TCS - The Container Store: I'm Expecting More Than Wall Street

2023-12-28 16:34:52 ET

Summary

- Container Store Group sells organizing solutions ranging from storage bins to hangers.

- The company's sales have decreased after a pandemic boost, also pressuring margins due to a large amount of fixed costs.

- Wall Street analysts have low expectations for the company's financial recovery, below my baseline estimates.

- The current valuation seems to provide a good upside in the case that a financial recovery happens.

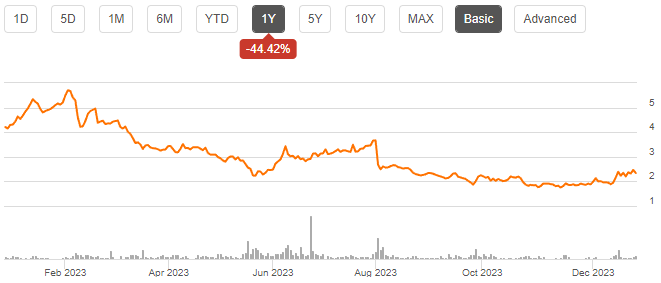

The Container Store Group ( TCS ) is a retailer of organizing solutions. The company’s offering includes products such as storage bins, hangers, shoe boxes, drawers, trays, and shelves among a number of other products. Container Store Group sells the products through its retail stores, website, call center, and through wholesale to other retailers. After the pandemic boosted the company’s demand for a couple of years, Container Store Group hasn’t been able to contain its boosted earnings level, with the bottom line deteriorating with lower sales. As the earnings have fallen, so has the stock – Container Store Group’s stock price has nearly halved in the past year, without the company currently paying out any dividends.

{kind=link}

Sales Are Pressured by Previous Boost

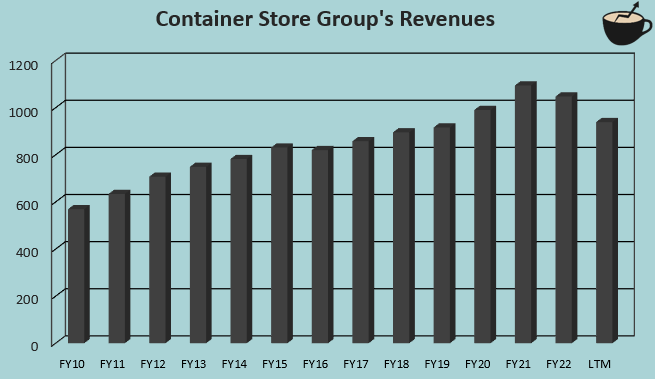

Prior to the pandemic, Container Store Group achieved a revenue CAGR of 5.4% from FY2010 to FY2019. The growth was boosted further by the pandemic, as revenues grew by 8.1% in FY2020 and by 10.5% in FY2021 as consumers stayed home boosting demand. The boosted sales have since reversed with the pandemic subsiding and the consumer sentiment worsening, resulting in accelerating revenue decreases in the past few quarters.

{kind=link}

I don’t believe that the decreasing revenues are likely to be a sign of structurally damaged demand for the company – the market for organizing solutions was boosted by the pandemic, but the higher sales during the pandemic are likely to have caused a lower demand for a couple of years afterwards due to the products’ long lifespan. Container Store Group achieved a revenue growth of 2.3% in FY2019, and with extrapolation of the similar growth, the company should have generated a total of around $3365 million in sales from FY2020 to H1/FY2023, but has generated $3558 million in the same period mainly due to the pandemic boost. The current hangover from overly positive demand is projected to continue – further decreases would bring the actual generated revenues, and the projected pre-pandemic estimate closer, which seems rational. Currently, trailing revenues are still very slightly above the FY2019 level.

Container Store Group’s management mainly relates the lower sales to mainly a challenging macroeconomic environment in the Q2/FY2023 earnings call instead of a tough industry demand with the previous pandemic boost – the lower sales isn’t only a result of the pandemic, but also a result of the tougher macroeconomic situation.

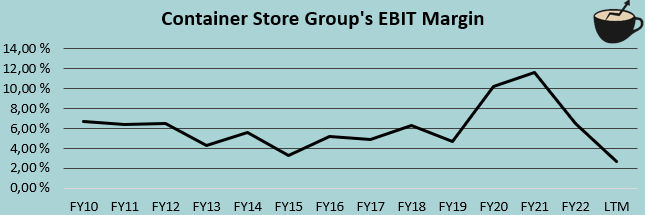

As a retailer, Container Store Group has quite a good amount of fixed costs – as the sales level comes down, so does the company’s operating margin, and vice versa. The company’s EBIT margin was boosted by the pandemic into low double digits, but has historically been quite significantly lower – from FY2010 to FY2019, the average EBIT margin has been 5.4%. With the lower sales, the current trailing EBIT margin stands well below at 2.7%. With an eventual sales recovery that I believe to be highly likely, the margin should scale back into near historical figures in my opinion.

{kind=link}

Container Store Group has had quite low elasticity in the company’s gross margin despite a lower demand – the gross margin has only fluctuated between the current trailing 57.3% and 58.6% from FY2014 to the trailing figures. I believe that it’s a strong sign that the company hasn’t seen it necessary to compensate in the sales prices too significantly.

