EPRT - The Cream Always Rises To The Top: Always Insist On Quality

2024-01-18 07:00:00 ET

Summary

- I always enjoy writing on quality stocks.

- Because quality stocks with healthy balance sheets are more likely to succeed in the long run.

- We track high-quality REITs with sector diversification.

- I selected four of the highest quality REITs using a new index screener.

They say “ the cream always rises to the top ,” meaning the best always stand out eventually. And while that idea can be debated in so many areas of life…

I think it’s a distinctive rule when it comes to investing.

Oh, it might often seem otherwise, especially when certain categories of stocks are in a bubble. At times like that, the most ridiculous companies can obtain the most positive valuations, while actually worthwhile stocks are left floundering or worse.

The dot.com craze was a good example of this. There were so many examples of absolutely ridiculous companies getting tons of money in the years leading up to 2000.

Note that I say “getting” and not “making” or “keeping.” There’s a difference.

Take Kozmo.com, a delivery service that allowed certain big-city residents the chance at instant retail gratification. People could order a product – from electronics to a pint of Ben & Jerry’s ice cream – and have it delivered to their door in the next 60 minutes.

All without paying a delivery fee.

The concept itself was popular, mind you. Why wouldn’t it be? And according to CNN , Kozmo bagged “about $280 million from investors, including $60 million from Amazon and a $150 million promotion deal with Starbucks.”

However, “free delivery and no minimum purchase” led to the company crashing and burning. Just one more example of how the non-cream always eventually drops to the bottom.

Don’t let your profits do the same. Commit to quality every time.

An idea That’s Literally Built on the Q Word (Quality)

That insistence is why I was more than happy when one of my readers asked me about the subject recently. The reader wrote:

“Thanks again for helping people like me who have so much to learn about REITs. Are you planning a piece on companies with iREIT scores above 90?”

This was in response to my “ Who’s Buying BBB+ Rated REITs ” article, published on Jan. 11. It detailed companies that S&P had rated at the bottom of the investment-grade ladder – but still found worthy of the investment-grade title.

These stocks can have greater growth advantages than their more highly rated competitors. Yet they still have healthy balance sheets, which shows they’re not taking foolish risks in order to achieve that growth.

In order to determine what a quality stock is we consider a variety of factors such as:

- Earnings strength and consistency

- Dividend strength and reliability

- Dividend safety

- Balance sheet strength

- Forward-looking growth (analyst estimates)

In which case, you might not be surprised to see which REITs make the cut…

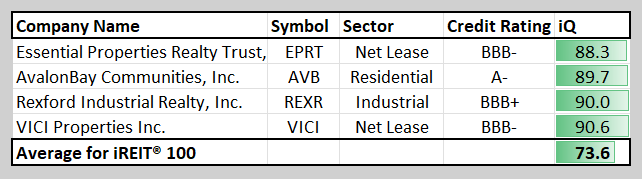

VICI Properties ( VICI )

VICI is a gaming REIT with some of the highest quality properties you can think of such as Caesars Palace on the Las Vegas Strip that totals more than 8.5 million square feet and includes world-renown gaming facilities.

In addition to its casinos, Caesars Palace is constructed with six towers containing almost 4,000 hotel rooms, a nightclub, multiple restaurants, bars and lounges, a 4,300 seat coliseum venue, and retail outlets throughout the property.

VICI - IR

Or Excalibur in Las Vegas which is operated MGM Resorts and totals more than 2.8 million SF, including 93,000 SF of gaming space, approximately 3,980 hotel rooms, a spa and fitness center, multiple restaurants and bars, and around 25,000 SF of convention facilities.

VICI - IR

When it comes to high-quality trophy properties there are not many others in VICI’s league. VICI has a 127 million SF portfolio that's comprised of 54 gaming facilities and 39 non-gaming facilities for a total portfolio of 93 experiential assets located across the U.S. and Canada.

VICI’s core-gaming properties are located across 15 states and total 124.0 million SF, including 4.0 million SF of casino space, 7 million SF of convention space, more than 60,000 hotel rooms, approximately 500 retail outlets, and over 500 bars, restaurants and nightclubs.

{kind=link}

VICI - IR

VICI’s non-gaming experiential assets total 39 properties covering 2.4 million SF across 17 states. Their non-gaming experiential properties are primarily family entertainment bowling centers that they acquired from Bowlero ( BOWL ) just several months back. These properties contain more than 1,500 bowling lanes and more than 1,100 arcade machines across 17 states.

