TCS - The Container Store: A Bleak Near-Term Outlook

2023-06-07 04:00:16 ET

Summary

- Traffic volumes experienced a decline in March and April, impacting outlook views.

- There has been a reduction in average tickets, according to CEO Satish Malhotra.

- Container Store has moved too far from its core business of containers into completely unrelated products.

- The critical metric of accounts payable as a percentage of inventory continues to worsen indicating vendors are requiring stricter terms.

Specialty retailer The Container Store Group ( TCS ) continues to struggle and their guidance numbers for this fiscal year are just plain awful. While it is not currently seriously distressed financially, if it does not dramatically improve it could join the long list of "former retailers". I put TCS on my watch list after the recent stock plunge, but until I see some hope that management gets their act together managing their product lines, it will remain only on the watch list and not on my current holdings list. I rate TCS a neutral/hold.

Leonard Green & Partners, who still currently own 30.5% of TCS, sold 5 million shares in early February 2021 for $15.15, which was near the top of the recent trading cycle.

Management's New Guidance Numbers Shocker

Many investors expected that TCS would benefit from the liquidation of bankrupt Bed Bath & Beyond ( BBBYQ ), but it seems if there is any benefit, it is very modest because the guidance numbers for 1Q are terrible. Same store sales are expected to decline 19% to 23%. EPS 1Q is expected to be a loss of $0.13 to a loss of $0.19 per share. Full fiscal year guidance numbers are for total revenue of $885million to $900 million, which on a comparable store basis is a decline of "mid to high teens". GAAP annual EPS is expected to be $0.07 to $0.17 and adjusted EPS of $0.21 to $0.31.

I wish that management would include what GDP and interest rates numbers they are using to estimate the guidance numbers. I am expecting that GDP will decline at least 2% in real terms in 1Q 2024. I have serious doubts, therefore, that TCS will see improving results in the second half of their fiscal year.

What makes these total revenue guidance numbers so troubling is that management stated they are adding products - an additional 1,000 SKUs. Plus, since inflation continues to remain elevated, I would expect some price increases. If total revenue is expected to decline that implies a very significant decline in their current products before they added additional ones. This, in my opinion, is a major yellow flag and why I am not buying TSC stock. Often, we look at the same store or comparable store numbers, I wish we were able to get changes in sales of the same product items - same SKU sales changes. We get group numbers, but not individual product numbers.

It looks like both traffic volume is declining and so is average ticket prices. According to CFO Jeff Miller: "We were experiencing lower traffic volumes...We saw a notable decline in that during the month of March and we continue to see that in the month of April, which is what's driving our outlook view." CEO Satish Malhotra stated during the same call: "We have seen a reduction in average ticket". Do these declines indicate a recession?

TCS stock soared with the rest of the market on June 2 after the jobs market was stronger than expected. A potential recession has negatively impacted TCS stock price, but I think the Fed will now raise rate this year and it is, in my opinion, more likely - not less likely - we will see negative growth in certain sectors of the economy such as discretionary retails sales in late 2023 and 2024 because of increased interest rates.

Latest Results

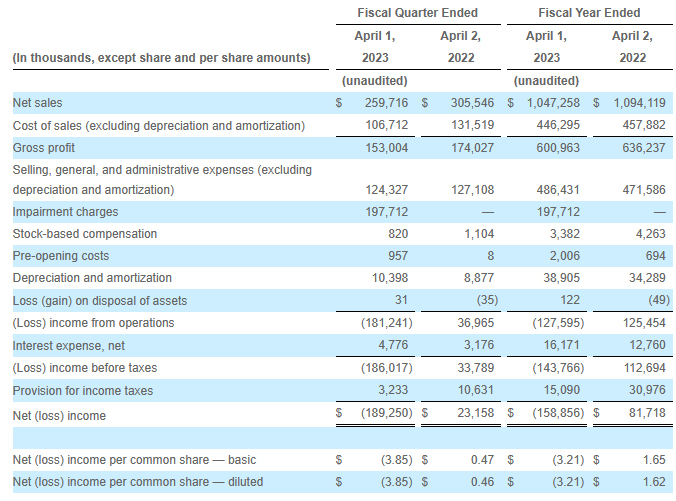

The results for last year look worse at first glance than they actually were because the GAAP loss per share of $3.21 includes an impairment charge to write down goodwill by $197.7 million. Without that charge they had an adjusted EPS of $0.75 for the year. The metric that caused a lot of concern was that comparable store sales were down 13.1% for 4Q.

