BKE - The Buckle: Our Reasons For Upgrading To 'Buy'

2023-07-25 00:48:11 ET

Summary

- Buckle, Inc., a US retailer of casual apparel, footwear, and accessories, has seen a 13% increase in stock price since our last writing in October 2022, underperforming the broader market.

- Despite a challenging macroeconomic environment, the company has maintained strong fundamentals, including profitability, efficiency, and liquidity.

- These strong fundamentals, and the improving macroeconomic environment are expected to positively impact sales, earnings, and margins, leading to an upgrade in rating from "hold" to "buy".

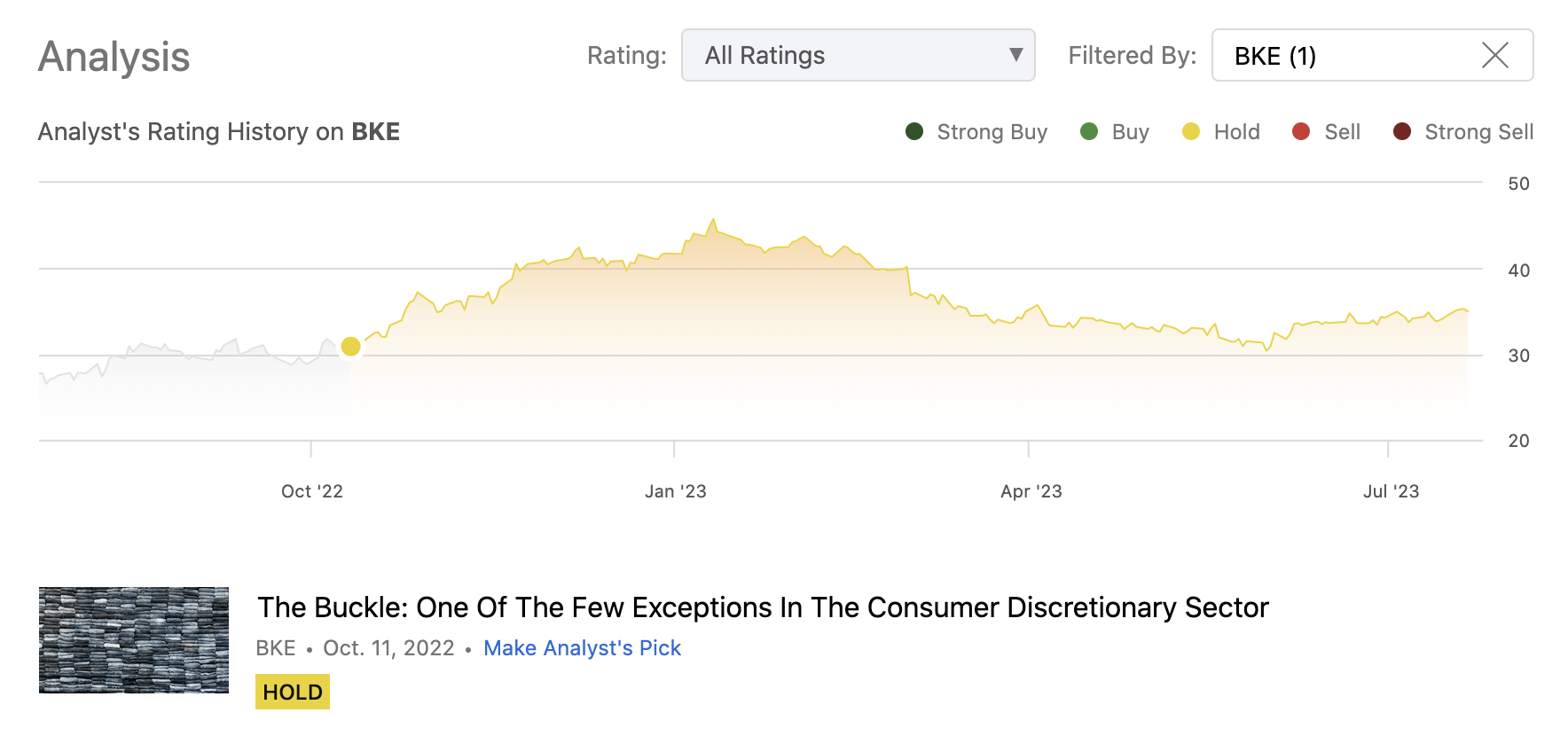

The Buckle, Inc. (BKE) operates as a retailer of casual apparel, footwear, and accessories for young men and women in the United States. We have started coverage on the firm in October 2022 with an initial "hold" rating.

