CATO - The Cato Corporation: Pressure On Growth Rates And Profitability Continues

2023-10-03 04:40:22 ET

Summary

- The company's revenue decreased by 7.1% YoY, while operating margin reached 1.3%.

- Declining same-store sales and the deleverage effect continue to put pressure on business profitability.

- I don't expect we can see a recovery in growth and profitability in the coming quarters, so my recommendation is hold.

Introduction

Shares of The Cato Corporation ( CATO ) have fallen 20% YTD. Despite the fact that the company's shares have declined significantly, I believe that it is still not the best time to open a long position in the company's shares. In my article, I would like to analyze current business trends and share my own opinion on future financial results of the business and valuation.

Investment thesis

On the one hand, I like the fact that the company has a long operating history, is run by excellent management and has no debt load on the balance sheet, however, on the other hand, at the moment, I believe that investors will need to wait for the financial results for the next quarters before than to make a purchase decision as pressure on operating and financial results may continue while I do not see additional growth drivers/catalysts.

Company overview

The Cato Corporation sells value-priced fashion apparel and accessories for men and women. The main sales channel is retail. As of the 2nd quarter of 2023, the company operates 1,247 stores in 31 states. The company's stores operate under the names "Cato", "Versona", "It's fashion" and "It's Fashion Metro".

2Q 2023 Earnings Review and my expectations

The company's revenue decreased by 7.1% YoY due to a decrease in same-store sales by 6%. Gross profit margin increased from 33.1% in the 2nd quarter of 2022 to 35.7% in the 2nd quarter of 2023 due to a decrease in distribution and freight costs, as well as markdowns.

Gross profit margin (Company's information)

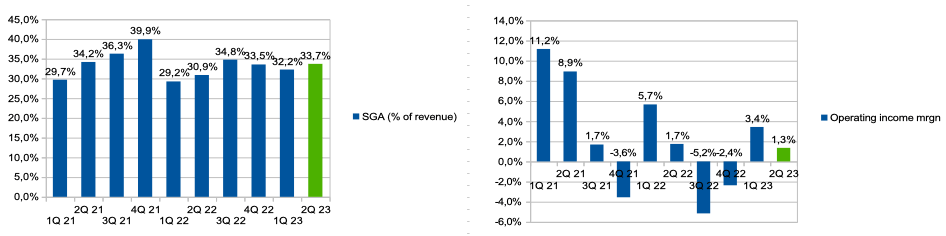

SGA expenses (% of revenue) increased from 30.9% in 2Q 2022 to 33.7% in 2Q 2023 due to the deleverage effect resulting from lower scale effects and higher salary costs. Therefore, operating margin decreased from 1.7% in Q2 2022 to 1.3% in Q2 2023.

SGA (% of revenue) and operating income margin (Company's information)

{kind=link}

I believe the company's operating and financial performance will continue to be under pressure in the coming quarters. On the one hand, I don't think we can see a quick recovery in discretionary consumer spending even if inflation slows because consumers will continue to face higher costs for interest payments, rent and food.

Additionally, I don't think we can see an improvement in the operating profitability of the business in the coming quarters because the company will continue to face deleverage effects due to reduced economies of scale as a high portion of operating expenses are fixed, meaning store rental costs and a fixed part of the salary.

Forecasting and valuation

I decided to make my own assumptions to calculate future multiples and draw my own conclusions about the current level of business valuation. Separately, I would like to note that in my forecasts I relied on my own expectations and market data, in addition, I tried to adhere to conservative assumptions. Thus, I believe that consumer spending will continue to be under pressure in the coming quarters and, therefore, the dynamics of traffic in the chain's stores, so I forecast a continued decline in revenue of 5% in the coming quarters.

In addition, I believe that the company's potential to increase the average ticket is limited, since price increases could lead to additional pressure on traffic and a decrease in market share, so I predict a stable level of gross margin until the end of the year, in line with the value in 2Q 2022 of the year.

As I expect the company's revenue growth rate to continue to be under pressure, I expect the deleverage effect to continue in the coming quarters due to lower economies of scale because a high portion of retail operating expenses (rent, salaries) are fixed. Thus, I assume that we will not see a reduction in operating expenses (% of revenue) in the second half of the year, so I forecast SGA expenses (% of revenue) at the 2Q level. So I think the net profit margin will be around 1% in the coming quarters. You can see the details of my calculations in the graph below.

Forecasting (Personal calculations)

{kind=link}

Next, I would like to calculate the multiples for 2023 based on my forecasts. Thus, in accordance with the P/S and P/E multipliers, the company's shares are traded at 0.2x and 16.8x, respectively. On the one hand, a valuation of 0.2x according to the P/S multiple looks attractive, but according to the P/E multiplier, the company is trading at 16.8x, which does not look cheap, because the current multiplier implies a premium to the sector median (12,64x) of about 33%. I believe the company deserves a discount relative to the sector median due to weak trading trends and business size. I agree that a recovery in consumer spending and rising net income could lead to a lower multiple and higher stock prices, but I don't think that will happen in the coming quarters.

Multiples (Personal calculations)

Risks

Margin: a decrease in economies of scale, as well as increased competition, which may lead to the need to increase costs for investments in prices and marketing, may contribute to a decrease in the operating profitability of the business in the following periods.

Macro (general risk): high inflation and declining real incomes may lead to lower consumer spending in the discretionary segment, which may have a negative impact on business revenue growth rates in the future.

Conclusion

Thus, my recommendation is a Hold because I think the decline in revenue growth and pressure on business margins will continue in the coming quarters, while the current valuation does not look cheap according to my calculations. I will happily change my recommendation to buy when I see the first signs of a recovery in store traffic and consumer spending.

For further details see:

The Cato Corporation: Pressure On Growth Rates And Profitability Continues