BKE - The Buckle: Patience Required

2023-10-21 09:52:00 ET

Summary

- Buckle's recent results show a decline in revenue and comp sales, with a negative outlook for Q3 and potentially Q4 as well, given recent sales trends.

- Unfortunately, the macro environment is worsening, with inflation, rising costs, and lower personal savings rates affecting consumer discretionary spending, and BKE unable to buck this trend so far.

- In this update, we'll look at the recent results, the stock's updated valuation, and whether the stock might offer enough of a margin of safety.

Just over 18 months ago, I wrote on Buckle ( BKE ), noting that the stock's attractive dividend yield (plus regular special dividends) would make the stock an attractive buy below $32.20. This turned out to be a very poor call as the stock continued to slide over the next months to a low of $26.50 per share before finally finding its bottom. And while the stock has delivered a positive return since then, including dividends, it has barely beat the S&P 500 ( SPY ) which is roughly flat in the period. Since then, the macro outlook has worsened, the stock has made another low high since Q4 2021, and it's hard to rule out further downside after weak September sales. In this update, we'll look at the recent results, the Q3 outlook & where the updated low-risk buy zone for the stock sits.

Recent Results & H2 Outlook

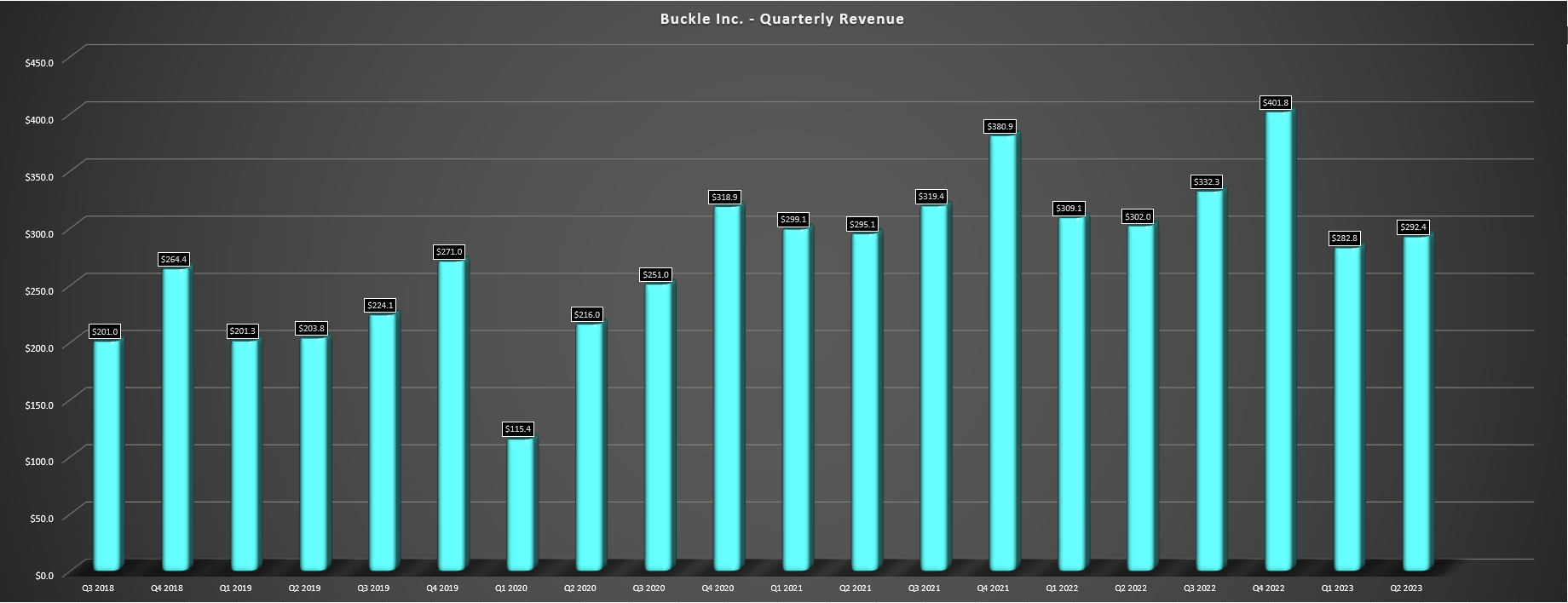

Buckle released its Q2 results in late August, reporting quarterly revenue of $292.4 million, a 3% decline year-over-year. This sharp decline was driven by a 3.3% comp sales decline, and year-to-date results have come in below my expectations as well, with comp sales down 6.3% year-over-year, and H1 sales down ~6% to ~$575 million. Digging into the results a little closer, the company noted that women's denims benefited from strength