{kind=link}

We have arrived at the neutral rating by discussing the firm's relatively strong financial performance, including sales and liquidity in 2022, despite the challenging macroeconomic environment, as well as the potential negative implications of the rising inventory levels and depressed consumer confidence levels.

Since our last writing BKE's stock price has increased by about 13%, underperforming the broader market, which has gained 26% in the same time frame.

Today, we will give an updated view on the macroeconomic factors that may have in impact on BKE's performance in the coming quarters, as well as on company specific metrics, in order to gauge whether BKE's stock could be an attractive stock to buy at the current price levels.

Macroeconomic environment

Consumer confidence

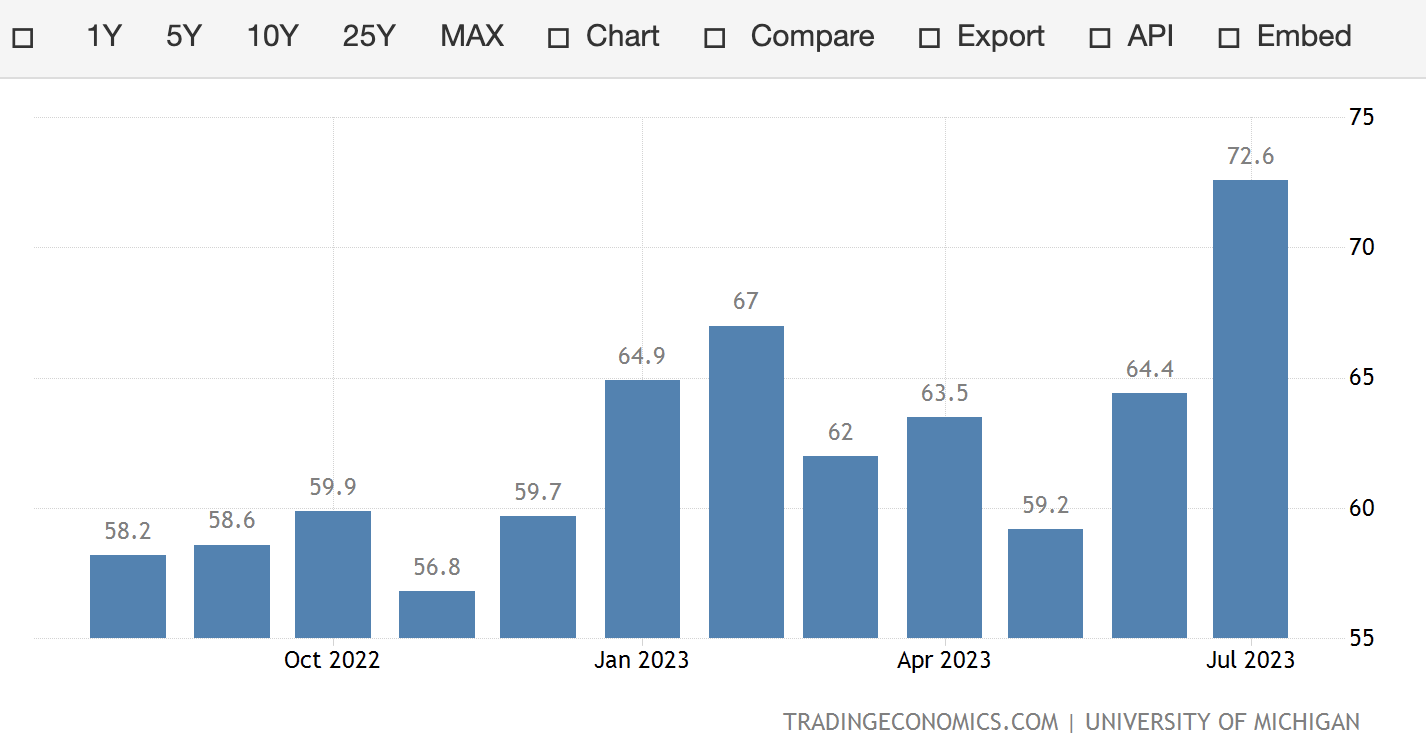

Consumer sentiment is often treated as a leading economic indicator, which can signal how the spending behaviour of the consumer may change in the near future. Higher consumer confidence, or better sentiment, indicates that people are less concerned about their financial outlook and about the overall state of the economy and therefore are more likely to spend on discretionary goods and services - just like the products that are also offered by BKE.

