USFD - The Chefs' Warehouse: A Great Prospect With Growth Set To Drive Value

Summary

- The Chefs' Warehouse continues to generate strong sales, profit, and earnings growth thanks to organic demand and acquisitions.

- This trend is likely to continue, making the business a compelling prospect.

- Add on top of this how shares are priced, and it's definitely a solid prospect for value investors to consider.

Going about our daily lives, it can be tempting to overlook the wonders of our modern era. For most of human history, we spent most of our time gathering food so that we could survive another day. But today, we reap the benefits of significant advances that have since enabled us to purchase almost anything we want for a modest price and put it on our dinner tables. But just looking at the picture through this lens ignores the vast and complicated network that has developed to get the food from its source of production to the ultimate end location. One of the key players in that journey is the food distribution business. And one player in this space that warrants some attention is The Chefs’ Warehouse ( CHEF ). Although a fairly small company with a market capitalization of only $1.26 billion, The Chefs’ Warehouse is growing at a rapid pace and it's trading at levels that look fundamentally appealing on both an absolute basis and relative to similar firms. So long as the picture does not worsen from here, I would make the case that the company warrants some upside potential for investors to enjoy. As such, I've decided to rate the enterprise a ‘buy’ at this time to reflect my view that shares should outperform the S&P 500 moving forward.

A specialty provider

According to the management team at The Chefs’ Warehouse, the company operates as a premier distributor of specialty food and center of the plate products, with operations spread across the US and Canada. Its emphasis is primarily on serving the needs of chefs who own and/or operate independent restaurants, fine dining establishments, country clubs, hotels, caterers, culinary schools, bakeries, and a variety of other food establishments. Unlike some food distributors, The Chefs’ Warehouse focuses on delivering specialty food products. Although this may sound very niche in nature, its current product portfolio includes over 50,000 SKUs (stock-keeping units) from over 2,500 suppliers.

The specific types of food the company distributes are varied in nature. But examples include imported and domestic offerings, such as artisan charcuterie, specialty cheeses, unique oils and vinegars, truffles, caviar, chocolate, and even pastry products. Other offerings include custom-cut beef, seafood, hormone-free poultry, and more. It also provides its customers with cooking oils, butter, eggs, milk, flour, and other ingredients that go into countless recipes. Over the years, the enterprise has established a sizable network of customers for which it provides primary foodservice distribution services for (more than 35,000 core customer locations in all). It also markets its products directly to consumers through its mail and e-commerce platform, called Allen Brothers, as well as through its direct-to-consumer e-commerce offering called ‘Shop Like a Chef’ that provides online home delivery of its products. The firm achieves all of this across 19 primary geographic markets in the US and Canada and through the operation of 40 distribution centers and related assets.

