BKE - The Buckle: Profitability King With Hints Of Value

2023-09-20 05:29:04 ET

Summary

- The Buckle’s niche approach, targeting mid-sized markets and people interested in fashion, positions the business well for positive growth, even if its competitive position is being eroded.

- We do think the risk of margins stepping down and growth being flat is elevated, but with such a substantial yield, investors can ride strong returns into the medium term.

- Analysts are forecasting EBITDA-M to remain in excess of 20% into FY27F, which implies an FCF yield over >10% for the next 4 years at least based on today’s share.

- The downside risk is somewhat protected due to the substantial discount it is already trading at relative to peers. Any lower and the business could get takeover.

Investment thesis

Our current investment thesis is:

- The Buckle’s niche approach, targeting mid-sized markets and people interested in fashion, positions the business well for positive growth, even if its competitive position is being eroded.

- We do think the risk of margins stepping down and growth being flat is elevated, but with such a substantial yield, investors can ride strong returns into the medium term.

- Analysts are forecasting EBITDA-M to remain in excess of 20% into FY27F, which implies a FCF yield over >10% for the next 4 years at least based on today’s share price.

- The downside risk is somewhat protected due to the substantial discount it is already trading at relative to peers. Any lower and the business could get takeover.

Company description

The Buckle, Inc., ( BKE ) is a specialty retailer of casual apparel, footwear, and accessories for young men and women. Headquartered in Kearney, Nebraska, The Buckle operates over 400 retail stores across the United States. The company was founded in 1948 and has established a strong presence in the fashion retail industry.

Share price

Buckle’s share price performance has been disappointing, losing over 30% of its value while the wider market has performed exceptionally well. This has been partially offset by strong distributions, although not to an insufficient level. The decline is a reflection of its mild financial development and change in industry dynamics.

Financial analysis

{kind=link}

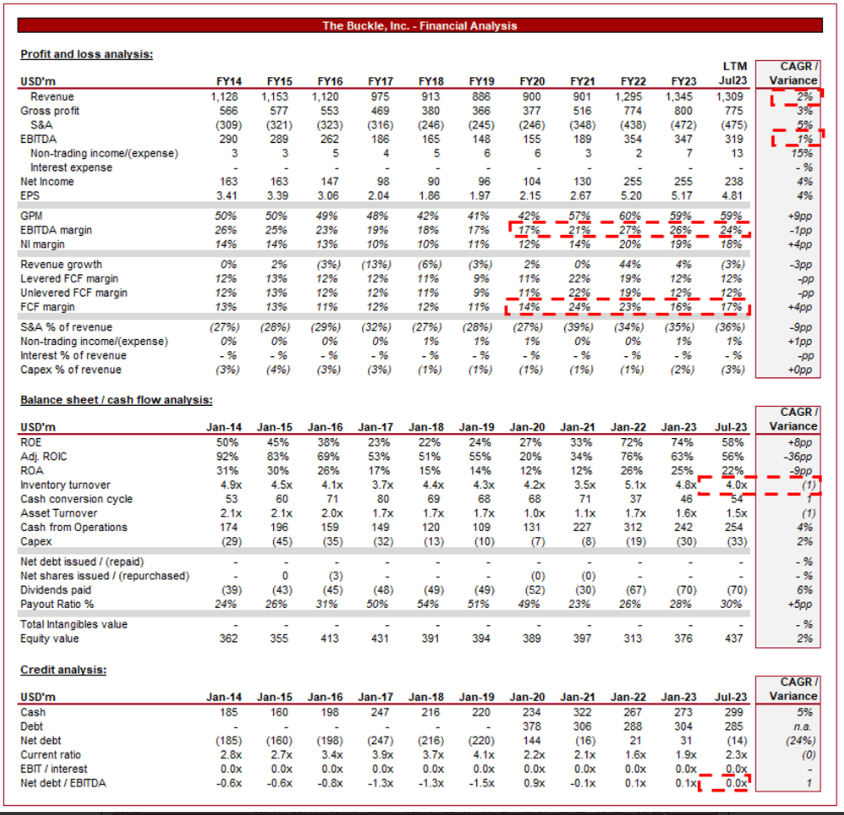

Presented above are Buckle's financial results.

Revenue & Commercial Factors

Buckle’s revenue growth has been underwhelming, with a CAGR of 2% into the LTM. YoY growth reflects the changing conditions faced by the business, with 3 fiscal years of negative growth and 2 at 0%.

