CHEF - The Chefs' Warehouse: Differentiation Driving Value

2023-06-13 14:47:40 ET

Summary

- The Chefs' Warehouse, Inc. is a premium food distributor with a focus on high-quality, artisanal products and strong supplier relationships, catering to the growing consumer preference for unique and sustainable food options.

- The company has experienced impressive revenue growth, with a CAGR of 15%, and has opportunities for further growth through e-commerce, expansion of food categories, and M&A activities.

- Despite poor margins in the foodservice industry, Chefs' profitability is higher than its peers.

- CHEF is trading at a premium to its peers, but not sufficiently so, in our view, given the superiority and trajectory.

Investment thesis

Our current investment thesis is:

- The Chefs' Warehouse, Inc. (CHEF) has developed differentiation in a relatively uniform industry through a focus on high-quality goods which are not easy to source.

- The company has built a discursive relationship with its clients to support menu changes and sourcing of products, whereas the broad line segment is wholly focused on price.

- The company's large national footprint and supplier relationships make its position difficult to challenge.

- Margins are not great from an absolute perspective but the company performs far better than any of its peers.

Company description

The Chefs' Warehouse is involved in the distribution of specialty food products in the United States, Canada, and the Middle East. They offer a wide range of approximately 55,000 stock-keeping units, including artisan charcuterie, specialty cheeses, unique oils and vinegars, truffles, caviar, chocolate, and pastry products.

In addition, they provide center-of-the-plate products like custom-cut beef, seafood, hormone-free poultry, cooking oils, butter, eggs, milk, and flour.

Share price

CHEF's share price has made respectable gains in the last decade, although has faced a degree of volatility throughout the period. This is a reflection of its overarching trajectory, although changing sentiment and expectations throughout the period.

Financial analysis

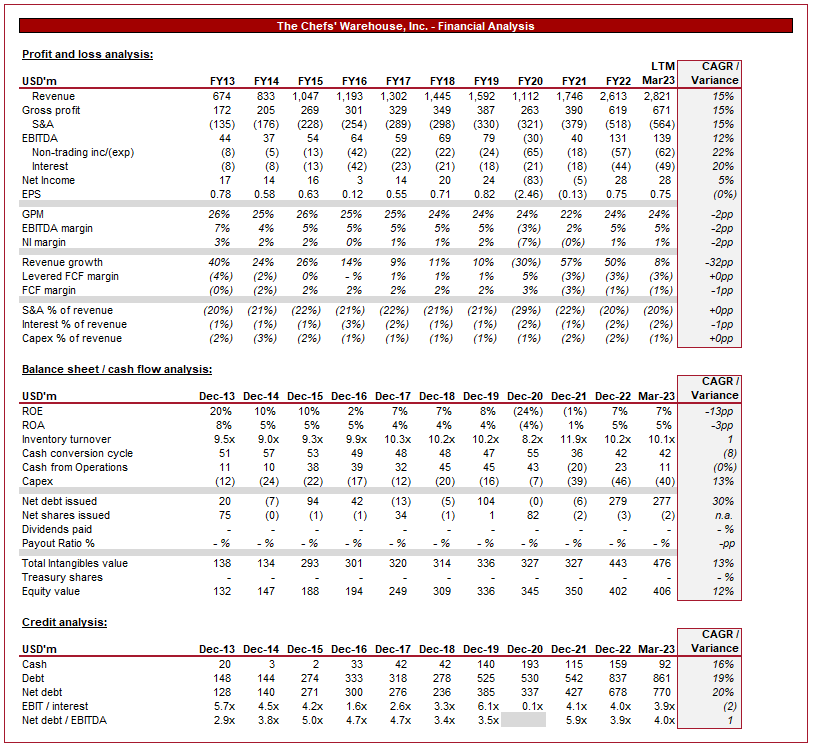

Chefs' warehouse financial analysis (Tikr Terminal)

{kind=link}

Presented above is CHEF's financial performance for the last decade.

