ALC - The Cooper Companies: Attractive If Management Can Pull Through

Summary

- The management team at The Cooper Companies released promising financial guidance for the firm's 2023 fiscal year.

- If the firm can hit guidance, then it may very well make for a decent prospect.

- But given the uncertainty and forward-looking nature of this guidance, investors might want to take a wait-and-see approach before investing.

One of the most unique companies I have come across in recent years is The Cooper Companies ( COO ). At its core, the company focuses on two main lines of operation. The first involves the production of vision products, including specialty materials like silicone hydrogel. The second involves a portfolio of products and services that focus on advancing the health of women, babies, and families. Specific medical devices, contraceptives, and other related offerings, are all held under this segment. In recent years, the company has demonstrated some attractive growth on both its top and bottom lines. Cash flows have been a bit lumpy. And on top of that, shares have, up to this point, been rather expensive. The good news is that the picture is changing and, when coupled with a decline in share price over the past year, the firm is starting to look more appetizing. In the event that shares fall further from here and/or if management can achieve their target for 2023, I could ultimately end up upgrading the company. But for now, it still does make for a solid 'hold' in my book.

The picture keeps improving

Almost exactly one year ago, on February 6th of 2022, I published an article discussing whether or not it made sense for investors to seriously consider The Cooper Companies as an investment prospect. In that article, I called the company a solid firm from a fundamental perspective. I concluded that the business would likely continue to expand in the long run. But because of how pricey shares were, I felt as though it made for a better 'hold' than a 'buy'. When I rate a company a 'hold', my assessment is that share price performance should more or less follow what the broader market achieves over the same period of time. Since then, the company has come pretty close to doing that. While the S&P 500 is down 9.7%, shares of The Cooper Companies have seen downside of 11.3%.