in private label, softness in branded styles offset this private label boost (related to planned inventory decreases). Meanwhile, sales in tops struggled because of an inability to source enough newness, and its women's business was further affected by a delayed start to the spring season that hurt sales in open-toe and sandals.

Buckle - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Moving over to men's, the results were better, with growth in denim and tops. However, footwear sales came in below expectations in a more competitive environment, and the company noted that footwear sales were down 13.5% year-over-year across combined categories vs. accessories, which were a standout, up 3.5%. This was consistent with the trend we saw in Q4 2022 and Q1 2023 (footwear down vs. accessories up). Unfortunately, since the sluggish Q2 with lower sales, trends don't appear to be improving, suggesting another soft quarter in Q3 and potentially Q4. The evidence of this is in the company's comp sales of [-] 5.0% and [-] 11.1% in August and September, respectively, a deceleration from [-] 3% in Q2.

Finally, looking at SG&A and margins, SG&A came in at 27.9%, up 150 basis points year-over-year with higher store labor expenses, higher G&A and higher marketing as a percentage of sales. Meanwhile, operating margins sunk to 19.2% year-to-date vs. 22.7%, and merchandise margin was down 30 basis points as well. The result of the lower sales and margin compression was that adjusted earnings per share fell 9% year-over-year to $0.92, and annual EPS looks like it will be down at least 15% year-over-year to $4.25 (FY2022: $5.13), representing its second consecutive annual decline after a massive year in FY2021. That said, the company has seen strong growth vs. pre-pandemic levels, and even if down to $4.25 this year, annual EPS will still be up over 90% from FY2019.

