PLCE - The Children's Place: Only Pain Ahead Following Consistent Declines

2023-11-06 04:22:02 ET

Summary

- The Children's Place's revenue has declined at an average (1)% rate, with increased competition and an inability to improve its value proposition being key factors.

- PLCE has faced numerous headwinds, including the rise of e-commerce, slowing birth rates, and intense competition. We have not seen a sufficient response from Management to improve its position.

- The Company is significantly underperforming its apparel peers, with limited quality characteristics. We consider this one of the worst businesses in the segment.

- PLCE’s valuation implies further downside is ahead, lacking a sufficient discount to its historical average.

Investment thesis

Our current investment thesis is that The Children's Place, Inc. (PLCE) is a low-quality company currently. It is facing a number of long-term headwinds, as price competition continues to increase, birth rates fall, and the business struggles to materially differentiate its brands. Compounding this is near-term headwinds, as economic conditions contribute to declining demand. PLCE's operational management has been a disaster, contributing to negative margins and a build-up of stock. We see limited scope for this stock to achieve long-term success and so suggest investors avoid it.

Company description

The Children's Place, Inc. is a leading specialty retailer of children's clothing and accessories in North America. With a focus on providing fashionable, high-quality products at affordable prices, the company operates a vast network of stores and an online platform, catering to infants, toddlers, and children up to 14 years old.

Share price

PLCE share price performance has been disappointing, losing almost 50% of its value during the last decade. The company has materially struggled, with minimal improvement and a negative outlook.

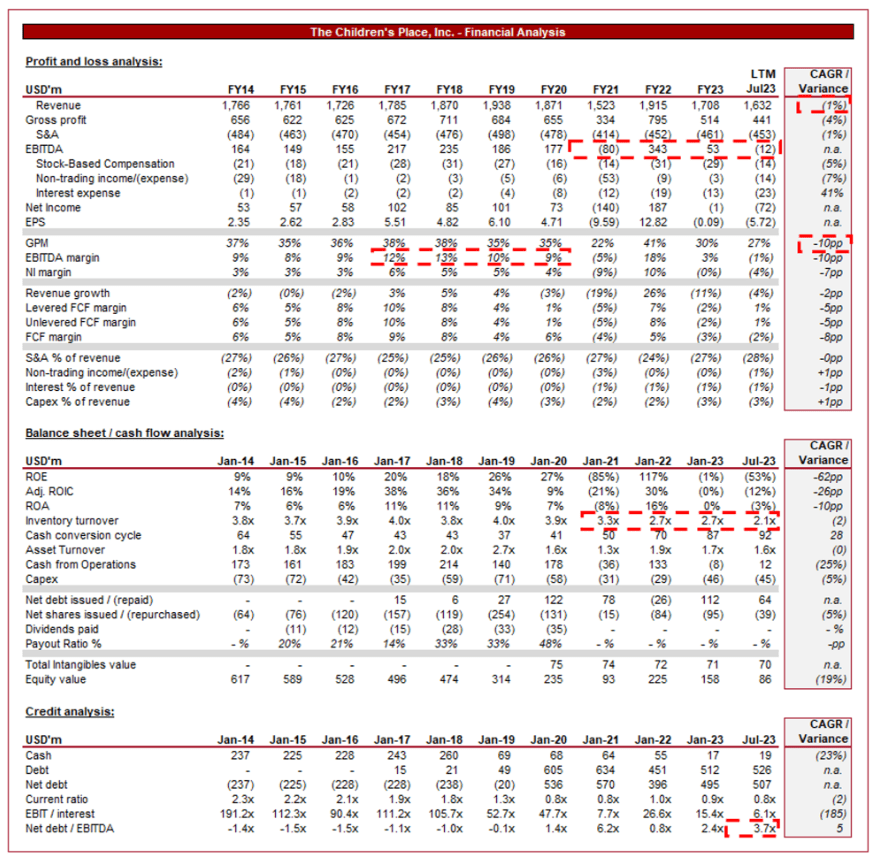

Financial analysis

{kind=link}

Presented above are PLCE's financial results.

