VICI - The Buy-Hold-And-Go-Fishing REIT Portfolio: Year 2

2024-01-16 06:30:00 ET

Summary

- The Go-Fishing Portfolio aims to provide a low-maintenance investment option for retirees seeking income from REITs.

- The portfolio includes ten REITs with an average dividend yield of 4.6% and projected FFO/sh growth rate of 5.1%.

- The portfolio composition remains unchanged for 2024, with a focus on dividend growth and survivability amidst credit crises.

A year ago I published The Buy-Hold-And-Go-Fishing REIT Portfolio . It was a response to the expressed desires of many of our members and my readers.

A lot of them have aged and are ready to wind down their individually managed real estate holdings. They want to replace the income and are attracted to REITs because they seem comprehensible.

These investors are not looking for positions they need to closely manage. They want holdings they can check in on once a year.

Their goal is to spend the dividends while living a life they enjoy. The metaphor for that here is to go fishing. That was the goal of an uncle of mine in retirement; there was nothing else he wanted to do.

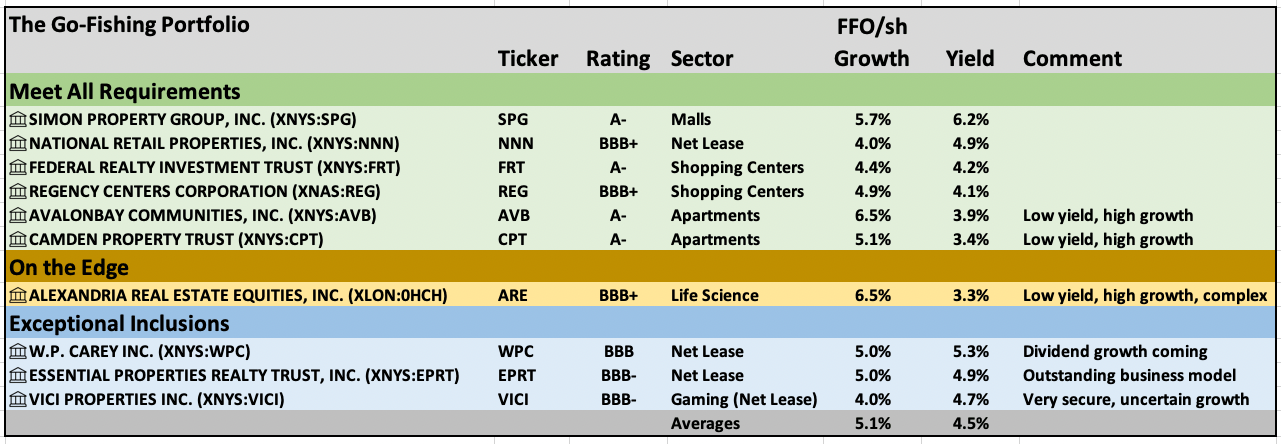

The point of the Buy-Hold-And-Go-Fishing Portfolio, or the Go-Fishing Portfolio for short, is to enable such a life. For its first year, I selected these ten REITs:

{kind=link}

This table shows the dividend yield a year ago and my long-term projected growth rate for each REIT at that time. Note that the averages were a 4.5% dividend yield and a projected FFO/sh growth rate of 5.1%. That FFO/sh growth rate will also be close to the growth rate of cash earnings.

On the assumption that the market will value earnings at a constant multiple, these REITs will produce an average, long-term, total return of nearly 10%. However, year-to-year and even decade-to-decade the average may differ. The reason is that earnings multiples vary, as discussed here .

What our intrepid fisherman can spend is the dividends. These will grow even if the market multiples stagnate or drop.

This yield may disappoint, as the yields of successful hands-on property owners are perhaps twice that dividend yield. But usually not without spending energy and always with valuation risk. And that valuation risk is magnified by their leverage, often 2x or more what REITs carry today.