{kind=link}

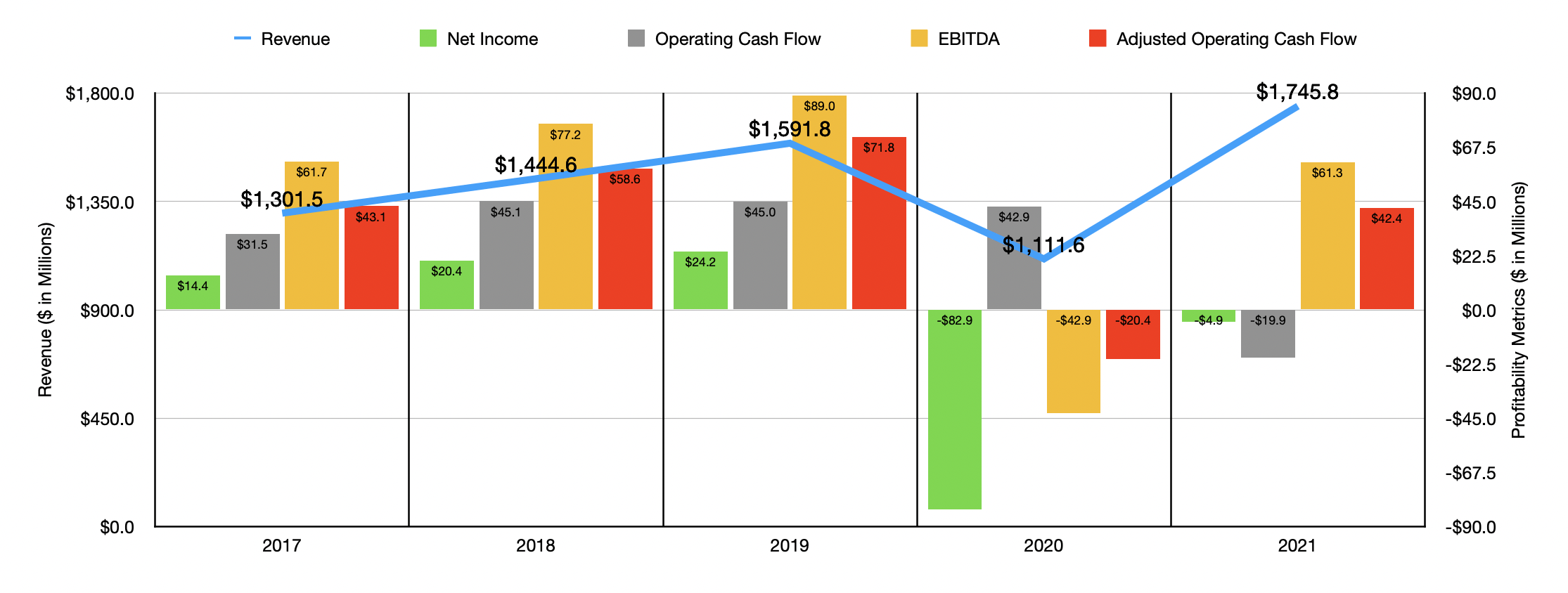

For the most part, the financial track record of the enterprise has been rather impressive. Between 2017 and 2019, sales shot up from $1.30 billion to $1.59 billion. Because of the COVID-19 pandemic, 2020 was a difficult year, with revenue plunging to $1.11 billion. Fortunately for investors, that decline was short-lived. In 2021, sales hit $1.75 billion. Some of this growth was driven by some acquisitions the company had engaged in. In 2020, for instance, it made one acquisition totaling $44.1 million. This was followed up by another acquisition that same year for $16.4 million. But the vast majority of the growth, totaling $574.2 million from 2020 to 2021, was driven by organic sales expansion, with organic case counts climbing 33.8% in the specialty category, specialty unique customers rising 26.1%, and placements rising 31.6%. For the center of plate category, pounds of product sold jumped by 28.2%. Some of this increase can be chalked up to the company passing on inflationary pressures to its customers. They estimated that inflation for the specialty category was around 9.6%, while for the center of the plate category it was 18.1%. But the rest was mostly driven by continued organic growth and the recovery following the pandemic.

From a profitability perspective, the picture has been not too different. Between 2017 and 2019, net income rose consistently, climbing from $14.4 million to $24.2 million. In 2020, the company generated a net loss of $82.9 million that eventually narrowed to a loss of $4.9 million in 2021. Other profitability metrics have been volatile as well. From 2017 to 2019, operating cash flow rose up from $31.5 million to $45 million. Despite the pandemic, cash flow was still strong at $42.9 million in 2020. But the pain in this space did hit from a cash flow perspective in 2021, with cash flow coming in negative to the tune of $19.9 million. If we adjust for changes in working capital, however, the company did post something of a recovery in 2021, with the $42.4 million in operating cash flow beating out the negative $20.4 million reported one year earlier. A similar trend can be seen when looking at EBITDA, with the metric climbing from $61.7 million in 2017 to $89 million in 2019 before dropping to negative $42.9 million in 2020. In 2021, however, it came in positive to the tune of $61.3 million.