{kind=link}

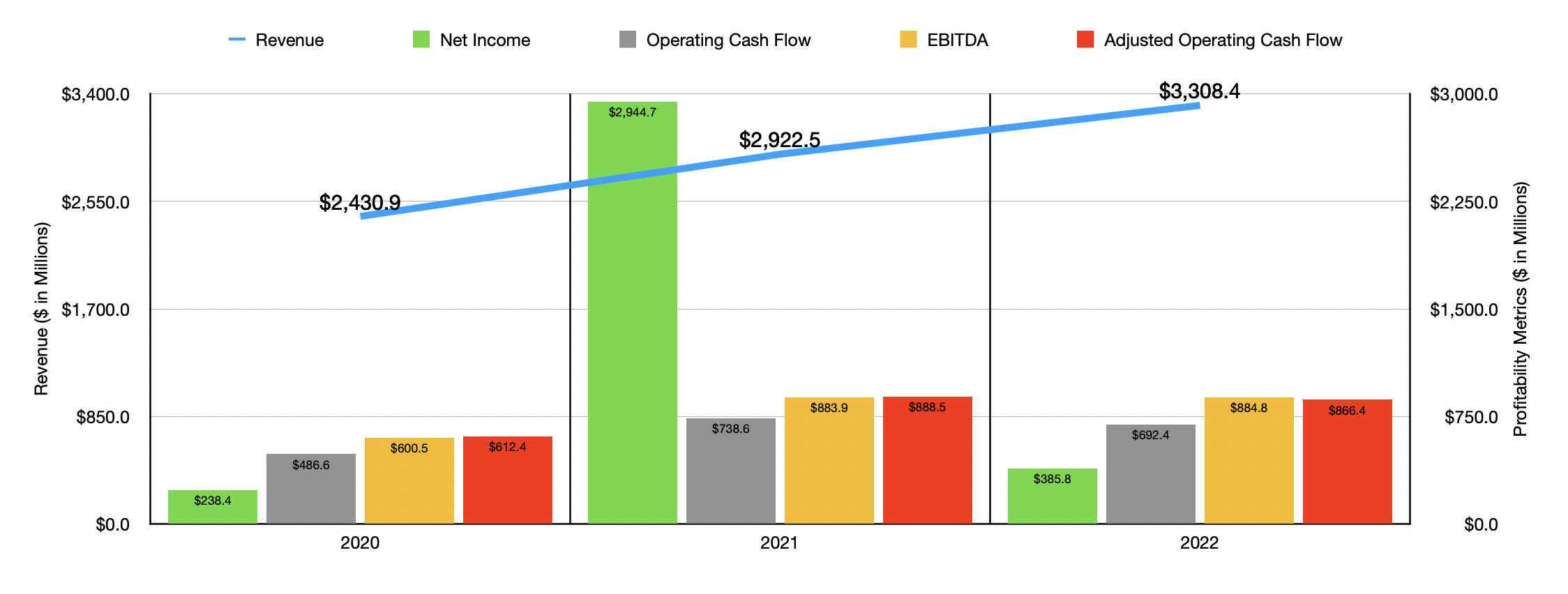

Given this decline in price, you might initially think that the fundamental condition of the company was worsening. But that hasn't exactly been the case. To see what I mean, we need only look at how the company performed for its 2022 fiscal year . After all, when I last wrote about the company, we only had data covering through the 2021 fiscal year. During 2022, sales for the business came in at just under $3.31 billion. That's 13.2% higher than the $2.92 billion generated during 2021. The company's growth occurred across all of its core operations. But the greatest growth came from its CooperSurgical segment, with sales shooting up 38.2% from $770.5 million to just under $1.07 billion. According to management, Office and surgical product sales shot up 40.4% from $451.3 million to $633.6 million, while fertility sales jumped 35.2% from $319.2 million to $431.5 million. Sales growth would have been higher had it not been for $33.4 million of a hit caused by foreign currency fluctuations. According to management, though, the growth was driven by the company's acquisition of Generate Life Sciences for $1.66 billion.

When it comes to profitability, the picture has been a bit more complicated than that. Net income actually plunged year over year, dropping from $2.94 billion in 2021 to $385.8 million in 2022. However, net income is not exactly the best way to look at the company, especially since the 2021 fiscal year saw a massive tax benefit for the firm. Instead, we should look at cash flow data. During 2022, operating cash flow came in at $692.4 million. That's down from the $738.6 million reported one year earlier. But if we adjust for changes in working capital, the metric would have fallen more modestly from $888.5 million to $866.4 million. Meanwhile, EBITDA for the company ticked up modestly from $883.9 million to $884.8 million.

When it comes to the 2023 fiscal year, management has provided some guidance . They currently believe that revenue will come in between $3.455 billion and $3.515 billion. This increase over what the company achieved in 2022 should be driven largely by organic growth of between 6% and 8%. The greatest growth should come from the CooperVision segment, with organic expansion of between 7% and 9%. Most notably, the company is forecasting earnings per share of between $12.30 and $12.60. At the midpoint, that would translate to net profits of $618.8 million. If we assume that other profitability metrics will rise at the same rate year over year, then we should anticipate adjusted operating cash flow of $1.39 billion and EBITDA of roughly $1.42 billion.