The idea here is to take the funds and initially equal weight the portfolio holdings. Rebalancing at intervals would be possible but is not part of the basic, minimum-effort gestalt. What the fisherman who put $1M into this portfolio a year ago got was a bit more than $45k, as the dividends came through in 2023 with some increases and no reductions in what was paid out during the year.

Growth reconsidered

Last year my projections for FFO/sh growth were based on the business model of each REIT. But they still reflected the environment of the last 20 years.

This year I thought a bit harder about the projected rate of FFO/sh growth. This sort of portfolio should not count on any growth driven by issuing shares. The market may not cooperate.

The strongest of these REITs have not been issuing shares since the mid-teens anyway. This includes Simon Property Group and AvalonBay.

Here is how the growth goes, overall and long-term. These REITs retain 20% to 30% of actual cash earnings and invest them at a return on new equity of something like 7.5%, give or take. This grows cash earnings by 1.5% to 2%.

In addition, they generate same-store NOI growth of 3%, give or take, although this depends heavily on the specifics of their rent escalators. One ends up with something like 4% to 5% projected FFO/sh growth, with individual variations.

We will consider next whether to add any REITs to the portfolio.

Add Any REITs?

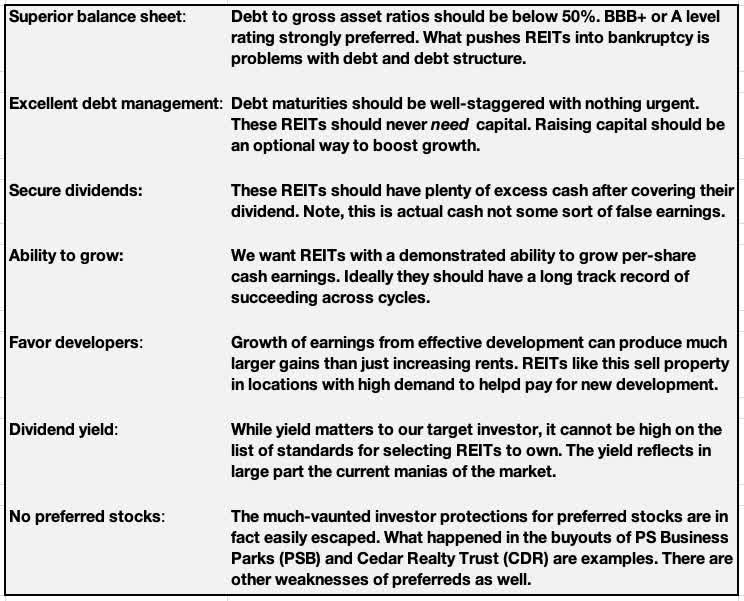

Here are the demanding requirements established last year to be considered for the Go-Fishing Portfolio.

{kind=link}

The goal here is to identify REITs with both a minimal default risk and an ability to grow their dividends well over time. These are the ones that should provide increasing real income yet can be ignored for a year or years.