{kind=link}

VICI - IR

And don’t forget about the four championship golf courses which include the Cascata in Las Vegas, Chariot Run in Indiana, Rio Secco in Las Vegas, and Grand Bear which is a Jack Nicklaus designed course in Mississippi.

{kind=link}

VICI - IR

VICI and its portfolio of trophy properties is all about quality. Additionally, VICI has some of the highest-quality gaming and hospitality operators including Caesars and MGM Grand, which are VICI’s largest two tenants and have W.A. extended lease terms of 31.9 and 51.5 years, respectively.

100% of VICI’s leases are structured on a triple-net basis, 91% of their rent roll have parent guarantees, and approximately 75% of their rent roll consists of tenants that are S&P 500 companies.

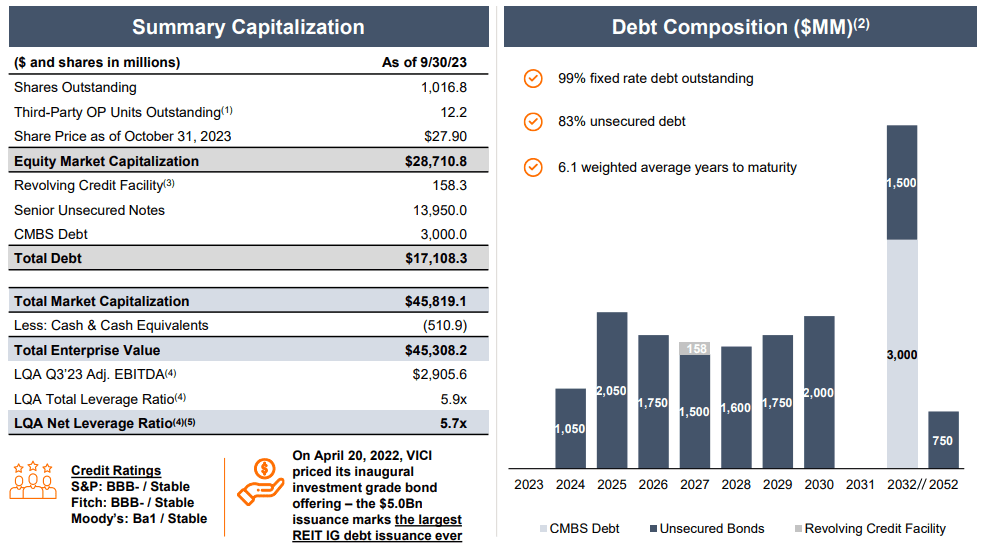

Additionally, VICI has an investment-grade balance sheet with a BBB- credit rating and debt that is well structured with 99% of their debt carrying a fixed rate, 83% unsecured, and W.A. term to maturity of 6.1 years. The gaming REIT is not overleveraged with a net leverage ratio of 5.7x and an EBITDA to interest expense ratio of 4.07x.

