COO - The Cooper Companies: Nothing To See Here

2023-09-26 08:21:30 ET

Summary

- The Cooper Companies, which focuses on vision products and medical devices, has seen a decline in profits and cash flows recently.

- Despite revenue growth, higher costs and expenses have put pressure on the company's bottom line.

- Shares of The Cooper Companies have dropped since earlier this year and are considered pricey compared to similar firms. A 'hold' rating is appropriate.

One thing that I know to be true is that I have always been interested in companies that have odd business models. Traditional retailers or restaurants and things of that nature have never appealed all that much to me. But a company like The Cooper Companies (COO), which focuses on producing and selling vision products, various medical devices, contraceptives, and more, definitely piques my interest. Management continues to grow revenue at a nice rate. However, profits and cash flows have pulled back recently. Even though the stock has dropped since I last wrote about the company earlier this year, shares do look a bit pricey on an absolute basis and, in some respects, relative to similar firms. The picture is not yet so bad as to make me bearish on the firm. However, I think I am bordering on being generous by rating it a 'hold'.

Tough to watch

At the end of January of this year, I wrote a rather neutral article regarding The Cooper Companies. At the time, I was encouraged by some promising financial guidance that management had made available covering the 2023 fiscal year. I stated that if management could hit that guidance, the company could make for a decent prospect. But because of the uncertainty of the economy at the time, combined with the uncertainty of being able to hit specific targets, and because of how shares were priced, I felt as though a wait-and-see approach made more sense for shareholders. At the end of the day, this led me to rate the company a 'hold' to reflect my view that shares probably would not perform much different than what the broader market would achieve. Unfortunately, fate had other plans in mind. While the S&P 500 is up 6.4% since the publication of that article, shares of our target have actually dipped by 5%.

