BKE - The Buckle: Strong Balance Sheet And Solid Performance At A Cheap Price

Summary

- The Buckle is continuing to report year over year growth after a fantastic 2021 fiscal year. The company is starting to expand again after years of stagnation.

- The company has fantastic profitability, reporting EBIT margins of about 26%. It also generates strong free cash flow, yielding 13.1% at the current valuation.

- Its balance sheet is extremely healthy. The company has an inventory position in line with its long term averages. It has no long term debt and low financial obligations.

- The business is trading at a cheap valuation. It is set to return extra cash to shareholders with a large special dividend in the coming months.

Investment Thesis

The Buckle ( BKE ) is successfully beating tough 2021 comparables. Last year, the retailer reported fantastic growth compared to both 2020 and 2019. The company’s finances are very healthy, and the business is starting to expand again. Although long term growth is still a risk, I believe that shares are cheap at the current valuation.

Promising Growth Trends

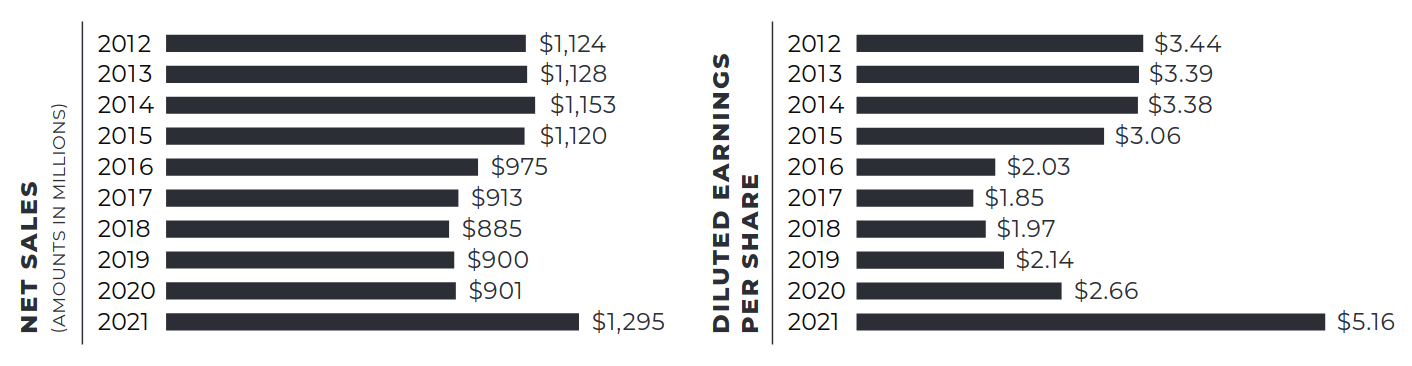

The Buckle experienced explosive growth in 2021. Previously, the core business had struggled to grow its top line. Revenues remained stagnant or declined for most of the last decade. Between 2013 and 2019, the company’s free cash flow declined by almost half. Then, the company had a fantastic 2021. After years of stagnant revenue, it reported revenues up over 43% and operating profit up over 150% from 2019 levels.

After this year of great growth, it was unclear if The Buckle would be able to retain this revenue growth. A lot of consumer discretionary businesses saw a one time boost from the pandemic. For many of these companies, that tailwind quickly subsided.

{kind=link}

It appears that The Buckle is retaining its revenue base. The company is continuing to report positive growth. Other retailers are reporting spending pullbacks. In August, the business reported 5.8% total year over year top line growth. In September, it reported a 3.8% total year over year revenue increase. I think that these trends are promising, especially compared to other retailers.

Besides The Buckle’s core denim and tops segments, the company is expanding its offerings. Its accessories and footwear segments are developing nicely. During the last quarter, these segments grew by 30% and 32% over 2019 levels. The company is also focusing on its youth segment. The category only makes up a small amount of sales, but it reported 37% year over year growth. The company expects back to school trends to improve this result.

The company is also repositioning itself to reduce its dependence on other brands. In 2016, the company’s exclusive merchandise generated $340 million in sales. Last year, that number expanded to $567 million. This is a 13% CAGR and represents an 8 percentage point expansion as a percentage of sales.

Management is also starting to expand the company again. They have started to grow their stores’ physical footprint. The company plans to open five new stores this year. This would be its first net increase in stores since 2015.

Solid Financial Health

The company states in its 10-K that it sells “medium to better-priced casual apparel.” I believe that this category is riskier than other segments during a recession. Other retailers are reporting that consumers are trading down outside of luxury categories. This hasn’t shown up in The Buckle’s monthly results yet, but it’s a risk to keep in mind in upcoming months.

The business is still heavily centered around denim products. In the last quarter, these made up about 40% of sales. I think that this segment will stay resilient even during a spending pullback. These items are a less discretionary category.

The business has elevated but healthy levels of inventory. During the last quarter, the company’s $129 million in inventory was the highest level since 2019. This is about 90 days of inventory, which is in line with The Buckle’s historical averages. The company also hasn’t reported high levels of markdowns.

The business has extremely strong margins. Last year, the company reported a fantastic EBIT margin of 26%. I think that this reduces the long term risk of the investment. Even if the company has a soft year, it should still be able to perform decently. The company expects increased margin pressure throughout the rest of the year. Management discussed this on their last earnings call .

The challenge there is really – I mean, store labor is the area where we’re seeing an increase in where we saw the increase in the second quarter, and that continues probably for the back half of the year that we were running so lean a year ago that – I mean we were at historically low levels of payroll and especially store level payroll. So even though we’re up 135 basis points year-over-year, we’re still down north of 260 basis points compared back to ‘19. So, I mean, again, it’s a really difficult compare on the SG&A side for the rest of the year.

The primary risk here is that the business returns to its long term trend of stagnant top line growth. If this happens, the company's current strategy may become a headwind. Increasing store counts and growing operating expenses are risky moves in a slowdown. I don’t believe that there are signs of a large slowdown, but The Buckle’s sales are down year over year in real terms.

Cheap Valuation And Solid Returns

The Buckle is trading at a forward P/E of 6.7 times and a forward EV/EBITDA of 4.6 times. Over the last twelve months, the company has driven strong shareholder returns with a ROIC of 29%. I think that this is reasonable for a company with a stable forward outlook.

The company has no major debt, and its ongoing obligations are covered by cash on hand. This is an extremely healthy position. Many of the company's peers are struggling with high debt burdens.

The Buckle generates strong free cash flow. It has a LTM free cash flow yield of above 13%. The company pays out a regular dividend yielding 4.1%. This is well covered by the company’s free cash flow.

The company hasn’t historically used its free cash flow to buy back its shares. Instead, the company has returned spare cash to investors with a large special dividend in the fourth quarter of each year. This is an interesting strategy. On their Q3 2020 earnings call , management said this is because the company has a smaller float. This dividend may have some tax implications for investors. Aside from that, I think it’s good that management is committed to returning cash to shareholders.

Final Verdict

The Buckle is an interesting retail play. Recent data points indicate that it is still performing well as the economy slows. The business is very financially healthy and is working on its competitive positioning. Shares are trading at a cheap valuation. The company returns cash to shareholders through a consistent dividend.

I think that there is a risk of a reversion to the company’s long term trend of stagnant growth. The company is successfully beating tough comparables. But the upcoming holiday season is going to be the major test of The Buckle’s business. Still, I believe that shares are undervalued at the current price.

For further details see:

The Buckle: Strong Balance Sheet And Solid Performance At A Cheap Price