EXEL - The Canary In The Coal Mine

2023-06-26 13:51:44 ET

Summary

- Markets have performed well so far in 2023, based on the major indices, but the rally has lacked breadth and been driven primarily by a few mega-cap stocks like Apple.

- The Federal Reserve's most aggressive monetary tightening since the early 80s is finally starting to be felt throughout the economy.

- This is starting to result in rising corporate defaults and a fast deteriorating commercial real estate market.

- A less dire but still very concerning situation that has some of the ghosts of 2008 around it seems to be developing.

- The state of the markets and my investing game plan for the second half of 2023 follow below.

The future is uncertain but the end is always near. "? Jim Morrison.

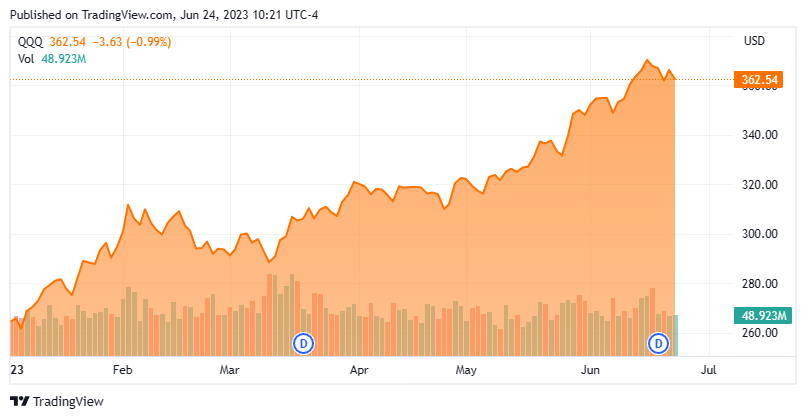

We are fast approaching the end of the first half of 2023. After a large pullback in the market in 2022 which saw the NASDAQ lose a third of its value, equities have bounced back nicely in the first half of 2023 despite rising interest rates and myriad other economic concerns. With a week to go in the opening half of 2023, the overall market is up nearly 15%.

{kind=link}

However, most of the rally has consisted of large rises from Mega-cap stocks like Apple ( AAPL ), Tesla Motors ( TSLA ), and NVIDIA Corporation ( NVDA ). This has led to a better than 37% gain in NASDAQ year-to-date.

{kind=link}

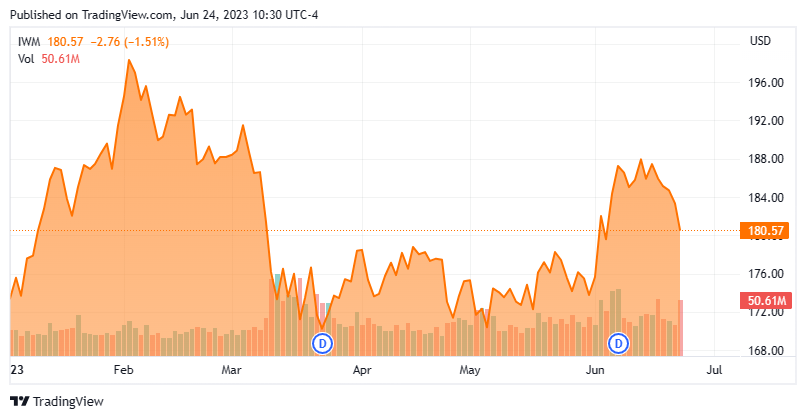

However, the breadth of the rally has been absolutely dismal, with the Russell 2000 Index (RTY) up less than five percent for the year. More concerning is that the impacts from the Fed's most aggressive monetary tightening since the days of Paul Volcker are just starting to be fully felt across the broader economy. Investors seem to be memory holing that it takes approximately 18 months for changes in monetary policy to work their way across the economy.

A situation is developing that feels like 2008-Lite to me, as corporate defaults and bankruptcies are rising at the fastest rate since 2010. They have already claimed some well-known companies here in 2023, such as Bed, Bath & Beyond (BBBYQ).

However, the " canary in the coalmine" as it relates to the economy and the markets is an increasingly dire situation in much of the commercial real estate sector. The last financial crisis was triggered by subprime mortgages that shattered equities and the economy in 2008. This time the likely economic recession ahead of us will be driven by the cascading impacts from this rapidly failing sector of the economy.

Approximately $270 billion in commercial real estate loans needs to be rolled over by the end of 2023, some $80 billion of that is on office buildings. Approximately $1.5 trillion needs to be refinanced over the next three years. The problem for creditors that hold commercial properties is that this refinancing will have much higher rates and in many cases with properties valued for significantly less than when the property's current debt was issued. This is particularly true for office and retail.

The pandemic triggered a roughly three-fold increase in the virtual workforce. This cohort has been very reluctant to return to the office. Many workers have moved to the suburbs; some have left their previous state entirely. This has resulted in a huge increase in office vacancies in cities like Chicago , New York , and San Francisco . Which in turn has eroded the market value of these properties. As leases expire, corporations will be reducing their corporate footprint, putting further pressure on lease prices and office values.