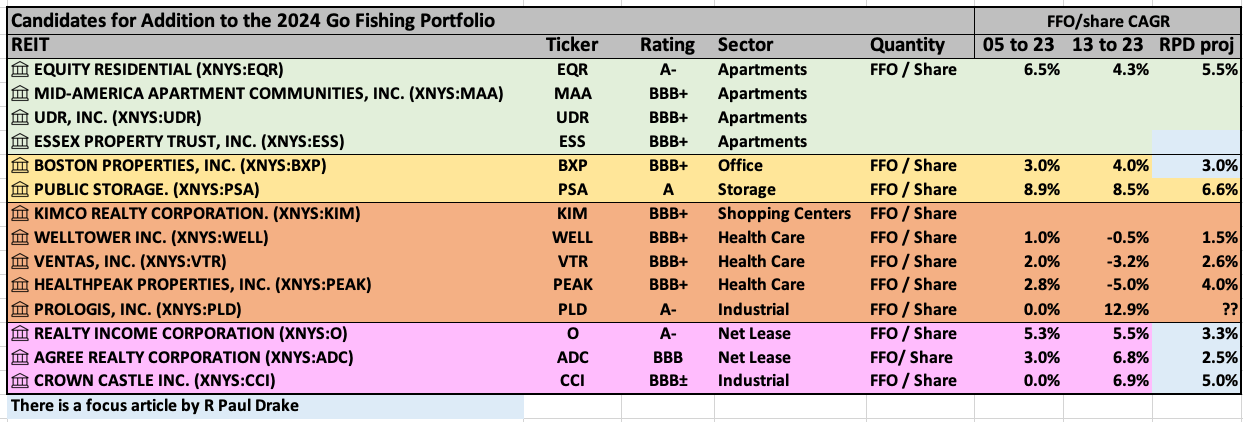

I went through and gathered the current remaining REITs with credit ratings of BBB+ or higher. Then I looked at all the other REITs to see if any seemed to me to be close to meeting the standards. Here is what that produced, followed by comments on some of these:

{kind=link}

The rows shaded light green show the other four large, highly rated apartment REITs, in addition to Camden and AvalonBay. There would be no objection from me to including any of them in the portfolio but pushing the portfolio fraction of apartment REITs above 20% seems unwise to me. The two included are the ones I know best.

The rows of shaded gold meet most of the requirements. BXP ( BXP ) just does not project to having the growth we want (and also just had a credit downgrade from Moody’s). I personally went long BXP last year, but at an effective yield on cost pushing 8%. But even then, it would have seemed a bit too risky to include them here.

As to Public Storage ( PSA ), their dividend yield is on the low side. More importantly, storage is an unstable sector that does not have my trust.

The REITs shown on rows shaded orange were all rejected last year . My view of each of them has not changed. To my mind, they just don’t fit the goals here.

There is a bit more to say about the three REITs shown in rows shaded purple. Ultimately there would be no objection from me if you wanted to put any or all of them in your version of a go-fishing portfolio.

A recent article of mine considered Realty Income ( O ) and Agree Realty ( ADC ). There is no issue with dividend security for either of them. But their low escalators limit their prospective growth during unfriendly markets.

So the question is whether dividend growth will keep up with inflation. For that to happen, their stock prices must be high enough to enable accretive share issuance.

Overall, if including one of them my choice of one of the two stocks would be ADC, despite the lower credit rating. On top of the growth rate issue just mentioned, my view is that Realty Income has reached the point of diminishing returns that come with large size.

That leaves Crown Castle ( CCI ). I looked at them in some depth this year here .

Their earnings are completely dependent on the evolution of the very small number of major wireless carriers. The merger of Sprint and T-Mobile had significant negative impact.

Today they pin high hopes on Dish. But if the Dish network folds that will produce more losses.

For earnings growth, Crown Castle depends entirely on the rate of growth of demand for bandwidth. Certainly, such demand will grow, but how fast? This will directly impact their growth.

So do they deserve their Baa3 (almost junk) rating from Moody’s? Or their BBB from S&P? Or their BBB+ from Fitch? You can decide.

At the end of the day, I find myself unconvinced about adding CCI here. No objection if you do, but it might make sense to wait until it seems that the next several years have a clear path to dividend growth.

Throw Anybody Out?

Why might we sell one of these REITs and throw it out of the Go-Fishing Portfolio?

The most likely reason would be a change in the prospects for dividend growth. To my mind, this is unlikely (but see below).

Note though, that the dividend has almost no chance of being eliminated for any of these REITs. Any cuts are likely to be well below 50%.

But suppose one of these REITs announced that they were going to target a payout ratio of 90% going forward and raised their dividend by 20% to 30%. That increased dividend might be worth collecting for some years, but eventually, it would make sense to swap out that REIT for one with better long-term prospects for the dividend to keep up with inflation.