Quarterly and Annual Income Statement

{kind=link}

Annual EBITDA

I Am Worried About Management

I am not comfortable that the current management can properly execute their business plan. For example, I went to their website and was actually very interested in an item for my garage that was on the first page. When I clicked on that item nothing happened. What? It is not just some temporary technical issue. It is how the first page of their website is formatted. This violates what I learned almost 50 years ago in B-school - make it as easy as possible for a customer to move from showing interest in an item to actually buying it. I had to make multiple clicks to get to the page that sold it. Even then I still could not click on it and buy it as shown. I had to select the various parts such as the stand, top, and various drawer sizes. I was turned off and did not buy it. This building feature might be desirable for many of their customers, but I wanted a simple purchase.

Item I Considered Purchasing

The Container Store

When I clicked on various types of products, I was shocked to see a reference to "Women's Small Closet With Drawers". I was surprised to see the reference to "women" being used since the trend in retail has been away from using any reference to the sex of a potential buyer. Even some retailers no longer use "boy's" toys or "girl's" toys, for example. I looked into the features of this closet, and it seems that anyone might be a potential buyer. I just do not understand why they are not more sensitive to how products are now expected to be marketed. Years ago, this approach was accepted and actually was even expected, but I think this could indicate that management may not fully understand how quickly the consumer market is changing. Remember their guidance numbers and recent sales are declining. Is this partially because they do not understand the current consumer market? Often small things are indicators of more widespread problems.

The Container Store

There were other issues I had with their website, but I think readers get what I am asserting that there seems to be a number of yellow flags with the execution of their business model by current management.

Moving Too Far From Their Core Specialty - Containers

The Container Store keeps adding products that are not really related to their core business. Management announced that they are adding "single serve coffee maker, sleek desk lamps, vintage fans and essential oil diffusers". I think this is a serious mistake. Adding too many products that are too far from their core container business is very risky. It is hard to control inventories for them. If they are out of stock or there are long delays in delivering orders to customers because of inventory issues, TCS will alienate their customers. If they only offer a few types/models of each new product some customers might think that they have a poor/limited selection, which is the customer mindset that they absolutely must avoid. In their container sector they do offer a huge selection. This wide selection of containers and directly related items is a key asset for TCS. They should not, in my opinion, risk it by offering so many unrelated products. A major reason why Tupperware Brands ( TUP ) is in such serious trouble is because they drifted way too far from their core Tupperware storage items. I hope their new chief merchandising officer understands that they need to get back to their core products.

The direction of opening smaller stores in more major markets might be a key to their turnaround. They are opening 3 this year. While the small stores will be able to only carry a limited number of products, it will get their brand in front of more consumers who can then order their specific desired items via their website. These smaller stores could also serve as a place to pick up and return items ordered from their website. These smaller stores need much less capital to open and to maintain their in-store inventory. (It will be interesting in the future to compare the sales per square foot for the smaller stores to the larger ones.)

Liquidity - Not a Problem (Yet)

While TCS is currently not in a serious financial problem, their financial position is headed in the wrong direction. They only have $6.958 million cash, which was a decrease of $7.294 million from the prior year. They do have $91.8 million available under their revolver and another $8.2 million available under Elfa's revolver.

One serious problem is their vendors seem to be requiring stricter terms. The trend of the critical metric of accounts payable/inventories is a major negative. It was at 38.8% at the end of the latest fiscal year compared to 43.7% the prior year. For the fiscal year ending March 31, 2019 it was 61.8%. It seems that some vendors are becoming less willing to ship under the normal invoice method.

CEO Malhotra Satish bought 33,500 shares for $2.2382 on May 19, which was after the poor guidance announcement, which might reassure vendors that TCS is financially stable and to give them confidence to deal with the retailer.

Debt of $167.9 million is a reasonable 1.45 x adjusted last year's EBITDA of $115.4 million. The problem, however, is that the going forward EBITDA could be much lower given the latest other guidance numbers. The interest rate of SOFR+1.25% for the revolving credit agreement is actually much lower than what I would expect.

Conclusion

Besides looking at financial figures for a consumer company I like to use their product or services. With retailers I like to actually shop in their stores and on their websites to get a better feel about their operating model. The Container Store no longer is a specialty retailer selling containers and directly related items, it has become a general retailer selling almost everything but the kitchen sink. This move from being a well-regarded specialty retailer is a serious business model mistake, in my opinion. It needs to refocus more on containers.

Using the latest price of $2.80 and prior year's adjusted EPS, TCS seems very cheap with a 3.7 P/E, but using the low-end of the adjusted EPS guidance number of $0.21 per share, the 13.3 P/E is not cheap. Since I am expecting a recession and have serious doubts they can even earn $0.21 per share, TCS is currently not cheap.

The latest guidance numbers were very troubling for investors. Seeing other specialty retailers, such as BBBY, file for bankruptcy has made investors very cautious about the retail industry. The Container Store Group may face a very difficult next 15 months if there is a recession that I expect. I need to see some changes by management in their business model before I move TCS off my watch list to my buy list. I rate TCS "neutral/hold".

For further details see:

The Container Store: A Bleak Near-Term Outlook