{kind=link}

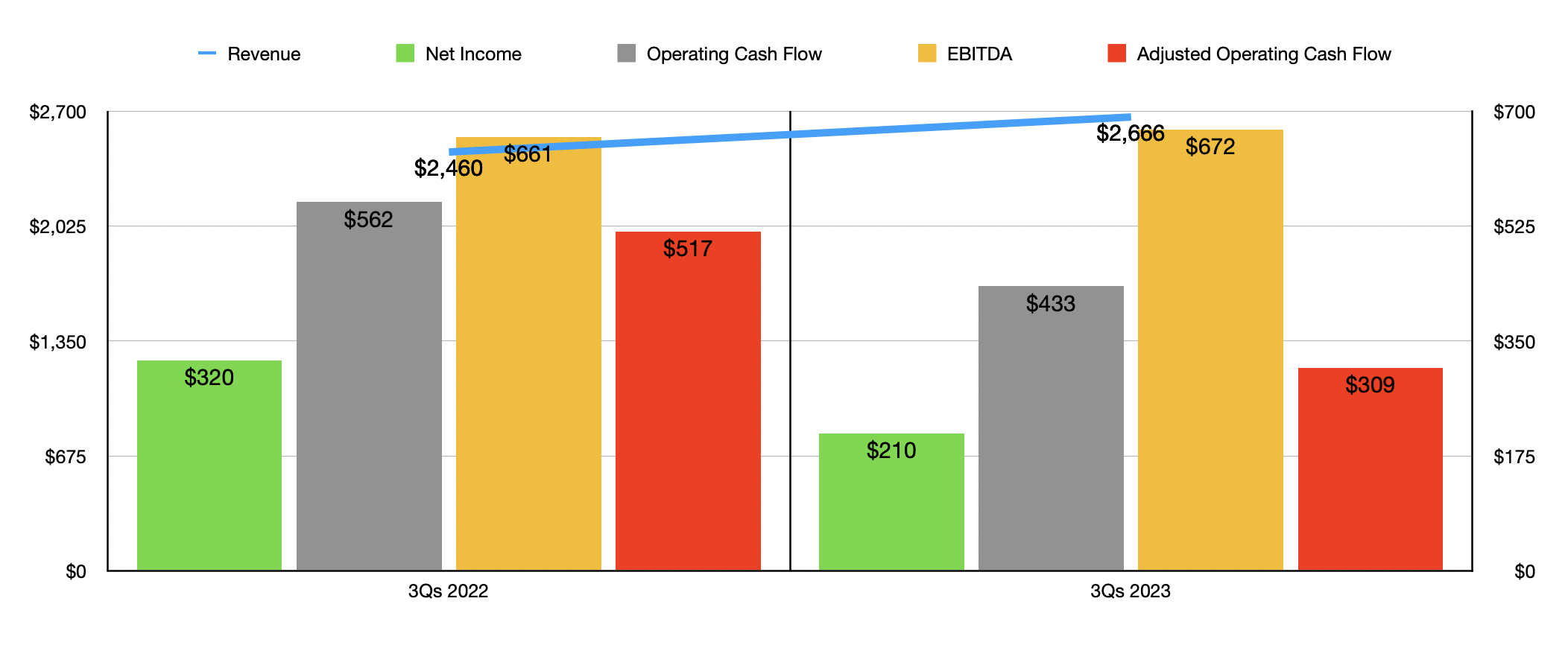

If you look only at the top line data, it might seem odd that shares have pulled back. After all, revenue during the first three quarters of the 2023 fiscal year came in at $2.67 billion. That represents an increase of 8.4% over the $2.46 billion the company generated one year earlier. The vast majority of this growth came from a 7% rise associated with the company's CooperVision product line. This centers around the sale of contact lenses. The big drivers here were the toric and multifocal categories, with sales up 10% and 14%, respectively. But on a percentage basis, the real driver was CooperSurgical. Revenue there spiked 11.1%, climbing from $778.8 million to $865.3 million. Office and surgical sales under this segment jumped from $455.9 million to $506.6 million thanks to strong demand for products like Paragard, Uterine Manipulators, Fetal Pillow, and more. Consumable products, genetic testing offerings, embryo options, and others bumped up the fertility category from $322.9 million to $358.7 million.

On the bottom line, however, the picture for the firm worsened. Net profits went from $320.2 million in the first nine months of 2022 to $209.7 million the same time this year. Despite the jump in sales, profits were put under pressure because of multiple reasons. For instance, selling, general, and administrative costs, rose from 40% of sales to 42%. While a good portion of this cost increase came about because of management working to push sales higher, the firm was also hit to the tune of $45 million from a termination fee under an asset purchase agreement related to Cook Medical's reproductive health business. Higher share based compensation and other related expenses pushed corporate costs under the selling, general, and administrative category up by 31% year over year.

Another contributor to the company's bottom line issues was research and development. But this was both small relative to overall revenue and should be applauded because it represents an investment in the company's future. Total research and development costs jumped 24% year over year. But that was an increase of only $19.5 million. And finally, interest expense for the enterprise skyrocketed, more than doubling from $34.5 million to $79 million. And that, management said, was thanks to higher interest rates. The good news is that interest rates will likely start dropping next year. So if they do, this would be short lived.