Alternative scenarios quickly reach science fiction. It is true that Simon cut their dividend by 40% during the pandemic, but that was when governments shut down nearly all their properties for about three months. Another similar event would produce a pretty small (4%) decrease in the income from the Go-Fishing Portfolio.

You can concoct scenarios where the government imposes vastly higher costs (or shutdowns) on some group of properties. This could impact the income or income growth from this portfolio. Decide for yourself how you want to react to the potential for such developments.

Temporary crises are a more realistic probability, such as the next financial crisis during which it becomes impossible to get new credit for some period. This is worth thinking about and is discussed below.

Turning to specifics, there are two REITs in the portfolio one might consider shedding. These are VICI Properties ( VICI ) and W. P. Carey ( WPC ).

In researching my recent article on VICI Properties, I encountered a fact that I did not know. Moody’s does not have them as investment grade.

VICI does disclose this (kudos) but otherwise writes, speaks, and acts as though they are an “investment grade” company (hard to blame them). But an analyst of the company ought to note that discrepancy and highlight it. There should be a difference between analysts and cheerleaders.

Moody’s still has VICI at the equivalent of BB+. To support an upgrade, they would need to see the Debt/Adjusted EBITDA ratio, near 5.7x, come down near 5.0x. Moody’s also highlights tenant and property concentration as a source of credit risk.

Beyond these aspects, VICI is adding riskier properties as it seeks to grow. They also have become so large that they share with Realty Income the problem that size makes quality growth harder.

Some of their new properties, such as water parks and bowling alleys, do not bring the security of their casinos. Although the risk to the dividend is small, these changes increase that risk.

Going forward from here my view is that the VICI dividend is not at risk but that over time it may grow more slowly. I see no urgency here and am leaving VICI in the portfolio, noting the need for closer annual monitoring than some other REITs demand.

My one clear mistake in constructing this portfolio a year ago was to include WPC. I thought they were at the point of being ready to steadily grow their dividend, but they were not. Instead, they cut it.

The recent dividend reduction of about 20% will reduce the portfolio income by 2% next year. We can expect the dividend increases from the other holdings to exceed that by quite a bit, but still, this is not what we want.

A bit of context seems worthwhile about where W. P. Carey is now. Current management inherited a real mess in 2017 and has been steadily fixing it.

In my article W. P. Carey: To Cut The Dividend Or Not , published about 30 months ago, I detailed the history and how their high payout ratio crippled their ability to grow the dividend and how cutting the dividend in order to retain a larger fraction of AFFO to drive growth would be advantageous.

Those arguments were similar to what WP Carey management had to say last year about their decision to finally cut the dividend. This got a bit lost amidst the story that they had also decided to shed their remaining office properties.

But I thought, wrongly, that they had progressed far enough that they would not need to cut. That case was made in my article last summer. On top of that, I failed to identify their office properties as the headwind that they seemed to have been.

So mea culpa. But what matters is where things stand now.

WPC will grow their dividend from here at a good rate, thanks in part to their excellent rent escalators. There is no way I would sell, and if putting together a new Go-Fishing Portfolio, I would definitely include it.

Perhaps more importantly, none of the other REITs in the portfolio have either the payout ratio issues or the property performance issues that W. P. Carey had.

So we end up not changing the portfolio composition. Although, as indicated, the REIT stocks that might be included or excluded at your option include ADC, O, CCI, VICI, and WPC.

Survivability Amidst Credit Crises

Based on history, equity REITs almost never suffer operating losses and very rarely produce negative cash from operations. What gets them in trouble at times is addressing their maturing debt. So we need to look at this every year.

When maturing debt cannot be handled, the two options are issuing a lot of stock to cover the debt or declaring bankruptcy. [In principle selling assets is a third option, but that may take too long or not be feasible amidst a crisis.] Any of these comes with a dividend cut or elimination.

During the Great Recession, many REIT dividends were cut and a lot of stock was issued. Amongst this group, dividends were cut by ARE, CPT, REG, and SPG. CPT, REG, and SPG also issued comparatively modest amounts of stock, diluting shareholders by 20% to 30%.

