PLCE - The Children's Place: Business Performance Will Likely Revert To The Mean

2023-09-21 06:59:00 ET

Summary

- The Children's Place stock is currently undervalued due to recent challenges with high-cost input inventory and weaker-than-expected earnings.

- The company is expected to return to profitability in the second half of 2023, which could lead to a significant increase in its stock price.

- PLCE's management has provided guidance for adjusted net earnings of at least $5 per share for the second half of the year.

Investment Thesis

The Children's Place ( PLCE ) is currently being heavily discounted by the market due to a string of unfortunate events in 2022. However, we believe that the inflated inventory costs stemming from cotton and freight have subsided, and the company's business performance will revert to its historical mean. We anticipate that the upcoming quarter will serve as a turning point for the company, as it will be the first quarter to restore gross margins, generate free cash flow, and reduce leverage on the balance sheet.

During its Q2'23 earnings call , the management team reaffirmed its guidance for at least $5 adjusted EPS for the second half of 2023. We have taken the following steps to cross check management's guidance:

- We have cross-verified that both cotton prices and freight prices have returned to normal levels.

- We have also verified that from 2008 to 2019, PLCE consistently generated EBITDA of over $100 million in the second half of the year. This indicates that even during financial crises, the business continued to generate positive cash flows.

- Furthermore, we have identified no significant changes in the competitive landscape of the children's apparel business.

- Most retailers went into the 2H with a healthy inventory, so there is no promotional pressures as well.

After PLCE's business reversion back to the mean, its stock will appear very attractive, especially considering it will generate at least $5 adjusted EPS in the second half of the year, while the stock is currently trading at only around $26. We believe that this significant disconnect between PLCE's near-term prospects and its stock price presents a compelling investing opportunity for investors.

What caused the cheap valuation at PLCE

Children's Place has recently reported a string of bad earnings. In Q4'22, the company reported a Non-GAAP EPS of -$3.87, which was a significant decline from the Non-GAAP EPS of $1.43 in 2021Q4. In Q1'23, the company reported a $2 per share loss, which was even more of a decline from the $1.05 per share loss in Q1'22. In Q2'23, the company reported Non-GAAP EPS of -$2.12.

So what happened to PLCE's recent reported earnings and why are they so bad? Children's Place's 2022 && early 2023 operating results were adversely affected by a combination of unprecedented input costs, a sharp rise in cotton prices, and increased expenses related to air freight and container transportation. These factors led to higher costs for the company, which resulted in lower profits.

To make it worse, many retailers carried too much excessive inventory going into Q4'22 and the excess inventory as made it even worse for retailers. Many retailers have had to offer discounts on inventory sales in order to clear through the high-input cost inventory. This has squeezed margins for many retailers including PLCE. I cited the following online sources to help investors to digest the inventory glut issue happened in 2022.

- Retailers' biggest holiday wish is to get rid of all that excess inventory. ( source )

- How 2022 became the year of the inventory glut. ( source )

Its business performance will restore back to mean in 2H 2023

The good news is that all the previously mentioned unfortunate events are now in the past, and PLCE's business is on the cusp of a turning point.

PLCE's management mentioned in its latest earnings call that its adjusted net earnings will be more than $5 for the second half.

For the back half of 2023, the company continues to expect to deliver double-digit operating margins, driven by strong product offerings, decreased input costs embedded in inventory, the benefit of reduced inventory levels and strong expense discipline.

Our effective tax rate is expected to be approximately 20% to 21%. Adjusted net earnings per diluted share are expected to be in the range of $5 to $5.25.

We have taken the following steps to cross check management's guidance.