{kind=link}

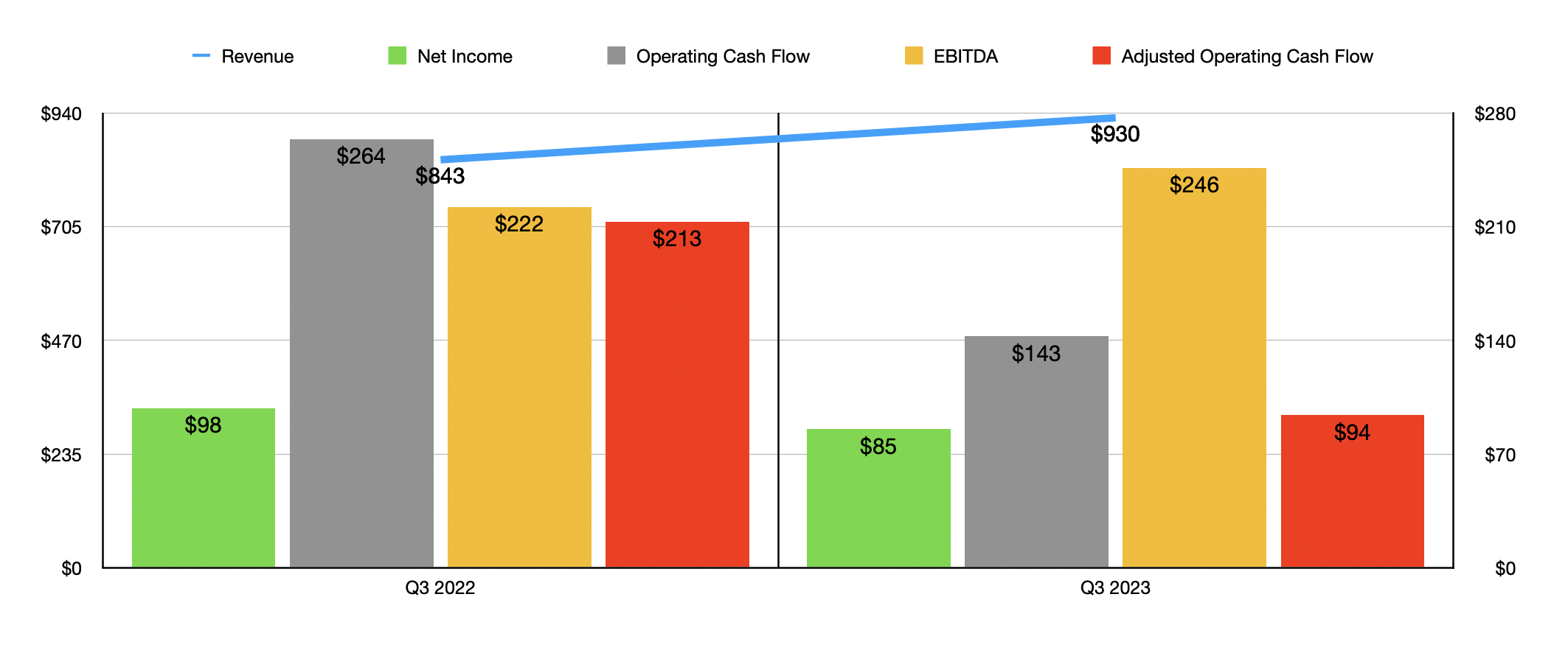

Unfortunately, the decline in profits also caused cash flow metrics to worsen. Operating cash flow, for instance, went from $561.7 million to $433.3 million. If we adjust for changes in working capital, the decline would have been from $517.2 million to $309.1 million. The only profitability metric that actually improved year over year was EBITDA. According to the data provided, it inched up from $661.2 million to $672.4 million. It's important to note that the bottom line pain for the company continues into the present day. As you can see in the chart above, profits and cash flows were down in the third quarter of the year relative to the same time last year.

