PLCE - The Children's Place: The Right Place For A Retail Turnaround

2023-07-10 10:45:00 ET

Summary

- The Children's Place is undervalued, and we expect improved quarterly results beginning in Q3-F23, with significant catalysts set to jumpstart earnings growth and re-rate the shares higher.

- Despite a challenging F2022 with bloated inventories and higher costs, an increased credit facility, streamlined operations, and insider buying suggest PLCE is on the cusp of a turnaround.

- Lower freight and cotton costs will generate earnings growth in 2H:F23, while right-sizing inventory will unlock working capital for free cash flow.

- At 8x our F2024 adjusted EPS estimate, PLCE would trade at $48, representing 80% upside.

Investment Thesis

The Children's Place (PLCE) is undervalued and will continue to re-rate higher, as quarterly results materially improve beginning in Q3-F23. Shares sold off over the past year, as F2022 and early F2023 (Q1-F23 and expected Q2-F23) results were greatly affected by bloated inventories and higher costs, which in turn hurt working capital and free cash flow generation. Given significant catalysts that are set to be realized beginning in 2H:F23, we think earnings growth and multiple expansion will push PLCE shares higher. We value PLCE at 8x our F2024 adjusted EPS estimate of $6.00, resulting in 80% upside.

Stock Chart

Since bottoming out at $14.27 intraday on June 1st amidst a brutal sell-off spurred by weak Q1-F23 results (i.e., missed consensus and lowered full-year guidance) and retail sector sentiment, PLCE shares are up 85%. We contend there is significantly more upside potential, including another 38% merely to be flat for the year.

Business Overview

The Children's Place - Company Overview (Investor Presentation)

{kind=link}

The Children's Place is the largest pure-play children's specialty apparel retailer in North America. PLCE designs, contracts to manufacturers, sells at retail and wholesale, and licenses to sell fashionable, high-quality merchandise predominantly at value prices under these proprietary brand names: The Children's Place, Place, Baby Place, Gymboree, Sugar & Jade, and PJ Place.

With digital sales planned for 50% of PLCE's total revenue and traditional malls representing less than 30%, this retail company is far from a "mall-based retailer."

Transitory Challenges - F2022 & 1H:F23

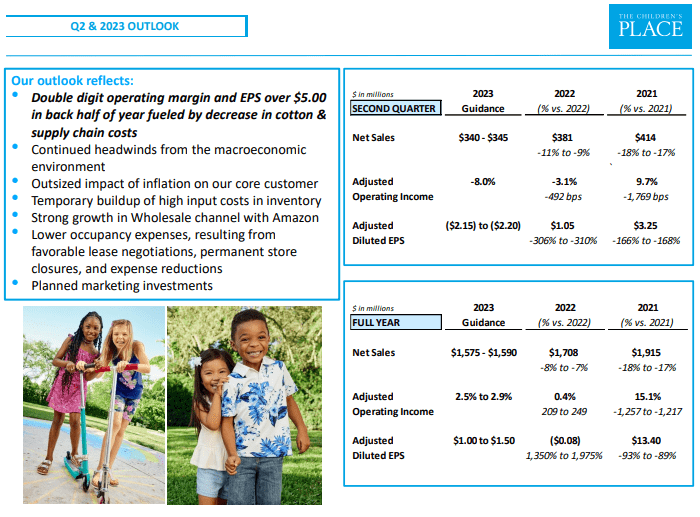

F2022 was a very challenging year for The Children's Place, given tough year-over-year comparisons to periods when pandemic-related federal stimulus fueled consumer spending. Further, compressing bottom line performance were supply chain issues, including increased freight expenses and higher cotton costs (the main input for the cost of goods sold). In addition, the macroeconomy was tumultuous, and the retail environment was promotional. Given this backdrop, PLCE reported weak F2022 results : net sales were down 11% to $1.71 billion, adjusted gross margin declined 1,150 basis points to 30.1%, and an adjusted net loss of $1.1 million (compared to adjusted net income of $199.2 million in F2021).

Q1-F23 results were more of the same from F2022, yet investors were further surprised by the reduced full-year F2023 outlook. In Q1-F23, net sales were down 11%, gross margin eroded by 920 basis points, and adjusted net loss was $28.8 million (compared to adjusted net income of $19.8 million in Q1-F22). Management is more cautious, based on the effect that the macroeconomy, particularly inflation, has on the customer base.