Macro Outlook & Sector-Wide Trends

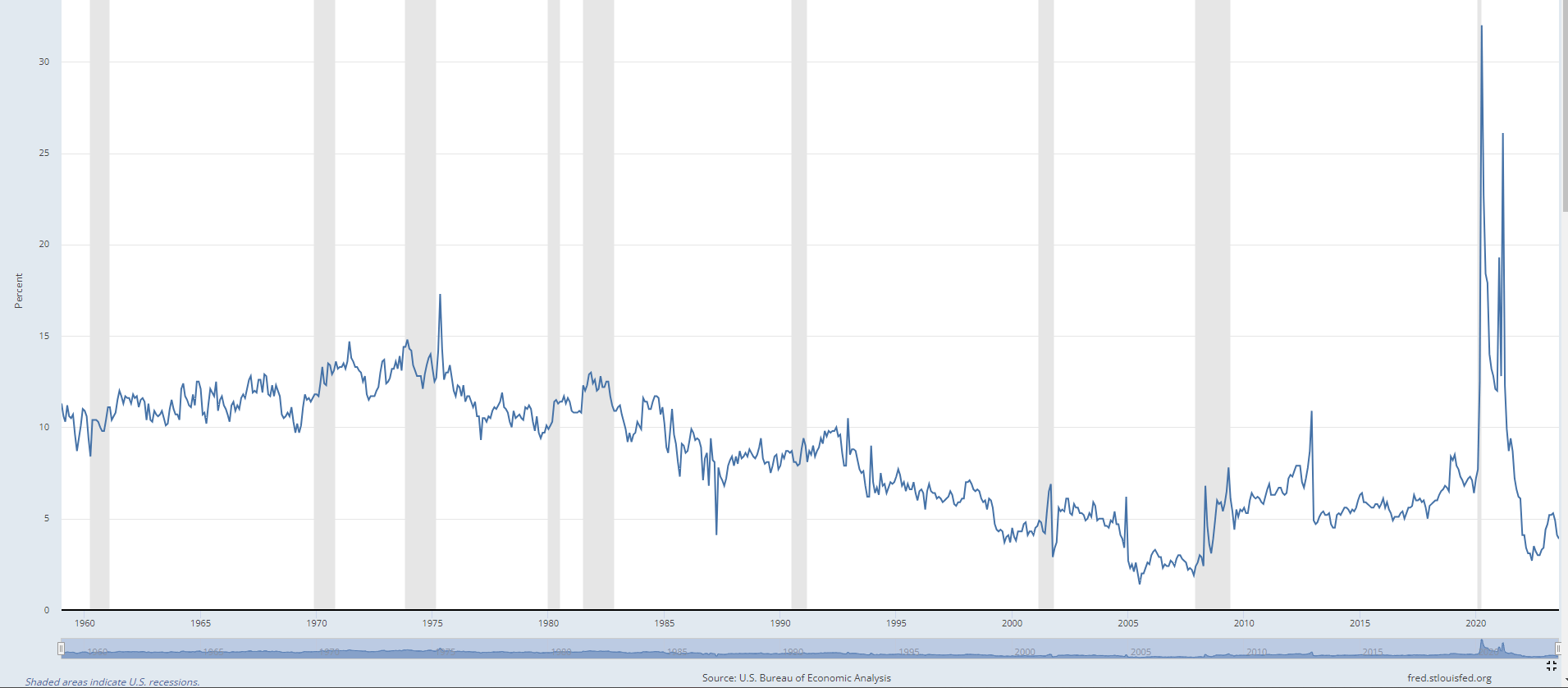

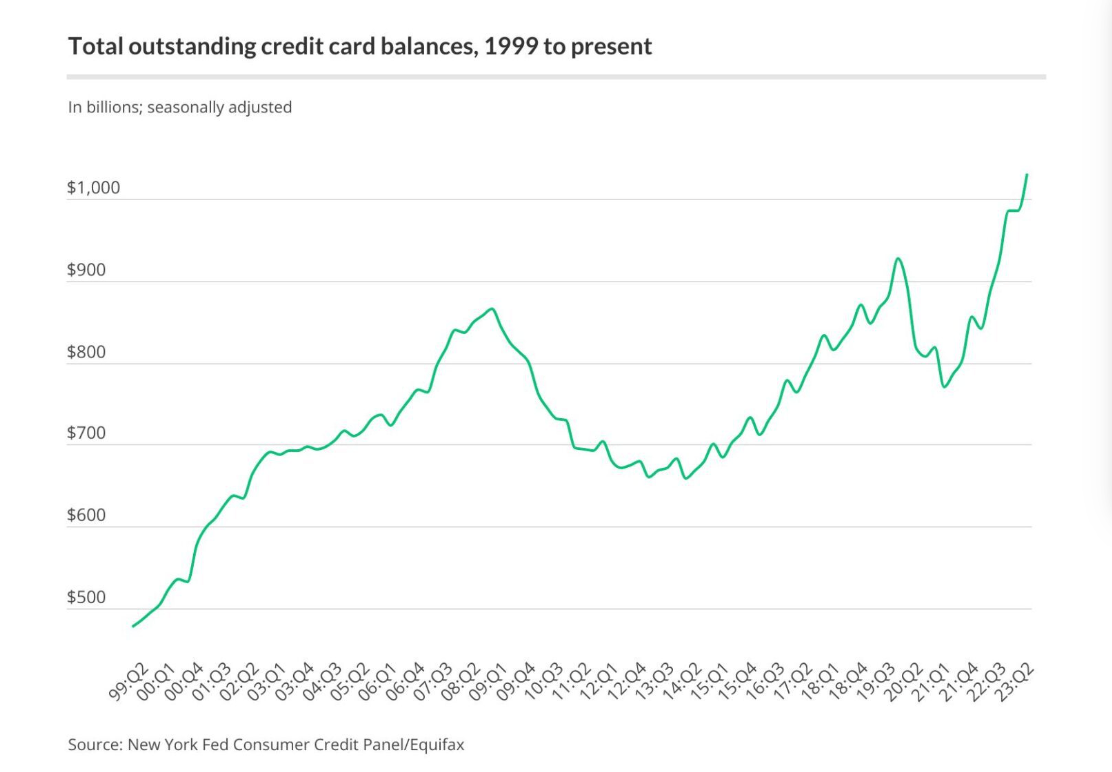

As for the macro environment, it's certainly not improving, and although Buckle's sales came in weaker than I expected, it can only control so much. However, it's not ideal to see things arguably worsening, with sticky grocery and utilities inflation and rising mortgage/rent costs contributing to lower personal savings rates, which have continued to trend down. This will continue to affect discretionary spending for consumers, and it certainly doesn't help that student loan repayments have restarted, which could impact some of Buckle's younger consumers as well. Plus, as shown below, outstanding credit card balances have hit new all-time highs, suggesting that consumers may be finally getting tapped out, and that isn't a great setup when money needs to be set aside for what's always an expensive holiday season, setting up what could be a rough hangover and Q1 for retail sales in January/February.

US Personal Savings Rate - FRED, BLS Credit Card Balances United States - LendingTree.com