{kind=link}

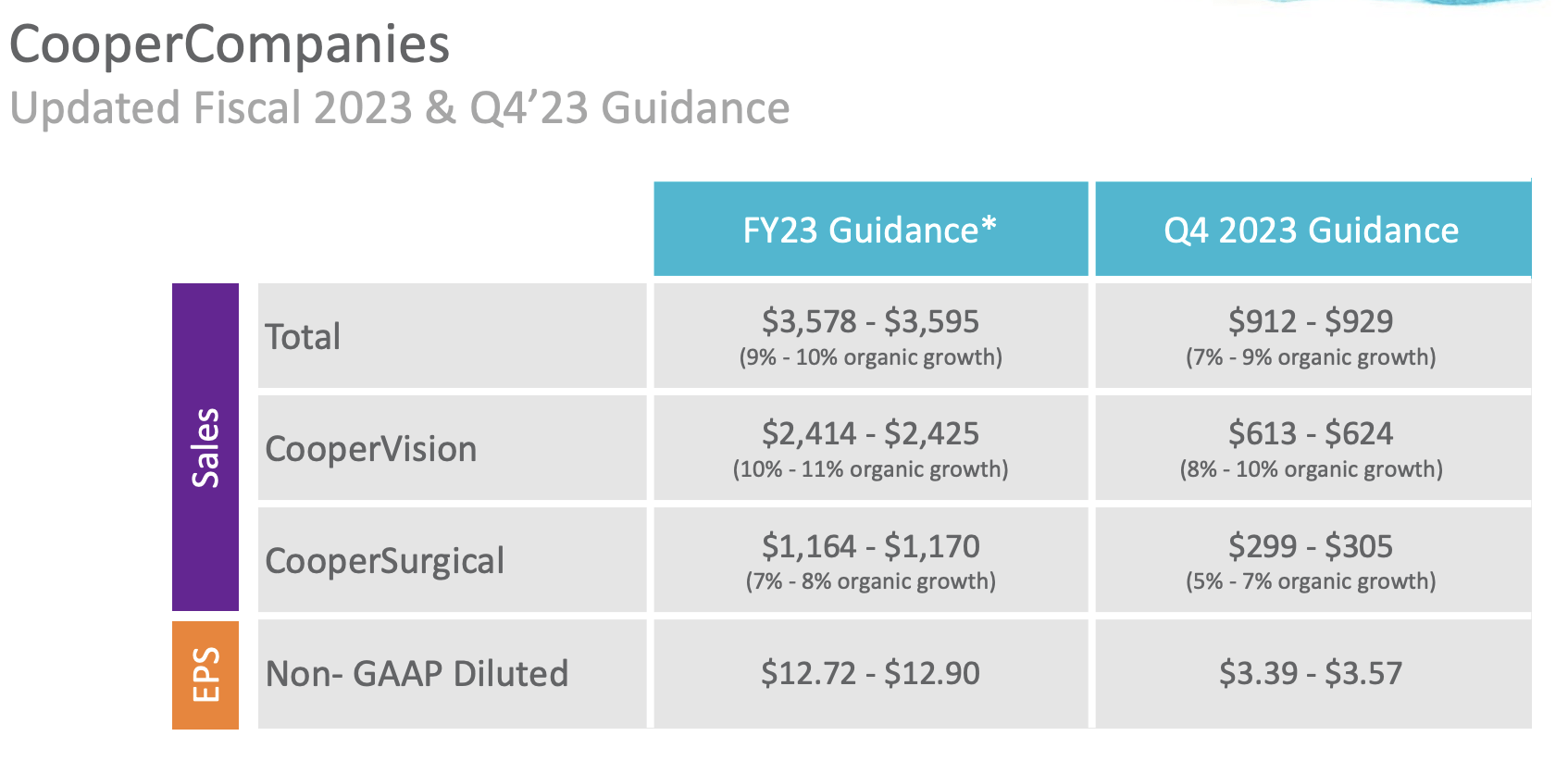

When it comes to 2023 in its entirety, management has said the overall revenue should be between $3.58 billion and just under $3.60 billion. That would translate to a 9% to 10% organic growth rate, with CooperVision leading the way with a 10% to 11% organic growth rate. Adjusted earnings per share, meanwhile, should be between $12.72 and $12.90. That would translate to adjusted profits of $639.2 million. That would be modestly higher than the $617.3 million reported last year. Based on my own estimates, adjusted operating cash flow should be around $517.8 million, while EBITDA should be somewhere around $899.8 million.