{kind=link}

We have raised our concerns in October 2022, as consumer confidence readings have reached historic lows. Since then the sentiment has substantially improved, indicating that consumer spending may accelerate in the near future, potentially positively impacting the demand for BKE's products.

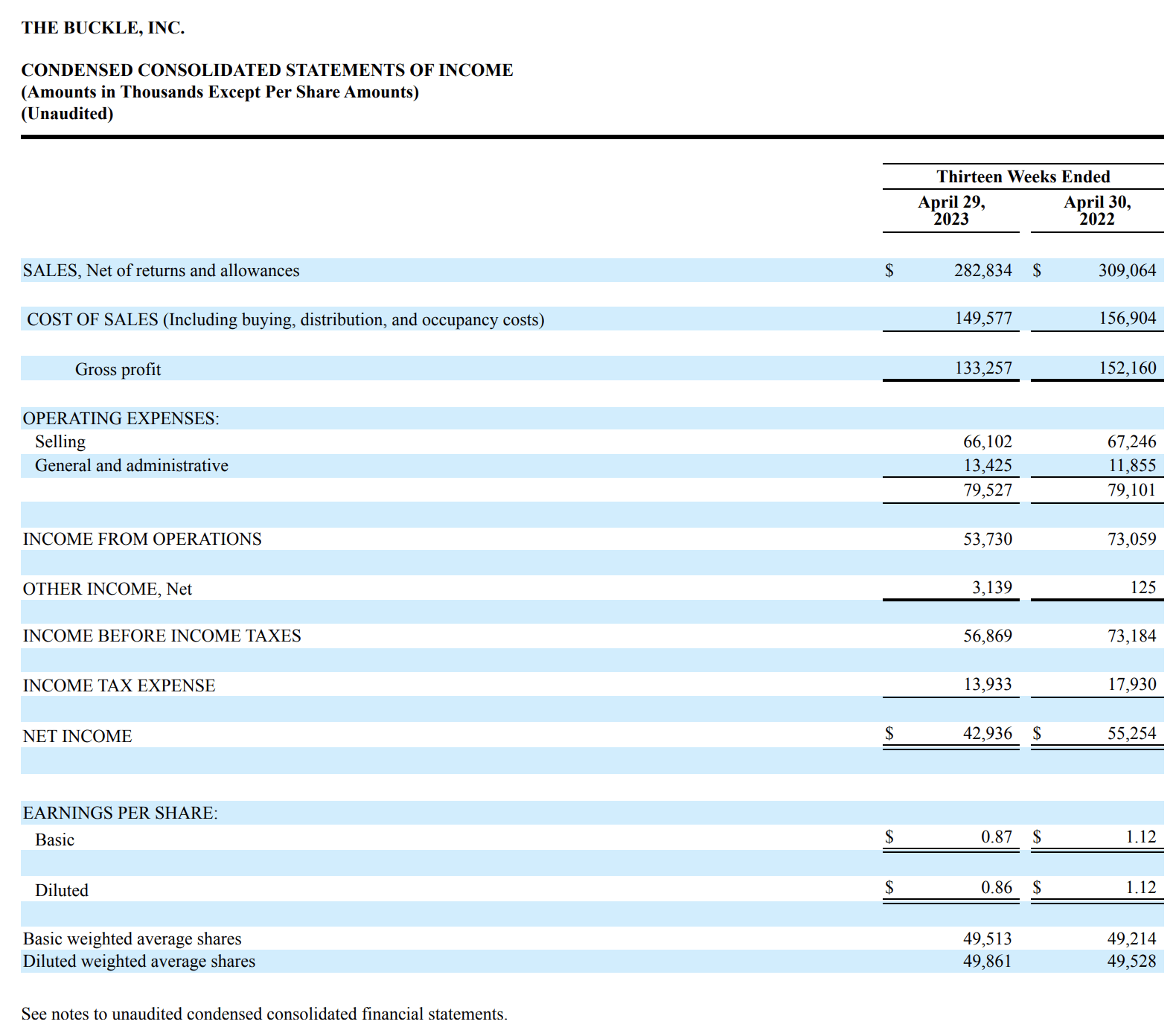

For this reason, we are much more optimistic about BKE's business going forward than we were in 2022. Bear in mind however that the improvement may come with a certain time lag. The Q1 results , both in terms of sales and earnings have been significantly lower than in 2022. The deteriorating results were explained in the financial statements as:

The reduction in total sales for the period was the result of a a 10.0% decrease in the number of transactions and a 0.6% decrease in the average unit retail, which were partially offset by a 2.3% increase in the average number of units sold per transaction.

The comparable sales decline has continued into June as well.

Q1 income statement (BKE)

{kind=link}

Inflation

while consumer confidence plays an important role on the demand and sales side of the equation, inflation plays a role on the cost side. High inflation rates normally lead to higher input costs, including raw materials, transportation etc., often leading to margin contractions, if the firm is not able to fully shift the cost increases to the customers.

{kind=link}