Revenue & commercial factors

CHEF has grown revenue at an impressive rate, delivering a CAGR of 15%. The company has only had 2 years of growth less than 10% (one of which was impacted by Covid-19), reflecting the impressive trajectory the company is currently on.

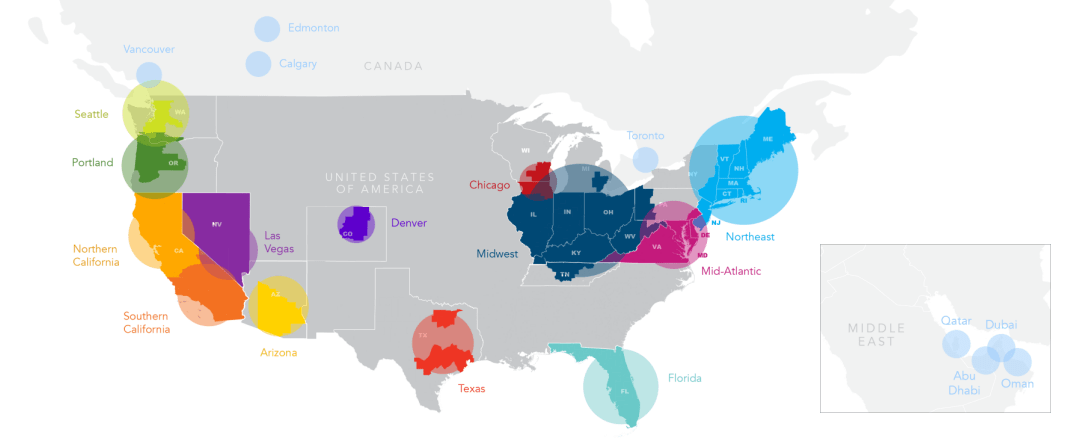

The business operates across the US, with a large number of distribution centers and a diversified range of suppliers. This allows the business to flexibly meet changing levels of demand (impacted by growth, seasonality, etc), as well as provide value through optionality.

Geographical reach (The Chefs' Warehouse)

{kind=link}

CHEF operates with a different business model to other food services businesses in the US, namely, it looks to be a premium option in the marketplace. Management's focus is on having a workforce with strong culinary experience, both through recruitment and training. The intention is to support clients in making an informed decisions (relationship-driven, rather than buyer/seller), which is a far more important factor when dealing with upmarket establishments. Many upmarket restaurants pride themselves in the quality and sourcing of its foods, and I believe this is considered a selling point, and so CHEF's ability to collaborate with its clients is perceived to be a value-add.

In conjunction with this, CHEF's focus is on both sourcing high-quality products and ensuring they have a wide breadth of suppliers in key produce. Given that the products are of high quality, many of the suppliers are niche. This gives CHEF leverage with the suppliers, but importantly also adds greater value through their ability to discover and curate an offering for its clients. The majority of its clients will not have anywhere near the skills or time required to find many specialist products, relying on CHEF's expertise to guide them.

Finally, the business model allows CHEF to do the basics well. The company still provides a broad line selection, as well as the scale of many of the largest broad line distributors. As a result of this, CHEF has the scale the average specialty lacks while being able to serve basic needs in conjunction with specialty goods.

Foodservice is estimated to be a $297bn industry, with c.15k suppliers. For this reason, the industry is highly segmented, with local suppliers supporting local businesses. Despite this, there are several large players in the market (some of which specialize), including United Natural Foods ( UNFI ), US Foods ( USFD ), Performance Food ( PFGC ), SpartanNash ( SPTN ), and The Andersons ( ANDE ). The attractiveness of the market for CHEF is that there is a greater fragmentation among specialists due to their nature, giving the company scale benefits, as well as scope for M&A.

Further, CHEF remains focused on specialist restaurants, which comprise c.35% of the market. Chains are generally focused on low-cost, bulk purchases and so are not compatible with CHEF's offering.