{kind=link}

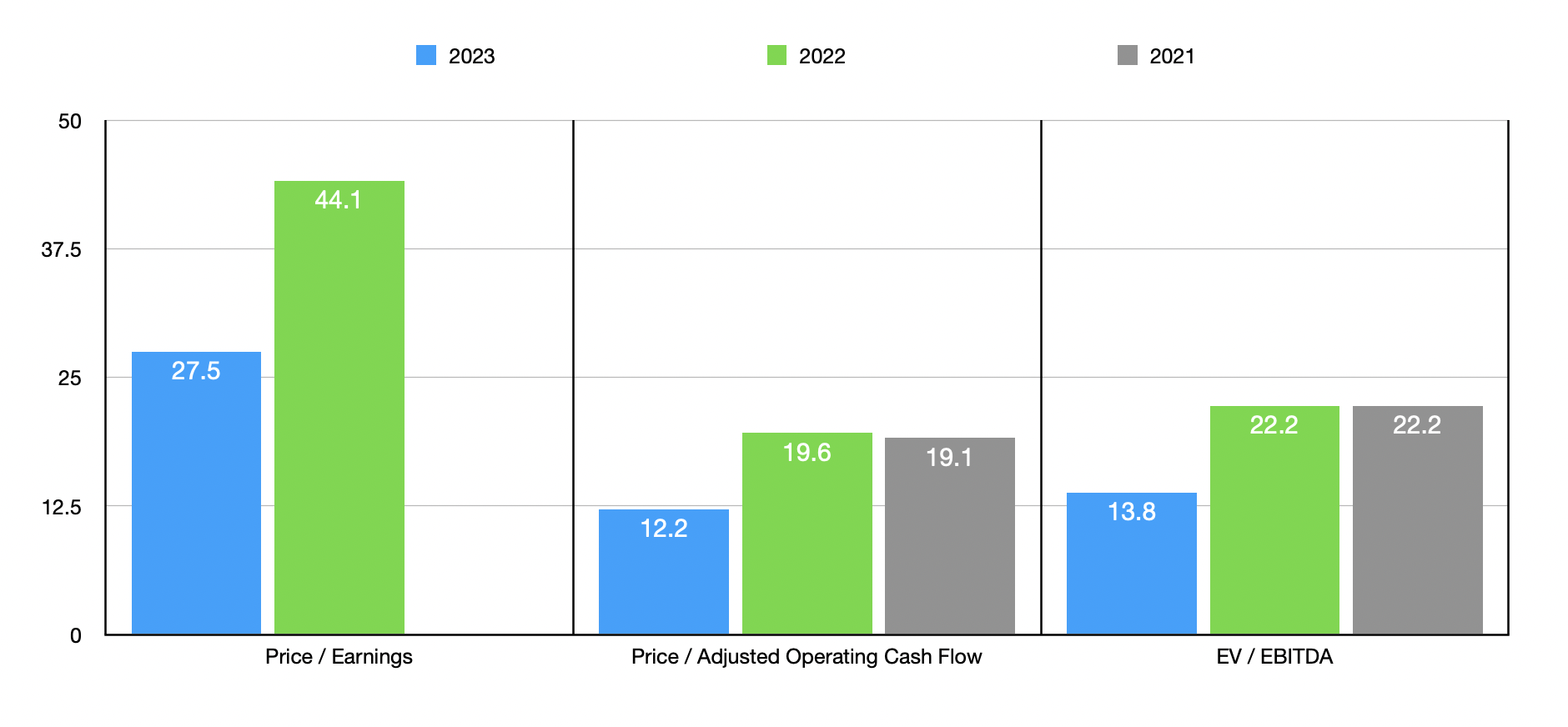

Based on these figures, the company is trading at a forward price-to-earnings multiple of 27.5. The forward price to adjusted operating cash flow multiple should be 12.2, while the EV to EBITDA multiple should come in at around 13.8. Based on these figures alone, I would say that the company would warrant a soft 'buy' rating. But it's also important to note that any number of things could change the final outcome for the company. If we value the firm based on 2022 figures, the firm looks much closer to fair value. These calculations, as well as calculations pricing the company based on 2021 data, can be seen in the chart above.

Relying on the 2022 figures, I decided to compare the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.6 to a high of 411. Using the price to operating cash flow approach, the range was from 4.3 to 202.4. In both of these cases, two of the five companies were cheaper than our prospect. Finally, using the EV to EBITDA approach, the range was from 6.6 to 80.9. In this scenario, three of the five firms were cheaper than our prospect.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| The Cooper Companies |

| 44.1 |

| 19.6 |

| 22.2 |

| DENTSPLY SIRONA ( XRAY ) |

| 19.3 |

| 13.4 |

| 9.5 |

| ICU Medical ( ICUI ) |

| 360.7 |

| 202.4 |

| 32.9 |

| QuidelOrtho Corporation ( QDEL ) |

| 4.6 |

| 4.3 |

| 6.6 |

| Neogen Corporation ( NEOG ) |

| 411.0 |

| 54.5 |

| 80.9 |

| Alcon ( ALC ) |

| 65.0 |

| 29.4 |

| 21.2 |

Takeaway

Based on 2022 data, I would make the case that The Cooper Companies is very much fairly valued, both on an absolute basis and relative to similar firms. Having said that, management's guidance for 2023 is promising and, if the company can achieve what management says it can, then there could be some upside from here. Since there is always uncertainty about the future, I cannot yet in good conscience rate the company any better than a 'hold'. But if we see strong evidence as the year goes by that this target is realistic and/or if shares of the company fall further from here, then I could change my mind and upgrade it.

For further details see:

The Cooper Companies: Attractive If Management Can Pull Through