{kind=link}

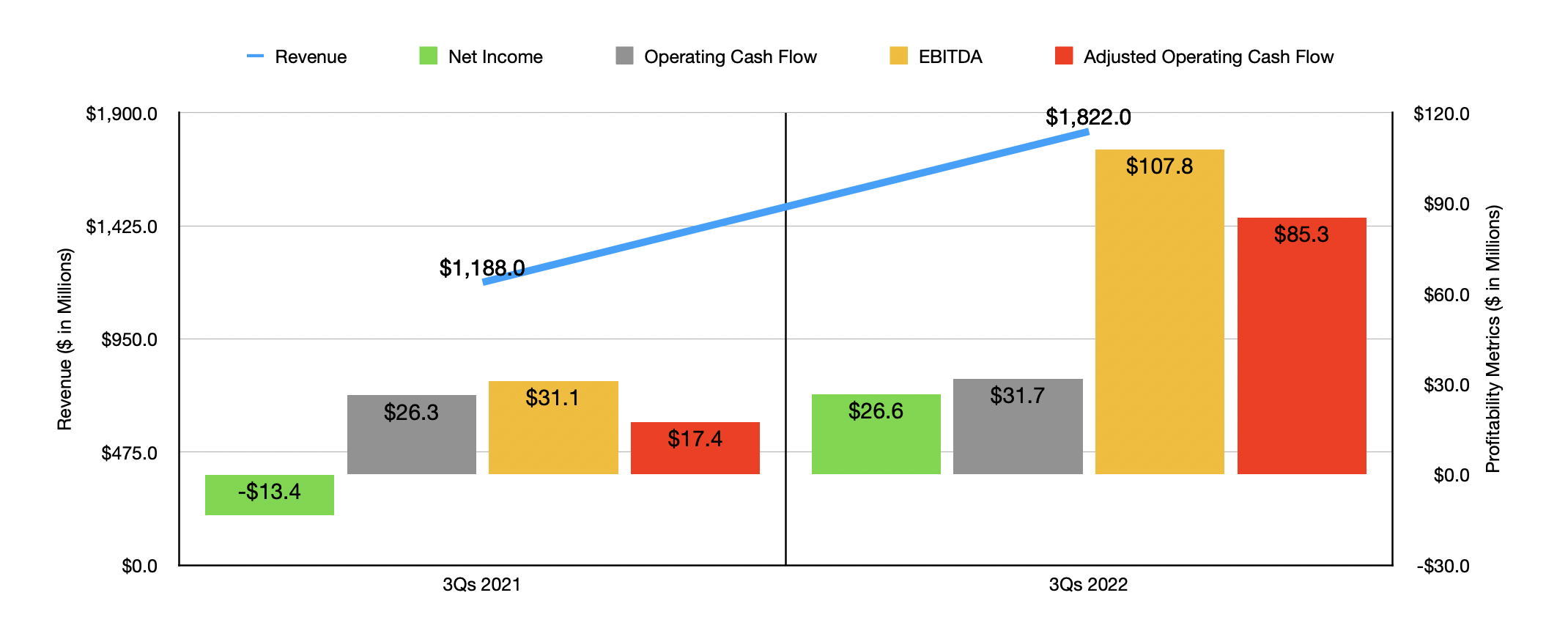

Sales growth for the company has continued nicely into the 2022 fiscal year. For the first nine months of the year , revenue totaled $1.82 billion. That represents a significant improvement over the $1.19 billion reported one year earlier. Some of this was driven by various acquisitions, such as one totaling $31 million in 2021 and three for a combined $32.5 million during the first nine months of 2022. However, management attributed most of the sales increase to a 31.3% surge in organic case count associated with its specialty category of products. This is not to say that other factors did not come into play. Organic pounds sold in its center of the plate category jumped by 16.4%, while inflation for the specialty category totaled 15.5% and was 11.6% for the center of the plate category.

This increase in sales, combined with some margin improvement was instrumental in improving profitability. For the first nine months of 2022, the company generated net profits of $26.6 million. That stacks up favorably against the $13.4 million loss achieved the same time one year earlier. Operating cash flow inched up more modestly from $26.3 million to $31.7 million. What's really impressive though is that if we adjust for changes in working capital, the metric would have risen from $17.4 million to $85.3 million. Over that same window of time, EBITDA for the company also shot up, climbing from $31.1 million to $107.8 million.

