. The failure of profit margins to live up to current expectations could have very nasty consequences for a market valued at record extremes on record margins. At this point, chasing the recent market rally is akin to picking up pennies in front of a steam roller, especially if it turns out that mega-cap earnings are not as insulated from the business cycle as everyone assumes.

BOTTOM LINE

After a short-lived period of reversion to normalcy, another narrower cohort of the market appears to be reinflating the recently busted bubble. Consequently, the first six months of the year have been frustrating for fundamental investors. This was the second worst six-month period on record for value relative to growth, behind the depths of the pandemic and the height of the dot-com bubble. Notably, both wound up being particularly rewarding entry points for fundamental investors.

The bifurcation between AI and everything else has made investing in an increasingly uncertain environment even more challenging. It also suggests that investors are ignoring good businesses simply because they don't have an AI label attached to them. The good news, as evidenced by our increasing portfolio turnover, is that the investment menu of such ignored opportunities is as lengthy and tasty as ever. In fact, despite the short-term madness of crowds, or perhaps because of it, our research pipeline is growing with an ongoing flood of new ideas, and our enthusiasm for our portfolio and prospective returns are as good as they've ever been.

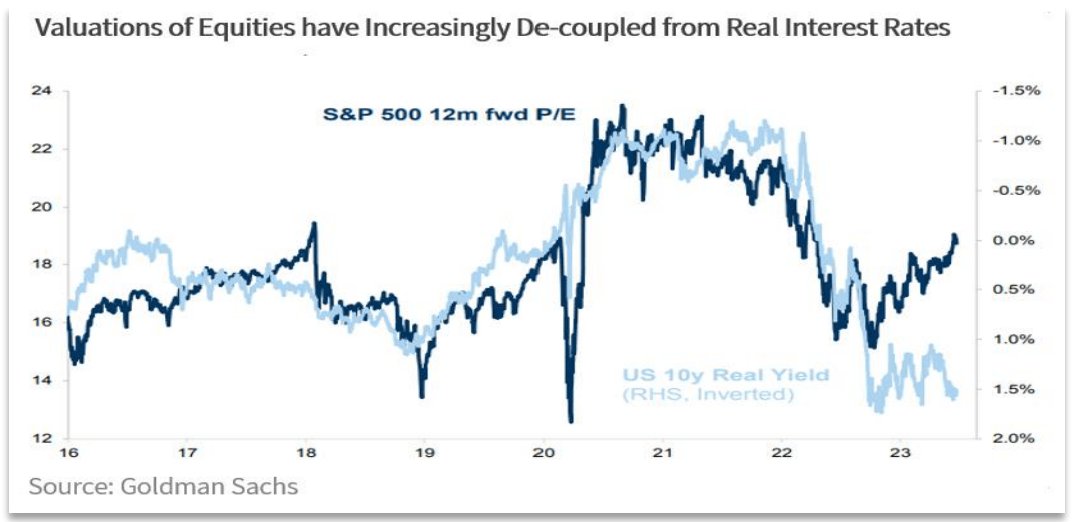

If the previous low-rate region encouraged leveraged risk-taking and general stupidity, the reversal of that regime should now push the pendulum back toward normalcy , as companies refocus on profitability and investors return to fundamentals. Valuations are unlikely to remain detached from interest rates for long (chart below). While there are always reasons to worry and risks on the horizon, for Broyhill, the return to fundamental investing is as exciting as it gets.

{kind=link}

The value locked within many of our core positions is now being recognized, but share prices remain far from our estimates. A number of our "legacy" businesses have proven more resilient than many venture-backed "disruptors" assumed. Our pipeline is as robust as it's been in years, and we have begun accumulating shares in several companies that we believe are incredibly mispriced.

A recession seems all but certain. The only question that remains, in our opinion, is the magnitude of the pending downturn. Accordingly, we remain conservatively positioned for the time being while still deploying capital to equities whose price already reflects more challenging times ahead. Otherwise, we stand ready to deploy capital more aggressively when additional opportunities present themselves.