Since our last article, the core inflation rate in the United States has declined by about 1.5%, which is a material improvement. For this reason, we believe that in the coming quarters, BKE's business may experience some improvement in its margins as well. But let us dive a bit deeper into this topic by discussing how the firm's profitability has developed over the past years and what we expect going forward.

Company specific metrics

Profitability

To assess a company's profitability, investors and analysts often use the gross profit margin, the operating margin, and the net profit margin. The following chart shows these three metrics for the past five years.

We can see that despite the challenging macroeconomic environment and the numerous headwinds in the past years, BKE has managed to keep its margins constant. In 2023, however, we have seen a slight decline in the first quarter, but this may be attributed to a seasonal pattern, as Q1 margins appear to be narrower in each year.

The reasons for the Q1 margin contractions have been summarized by the firm:

- The current quarter gross margin decline was the result of 140 basis points of deleveraged buying, distribution, and occupancy expenses, along with a 70 basis point decline in merchandise margins.

- Selling, general, and administrative expenses were 28.1% of net sales for the first quarter of fiscal 2023, compared to 25.6% for the first quarter of fiscal 2022. The increase was the result of increases in store labor-related expenses (2.00%, as a percentage of net sales) and certain other expense categories (1.50%, as a percentage of net sales), which were partially offset by a reduction in expense related to incentive compensation accruals (1.00%, as a percentage of net sales).