{kind=link}

VICI - IR

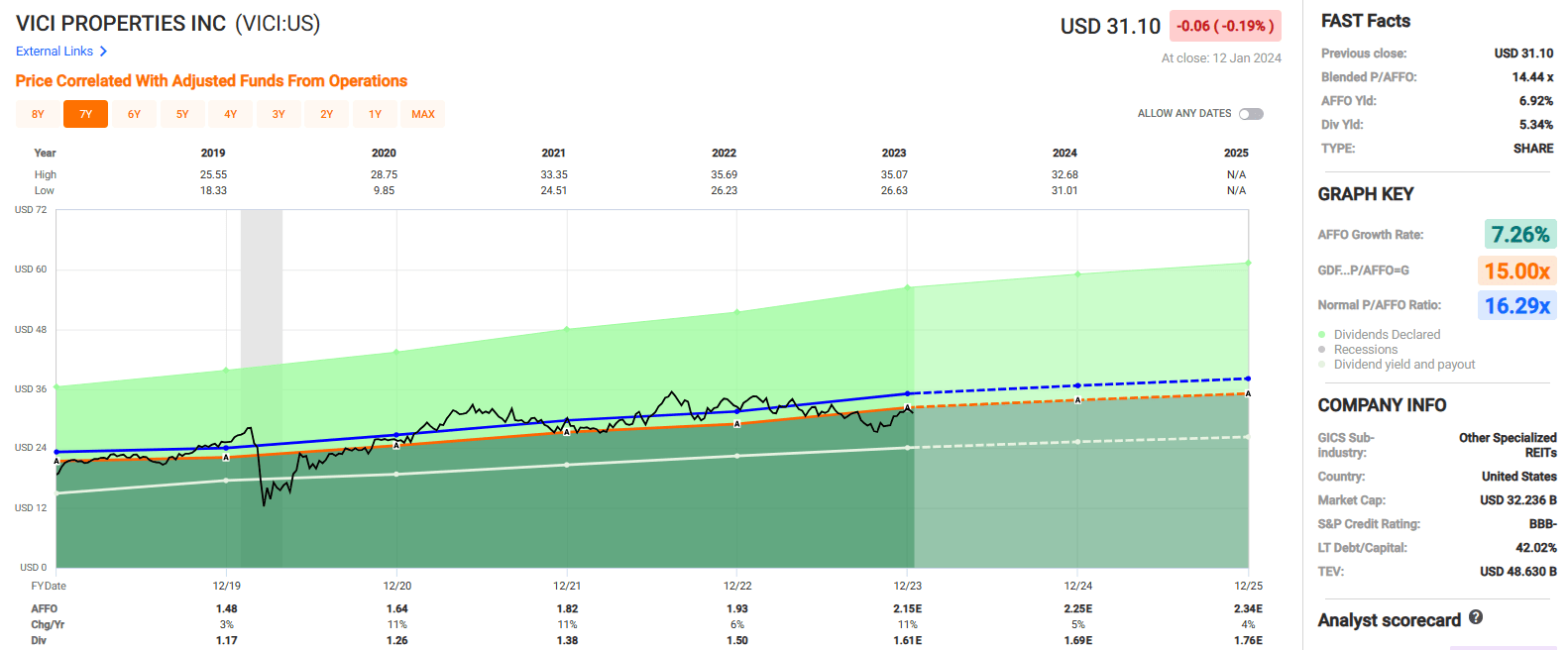

Since 2019 VICI has delivered an average AFFO growth rate of 7.26% and an average dividend growth rate of 10.11%. Analysts expect AFFO per share to increase by 5% in 2024 and then increase by 4% the following year.

The stock pays a 5.34% dividend yield that is well covered with an AFFO payout ratio of 74.88% and trades at a P/AFFO of 14.44x, compared to its average AFFO multiple of 16.29x.

We rate VICI Properties a Buy and assign it a quality rating of 90.5.

{kind=link}

FAST Graphs

Rexford Industrial Realty ( REXR )

Rexford Industrial might not have the same type of trophy properties as VICI, but what they do have is industrial properties located in what many would argue is the highest-quality industrial region in the world.

REXR differentiates its investment strategy from many of its industrial REIT peers by exclusively focusing on industrial properties located throughout infill Southern California (“SoCal”).

Rather than diversifying their properties across multiple states or countries, REXR attempts to be the market leader in the top industrial market.