Wall Street Analysts Expect Less

The company’s Wall Street analysts don’t seem to expect a financial recovery at least in the next couple of years – the two analysts on the stock estimate an EPS of $0.28 for FY2024 and an EPS of $0.21 for FY2025. In FY2018 and FY2019 respectively, Container Store Group achieved a normalized EPS of $0.37 and $0.27; the estimates expect the company’s earnings level to be impaired on a long-term basis, which I see as unlikely. A financial recovery that I expect would positively surprise the analysts on Wall Street, possibly being a catalyst for a stock rally.

Strategic Initiatives

Container Store Group has several strategic initiatives, as told in the Q2/FY2023 investor presentation . The company targets to deepen customer relationships through new assortments including more premium products, and through rewarding loyal customers. In addition, Container Store Group invests in improved digital capabilities, including mobile app upgrades, SEO enhancements, and improved branding on digital platforms. Although I don’t believe the initiatives to have too significant of an impact on financials, I believe that they prove the management’s active pursuit in improving operations.

The company is also trying to expand its reach. The company is actively expanding its store footprint, as the store base grew from 95 to 98 year-over-year in Q2, and believes to open a total of 5 new stores in FY2023 – I believe that this signals the management to have a good belief in a recovering profitability.

Valuation Provides Upside in Case of Financial Recovery

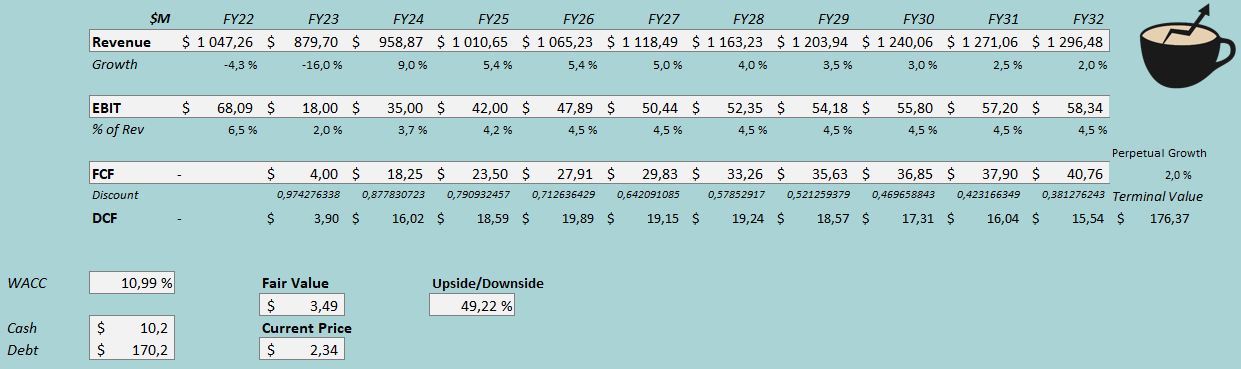

To estimate a fair value for the stock and to contextualize the valuation, I constructed a discounted cash flow model as usual. In the DCF model, I estimate a financial recovery after a weak performance in FY2023. For the current fiscal year, I estimate revenues to decrease by -16%, in line with analysts’ expectations. After the year, I believe that the demand should start to recover, with a revenue growth estimate of 9% for FY2024. Afterwards, I estimate the growth to slow down into 5.4% for a couple of years, representing the pre-pandemic historical rate. The growth slows down in steps into a perpetual growth of 2%, representing a total CAGR of 4.4% from FY2023. On the margin side, I estimate a partial recovery. After a weak EBIT margin of 2.0% for FY2023, I estimate a recovery in the upcoming years into a margin of 4.5%, still slightly below the pre-pandemic average. The company has a decent cash flow conversion, although capital expenditures are currently quite high.

The mentioned estimates with a cost of capital of 10.99% craft the following DCF model. The model estimates Container Store Group’s fair value at $3.49, around 49% above the stock price at the time of writing. The stock isn’t priced for a financial recovery that I see as likely, but rather a scenario that’s estimated by Wall Street analysts; I believe that the risk-to-reward on the stock is great at the current level.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2/FY2023, Container Store Group had $5.3 million in interest expenses. With the company’s current amount of long-term debt , Container Store Group’s annualized interest rate comes up to 12.31% - I believe that the interest also covers a small part of the company’s leases, making the interest rate high when only accounting for long-term debt as interest-bearing debts, but I believe that the figure is useful as the lease payments are taken from cash flows regardless, and affect the company’s income. Due to a low equity valuation and quite a high amount of debt, I estimate the debt-to-equity ratio to stay high, with a long-term estimate of 60%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.82% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Container Store Group’s beta at a figure of 1.34 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 12.04% and a WACC of 10.99%.

Takeaway

After heightened sales during the pandemic, Container Store Group’s demand is facing a hangover. The lower stock price seems to represent a good buying opportunity in my opinion – Wall Street analysts, and the current valuation, don’t believe in a full financial recovery into a pre-pandemic trajectory. If only a partly recovery is achieved, the stock could be fairly valued, but until a longer period of weak earnings, I see such expectations as quite bearish. For the time being, I have a buy rating on the stock.

For further details see:

The Container Store: I'm Expecting More Than Wall Street