{kind=link}

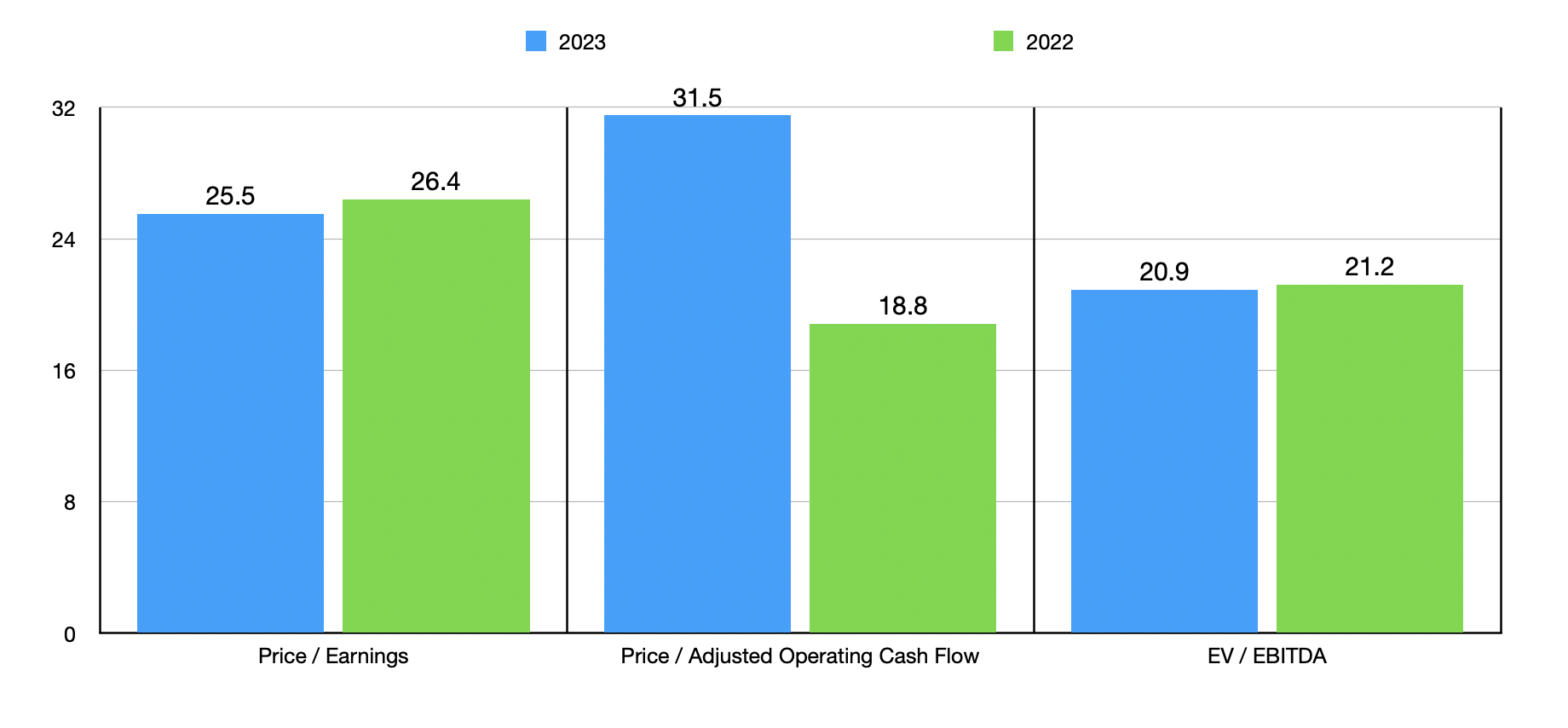

In the chart above, you can see how shares are priced, both on a forward basis and relative to what the company achieved in 2022. In two of the three ways, the stock does look a bit cheaper. But when it comes to adjusted operating cash flow, it looks far more expensive. In the table below, meanwhile, I compared the enterprise to five similar firms. On a price to earnings basis, only one of the companies was cheaper than it. But when it comes to both the price to operating cash flow approach and the EV to EBITDA approach, three of the five ended up being cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Cooper Companies |