Revenue & Commercial Factors

PLCE has struggled to achieve consistent growth, with 6 fiscal years of negative growth in the last decade. This trend has continued into the LTM period, with margins broadly following suit.

Business Model

PLCE focuses exclusively on children's apparel, catering to a specific market segment. It offers a wide variety of clothing, footwear, and accessories for infants, toddlers, and young children. This pure-play focus has allowed it to establish a strong brand identity in the children's retail market.

The majority of the products sold by PLCE are under its private label. Private label products yield higher profit margins as they eliminate the need for third-party brand markups, as well as allow for brand development and a superior relationship with their customers.

The company maintains control over its supply chain, from design and production to distribution. This vertical integration gives them the flexibility to respond to changing trends and customer demands effectively. This said, Management has poorly responded to recent shifts in demand, contributing to inventory build-up and a requirement to heavily discount in order to balance working capital position.

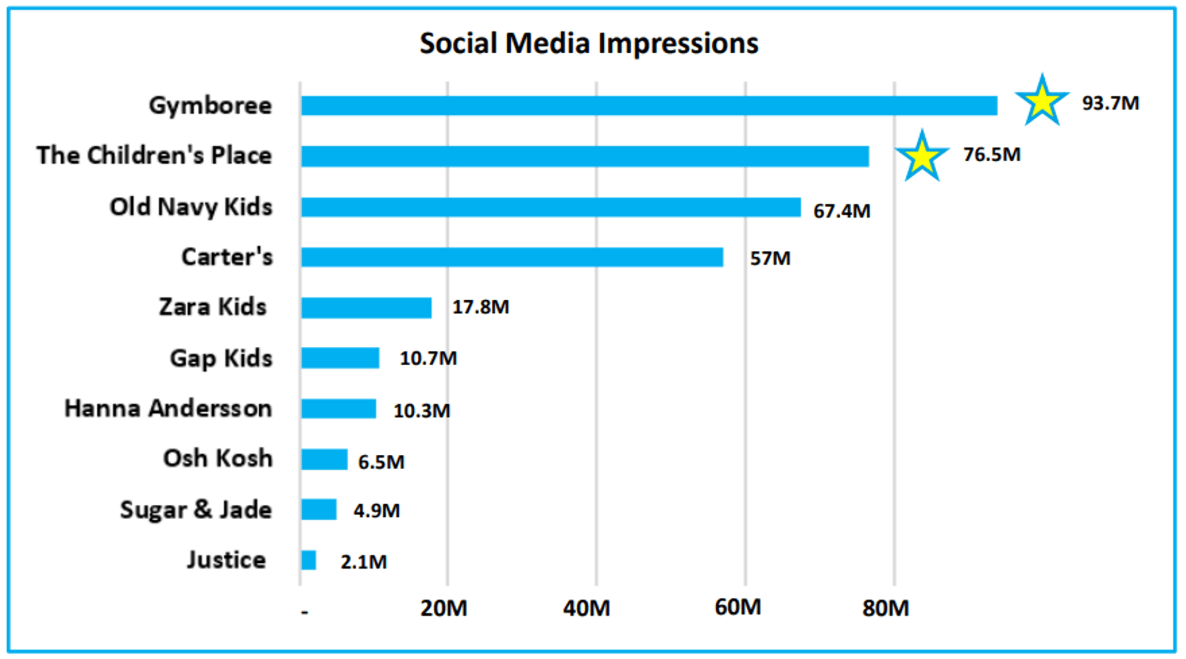

PLCE invests heavily in online marketing and branding efforts to create a compelling set of brands, seeking to reach young families and operate within the sphere of future growth. As the following illustrates, the company has generated good impressions relative to its peers.

Social media impressions (PLCE)

{kind=link}

PLCE operates both physical stores and a robust online platform. Its omnichannel approach allows customers to shop in-store, online, or through mobile devices, providing convenience and catering to diverse shopping preferences. The company is currently aggressively rebalancing toward e-commerce, closing stores, and developing relationships in the online-only segment, such as with Amazon ( AMZN ). This is one of the primary reasons for the revenue slowdown.

