PLCE - The Children's Place Is A 'Buy' As Headwinds Turn To Tailwinds

2023-09-21 16:42:26 ET

Summary

- The Children's Place, Inc. has multiple drivers including a partnership with Amazon and improved marketing.

- Lower cotton, freight, and occupancy costs should drive earnings results in the 2H and into next year.

- The stock looks inexpensive and does not take into account its ongoing turnaround.

The Children's Place, Inc. ( PLCE ) looks like an intriguing retail turnaround story, as cotton and freight headwinds turn to tailwinds and the company moves to a more digital retailer.

Company Profile

PLCE is a children's apparel retailer that operates both in the U.S. and internationally, mostly in Canada. It primarily sells apparel for girls and boys (sizes 4-18), toddler girls and boys (sizes 6 months-5T), and baby (sizes 0-24 months). Its Sugar & Jade brand, however, targets tween girls, while PJ Place sells sleepwear aimed at Gen Z and Millennial consumers.

The company operates under several brands, including The Children's Place, Place, Baby Place, Gymboree, Sugar & Jade, and PJ Place. It had 596 stores in the U.S. and Canada at the end of fiscal Q2, 2024. The company also operates e-commerce stores under its branded names.

In addition to direct to consumer sales, PLCE also has a wholesale relationship with Amazon ( AMZN ). Meanwhile, the company also has over 200 international points of distribution with five partners operating in 15 countries

Opportunities and Risks

One of PLCE's biggest opportunities is its partnership with Amazon. The company began to lean into AMZN as a distribution channel during the pandemic, and it has really been blossoming for the company. AMZN obviously gives PLCE a big audience of buyers, and the company has built out its advertising strategy around promoting its namesake and Gymboree brands on the website. This includes marketing campaigns featuring creative influencers.

So far, its AMZN initiative appears to be working, with the company seeing sales and traffic up triple digits in Q2 versus a year ago.

On its fiscal Q2 earnings call , Brand President Maegen Markee said:

"The significant time and resources that we have dedicated towards building our Amazon marketplace since the beginning of the pandemic have resulted in another outstanding quarter. Amazon site sales and traffic were both up triple digits in Q2 versus Q2 of 2022. We participated in July Prime Day events, resulting in TCP's largest week on Amazon in our history. It's really incredible when we compare our relationship with Amazon today versus prepandemic. The progress that we have made on both sides has been transformational. And again, the exciting part is that we believe we have significant opportunity for continued wholesale growth in the back half of this year and beyond with this important partner."

Marketing in general, though, is another potential driver for the company. Prior to the pandemic, the company spent under 2% of its sales on marketing, well below the 5-7% of other omnichannel apparel brands. Today the company is moving into that 5-7% range and is becoming more comprehensive. In the past, it used mostly bottom-of-the funnel marketing techniques, which are used on customers that have shown intent to purchase. Today, it has expand to top of funnel activities to help build brand awareness and acquire new customers. Q2 was the fourth consecutive quarter of increased customer acquisition for the company, as a result of its revamped marketing strategy.

Store optimization has been another strategy being deployed PLCE, as it continues to close down underperforming mall stores and focusing more on digital. The company now has 40% less stores than it did in 2019. The company planned to close about another 100 stores this year, leaving it with 500 entering 2024. At that point, it should be mostly complete with its store optimization plans.