| 25.5 |

| 31.5 |

| 20.9 |

| DENTSPLY SIRONA (XRAY) |

| 19.3 |

| 21.9 |

| 9.5 |

| ICU Medical (ICUI) |

| 360.7 |

| 69.2 |

| 17.8 |

| QuidelOrtho Corporation (QDEL) |

| 108.5 |

| 15.1 |

| 10.6 |

| Neogen Corporation (NEOG) |

| 442.2 |

| 89.8 |

| 39.1 |

| Alcon (ALC) |

| 108.4 |

| 28.8 |

| 33.7 |

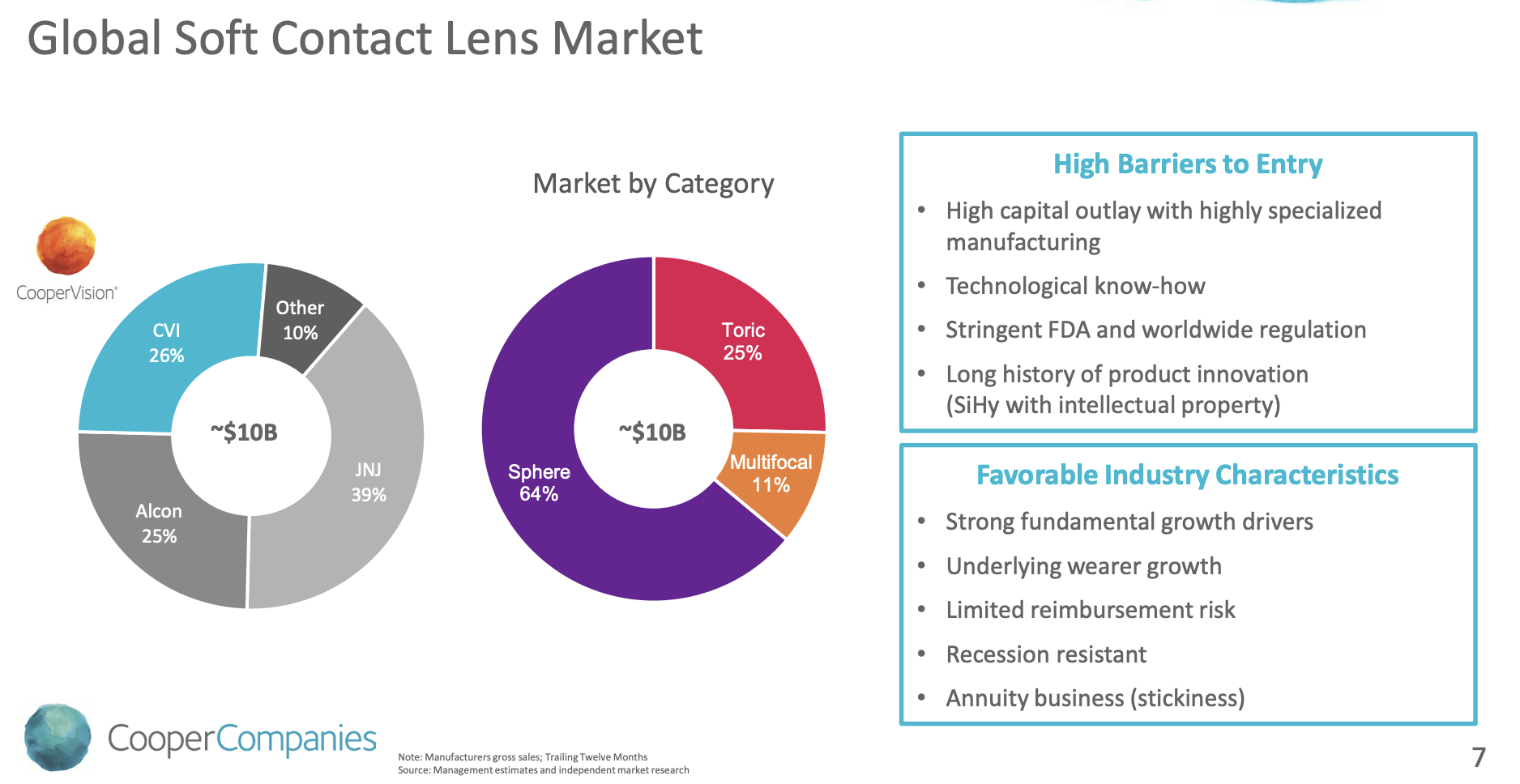

Based on the recent weakness that the company has seen so far this year, as well as on how shares are priced, I do believe that a 'hold' rating is still appropriate, if barely, for the firm. Having said that, I do believe that, in the long run, management will continue to grow the enterprise. How much growth, however, is up for debate. And this is because the business already has a massive market share in the areas in which it operates. In the global soft contact lens market, for instance, a market that is worth $10 billion, the company has a 26% market share.