Things were different for these four REITs after that. Things I happen to know: ARE began to grow like mad. CPT generated much higher growth of FFO/sh. REG completely reworked its portfolio. SPG substantially increased its liquidity.

Across the pandemic, only SPG cut their dividend, and only in response to the impact of government-mandated shutdowns.

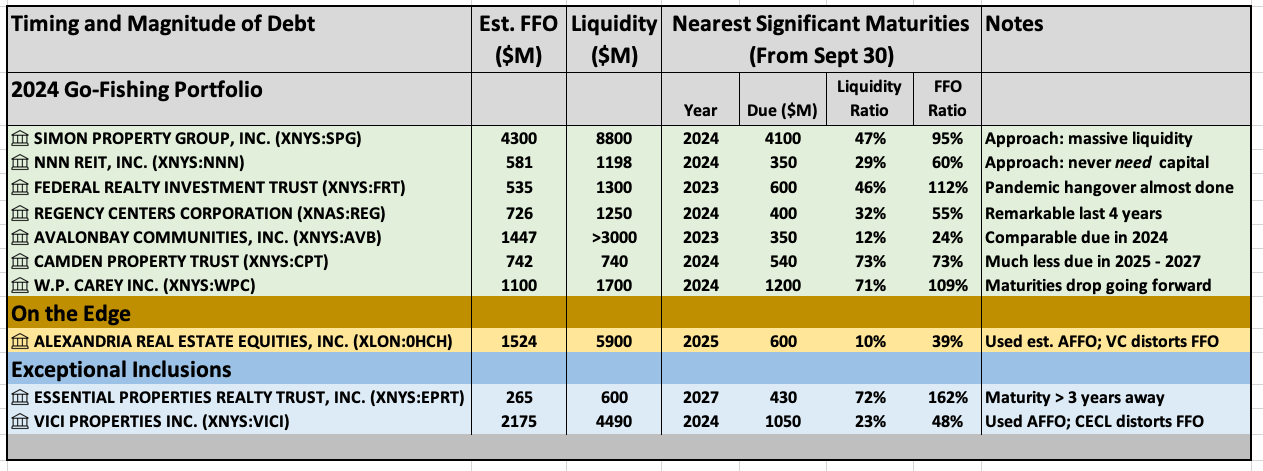

To see where things stand today, we look at three numbers and two ratios. The ratios are that of FFO to the nearest significant maturity and that of the nearest significant maturity to liquidity.

{kind=link}

The liquidity ratio is below 100% for all these REITs. This implies that they can pay off all debt due in the year shown.

The only one with debt still due in 2023 as of last September 30 was AvalonBay. Their debt due in 2024 is comparable, and the two together still require less than a quarter of their liquidity.

My preference would be to see liquidity ratios below 50%. But of the three cases where this is not true, two (Camden and W. P. Carey) will see much lower maturities after 2024 and one (Essential Properties) has no debt due until 2027.

In general, a low FFO Ratio is also desirable, as all of FFO is not available to service debt even in extremis . Most of these REITs have an FFO Ratio well below 100%.

The exceptions here include

- Simon, whose extra liquidity of nearly $5B does seem sufficient.

- Federal Realty, who decided to boost debt during the pandemic to sustain its dividend and is still working the debt back down.

- W. P. Carey, whose maturities will drop going forward. They also recently pushed their revolver and term loan out several years.

- Essential Properties, reflecting their newness and fast growth. If their FFO Ratio does not come down rapidly from year to year, it will become time to exit EPRT.