Although we like this strategy conceptually, Management has insufficiently developed the brand on the online stage in our view, which is why revenue has not accelerated and margins have actually declined. Impressions are great but they must be contextualized with conversion (impressions to sales) and the cost-effective effort (can easily drive impressions through quantity, which is less meaningful than quality), which is where PLCE is lacking. The company is not convincing consumers to purchase at a noticeably higher level than what its stores were already doing.

In conjunction with store closures, we consider the following factors as key to the decline in PLCE's competitive position, and thus growth:

- Changing Consumer Preferences - Fashion trends can change rapidly, influenced heavily by social media and fashion houses. PLCE needs to consistently innovate and adapt to evolving styles to retain customer interest, which is incredibly difficult as many consumers will choose to try new brands when these changes occur.

- Intense Competition - The retail market for children's apparel is highly competitive, with the above firms all vying for market share. The presence of both large-scale retailers and small boutique stores creates a challenging environment, without a significant degree of differentiation ability due to harmonizing designs among companies.

- Aging population - A decline in birth rates is contributing to reduced demand for children's clothes, with this trend seemingly expected to continue.

- Online Retail Challenges - E-commerce has significantly disrupted the traditional market, as businesses have utilized low-cost supply chains to flood the market with fashion-forward designs at lower prices.

- Shift to Fast Fashion - The rise of fast fashion retailers offering trendy children's clothing at lower prices has created a challenge.

We have not seen a sufficient reaction from PLCE to offset this pressure, likely because it is significantly out of its control. The company is not powerful enough to materially change its trajectory, which is driven by the industry.

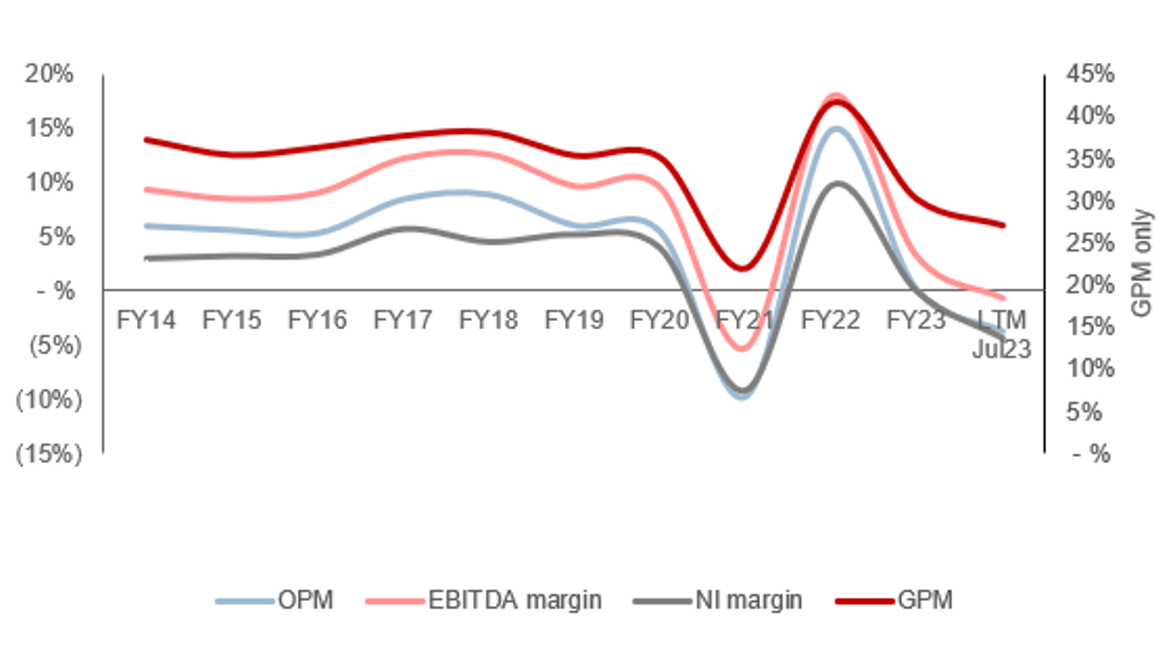

Margins

{kind=link}

PLCE's margins showed a reasonable degree of consistency prior to the pandemic, owing to Management's hesitancy to drive growth through discounting, and also a short period of improved demand. This has deteriorated considerably, with EBITDA-M turning negative, as Management has sought to stabilize sales.