Business Model

Buckle offers a curated selection of trendy and popular apparel and accessories, primarily targeting a younger demographic. It carries a mix of branded and private-label merchandise. The private-label segment is possible due to the

The company places a strong emphasis on customer service and engagement. It employs a personalized approach to sales, with store employees encouraged to build relationships with customers, provide styling advice, and enhance the overall shopping experience.

Buckle strategically selects store locations in high-traffic shopping centers and malls, often in smaller to mid-sized markets. This allows it to avoid the intense competition seen in larger urban areas (from large national and international chains) and build a loyal customer base in its chosen locations. In combination with its broad array of brands and products, Buckle provides a compelling proposition to these mid-sized markets.

Buckle has developed a portfolio of private-label brands like BKE and Daytrip has been a strong strategic decision, facilitated by strong brand development and relationships created with customers. This allows the company to achieve superior margins to retailing, while benefiting from cross-marketing (consumers looking for branded goods and discovering its own).

The company employs an inventory management system that allows it to respond quickly to changing fashion trends. The company is flexible with new designs, allowing it to update products and respond to differing demand levels among products.

Buckle has developed a respectable online presence, offering a user-friendly website and an e-commerce platform. This has allowed it to tap into the growing trend of online shopping and expand its customer reach beyond physical store locations. In combination with its physical locations, Buckle employs an omnichannel approach, a mildly competitive response to the e-commerce wave. The issue is that we think the company is likely too late. E-commerce is one of the primary reasons for the company’s growth slowdown we feel, as consumers have significantly more choice and the industry has seen a raft of new entrants that are e-commerce only.

Retail Industry

The Buckle faces competition from various retailers in the fashion industry, including department stores, specialty apparel stores, and e-commerce companies. Key competitors may include companies like American Eagle Outfitters ( AEO ), Abercrombie & Fitch ( ANF ), H&M ( HNNMY ), and Zara ( IDEXY ).

There are several key characteristics / trends currently impacting the apparel and retail industry:

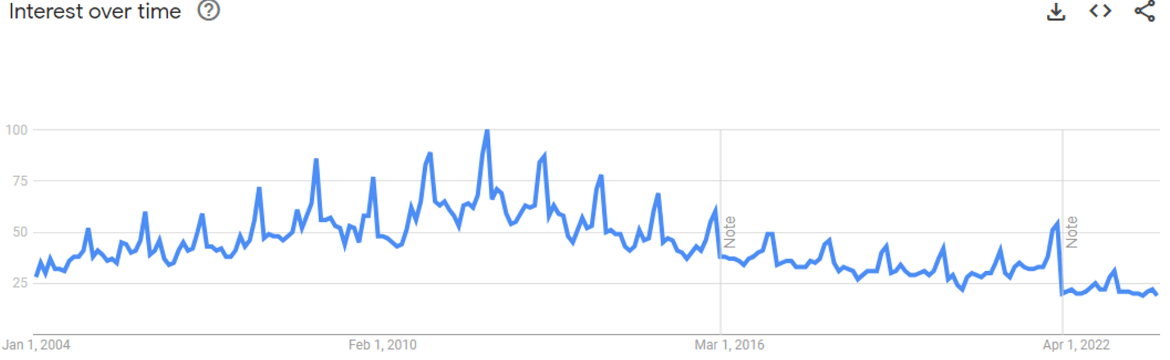

- Consumer Spending Trends - Consumer spending patterns, particularly in the apparel and fashion segment, play a significant role in the industry. The industry is highly sensitive to changing fashion trends, contributing to interest volatility over time, and significantly increasing risk. Staying on top of the latest styles and offering trendy products is crucial to achieving consistent growth. As the following illustrates, Buckle’s interest has consistently declined since c.2010, reflecting an inability to respond to trends.

{kind=link}

- Demographic Changes - Changes in the demographic composition of the population, including shifts in age groups, income levels, and cultural diversity, are threatening Buckle’s growth trajectory. The lack of new store locations reflects a weaker target demographic, limiting its ability to identify expansion locations.

- Competition - The retail industry, including specialty retail, is intensely competitive. We believe the rise of e-commerce and fast-fashion brands (working in unison) has contributed to a steep deterioration in Buckle’s competitive positioning. Buckle’s value proposition is far lower, as its current demographic can access greater choice, much of which is priced more attractively. We have not seen a sufficient response from Management to expect an improvement.

- Pandemic Effects - The COVID-19 pandemic highlighted the vulnerability of the retail industry to unforeseen disruptions from a supply chain perspective. However, it also provided a lifeline to many companies following a stimulus checked-fueled spending spree. Buckle has benefited materially from this, accelerating beyond its FY14 level following a number of years of decline. The risk is that with this impact unwinding, the business returns to a negative growth situation.