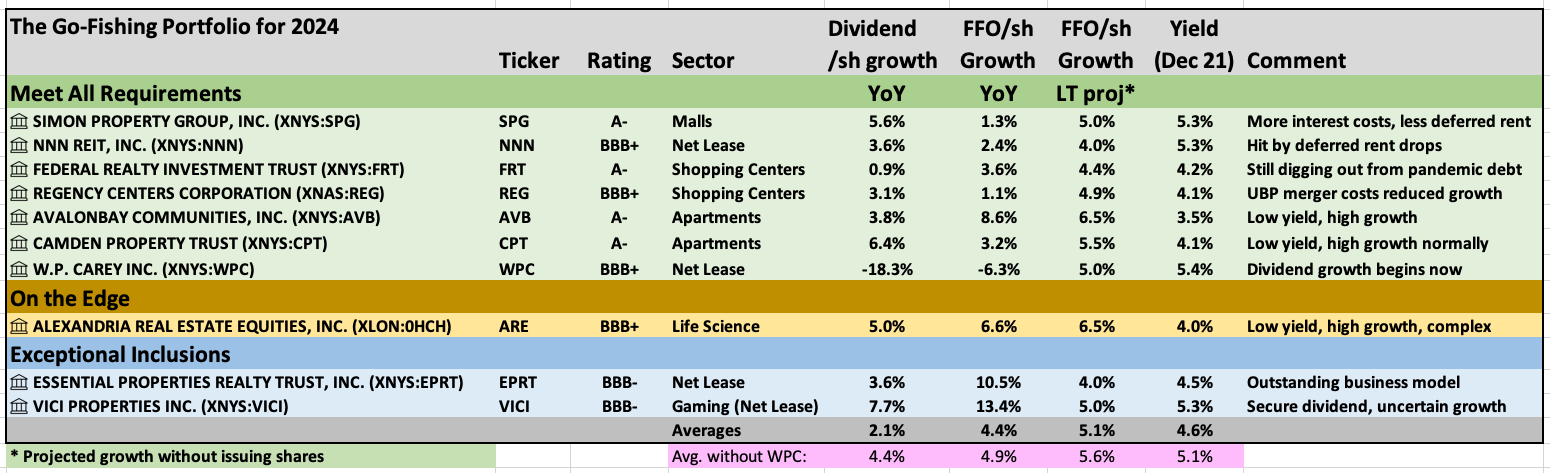

The 2024 Go-Fishing Portfolio

This leaves us ready to look at the 2024 Buy-Hold-and-Go-Fishing Portfolio and consider the future for its companies and payouts. Here it is:

{kind=link}

The portfolio has the same 10 REITs as last year. The only change is that WPC moved up into the light green as a result of its credit upgrade.

There are four columns related to performance and a column of comments. You can read the details at whatever level you like. Here are some highlights:

The dividends per share averaged about 4.5% (see above), but only grew by 2%. If you were smart enough to skip WPC, they would have grown at 4.4%.

Earnings, measured by FFO/sh, grew 4.4%. Some weak performers (and WPC) were offset by growth from EPRT and VICI. Both of those were able to grow earnings beyond the minimum generated from rent bumps and internal funds.

My refined long-term projection for FFO/sh growth is about 5% and reflects both downward and upward adjustments. This may be a tad high. Across the next year, I will pay closer attention to the growth achievable without issuing equity. The yield averages 4.6%, marginally above last year’s.

We will see how the next year goes, but barring a very deep recession I just don’t see any potential for a disappointment like WPC was this year. And even then, my expectation would be for quite modest impacts.

The largest risk lies in the two REITs with BBB- credit ratings, which also produced the largest growth in some way. Your choice is to remove them and get somewhat lower growth and less risk, or not.

Finally, the least important aspect of this portfolio is market value changes, especially over only one year. Growing income is the point.

But just so readers will not complain, here is the number. The price return on equal-weight Go-Fishing Portfolio bought one year ago was 6.0% for 2023.

As yet my own personal goals have not aligned with this portfolio. I’ve wanted higher yield. But as I age and if my investments succeed, the alignment will become closer. How about you?

For further details see:

The Buy-Hold-And-Go-Fishing REIT Portfolio: Year 2