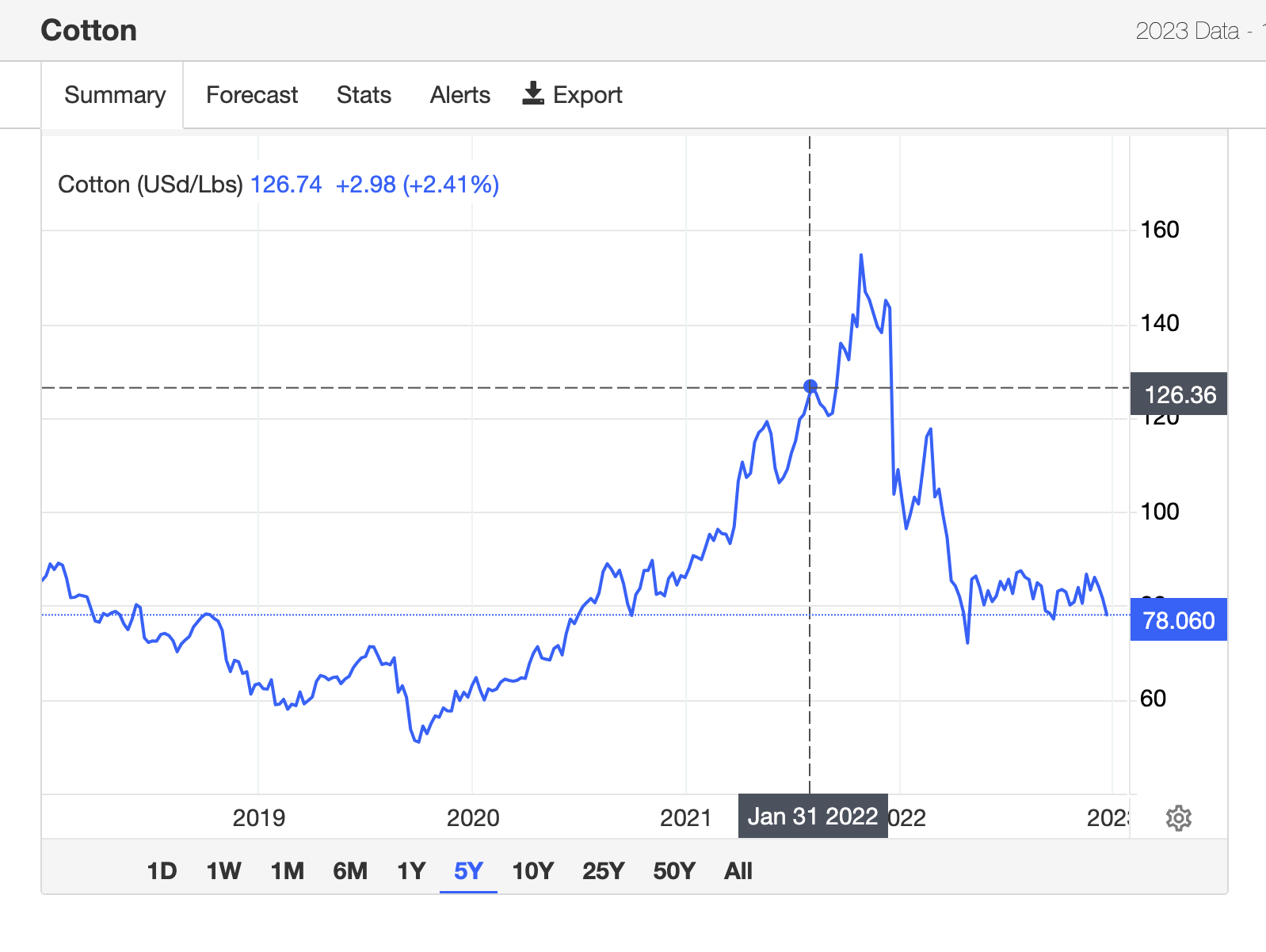

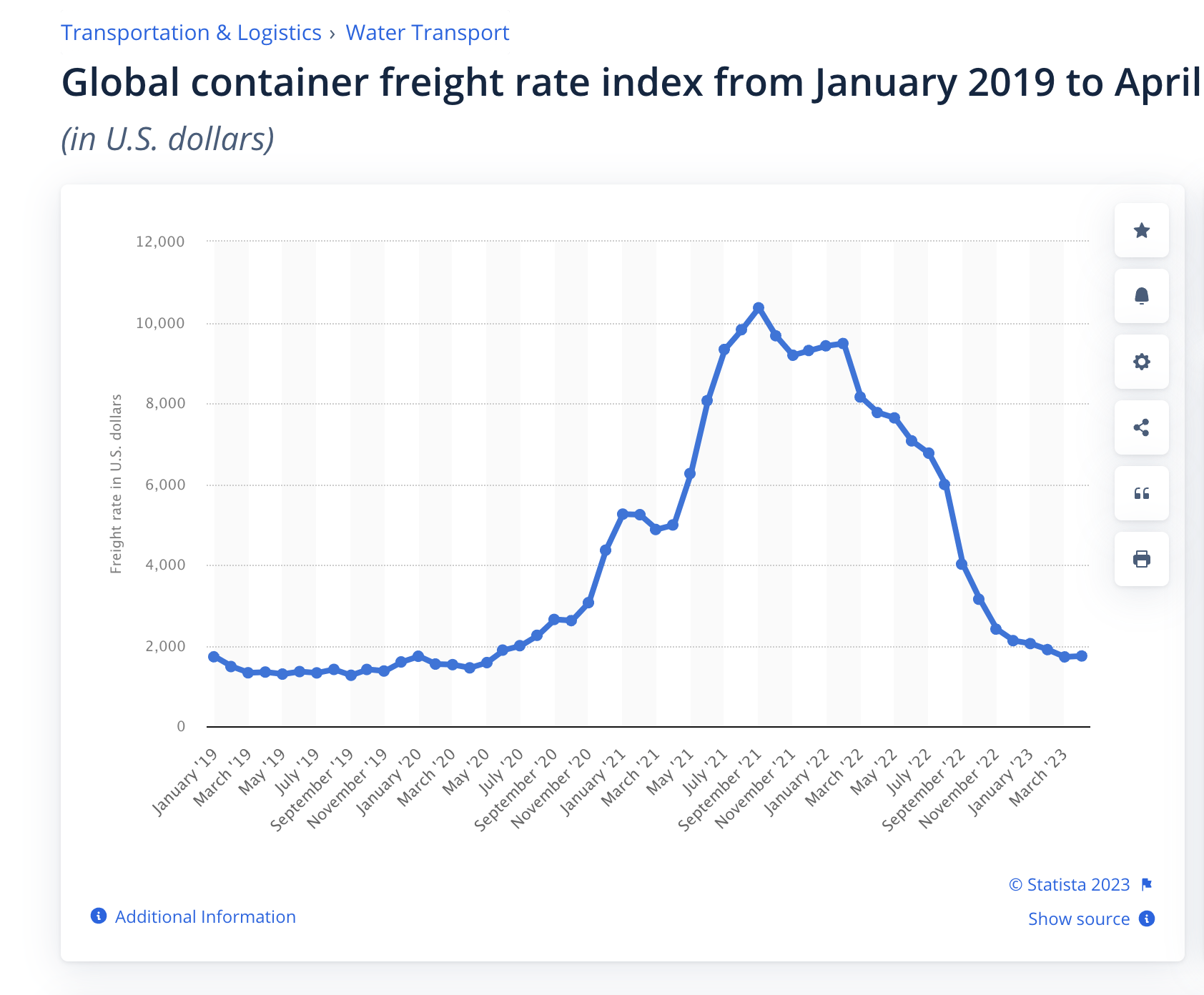

One, we have cross-verified that both cotton prices and freight prices have returned to normal levels. Cotton and fright prices are the major cost for its inventory and this means that its inventory cost will return back to normalized level.

The charts below shows that the cotton price spiked in 2022 and then normalized in late 2022. This is consistent with management's discussion of its high input cost inventory.

{kind=link}

The charts below shows that the global container freight rate price remain elevated during the pandemic and then normalized in late 2022. This is consistent with management's discussion of its high input cost inventory.

{kind=link}

Two, we have also verified that from 2008 to 2019, PLCE consistently generated EBITDA of over $100 million in the second half of the year.

This data indicates that even during financial crises, the business consistently generated positive cash flows. In the current high-interest rate environment and amid concerns of a future recession, this data serves as evidence that PLCE's business is not severely impacted by economic downturns, as children continue to grow and require new clothes every year.