Competitive Positioning

We consider the following factors to be Buckle’s key competitive advantages:

- Targeted Market - Buckle has focused on catering to a niche market segment, focusing on fashion-conscious young adults. Although this limits the potential for explosive growth by targeting the mainstream, it has allowed the business to develop a strong brand.

- Regional Focus - The company has chosen to focus on smaller to mid-sized markets, which may have less growth potential compared to larger metropolitan areas. This said, it allows the company to capture a far larger portion of the market, with reduced competition.

- Choice - Buckle provides consumers with access to a range of brands, including Ray-Ban, Wrangler, Dr Martens, Levi, Hey Dude, and Oakley. Given the Regional Focus, Buckle is one of the few providers of these brands to many of its markets.

- Private Label - Its quality suite of private-label products resonates well with consumers, contributing to strong demand and more loyal customers. With purely retailing, consumers have little reason for loyalty given they are chasing the most affordable product (which is the same among all retailers). Whereas Buckle provides its own brands for consumers to also shop for.

Economic & External Consideration

Buckle is currently being negatively impacted by economic conditions, with an extended period of high inflation and elevated interest rates contributing to reduced discretionary spending. The impact of this will likely be felt for an extended period, as consumers sure up finances. This is exacerbated by Buckle’s core demographic, which is disproportionately exposed to current conditions.

Buckle’s recent quarterly results are summarized as follows:

- Successive quarters of negative revenue growth (-8.5% and -3.2%), with weakness across both stores and e-commerce. This is a reflection of softer discretionary spending, offset marginally by positive pricing action contributing to an increase in average sales value.

- Significant margin erosion at a GPM level (GPM falling to 58% and 57% in the last 2 quarters), due to an accumulation of stock and increased discounting activities.

- During the L26W period, 2 stores were opened, 3 closed, and 10 remodeled. This is a concern for growth as it implies Management is afraid of medium-term growth and thus has not been seeking new locations or does not broadly see locations where demand is sufficient. This follows on from prior periods of similar lackluster expansion.

Margins

{kind=link}

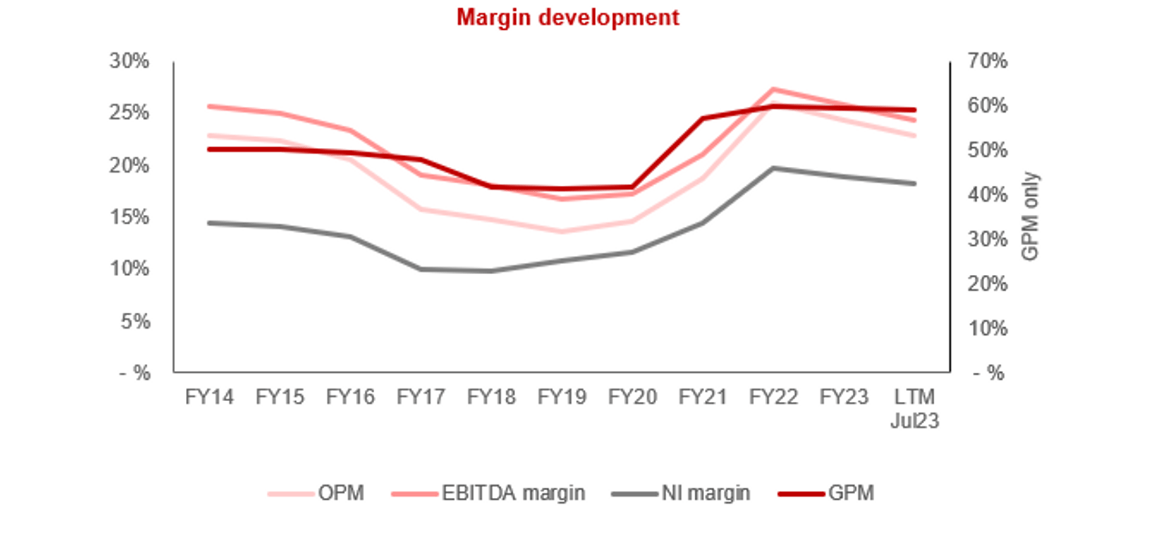

Despite the changing competitive landscape, Buckle has done a good job of maintaining its margins. Credit should be given to Management for not foregoing margins to chase revenue growth, allowing for broadly flat results. GPM has developed well, as operational efficiencies and strategic supply chain management have allowed for declining costs. This has been reinvested into S&A spending.

Given the industry’s competitive landscape and lack of commercial development, we worry that its current margins are not sustainable. There has already been significant erosion in the LTM period, with our view being more is to come. This could mean the business normalizes at an EBITDA-M of around c.20%.