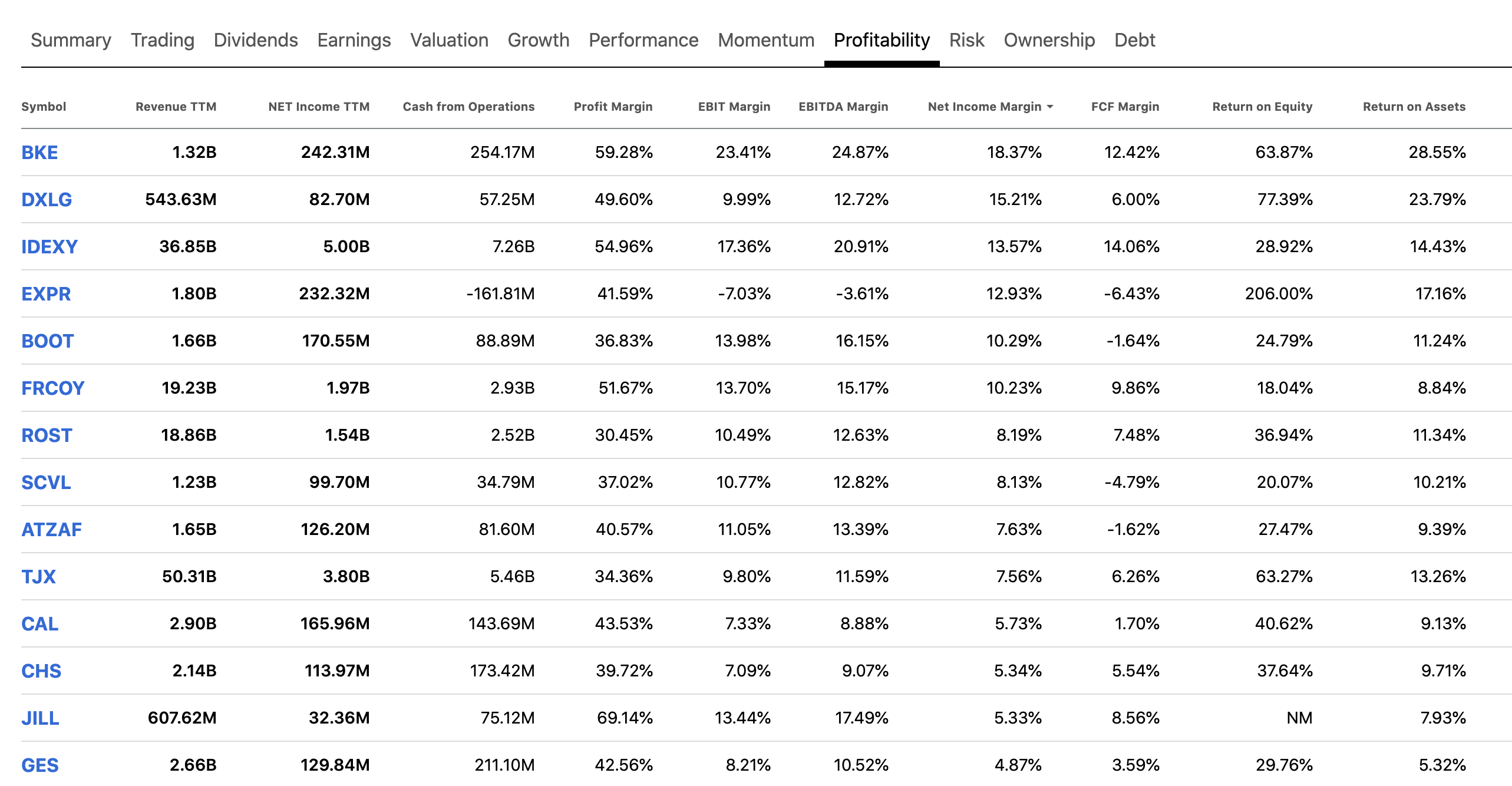

Even with the contraction in Q1 When ranking companies in the apparel retail industry by the net profit margin, BKE is on the top of the list.

{kind=link}

Looking forward, we believe that the moderating inflation levels will benefit BKE's business, as already highlighted above.

Also, in our previous article we have raised our concerns related to inventory management and inventory levels. Having excess inventory during times of low consumer confidence may lead to obsolescence. Getting rid of obsolete inventory may hurt the margins as deep discounts may need to be applied.

The chart above shows that BKE's inventory levels have fallen somewhat in Q4 2022, but have bounced back in Q1 2023. Just as before, we would like to see this figure falling further, until reaching its long-term average.

Efficiency

Asset turnover is one of the most popular ratios to assess a company's efficiency. The chart below shows that since the bottom in 2020, BKE's efficiency has been gradually increasing, almost reaching its pre-pandemic levels.

This development essentially shows that the firm has been able to utilize its assets more efficiently and able to generate more revenue per unit asset.

At this point, we generally like to take a look whether the sales figures may have been artificially inflated or not. In some cases firms use aggressive accounting practices and change revenue recognition practices in order to "pull demand forward" from future periods and show sustained demand across quarters. Such practices can be often recognized by comparing the growth of revenue to the growth of accounts receivable. If accounts receivable grow at a faster pace, revenue manipulation may be a concern. Fortunately, this is not the case with BKE, as the following chart indicates.

