CHEF - The Chefs' Warehouse: An Expensive Strategy

2023-11-28 20:19:14 ET

Summary

- Chefs' Warehouse is a wholesale food distributor operating mostly in the United States, building distribution networks in select areas.

- The company's strategy of constant acquisitions has not created shareholder value as it has resulted in significant dilution, a large debt balance, and ultimately a stagnant stock.

- The current stock price seems overvalued - I have a sell rating due to a poor risk-to-reward.

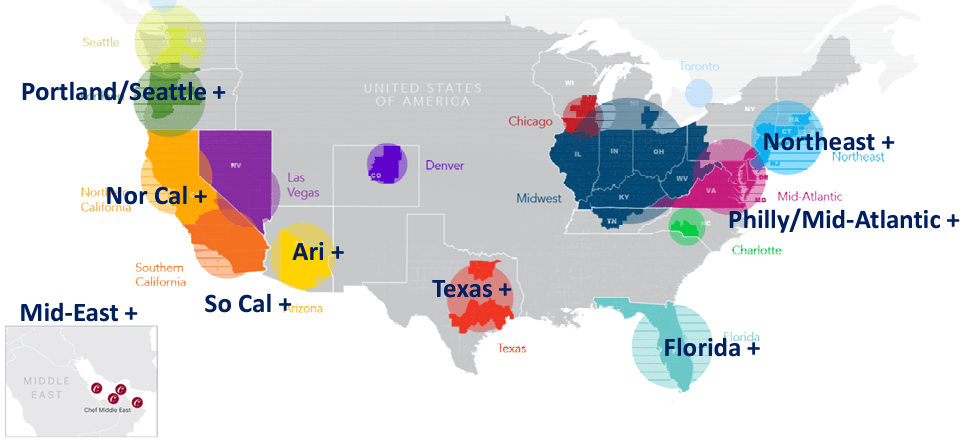

The Chefs' Warehouse ( CHEF ) is a wholesale food distributor, operating mostly in the United States and Canada. The company provides food products from more than 2500 suppliers mostly to restaurants through over fifty distribution centers. In the United States, Chefs' Warehouse has a focus on building extensive networks in select geographical areas, improving efficiency in the areas as the networks grow locally. The strategy of a focus in geographical network creation is in line with many competitors’ strategy - for example, food distributor SpartanNash focuses on the east side of the United States in select locations, and Sysco focuses on acquiring businesses in the fragmented industry similar to Chefs' Warehouse, providing a comprehensive offering. Chefs' Warehouse's geographical areas are concentrated in multiple parts of the United States:

Chef's Warehouse Q2 Investor Presentation

{kind=link}

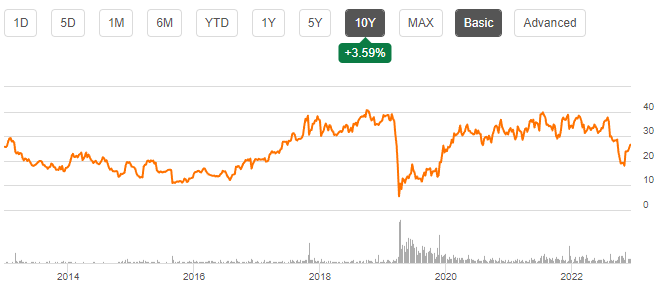

To scale the distribution networks, Chefs' Warehouse does constant acquisitions boosting the long-term revenue and earnings level. The valuations of the acquisitions are often with at least partly uncertain terms, though, as press releases about the acquisitions are in my opinion limited in information. The strategy revolving largely around acquisitions seems to have worked quite poorly historically, at least when looking at realized returns on the stock – the company doesn’t have cash flows for dividends, and the stock has only appreciated by 4% in the past ten years:

Ten Year Stock Chart (Seeking Alpha)

{kind=link}

A Long-Term Financial View

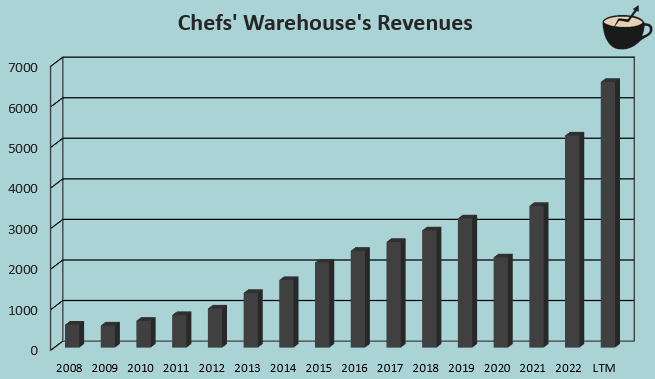

Due to the strategy of acquisitions, Chefs' Warehouse has grown impressively. From 2008 to LTM figures, the company’s revenue CAGR is 18.1%:

Author's Calculation Using TIKR Data

{kind=link}

As the growth is maintained through constant acquisitions, Chefs' Warehouse’s organic growth seems very modest. In the company’s Q3 earnings call , CEO Christopher Pappas mentioned a target of an annual organic growth between 4% and 6% in coming years. The target seems achievable through cross-selling between Chefs' Warehouse and recently acquired companies. I suggest to keep a close eye on the company's organic growth instead of overall revenue growth level.