{kind=link}

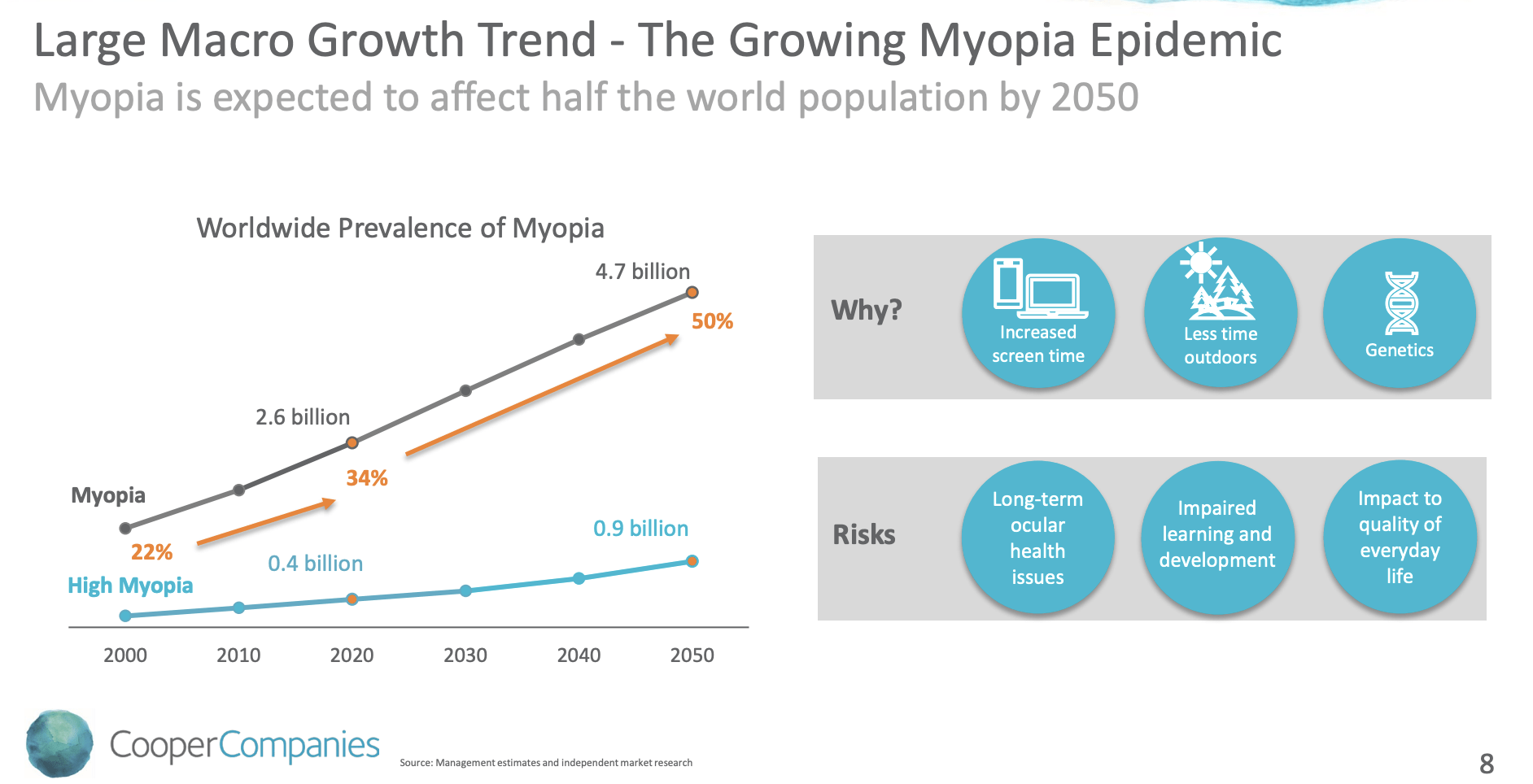

But even if this market share remains unchanged, the company does stand to benefit from continued growth in vision problems. As an example, in 2020, it was estimated that 2.6 billion people across the world had myopia, with roughly 0.4 billion having high myopia. By 2050, these numbers should grow to be 4.7 billion and 0.9 billion, respectively. Add on top of this an unspecified degree of higher net pricing that management expects to achieve in the many years to come, and there definitely is revenue potential for the firm. When it comes to the CooperSurgical unit's fertility division, the market is considerably smaller at around $2 billion. However, that space is expected to grow by between 5% and 10% per annum moving forward. Naturally, there are other niches that the company plays in under the CooperSurgical segment. But those are not considered to have the same kind of growth potential, according to management, that the fertility category does.

{kind=link}

Takeaway

I understand why some investors might be interested in The Cooper Companies. Operationally, I am fascinated by the enterprise. In the long run, I suspect it will continue to grow, and it may even succeed in capturing additional market share. But it's important not to get emotions involved in the picture. When you look at the numbers, you see a company that is growing revenue consistently, but that has seen a weak spot in earnings and that has shares that are trading at levels that aren't exactly cheap. The company does deserve some slack because of its large share of the contact lens market. But it's not enough for me to rate the company anything higher than a 'hold' at this time.

For further details see:

The Cooper Companies: Nothing To See Here