PLCE will inevitably bounce back from these lows, although based on our commercial analysis, we are hesitant to suggest the company will return to its pre-pandemic levels. E-commerce and low-cost providers in particular are not going away and will further contribute to market share loss. We see the company normalizing at an EBITDA-M in the MSD/HSD region.

Quarterly results

PLCE's recent performance has been dire, continuing from the struggles experienced during FY22. Revenue has declined 6 successive quarters in a row, with the last four being (8.8)%, (10.2)%, (11.2)%, and (9.3)%. In conjunction with this, EBITDA-M has been negative for the last 3 quarters.

This is a reflection of the wider macroeconomic impact on the apparel industry. With heightened inflation and interest rates, consumers' discretionary spending is softening, as living costs soar. This has been slightly muddied by inflationary price increases creating the perception of resilience. PLCE is better positioned as consumers are not going to forego clothing for their children, who more quickly will require larger sizes. However, this is offset by the ability to trade down to more affordable options.

We believe conditions appear to be worsening, with investors turning bearish again. The compounding impact of an extended period of heightened rates/inflation is beginning to cripple any market resilience.

Given the numerous periods of negative growth already, we suspect PLCE is rapidly approaching its "bottom", although revenue stagnation subsequently is likely. The business has limited scope to offset this impact or protect its business model. The concern is that many of its peers will continue to aggressively seek market share growth and thus maintain marketing efforts while the likes of PLCE reduce spending to protect margins.

Key takeaways from PLCE's most recent quarter are:

- top-line beat was due to strong digital performance as a result of the Back-to-School season. Management has seen good returns on its First-to-Market Back-to-School digital marketing strategies.

- PLCE's e-commerce channel now represents 51% of its retail sales in Q2'23 versus 47% in Q2-22 and 30% in 2019. This has been driven by an aggressive reduction in footprint and an effort to transition those sales online, with the Company ending Q2'23 with 596 stores and square footage of 2.9m, a decrease of 9% compared to the prior year.

- Inventory has declined 12.9% versus the prior year, as Management has accelerated the liquidation of seasonal inventory (at an ever-declining margin) and a reduction in average unit costs as inflationary pressures soften.

Balance sheet & Cash Flows

PLCE is conservatively financed, reducing any downside risk associated with its near-term performance currently. Interest coverage is at 6x, which is likely close to the lowest the company will reach.

Inventory turnover remains below despite the liquidation efforts, falling to a decade low. This is a compounding issue that Management is poorly navigating, although we suspect this should unwind following the back-to-school and holiday season combination.