A recent article on CNBC put the situation bluntly:

Capital is much more expensive now," said Mohsin Meghji, founding partner of restructuring and advisory firm M3 Partners. "Look at the cost of debt. You could reasonably get debt financing for 4% to 6% at any point on average over the last 15 years. Now that cost of debt has gone up to 9% to 13% ."

Earlier this month, Park Hotels and Resorts ( PK ) announced it would stop payments on a $725 million, non-recourse CMBS loan secured by two of its San Francisco hotels. The hotels are the 1,921-room Hilton San Francisco Union Square and the 1,024-room Parc 55 San Francisco.

This was quickly followed by an over $500 million default around the largest mall in San Francisco. Meanwhile, this week, the owner of an apartment complex in the Upper West Side of Manhattan moved towards defaulting on just over $195 million worth of commercial mortgage back loans on the property. This, at a time, when average rents in NYC are at all-time highs.

Obviously, this trend has huge downstream impacts. It is also very easy to see why this development will accelerate in the coming months. Let's say you are an owner of an office building purchased for $300 million in 2018 with 30% down with the blended interest rate on the remaining debt averaging 5.5%. Five years later, that loan is coming due and needs to be rolled over. Unfortunately, the building is now valued at only $195 million, wiping out all equity, and to refinance the remaining loan will now have to be done at a 10% to 12% interest rate. The logical recourse, and sometimes the only one, is turning the property over to the lenders.

The lender hardly wants to operate an office building, so they sell, most likely at a significant discount. This further depresses office values in the area. Increasing default rates are also a huge headwind for the regional banks that supply some 70% of the loans to the commercial real estate industry. Their response to increasing loan losses will be to be more stringent with credit criteria and loan out less money. This, in turn, will reduce overall economic activity and could easily turn into a " credit crunch." In addition, as losses increase, regional banks will be forced to sell off some of their loan and bond portfolios at a loss, negatively impacting earnings.

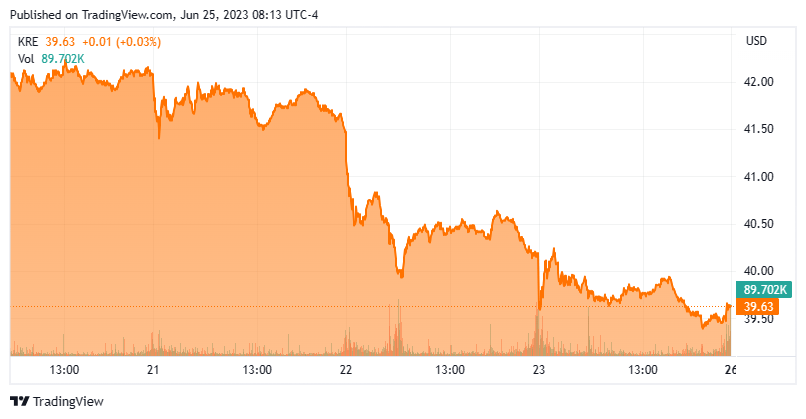

A preview of how fast sentiment can change on regional banks was provided last week, when the SPDR® S&P Regional Banking ETF ( KRE ) fell hard late in the holiday-shortened trading week.

{kind=link}

My view is the second half of 2023 is going to see an acceleration of defaults and negative headlines around the commercial real estate sector. This will throw the economy into the recession before year-end. I have taken steps to insulate my portfolio and assets from this scenario, one which should trigger at least a 10% to 20% pullback in the overall market.

First, I sold the 2bd/2.5bth condo I purchased in the fall of 2020 here in Delray Beach, FL for a large gain last month. I am now locked into a below market value lease on a house a few blocks away through late 2024. Palm Beach County has seen a huge spike in housing values since the pandemic as the region has seen a massive influx of New Yorkers and others fleeing the northeast as well as places like Chicago and California. My guess is that average property values will come down 15% to 25% in a recession scenario, especially with mortgage rates near seven percent on average.

I have parked those sale proceeds and approximately half my equity portfolio in short-term treasuries that yield north of five percent currently. Most of the remaining portion of my long equity portfolio is within covered call holdings on names with great balance sheets such as Exelixis ( EXEL ). Over the past month, I have been adding " stabilizers" to my portfolio.

I do this by executing bear put spreads on equities I feel have gotten quite a bit overvalued such as Apple, Walmart ( WMT ) and RH ( RH ) and will be vulnerable if the economy starts to contract and the overall market pulls back.

This strategy involves buying a put and simultaneously selling a put at a strike under the first put on the same calendar month. Using this strategy, an investor is looking to capture a profit if the stock in question declines within the option duration enough to make the trade a winner.

I like to go 4-6 months out with these option pairs and approximately 5% to 10% below the current trading level of the stock for the top end of those put spreads. If these stocks fall 15% to 20% within the option duration, I typically will make 4-6 times my money which will greatly offset losses in my long portfolio.

I rarely do this within my portfolio, but it feels very likely that investors will not be able to whistle past what I think will fast become a graveyard in the commercial real estate sector in the second half of the year. This will have all sorts of negative effects throughout the financial system that are not reflected in the current trading levels of the market.

Hope is the great deceiver. Hope is the piper who leads us sleepy to our slaughter. "? Brent Weeks, The Broken Eye.

For further details see:

The Canary In The Coal Mine