{kind=link}

{kind=link}

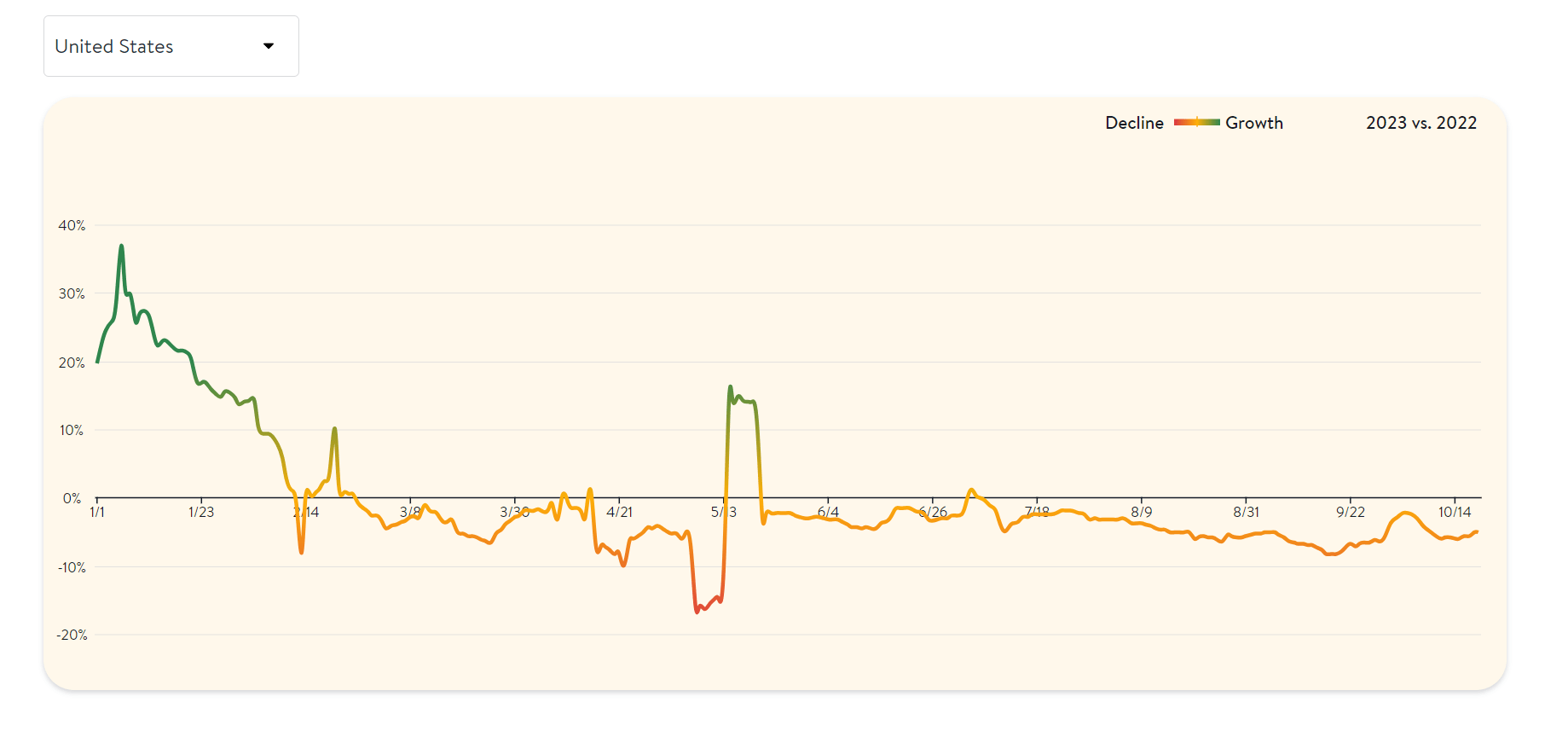

Meanwhile, although restaurant traffic may not be directly correlated to foot traffic and spending in apparel retail stores, it's not ideal to see large operators like Darden ( DRI ) discussing early signs of some trading down, and it's certainly not ideal to see a continued deceleration in traffic for restaurants based on seated diners according to OpenTable. In fact, restaurant industry traffic has decelerated meaningfully since July, with August and September traffic down sharply industry-wide, and October traffic off to a slow start as well. Finally, quick-service traffic also fell sharply in September logging its worst month year-to-date, suggesting that even trade-down beneficiaries like quick-service and fast-casual are seeing negative traffic, which was previously a sanctuary among a period of slowing casual dining sales. And given this backdrop, it's hard to be optimistic about retail names beating top and bottom line estimates as we head into Q3 and what could be a promotional holiday season in Q4 as some retailers look to win sales.

United States Seated Diners - OpenTable

{kind=link}

Overall, this setup does not inspire much confidence for owning Buckle, and it could be difficult for the company to meet Q3 revenue estimates of $318 million and $0.99 in quarterly EPS, respectively. Plus, these estimates are already implying a 4%+ decline year-over-year in sales. Given Buckle's solid execution over the years and strong track record, I would normally prefer to ignore the short-term noise and focus on the bigger picture. However, this strategy only makes sense if there's a high level of confidence that a margin of safety is already available in the stock. And with BKE up 17% off its recent lows and trading at a reasonable valuation, but not what I would extreme, I don't see enough of a margin of safety just yet to justify jumping in the stock ahead of Q3 Earnings where there's a greater risk of a miss than a beat.