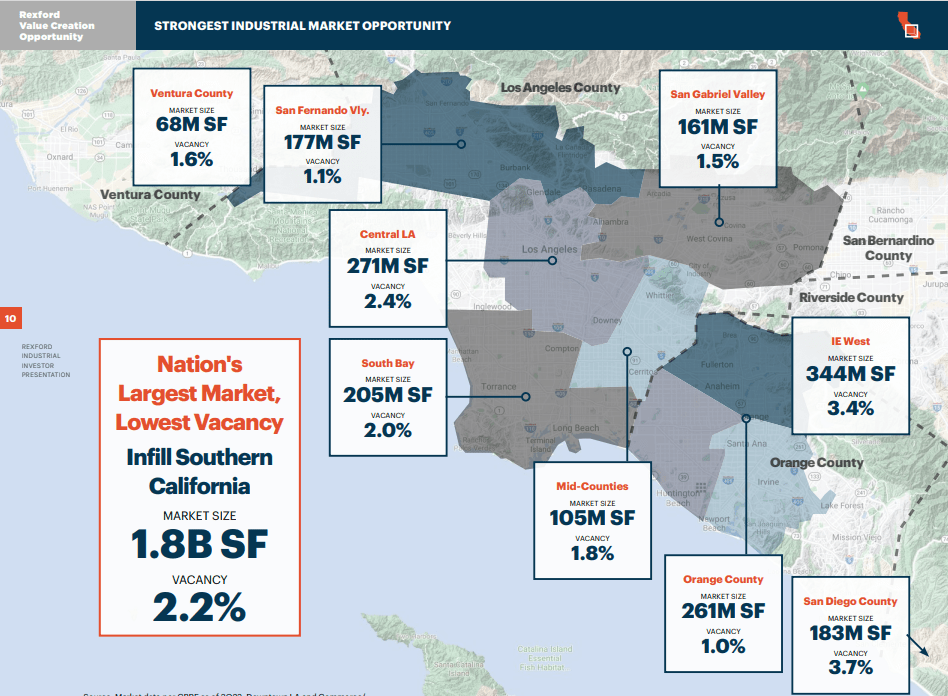

SoCal has a perpetual supply and demand imbalance due to the vast economy and the limited supply of developable land in the region. It's the largest U.S. industrial market and the fourth largest global industrial market with more than 600,000 businesses and approximately 22 million residents.

While there's high demand for products flowing through REXR’s distribution centers, SoCal is the lowest supply risk market in the U.S. due to the scarcity of developable land.

The SoCal region is surrounded by natural barriers including the ocean to its west and the mountains to its east, which makes land suitable for development a finite resource. That combined with restrictive zoning regulations constrains supply in SoCal while the demand for goods and services continues to grow.

As Will Rogers once said:

“Buy land. They ain’t makin’ any more of the stuff.”

REXR has a mission-critical, irreplaceable portfolio that consists of 373 industrial properties covering roughly 45.8 million SF across the SoCal region which serve a tenant base of approximately 1,600.

To highlight the favorable dynamics of the SoCal infill market, at the end of the third quarter, REXR reported releasing spreads of 64.8% on a GAAP basis, and 51.4% on a cash basis.

{kind=link}

REXR - IR

In addition to REXR’s irreplaceable industrial properties, the SoCal focused REIT has a very high-quality rating due to its impeccable balance sheet.

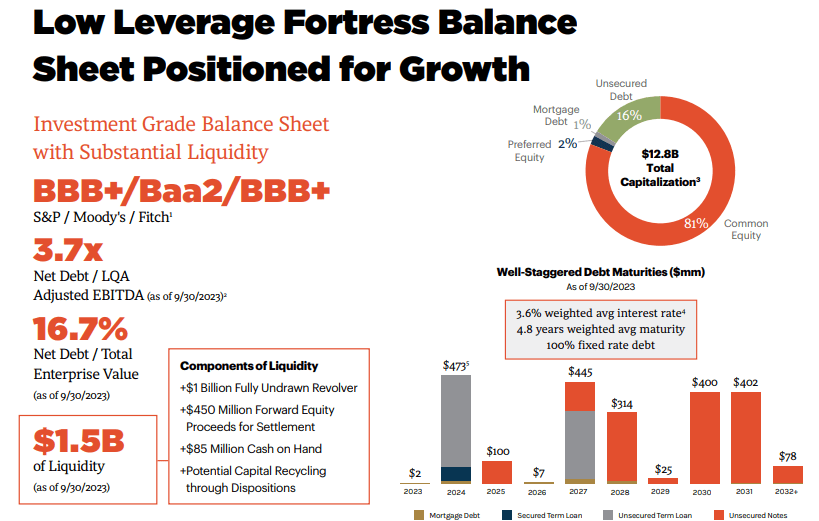

Rexford is investment-grade with a BBB+ credit rating and has excellent debt metrics including a net debt to adjusted EBITDA of 3.7x, a long-term debt to capital ratio of 24.23%, and an EBITDA to interest expense ratio of 7.92x.

Their debt is 100% fixed rate with a weighted average interest rate of 3.6% and a weighted average term to maturity of 4.8 years. Plus, the company reported $1.5 billion of liquidity as of the end of the third quarter.