The Children's Place - F2023 Financial Outlook (Investor Presentation)

{kind=link}

Nonetheless, we think PLCE is incredibly attractive based on current F2023 guidance, since it indicates a massive turnaround beginning in 2H:F23. In our view, too many investors (especially when the stock traded below $18) focused on 1H:F23 (the trough) and discounted 2H:F23 (the likely inflection point). F2023 guidance includes adjusted earnings of $1.00 to $1.50, down $2.50 to $3.00. In our view, the vast majority of this variance is due to the worse 1H:F23 than management expected at the beginning of the year. We expect adjusted earnings to be $5.45 in 2H:F23.

Recent Developments - Incrementally Bullish

In recent weeks, there have significant developments that bolster our investment thesis: (1) increased credit facility; (2) streamlined operations; and (3) insider buying

Expanded Credit Facility

On June 5th, PLCE announced a $95 million increase to its revolving credit facility to $445 million (from $350 million). In our view, this timely development further positions PLCE well for 2H:F23, as it helps to improve the retailer's working capital.

Streamlined Operations

On June 28th, PLCE announced a 17% reduction of its salaried workforce , including 181 positions. We estimate this headcount reduction could result in at least $1 in incremental adjusted EPS beginning in F2024. The retailer also reiterated plans to terminate its corporate office space lease early, in order to downsize its footprint and save costs on both the amount of space and lease terms.

Insider Buying

On July 6th, Jane Elfers, president and CEO, disclosed that she i nvested more than $1 million in PLCE stock , buying 43,000 shares at an average price of $23.70. This activity increased the beneficial ownership of Elfers in PLCE by more than 10% to 370,033 shares. In our opinion, Elfers demonstrated confidence in the company's strategy and ability to deliver stronger results over the next 12 to 18 months.

Financial Expectations

We expect PLCE to generate adjusted EPS of $1.25 in F2023 and $6.00 in F2024. Underpinning these expectations are the right-sizing of its inventory levels, lower freight shipping costs (no need for super expensive airfreight and conventional container rates have returned to "normal" / pre-pandemic levels), a sharp reduction in cotton prices (the main input for its merchandise), and realization of the benefits from its announced expense reduction initiatives. We view our F2024 estimate as somewhat cautious, given uncertainty in the macroeconomic environment, particularly for PLCE's middle-class core customer.

We anticipate an approximate $75 million working capital "gain" in F2023. On the Q1-F23 conference call , management stated PLCE anticipates "inventory investments to be down throughout fiscal 2023, providing a significant opportunity to expand free cash flow." Based on anticipated net income, working capital gain, non-cash stock-based compensation add back, depreciation add back, and relatively modest capital expenditures, we expect free cash flow of more than $125 million this year (approximately $10.00 per share), the bulk of which will be used to pay down debt.

We think our F2024 adjusted EPS estimate is reasonable, even with modest same-store sales growth, given the vast majority of earnings growth will be generated by gross margin expansion and lower SG&A costs. For example, on the Q1-F23 conference call, management reiterated that approximately 100 stores would be closed by year-end F2023, further reducing expenses for this "digital first" retailer.

Valuation

We value PLCE at 8x our F2024 EPS estimate of $6.00, resulting in a $48 stock price. Our admittedly conservative multiple is based on the mean of the historical 5-year average forward P/E multiples of PLCE, 13x, and Carter's (CRI), 15x, which is 14x and then discounting it by 40% based on macroeconomic and execution risks. Over the longer term, provided a successful turnaround operationally and balance sheet clean-up (i.e., debt reduction or elimination), we think PLCE can re-rate higher to closer to this historical forward P/E multiple and therefore trade at $80.

Risks

In our view, the key risks for The Children's Place are: (1) macroeconomy; (2) execution; and (3) competition

We think a recession, persistently high inflation, and/or a rise in middle-class unemployment would hurt consumer discretionary spending. If this occurs, then PLCE may be unable to leverage its fixed costs. However, this risk is mitigated by the expense reductions previously discussed.

As with any corporate turnaround, especially within the retail sector, there is execution risk in achieving goals. However, we think this risk is mitigated by the recent insider buying (i.e., signaling confidence).

We also think there is a competitive risk. For example, in 2022, the competitive landscape was promotional with big box stores, such as Walmart ( WMT ) and Target ( TGT ), heavily discounting children's apparel which necessitated higher-than-planned markdowns at PLCE that eroded its margins.

Conclusion

The Children's Place is a compelling turnaround story, one that requires forward-thinking to see past the challenging past six quarters and appreciate the built-in catalysts that will kick-start the turnaround (i.e., earnings growth) and re-rate the stock higher: lower freight and cotton costs, expense reductions, and debt reduction. At 8x our F2024 adjusted EPS estimate of $6.00, PLCE would trade at $48. Therefore, we suggest that there is at least 80% upside over the next 12 months.

For further details see:

The Children's Place: The Right Place For A Retail Turnaround