{kind=link}

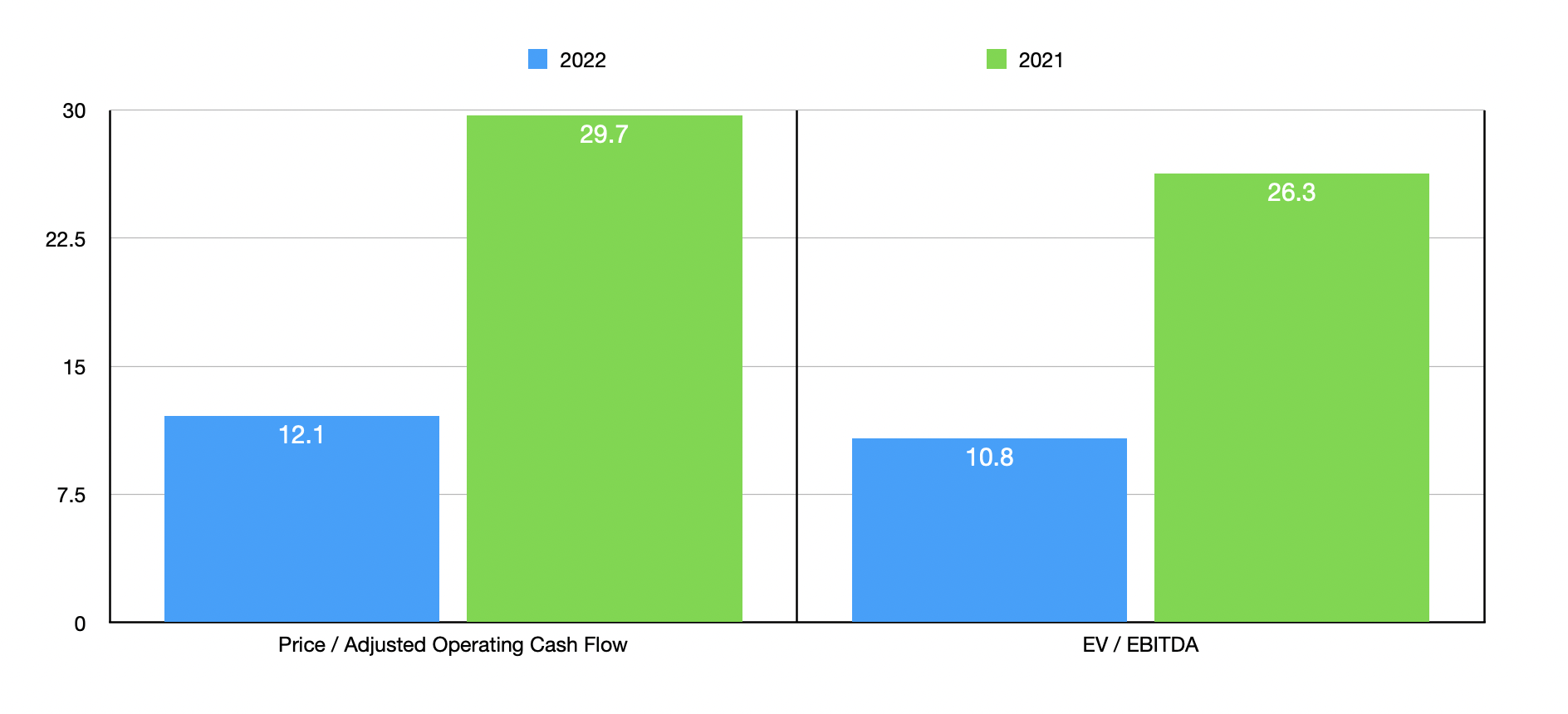

For 2022 as a whole, management said that revenue should be between $2.45 billion and $2.55 billion. This should help to push EBITDA up to between $145 million and $155 million. No guidance was given when it came to other profitability metrics. But if we annualize results experienced so far for the year, we should anticipate adjusted operating cash flow of $103.8 million. Based on these figures, the company is trading at a forward price to adjusted operating cash flow multiple of 12.1 and at a forward EV to EBITDA multiple of 10.8. By comparison, using the data from 2021, these multiples would be 29.7 and 26.3, respectively. As part of my analysis, I also decided to compare the company to five other food distribution businesses. On a price to operating cash flow basis, the four companies with positive results ranged from a low of 15.4 to a high of 43.9. In this case, The Chefs’ Warehouse was the cheapest of the group. Using the EV to EBITDA approach, the range was from 5.9 to 14.1. In this scenario, three of the five companies were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Chefs' Warehouse |

| 12.1 |

| 10.8 |

| The Andersons ( ANDE ) |

| N/A |

| 5.9 |

| SpartanNash Company ( SPTN ) |

| 43.9 |

| 8.5 |

| United Natural Foods ( UNFI ) |

| 15.8 |

| 6.5 |

| US Foods Holding Corp ( USFD ) |

| 15.4 |

| 14.1 |

| Performance Food Group Company ( PFGC ) |

| 16.1 |

| 13.3 |

Takeaway

With all the data in front of me right now, it appears as though The Chefs’ Warehouse it's doing quite well for itself. Through acquisitions and organic growth, the company is expanding nicely and that trend is likely to continue. Although the pandemic time was a rather difficult period for the business, the overall trajectory of the company is positive and shares look cheap on both an absolute basis and relative to similar firms. Because of this, I do feel comfortable rating it a ‘buy’ at this time.

For further details see:

The Chefs' Warehouse: A Great Prospect With Growth Set To Drive Value