{kind=link}

REXR - IR

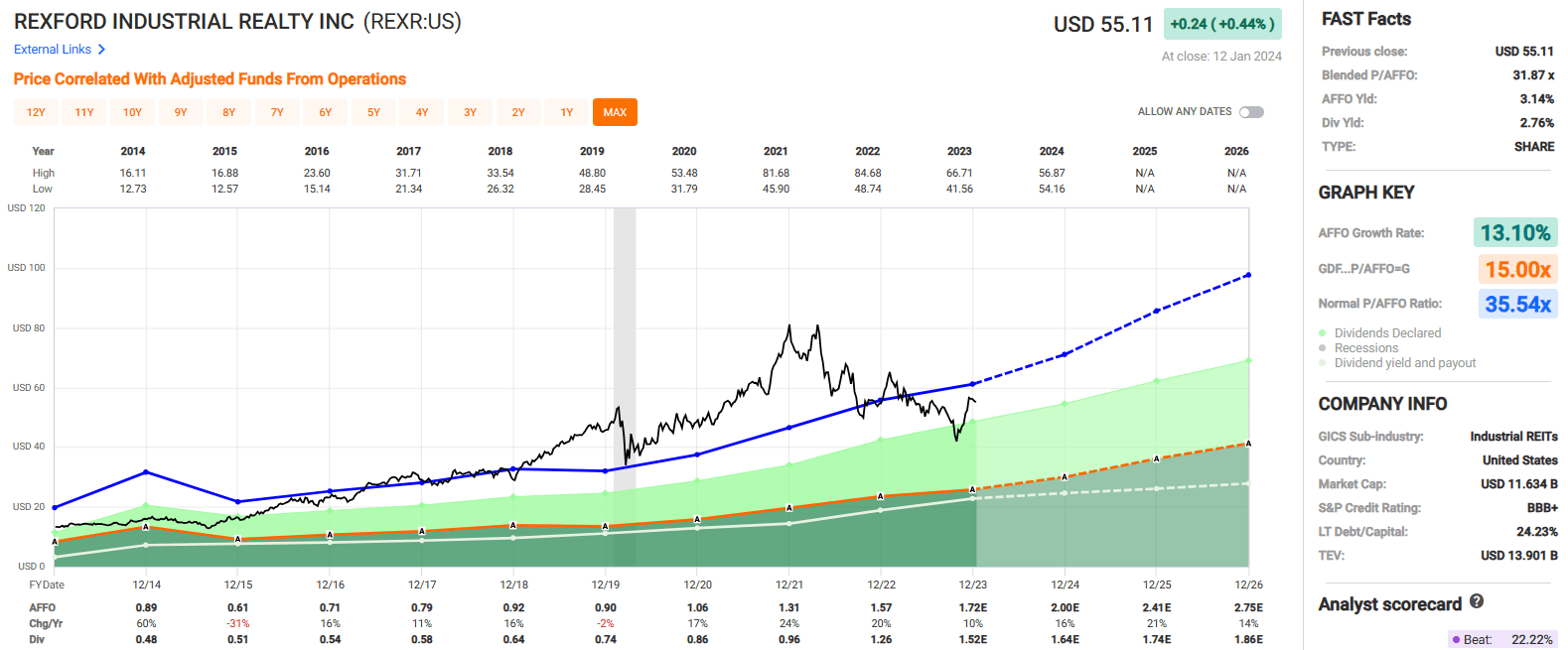

As one might expect from the releasing spreads REXR reported in 3Q23, they have delivered very strong AFFO growth since 2014 with a blended average AFFO growth rate of 13.10% since that time. Analysts expect this trend to continue with AFFO per share expected to increase by 16% in 2024 and then increase by 21% in 2025.

REXR pays a 2.76% dividend yield that is well covered with an AFFO payout ratio of 88.4% expected in 2023, and an expected 2024 AFFO payout ratio of approximately 82%.

While the 2.76% yield might not be the highest in the REIT sector, this is dividend growth company with an average dividend growth rate of 13.08% over the past eight years.

Currently shares are trading at a P/AFFO of 31.87x, compared to its average AFFO multiple of 35.54x.

We rate Rexford Industrial a Strong Buy and assign it a quality rating of 89.9.

{kind=link}

FAST Graphs

AvalonBay Communities ( AVB )

AvalonBay is the largest publicly traded multifamily REIT with a market cap of approximately $26 billion and a portfolio comprised of 296 multifamily communities containing roughly 89,200 apartment homes across 12 states and the District of Columbia.