Balance sheet & Cash Flows

Buckle’s inventory turnover has declined in the most recent quarter, suggesting the revenue slowdown is beyond Management’s expectations. This implies more difficulty before things get better, with more pressure to discount goods.

Buckle’s strong profitability translates to FCF, allowing the business to utilize no debt and accumulate cash while paying strong dividends. Even with slow growth and the potential for margin erosion, we believe its strong yield will remain and the company could easily grow distributions if desired.

We would like to see some cash utilized to acquire brands, as this has the potential to improve its future trajectory. It has a strong retail footprint and lucrative customer base and so the ability to immediately enhance small brands is clear.

Outlook

{kind=link}

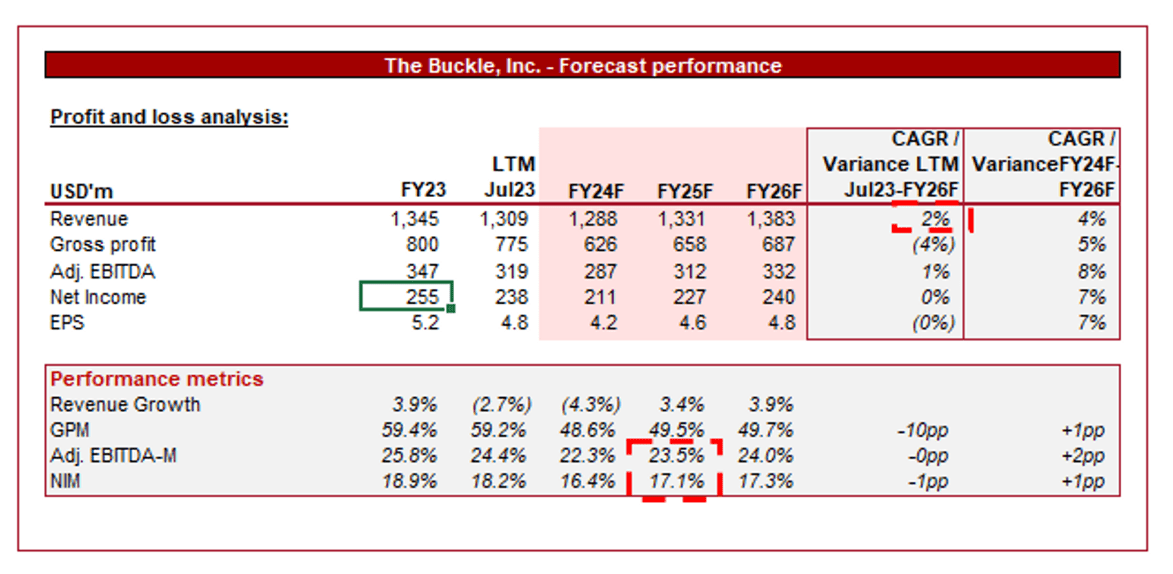

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of its modest growth, with a CAGR of 2% into FY26F. In conjunction with this, margins are expected to incrementally soften.

The growth forecast aligns with our view, as we struggle to see any material improvements to the business that can drive commercial improvement. Buckle will continue to face strong competition, contributing to struggles with achieving growth in excess of inflation.

Margin expectations are equally reasonable, primarily due to the lack of response to competitive threats, leading to an erosion of its competitive positioning.

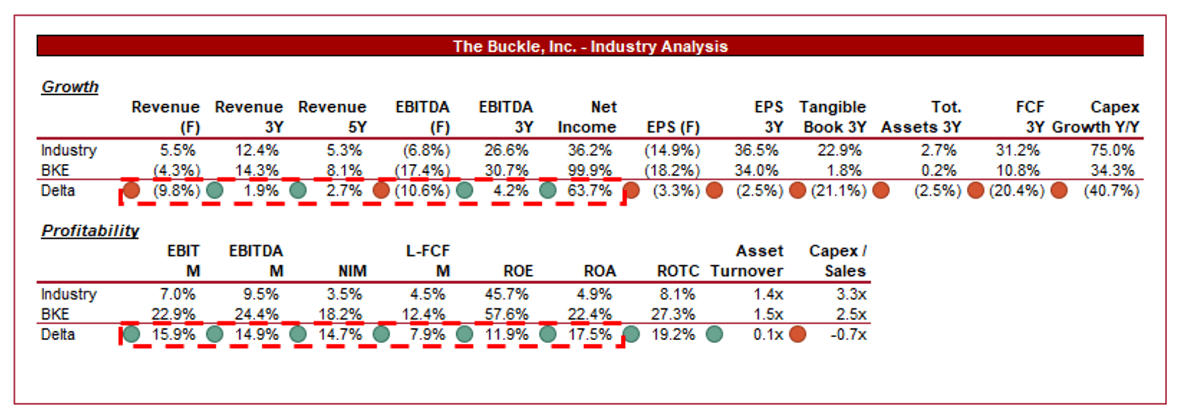

Industry analysis

{kind=link}

Presented above is a comparison of Buckle's growth and profitability to the average of its industry, as defined by Seeking Alpha (31 companies).