Further, there is a growing consumer preference for unique, high-quality, and artisanal food products. This has been driven by increased awareness of dietary requirements and health issues. As consumers become more food-savvy and seek novel culinary experiences, CHEF is primed to benefit from changing menu choices.

In conjunction with this, there is a growing trend towards locally sourced and sustainable food products. This is partially due to the factors above, as well as the desire to be more sustainable due to environmental concerns. CHEF's investment in strengthening its partnerships with suppliers and promoting sustainable practices can support preferential sourcing as demand increases.

The following are a handful of CHEF's current customers. Unsurprisingly, many are upmarket establishments, targeted at wealthy individuals. The nature of these services means the quality of food is critical, which should give Chefs' sticky revenue and growth in line with their development.

Clients (Chefs' Warehouse)

A business such as this can grow organically in two ways. Acquisition of new customers and increasing spending per customer.

An area of growth for CHEF is e-commerce. The company launched a new website in August 2022, allowing the business a range of benefits, including:

- Data collection, which can help make supply chain decisions to optimize inventory.

- Convenience for clients through investment in the experience.

- Increased online presence to drive greater sales.

34.5% of specialty category sales were through the company's site, compared to 17% in 2019. This suggests noticeable improvement, as well as scope for new customers.

Further, growth will also be supported by increasing the number of food categories, such as fresh seafood, as well as an increase in the number of brands.

M&A also represents a key opportunity for the business and an area we believe Management should focus on. The fragmentation of the market represents a key opportunity to conduct regular tuck-in transactions.

Most recently, the company acquired "CHEF" in the Middle East, giving the company exposure to the UAE, Qatar, and Oman, which are all growing nations. The company has an EBITDA-M of c.7% (accretive to CHEF) and was acquired for $110m (also accretive for CHEF). This transaction on paper looks to be a good deal. CHEF acquired 3500 customers and 4,500 additional SKUs.

Economic & external consideration

There is a risk that CHEF faces a slowdown in sales due to economic conditions. With high inflation and rising rates, we are seeing consumers' finances squeezed, contributing to lower discretionary spending. In conjunction with this, businesses are struggling with rising costs and softening sales.

The impact on CHEF could be a reduction in demand, as restaurants face lower demand for foods. We are not overly concerned with this as it should be a near-term risk, but independent restaurants look worst placed to weather the impact.

Margins

Margins in the foodservices industry are not good. CHEF has an EBITDA-M of 5% and a NIM of 1%. The company has seen almost no improvement in the last decade, reflecting the high levels of competition and prices demanded by customers.

Due to the poor margin on costs, it is critical for a business such as CHEF to generate operating cost leverage. Despite Management stating this is a focus for them, we have not yet seen the benefits. Revenue has more than doubled since FY15 levels yet margins are identical. A portion of this is likely due to the offsetting impact of inflationary pressures.

The adoption of technology and automation also has the scope to enhance operational efficiency, inventory management, and customer service. This is another opportunity for improvement.

Balance sheet

CHEF has a ND/EBITDA ratio of 4x, which is quite high in our view but reflects the large physical investment required in distribution facilities. With interest payments representing 2% of revenue, we are not overly concerned.

What is more concerning, however, is the poor cash generation relative to capex. Despite no distributions to shareholders, the company has seen declining cash (partially due to the acquisition of CME). This represents a major stumbling block for executing an M&A strategy. For this reason, if growth is to continue through investment, we do not expect distributions to be initiated.