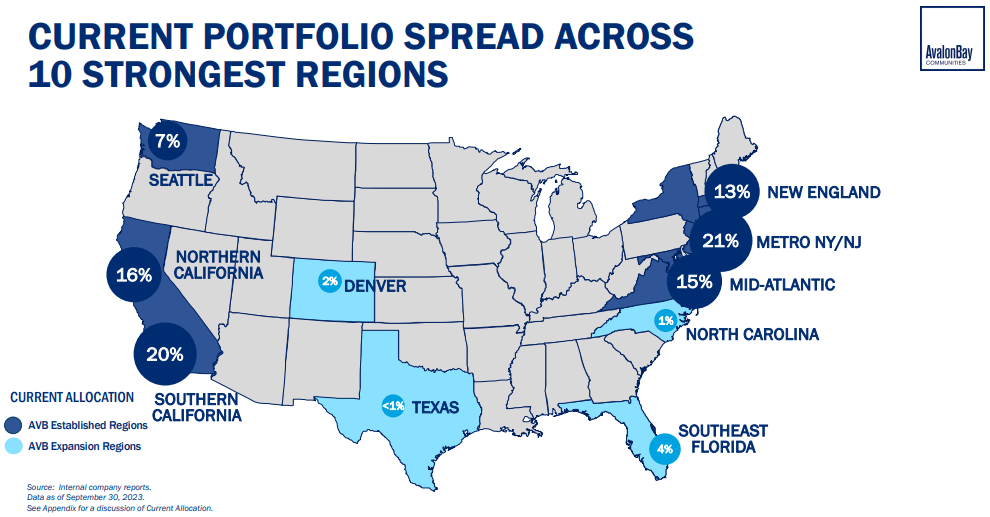

AVB specializes in the development, acquisition, and management of high-quality apartment communities in leading metropolitan areas primarily located in New England, New York and New Jersey, the Mid-Atlantic, California, and the Pacific Northwest.

The apartment REIT targets locations in regions that have growing employment in high wage job sectors and regions where there is lower housing affordability. In addition to their established markets listed above, AVB has been recently expanding into the Carolinas, Florida, Texas and Colorado.

As of Sept. 30, 2023, AvalonBay reported a same-store economic occupancy of 95.7% and a same-store average rental revenue of $2,962.

{kind=link}

AVB - IR

Now as many of my followers know, I have a real appreciation for multifamily REITs with heavy Sunbelt exposure such as Mid-America ( MAA ) and Camden Property ( CPT ) due to the favorable migration trends.

AvalonBay has some Sunbelt exposure with its established markets in Southern California and its expansion markets in Texas, Florida, and the Carolinas, but they're also more geographically diversified with high-quality properties along the East and West Coast regions of the country.

Many of its established markets do not have the same supply risk as Sunbelt markets, and due to its premier locations, AVB is able to generate an average same-store rental revenue of almost $3,000 per unit, vs Mid-America which reported 3Q same-store average effective rent of $1,690 per unit, and Camden Property which reported an average monthly rental rate per apartment home of $1,999.

{kind=link}

AVB - IR

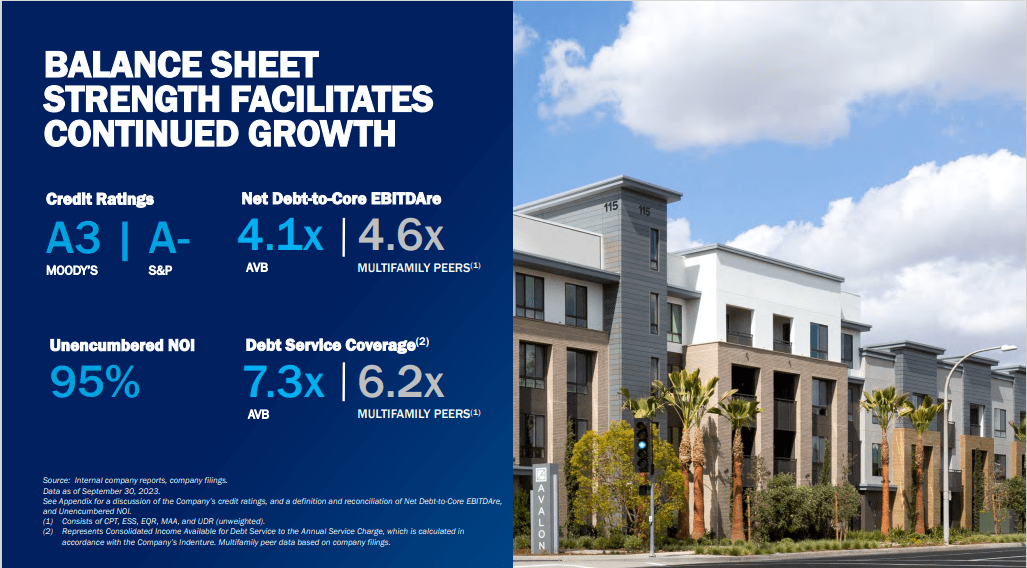

Along with its premier locations, AVB has a fortress-like balance sheet with an A3 credit rating from Moody’s and an A- rating from S&P Global.