Three, furthermore, we have identified no significant changes in the competitive landscape of the children's apparel business.

We haven't identified any significant changes that would have a negative impact on the competitive landscape of the children's apparel business for PLCE. Notably, in 2019, one of PLCE's competitors, Gymboree, went bankrupt, which should have a positive impact on PLCE's business.

Four, most retailers went into the 2H with a healthy inventory, so there is no promotional pressures as well.

We have checked the latest earnings reports from Target (TGT), Walmart (WMT), Nordstrom (JWN), and Macy's (M). They all indicate a trend of reduced year-over-year inventory levels and a healthy inventory position entering the second half of the year. This implies that there will likely be less heavy promotional activity this year, and retailers are expected to maintain healthy gross margins, including PLCE.

How to value PLCE after 2H 2023

We will analyze PLCE's historical earnings and valuations to arrive at a conservative estimate of the company's value after input costs normalize in 2024. Our estimate does not factor in the potential sales growth from PLCE's initiatives, such as its partnership with Amazon, the consolidation of the children's apparel sector (With recent bankruptcies of competitors such as Gymboree, Crazy 8, and Payless, PLCE stands as the last remaining specialty competitor in malls at lower price points).

The table below summarizes PLCE's earnings and values before the pandemic and my estimate for 2024.

| (In thousands, except EPS) |

| FY2024 (Estimate) |

| FY2019 |

| FY2018 |

| FY2017 |

| Total Revenue |

| 1,870,667 |

| 1,870,667 |

| 1,938,084 |

| 1,870,275 |

| Gross Profit |

| 655,305 |

| 655,305 |

| 683,596 |

| 711,355 |

| Operating Income |

| 96,358 |

| 96,358 |

| 111,328 |

| 161,510 |

| Net Income |

| 73,300 |

| 73,300 |

| 100,960 |

| 84,698 |

| EPS |

| $5.95 |

| $4.71 |

| $6.1 |

| $4.82 |

| Basic Shares Outstanding |

| 12.3M |

| 15.5M |

| 16.5M |

| 17.6M |

| Net cash provided by operating activities |

| 177,902 |

| 177,902 |

| 139,914 |

| 214,383 |

| Capital expenditures |

| (57,502) |

| (57,502) |

| (71,114) |

| (58,657) |

| Free Cash Flow |

| 120,397 |

| 120,397 |

| 68,800 |

| 155,726 |

| Market cap at year end |

| 725.7M |

| 934.0 M |

| 1.6B |

| 2.7B |

| PE |

| 10 |

| 12.7 |

| 16 |

| 31 |

| Price/FCF |

| 6 |

| 7.7 |

| 23 |

| 17 |

Based on the estimated 2024 earnings per share ((EPS)) of $5.95 and a price-to-earnings ((PE)) ratio of 10 or price-to-cash-flow ratio of 6, PLCE could be valued at $725.7 million in 2024.

Risk

I would like to emphasize the potential risks associated with this investment idea. My thesis is based on the expectation that PLCE will return to profitability in the latter half of this year. The hypothesis is that this regained profitability will enable the company's management to repurchase its shares at a low price, in case the market fails to recognize its value.

However, it is crucial to consider the risk if PLCE failed to achieve profitability in the latter half of 2023 or even in 2024. One key concern is the company's weak balance sheet, which currently holds only $16 million in cash. If PLCE encounters another retail inventory glut event or experiences another spike in input costs in the near term, it may not have the financial capacity to withstand these external challenges. Such circumstances could severely test the company's financial strength and stability.

Summary

PLCE is currently facing challenges related to high-cost input inventory, which has contributed to its depressed stock prices. Furthermore, the company has been reporting weaker-than-expected earnings, which has further impacted its market valuation. However, there is an expectation that PLCE will soon return to a normalized level of profitability. As PLCE moves towards profitability, there is a possibility that the market will respond positively, leading to an increase in its market valuation.

For further details see:

The Children's Place: Business Performance Will Likely Revert To The Mean