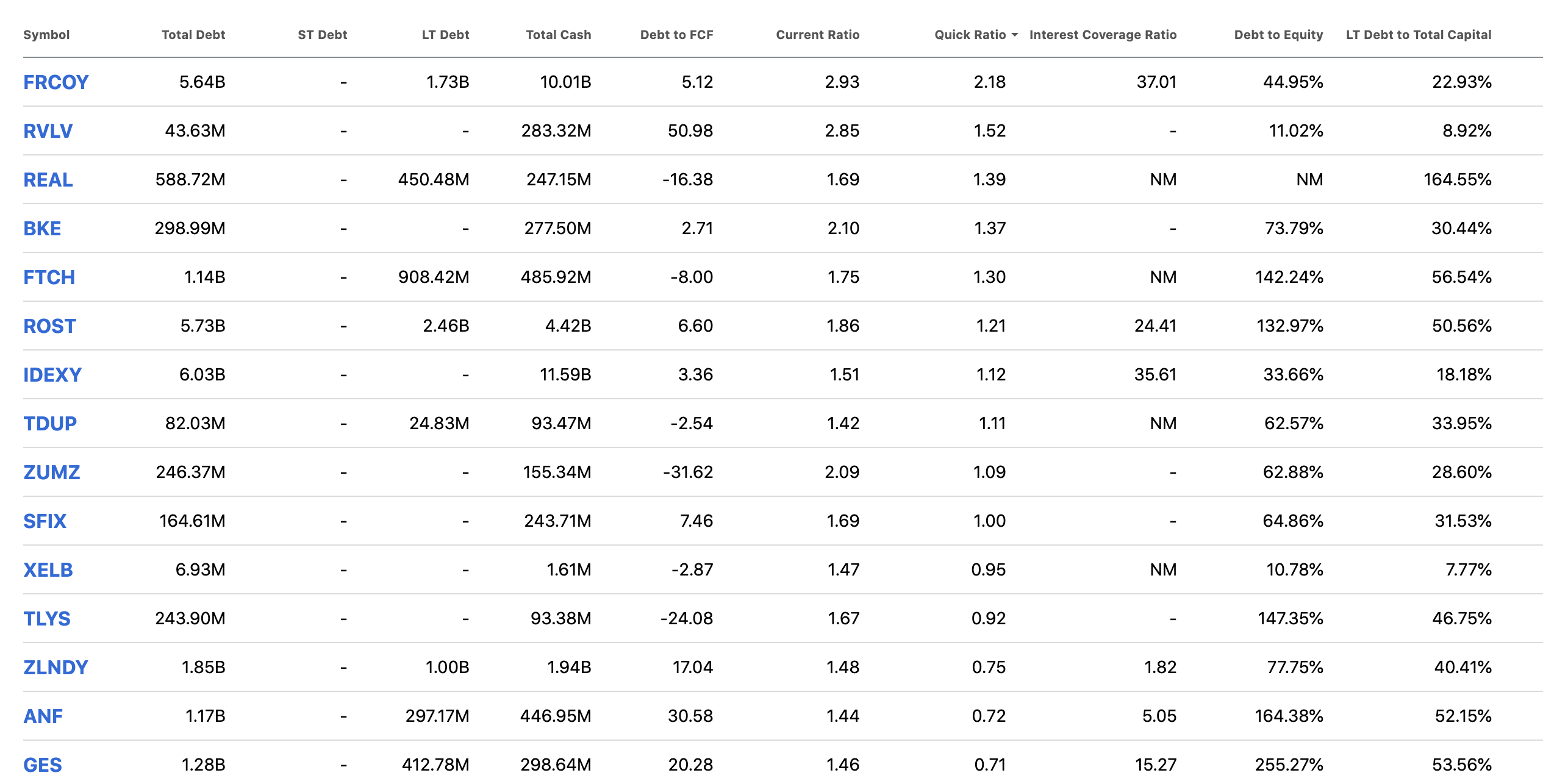

Liquidity

In October 2022, we have highlighted that BKE is well-positioned from a liquidity point of view to manage potential downturns.

Also, as of now, both the current- and the quick ratio are above one, indicating that the current assets, even without considering inventory, are sufficient to cover current liabilities.

To put these figures into perspective, the following table shows several of BKE's peers from the apparel retail industry. Clearly, BKE compares relatively favourably to most of them.

{kind=link}

To sum up

In the previous quarter, BKE's sales have fallen and its margins have contracted. Despite these developments however, BKE remains the highest net margin player in the apparel retail industry.

The firm has also managed to maintain its strong liquidity position and improve its efficiency since our last article.

Looking forward, the improving macroeconomic environment is likely to positively impact BKE's sales and earnings figures as well as its margins.