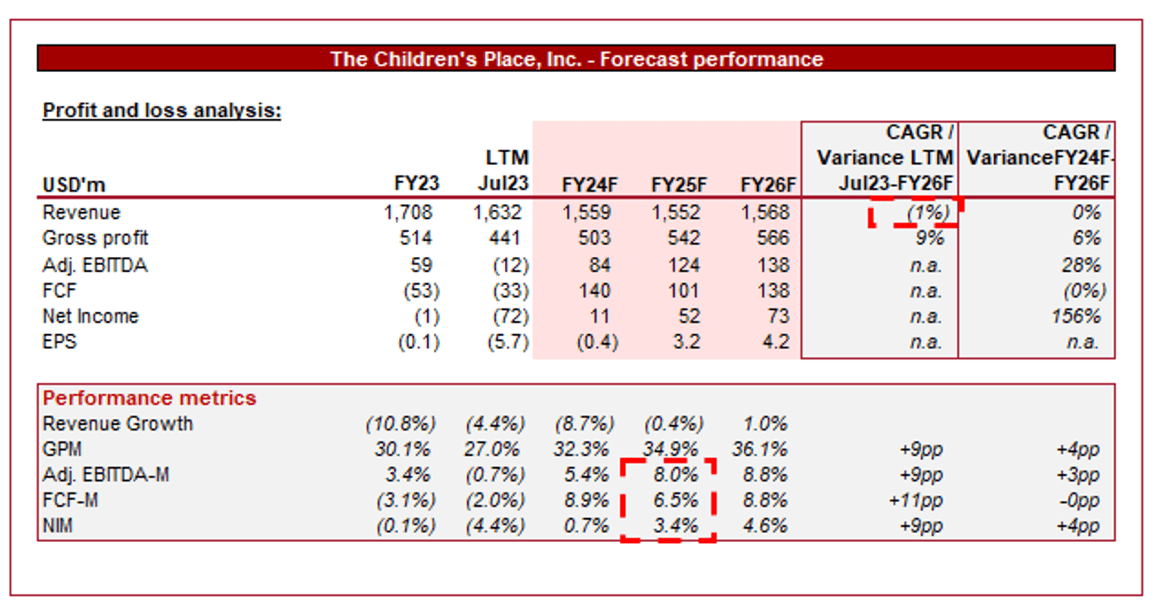

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its poor growth, alongside an improvement in margins to below its pre-pandemic levels.

We consider these assumptions to be reasonable. The company will likely continue to close stores as it focuses on the e-commerce channel, although has not shown an ability to accelerate e-commerce sufficiently to achieve growth.

Industry analysis

Apparel Industry (Seeking Alpha)

Presented above is a comparison of PLCE's growth and profitability to the average of its industry, as defined by Seeking Alpha (28 companies).

PLCE is performing poorly relative to its peers. The company's growth has significantly lagged behind the wider apparel industry, reflecting its declining market share and underwhelming strategic direction.

Further, the company's profitability is disappointing, even when considering its pre-pandemic level. This also illustrates the level of underperformance compared to its leading peers.

We do not believe PLCE is remotely attractive relative to its peers. This industry is incredibly competitive and influenced by changing consumer trends. For this reason, investors must be selective.