Outlook

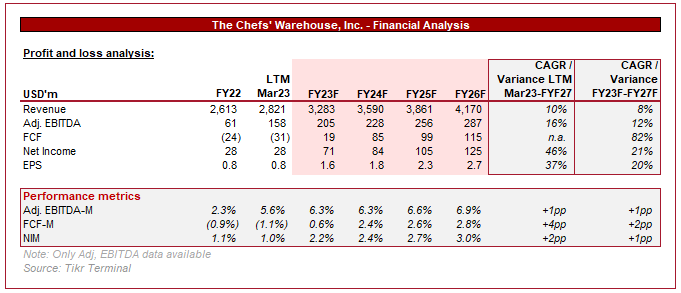

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting strong growth to continue, taking a conservative view of 8%. We concur with this assessment although believe the current trajectory implies a rate closer to 12%.

Margin improvement is also forecast although not to a material level. This looks reasonable given the difficult industry conditions.

Peer analysis

In order to assess the company's relative performance, we have compared its profitability to the peers stated above.

The average EBITDA margin of the group is 2.2%, far below CHEF's current level. This implies the company has managed to achieve a premium for the service it offers while still delivering an impressive growth rate (c.(3)% 5Y growth rate relative to the peers).

{kind=link}

Valuation

CHEF is currently trading at a NTM EBITDA multiple of 10x. This compares to a peer average of 8.2x, implying a c.20% premium.

With almost double the margins and a slightly lower growth rate, this premium looks justified. Many of the peers target the broad line, where pricing is the key value driver. For this reason, we could see the margin delta increase over time rather than decline, as competition drives down prices. Growth will be the trade-off, as the premium segment will not perform as well, especially if the current inflationary pressures have a lasting impact. This said, we are not overly concerned. The industry is mature on an organic basis, the growth delta is not material enough to compensate.

CHEF has achieved differentiation and thus built a moat (to the extent one can in such an industry). This is not an unchallenged position but we feel its supplier and customer network is not easily challenged due to the scale, protecting the business in the near term. Due to the poor profitability and thus FCF generation of the industry, competitors are not in a position to just outspend CHEF.

For these reasons, we believe a premium is justified. CHEF is in a position to defend its business model should its competitors attempt to take market share.

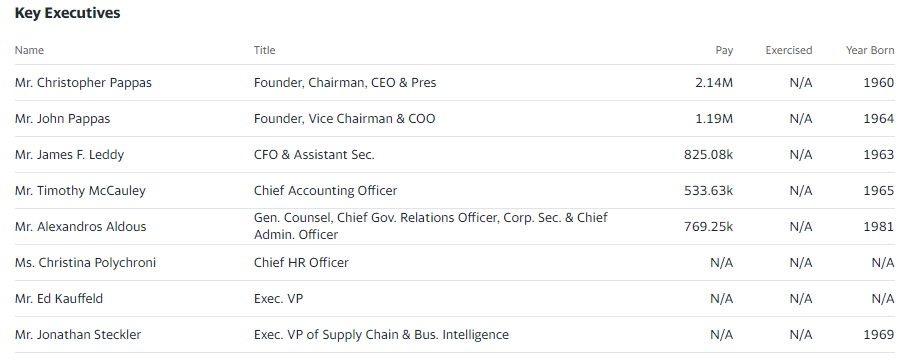

Management

It should be noted that Founders Christopher and John Pappas have strong control over the business, acting as Chairman, Vice Chairman, CEO, and COO. This may be concerning to some but thus far, they have delivered. Christopher owns c.6.5% of the business and John owns 3.4%.

Executive team (Yahoo Finance)

{kind=link}

Key risks with our thesis

The risk to our current thesis is the potential for slowing demand impacting investor sentiment. Thus far, the company has shown impressive resilience and maintained its current trajectory. Investors are pricing this premium based on continued outsized growth along with its market-leading profitability. If revenue slows sufficiently, questions must be asked if the margin premium justifies the growth delta.

Final thoughts

We are not the biggest fan of the foodservice industry. Margins are terrible and the scope for improvement is limited. This impacts the possible development opportunities to achieve improved value. CHEF has done a fantastic job to differentiate itself and achieve good margins. We see no immediate challenge to its current position and growth reflects that in our view.

For further details see:

The Chefs' Warehouse: Differentiation Driving Value