We are grateful for your continued trust and partnership. We come into the office each day striving to earn it, and we realize just how fortunate we are to have such a wonderful group of like-minded, longterm investors who place their confidence in us. You enrich our network, strengthen our competitive advantage, and just make our work all the more enjoyable.

As always, please feel free to reach out at any time with questions. We enjoy hearing from you.

Sincerely,

Christopher R. Pavese, CFA

DISCLOSURESBroyhill Asset Management LLC ("BAM") is an investment adviser in North Carolina. BAM is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. BAM only transacts business in states in which it is properly registered or exempted from registration. A copy of BAM's current written disclosure brochure filed with the SEC which discusses among other things, BAM's business practices, services and fees is available through the SEC's website a t www.adviserinfo.sec.gov . Performance calculation methodology. The performance of the Broyhill Equity Portfolio illustrated here is representative of the fully invested strategies available through various TAMPs (Turnkey Asset Management Platforms). The majority of BAM's SMAs include a significant cash allocation, which has averaged 30% - 40% in recent years, and also utilize options to complement individual position sizing and to hedge the portfolio as appropriate for individual clients. As a result, we believe that the historical performance of our flagship strategy (which includes both options and a significant cash drag) is not representative of a pure equity allocation. As such, this data may be useful for an advisor evaluating Broyhill, although individual results may differ based on each account's investment objectives, the date of initial funding, the opportunity set available at the time, specific investment vehicles available to the accounts, and individual fee schedules. These historical performance figures are for our equity-only strategy. Performance is calculated using time-weighted rates of returns, net of fees. Since these platforms report returns to Broyhill gross of fees, in order to report net returns, a 1.5% annual management fee has been subtracted from gross reported returns. This methodology has also been applied to the extracted attribution returns. Average position size is calculated from average capital invested divided by average portfolio capital in fully invested accounts. The investment return and principal value of an investment will fluctuate. Therefore, an investor's account, when liquidated or redeemed, will almost always have a different value than that shown herein. Current performance may be lower or higher than return data quoted herein. Past performance is not indicative of future returns. This information should not be used as a general guide to investing or as a source of any specific investment recommendations and makes no implied or expressed recommendations concerning the manner in which an account should or would be handled, as appropriate investment strategies depend upon specific investment guidelines and objectives. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. This document contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this document will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. No representations, expressed or implied, are made as to the accuracy or completeness of such statements, estimates or projections, or with respect to any other materials herein. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the securities transactions or holdings discussed were or will prove to be profitable. There are risks associated with purchasing and selling securities and options thereon, including the risk that you could lose money. Certain information contained herein constitutes "forward-looking statements," which can be identified by the use of forward-looking terminology such as "may," "will," "should," "expect," "anticipate," "project," "estimate," "intend," "continue," or "believe," or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future. Market value information (including, without limitation, prices, exchange rates, accrued income and bond ratings furnished herein) has been obtained from sources that Broyhill believes to be reliable and is for the exclusive use of the client. Market prices are obtained from standard market pricing services or, in the case of less liquid securities, from brokers and market makers. Broyhill makes no representations, warranty or guarantee, express or implied, that any quoted value necessarily reflects the proceeds that may be received on the sale of a security. Changes in rates of exchange may have an adverse effect on the value of investments. Indices represent unmanaged, broad-based baskets of assets. They typically used as proxies for overall market's performances. Index returns typically assume that dividends are reinvested and do not include the effect of management fees or expenses. You cannot invest directly in an index. Without prior written permission of index owner, this information and any other index-related intellectual property may only be used for your internal use, may not be reproduced, or redistributed in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an "as is" basis, and the user of this information assumes the entire risk of any use made of this information. Neither the index owner nor any third party involved in or related to the computing or compiling of the data makes any express or implied warranties, representations or guarantees concerning the index-related data, and in no event will index owner or any third party have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) relating to any use of this information. For additional information about other indices or strategies mentioned here, you may contact us at ir@broyhillasset.com . No part of this material may be copied, photocopied, or duplicated in any form, by any means, or redistributed without Broyhill's prior written consent. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Broyhill Q2 2023 Letter