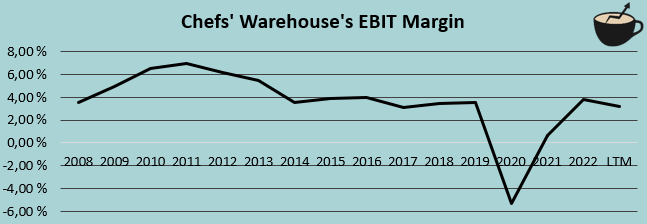

When excluding the pandemic’s negatively affected margins in 2020 and 2021, Chefs' Warehouse’s average EBIT margin from 2008 to 2022 has been 4.5%. The company’s current margin is well below the figure at 3.2%, but as Chefs' Warehouse is focusing on lowering capex, driving operational improvements in acquired businesses, and growing in scale, long-term margins should in my opinion be able to grow back to historical levels. Currently, the company guides for a long-term adjusted EBITDA margin target of mid-6% to 7%, compared to a 2023 middle point guidance of 5.7%.

Author's Calculation Using TIKR Data

{kind=link}

Acquisition Strategy Doesn’t Seem to Create Value

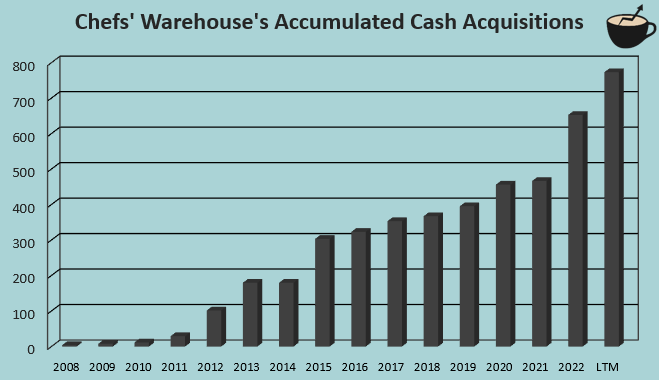

As can be seen from the stock price’s history, the acquisitions don’t seem to have created shareholder value – in the past ten years, the stock has stayed stagnant without a dividend, as cash flows are mostly spent on acquisitions. The company has had to even use equity as a way of financing, diluting outstanding shares from a count of 21.8 million in 2013 to 37.5 million in 2022. On top, Chefs' Warehouse has drawn a significant amount of long-term debt to finance the strategy – the company’s balance sheet reveals $677 million of long-term debt, of which $12 million is in the current portion.

Over the period from 2008 to the current date, Chefs' Warehouse’s cash acquisitions add up to $773 million, on top of which equity financing has represented a significant sum – with the stock price of $26.58 at the time of writing, the dilution from 2013 to 2022 represents a value of $417 million. If assuming that the entire dilution is due to acquisitions, the total amount spent on acquisitions from 2013 to the current date stands at approximately $1089 million. Compared to the current enterprise value of $1.7 billion, the made acquisitions make up most of Chefs' Warehouse’s current value.

Author's Calculation Using TIKR Data

{kind=link}

Still, the strategy does have some benefits. The acquired companies have cross-selling opportunities with Chefs' Warehouse’s existing business, a larger distribution network helps the company realize economies of scale, and integrating the acquisitions into Chefs' Warehouse’s larger operations can improve the acquisitions’ value due to a better cost control. These factors still seem to be priced into the acquisition prices though – the food distribution industry already has industry-consolidating competitors such as Sysco. Chefs' Warehouse doesn’t usually communicate the acquisition prices in press releases, giving quite a limited view to single acquisitions’ valuations and financials.

My Financial Estimates Signal Downside

The forward P/E multiple of 21.7 at the time of writing seems quite high for Chefs' Warehouse – the figure seems to price in a good amount of organic growth, as the earnings yield is around the same as current government bond yields in the United States.