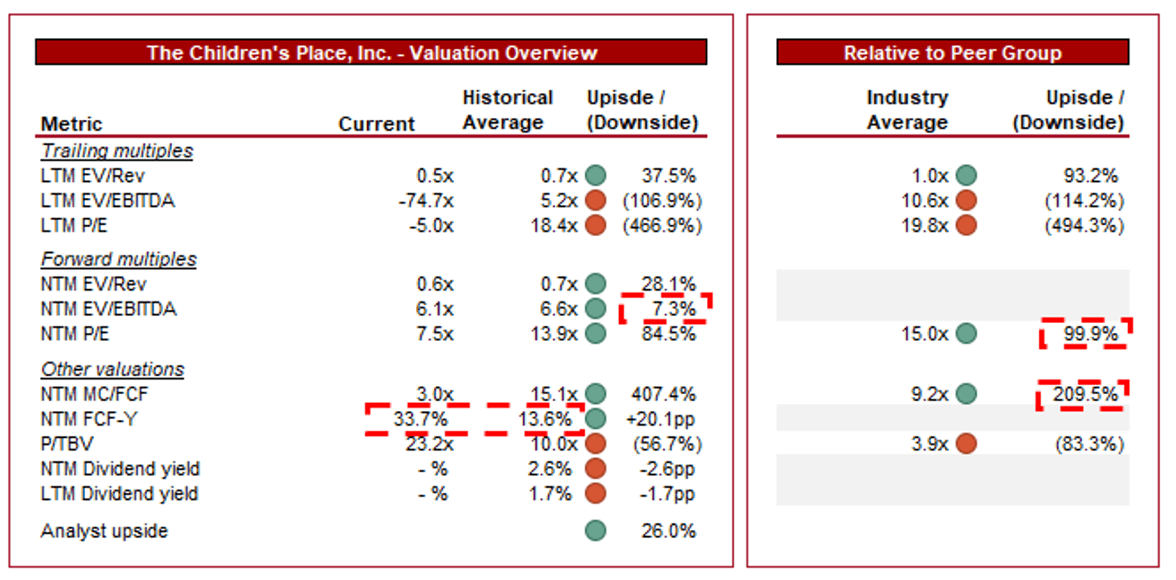

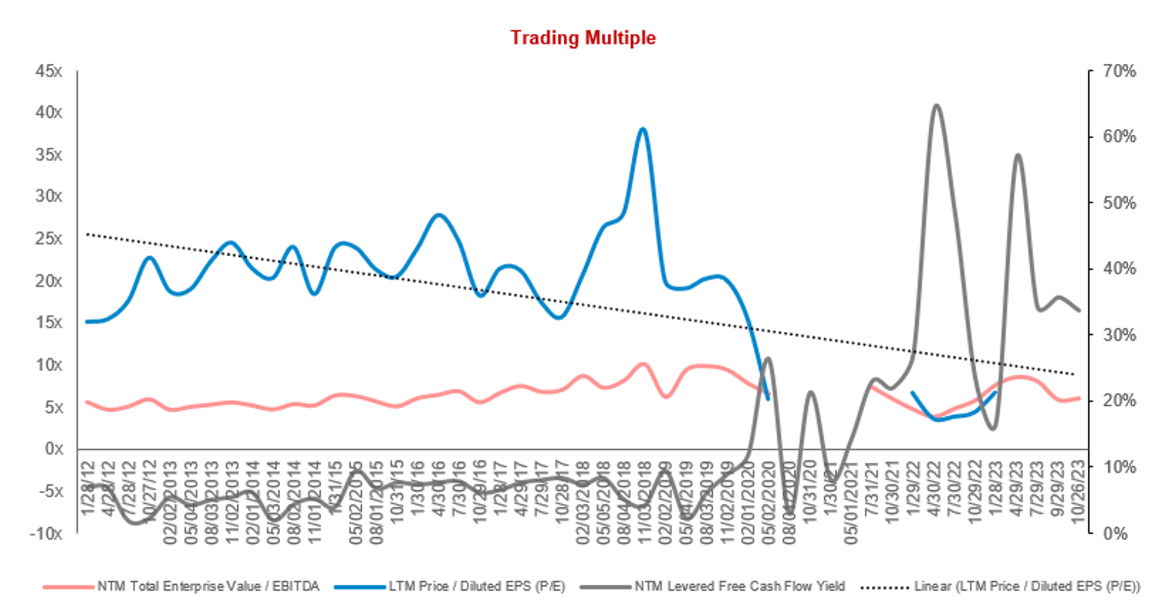

Valuation

{kind=link}

PLCE is currently trading at 6x NTM EBITDA and 8x NTM P/E. This is a discount to its historical average.

A discount to its historical average is warranted in our view, owing to the company's declining competitive position, margins, and growth trajectory. At a ~7% discount to its NTM EBITDA average, the business appears noticeably overvalued in our view. The company has significantly declined in attractiveness, and this is not wholly priced in.

Further, PLCE is currently trading at a ~100% discount to its peers on a NTM P/E basis and ~210% on a NTM FCF basis. This appears more reasonable relative to the weaknesses the company has exhibited.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Strong e-commerce growth.

- Effective marketing strategies to renew its brand.

Final thoughts

PLCE is not an attractive company currently. The business has struggled to achieve consistent growth for an extended period of time, forcing a transition to the e-commerce channel without sufficiently developing its business model.

PLCE performance relative to its peers and historical average is disappointing, with operational performance compounding its declining competitive position. We see very little going right with this company.

We suggest investors steer well clear of this company, with limited scope for future upside.

For further details see:

The Children's Place: Only Pain Ahead Following Consistent Declines