Valuation

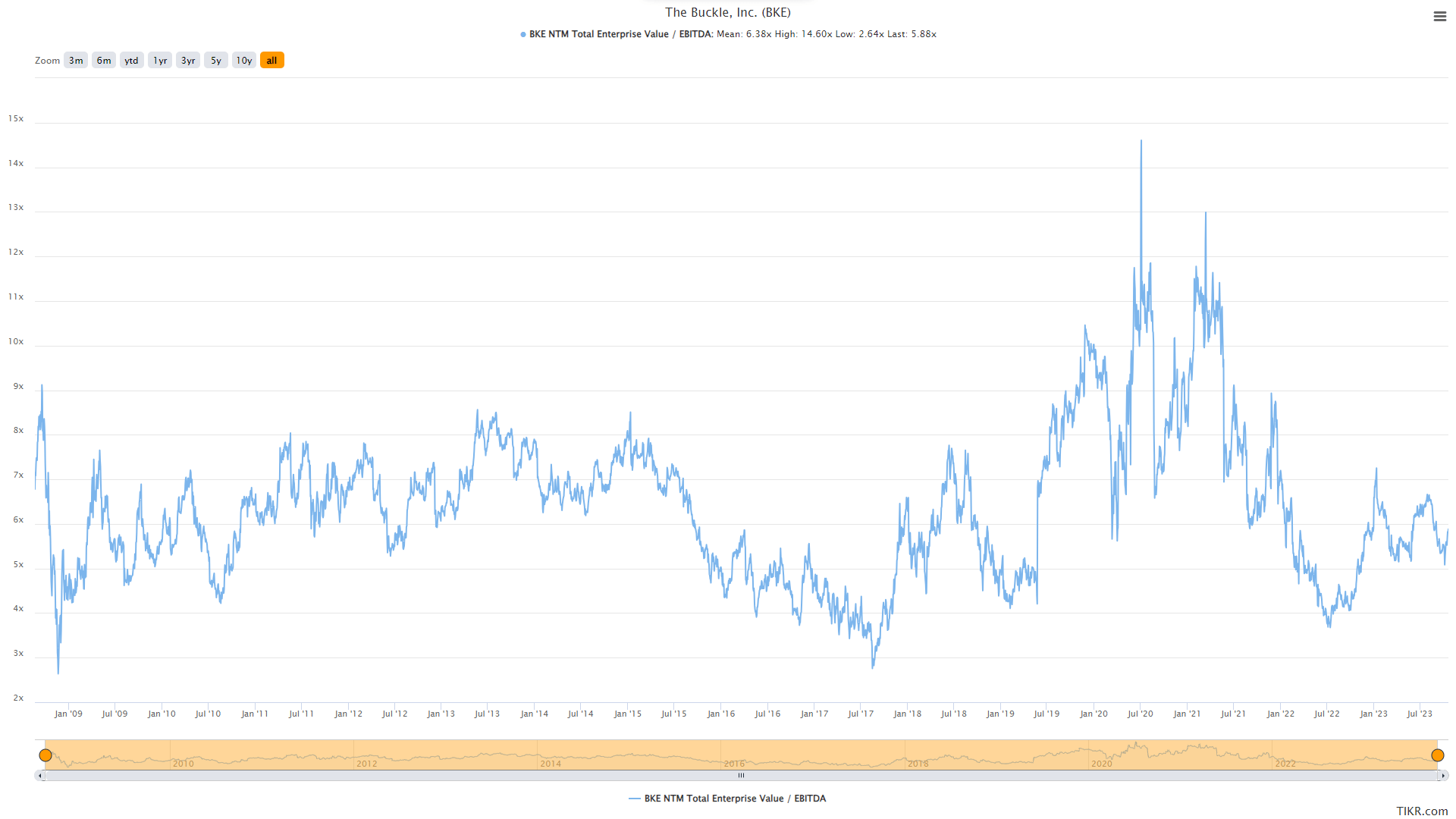

Based on ~50.4 million shares and a share price of $35.50, Buckle trades at a market cap of ~$1.79 billion and an enterprise value of ~$1.75 billion, making it one of the lower capitalization names in the Apparel industry group behind others like Boot Barn ( BOOT ), Abercrombie & Fitch ( ANF ), and Urban Outfitters ( URBN ). However, among the group it's arguably the most undervalued, trading at just ~5.5x FY2024 EV/EBITDA estimates vs. BOOT at ~9.5x, ANF at ~6.8x, and URBN at ~6.6x, respectively. And while Boot Barn should command some premium (given that much of its assortment can be designated as functional) and Buckle came off a tough quarter relative to ANF, BKE's valuation is becoming much more reasonable.

BKE EV/EBITDA Multiple - TIKR.com

{kind=link}

Using what I believe to be a conservative multiple of 6.5x EV/EBITDA (just above its 10-year average), given that it's a lower-growth name in the space, I see a fair value for the stock of $40.50, pointing to a 14% upside from current levels or a ~20%+ total return when including its dividend yield and historical special dividends. However, while this might appeal to some investors, I am looking for a minimum 30% discount to fair value when it comes to small-cap stocks to ensure a margin of safety even when factoring in expected distributions to shareholders. And if we apply this discount to BKE's estimated fair value of $40.50, the stock's ideal buy zone would come in at $28.40 or lower, well below current levels. Hence, I don't see any reason to chase the stock here after what's been a sharp rally, and it's hard to rule out a pullback to fill the gap left in the chart last summer (July 15th) at $27.55.

Summary

Buckle has had a disappointing H1 (in line with most of the industry) and its September sales have been no better, with comp sales decelerating by over 600 basis points from August to September and year-to-date comp sales sitting deeply in negative territory. On the positive side, some of this weakness looks priced into the stock at less than 7.0x EV/EBITDA. However, given the tough environment and multiple compression we've seen because of higher rates, I think investors should demand a higher hurdle for investment, and especially in names that haven't been able to buck the trend year-to-date. To summarize, I think there are more attractive bets elsewhere in the market today, and I would only get interested in BKE at a price of $28.40 or lower.

For further details see:

The Buckle: Patience Required