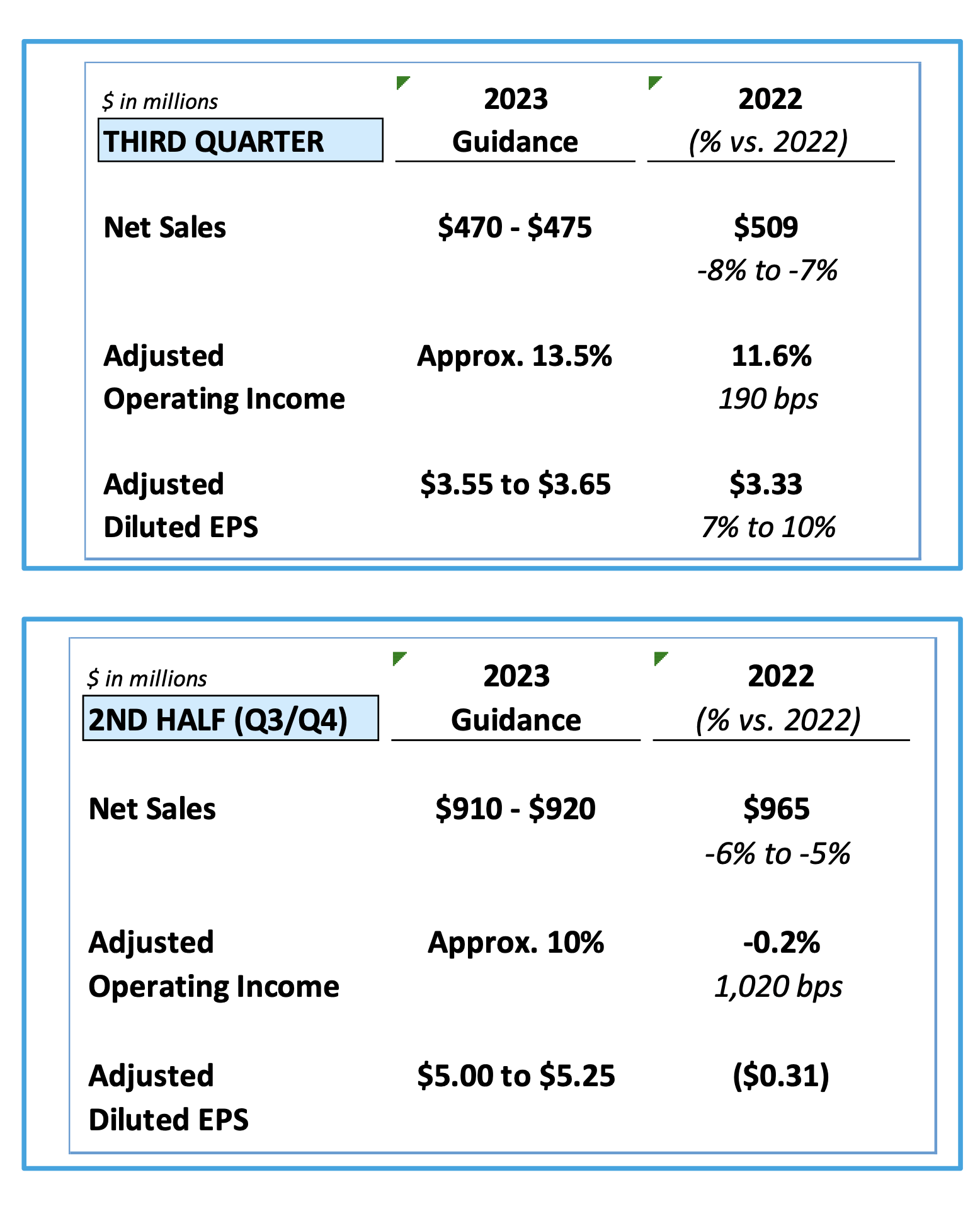

While the store optimization program decreases sales, it also significantly lowers occupancy expenses. This leads to much improved operating margins and higher earnings. This can be seen in the company's 2H guidance, where it is projecting revenue to decline by -5% to 6%, but for adjusted EPS to go from -31 cents to profits of between $5.00-$5.25.

{kind=link}

When it comes to risks, PLCE faces several. Chief among them is the economy and a slowdown in consumer demand. While children need clothes, it is also an area that families can cut back on as when they are hit by economic or inflationary pressures.

As with other apparel, the environment can also get more promotional when overall industry sales slow. PLCE's brands generally aren't strong enough to not get involved when the industry as a whole becomes more promotional. This, in turn, can hurt margins.

PLCE can also face cost pressures as well. High cotton prices impacted gross margins earlier, as did higher freight costs. Freight costs have come down, as have cotton prices, so these headwinds should begin to turn to tailwinds in the second half of this year into calendar year 2024.

Inventory risk is always a potential risk with apparel retailers. However, PLCE does expect it can operate at lower inventories as it moves to a more digital platform with less stores, which is a positive.

As a children's apparel retailer, PLCE also faces a unique risk in U.S. birthrates. Less births leads to less children, which leads to less sales of children apparel.

Valuation

PLCE currently trades at 10.2x the FY2024 (ending January) consensus EBITDA of $83.7 million and 6.9x the FY2025 consensus of $123.7 million.

From an EBITDAR perspective, it trades at 5x FY2024 my estimate of $169 million and about 4.4x FY2025 my estimates of $194 million. Note that EBITDAR takes out rent expense of about $80-85 million. Given that operating leases are now included as debt in the EV equation, EBITDAR is often a better metric to use for retailers.