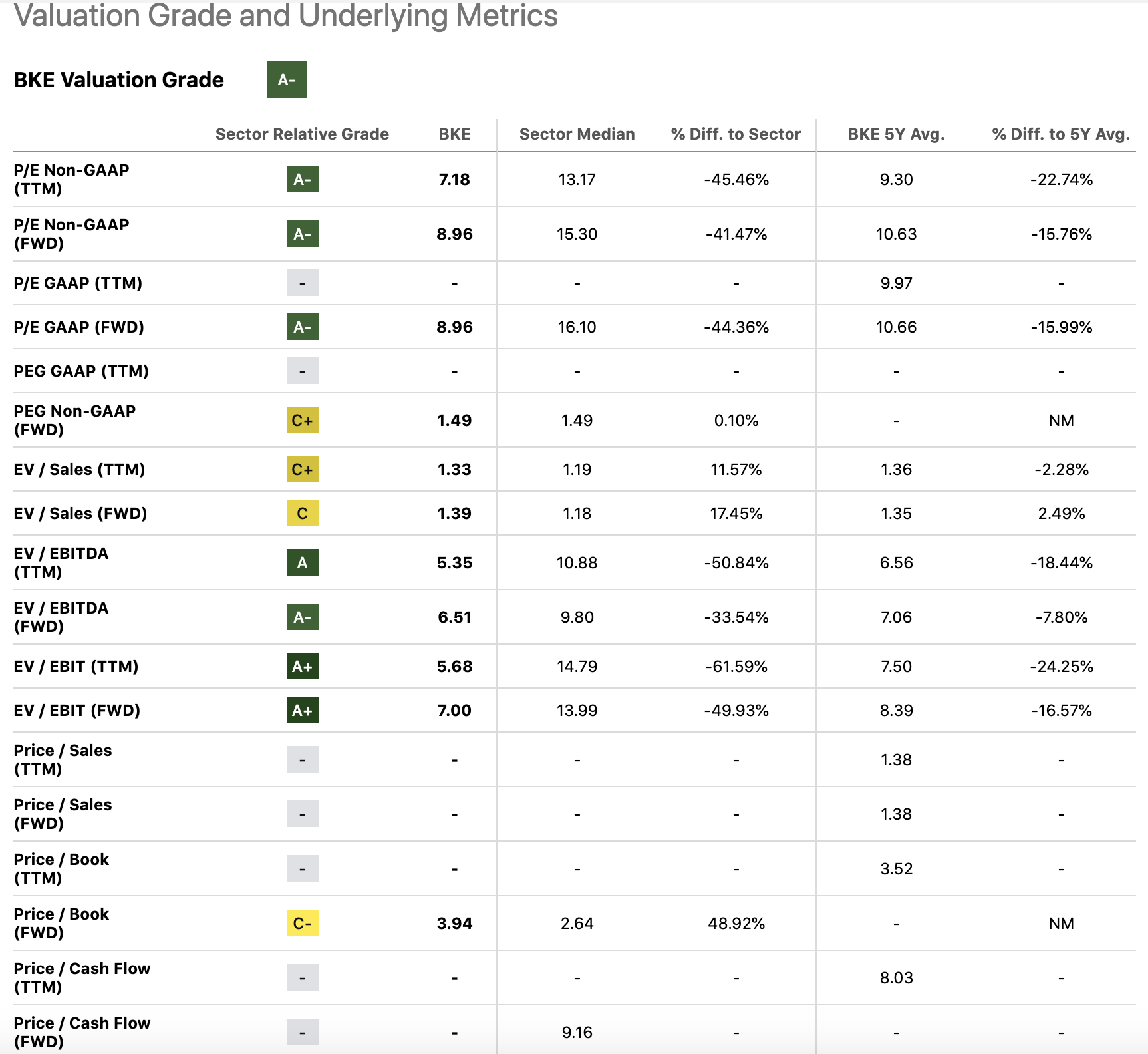

At the same time, BKE is selling at a significant discount compared to the sector median and also compared to its 5Y averages, according to a set of traditional price multiples.

{kind=link}

For these reasons, we upgrade our rating from "hold" to "buy".

For further details see:

The Buckle: Our Reasons For Upgrading To 'Buy'