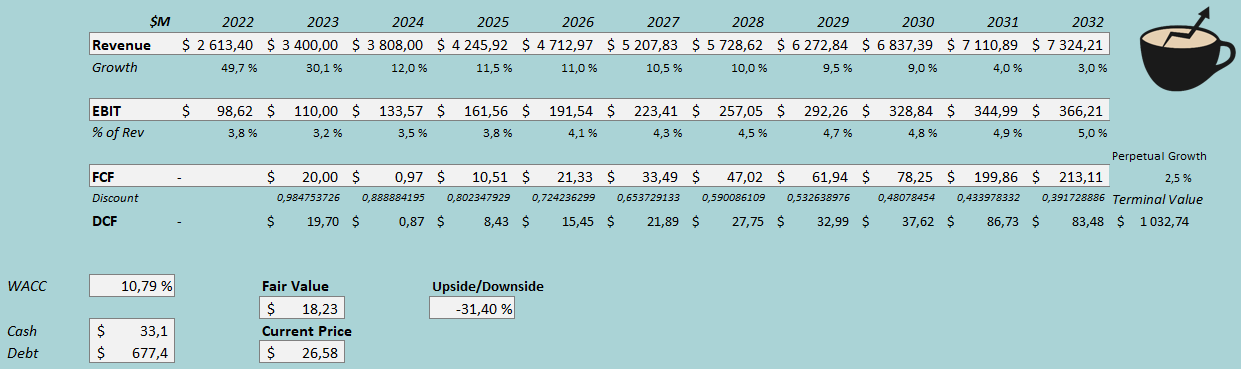

To get a better understanding of the valuation and to demonstrate a seemingly poor risk-to-reward at the current price, I constructed a discounted cash flow model in my usual manner. In the model, I factor in further acquisitions into revenues and free cash flow as they seem to be integral in the current management’s operating model. Due to recent large acquisitions, Chefs' Warehouse should grow fast in 2023, as it has done in the first three quarters – I estimate revenues of $3.4 billion for the year, in line with the management’s guidance. After the year, I estimate the growth to continue through slight organic growth and some acquisitions – for 2024, I estimate a growth of 12%, that slows down in steps as acquisitions slow down, with the acquisition strategy having its end in 2031 into an eventual perpetual growth of 2.5%.

For the EBIT margin estimates, I believe that a larger scale and the capex improvement should be able to grow Chefs' Warehouse’s margins back into a better level. I estimate the EBIT margin to scale slowly into a figure of 5.0% in 2032, which seems to be in line with the guided adjusted EBITDA margin of around 7%. As the acquisitions slow down through the years, I estimate an improving cash flow conversion. The cash flow conversion should be poor due to the acquisitions, but I estimate slightly positive values throughout the years. As the acquisitions stop in the model in 2031, the cash flow conversion improves massively.

With the mentioned estimates along with a cost of capital of 10.79%, the DCF model estimates Chefs' Warehouse’s fair value at $18.23, around 31% below the stock price at the time of writing – the stock is priced for more than I am ready to estimate from Chefs' Warehouse’s financials.

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the most recent reported quarter, Chefs' Warehouse had $11.4 million in interest expenses. With the company’s current amount of interest-bearing debt, Chefs' Warehouse’s annualized interest rate comes up to 6.72%. Chef’s Warehouse leverages a very high amount of debt, and I estimate the company’s long-term debt-to-equity ratio to be high at 50%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.47% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Chefs' Warehouse’s beta at a figure of 1.99 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 16.53% and a WACC of 10.79%.

Potential Bullish Drivers

My base scenario for Chefs' Warehouse signals a low risk-to-reward. The stock could still have bullish potential, if my financial estimates are exceeded. Most notably, I believe that the most notable factor could be that future acquisitions are made with widely cheaper prices than I anticipate and the company has done historically - as interest rates are higher than historically, Chefs' Warehouse could find better deals than it has historically done. It is quite tough to monitor the acquisitions' financials, though, as they're often reported with limited financial information.

Also, a lower cost of capital would make my DCF model fair value estimate largely higher. The high beta of 1.99 seems to be partly a result of a leveraged balance sheet, as operationally, Chefs' Warehouse doesn't seem to correlate too much with the macroeconomic situation. The model could potentially be flawed in the WACC due to Yahoo Finance's high beta estimate - if Chefs' Warehouse's earnings prove to be stable in coming quarters despite a tough macroeconomic situation, the cost of equity could be in need of a revisit.

Takeaway

I don’t think that Chefs' Warehouse’s current stock price reflects a good risk-to-reward. The company trades at a forward P/E around double of competitor SpartanNash’s figure, which I recently wrote a more bullish article on. Chefs' Warehouse’s strategy of acquisitions also doesn’t seem to have resulted in a very good result for investors, as the acquisitions eat up cash flows. The company has initiatives for lowering capex and slightly improving margins, but the improvements are in my opinion more than priced in into the stock price. For the time being, I have a sell rating for the stock.

For further details see:

The Chefs' Warehouse: An Expensive Strategy