It trades at a forward P/E of 30.7x the FY24 consensus of 92 cents and just at 7.0x the FY25 consensus of $4.05.

Revenue is expected to drop -4.7% this year, and then be around breakeven after that.

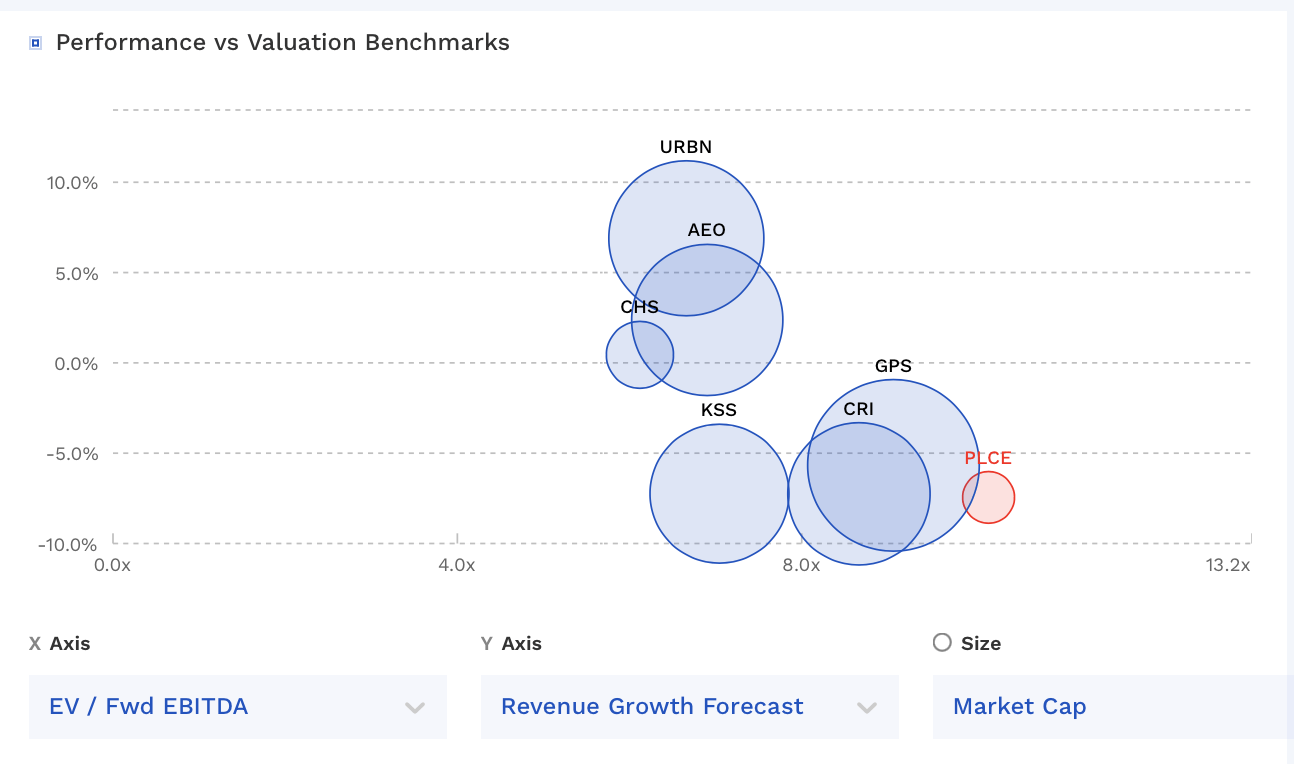

PLCE trades at a wide premium to its peer group on 2023 numbers, but towards the lower end based on 2024 numbers, given the jump in EBITDA and EPS it should see in 2024.

PLCE Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

At the end of the day, The Children's Place, Inc. is an operating margin turnaround story. The company should see a big boost to its earnings as cotton and freight headwinds turn into tailwinds. At the same time, it continues to reduce its store count, lowering costs and moving to higher-margin digital sales. Its initiative with AMZN is going strong, although it should be noted that these sales do come at lower margin. The company is also doing a better job with its marketing.

Overall, I think the turnaround at PLCE is taking hold, and at under 4.5x fiscal year 2025 EBITDAR, the stock looks inexpensive. There are risks to the stock, as the company is exposed to any economic weakness, but that appears largely priced into the stock at this point.

I rate PLCE a "Buy" with a $52 target, which is about a 6x multiple on FY25 EBITDAR.

For further details see:

The Children's Place Is A 'Buy' As Headwinds Turn To Tailwinds