Buckle performs well relative to its peers. The company’s revenue growth is comparable, although its profitability development has been less impressive. The expectation is for current conditions to impact the company to a greater degree, which we consider reasonable given its target market is more susceptible.

Buckle’s key strength is its margins, with a substantial premium to the industry average. This is incredibly impressive and slightly unbelievable given the level of competition within the industry and its general characteristics. Its focus on mid-sized cities has potentially insulated it from a degree of competition. Even with the threat of margin erosion, the business will inevitably be a leader.

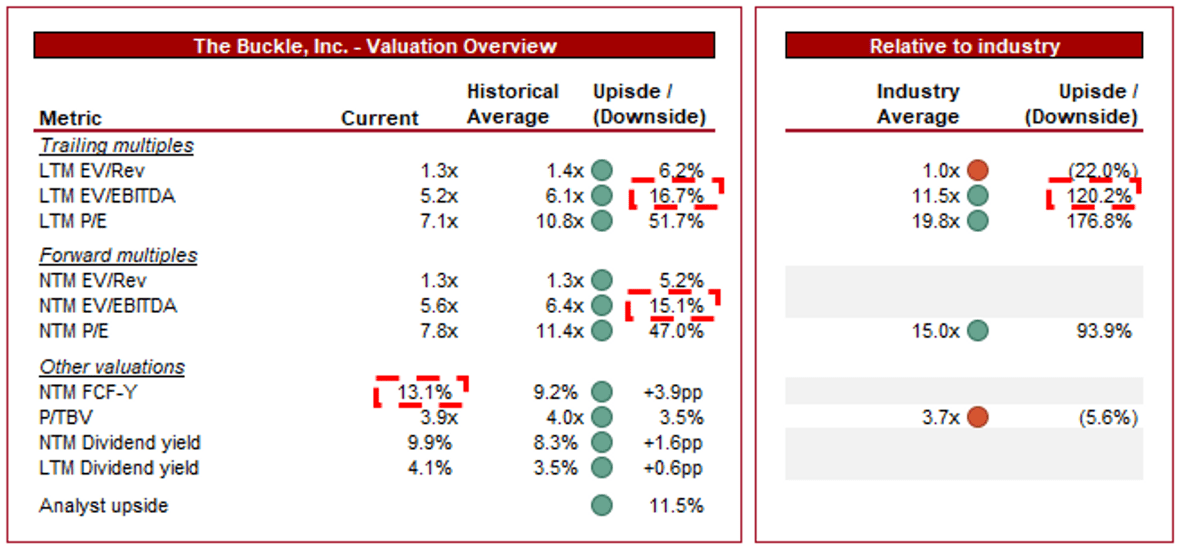

Valuation

{kind=link}

Buckle is currently trading at 5x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the continued weakness in growth and the risks associated with margin depreciation. Our view is that the current 10-20% discount appears reasonable.

Further, The company is trading at a >100% discount to its peers on an LTM basis EBITDA basis, and close to this on a NTM P/E basis. This appears extreme in our view, primarily due to the high profitability of the business. Investors are pricing in a substantial decline in profitability. As the company’s average FCF margin illustrates, this margin depreciation has yet to hit its distributable potential.

Key risks with our thesis

The risks to our current thesis are:

- Margin deterioration. The biggest risk Buckle is margin deterioration. Even if growth is mediocre, investors can enjoy a >10% yield that will drive healthy returns. If this is lost, however, the company’s attractiveness disappears. The key is that we believe it is sufficiently defensible, even if some erosion is experienced.

Final thoughts

The Buckle is an incredibly interesting business. Its margins are incredible and difficult to fully understand. When contextualized with its demographic focus, unwillingness to forgo margins substantially, and own-brand focus, we see that it's a uniquely curated position. With a poor response to a change in the competitive landscape, we are very happy to see profitability is of utmost importance.

We do not see a revitalization of growth occurring due to the lack of commercial development. This said, its own brand strength should mean margins do not ladder down aggressively, providing scope for an attractive FCF yield for investors. At an over 100% discount to peers, we believe there is value here.

For further details see:

The Buckle: Profitability King With Hints Of Value