95% of their net operating income (“NOI”) is unencumbered and the apartment REIT has excellent debt metrics including a net debt to Core EBITDAre of 4.1x, a long-term debt to capital ratio of 39.40%, and a debt service coverage ratio of 7.3x.

Additionally, their debt has a weighted average term to maturity of 7.5 years and the company reported $2.7 billion of liquidity as of their most recent update.

{kind=link}

AVB - IR

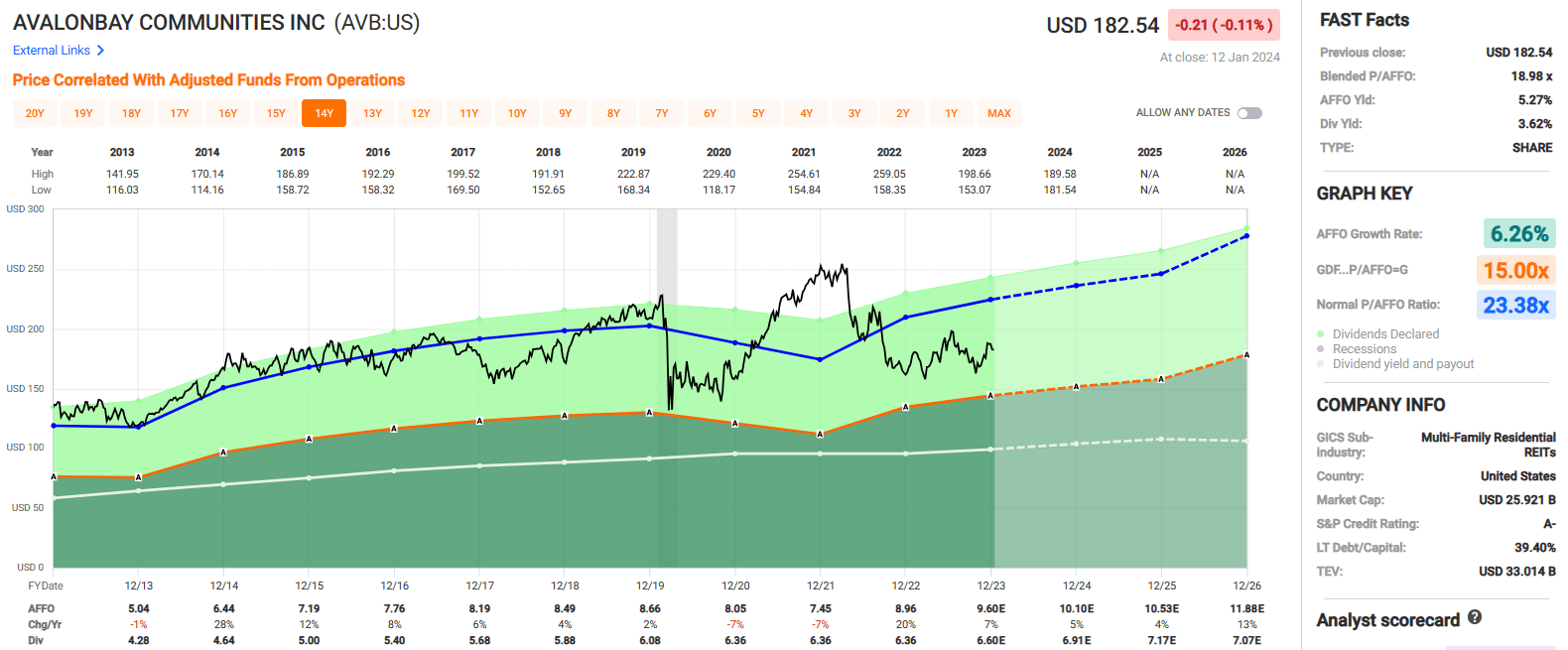

Since 2013 AvalonBay has had an average AFFO growth rate of 6.26% and an average dividend growth rate of 5.12%. Analysts expect AFFO per share to increase by 5% in 2024, by 4% in 2025, and by 13% in 2026.

AVB pays a 3.62% dividend yield that is well covered with a 2023 expected AFFO payout ratio of 68.75% and trades at a P/AFFO of 18.98x, compared to its average AFFO multiple of 23.38x.

We rate AvalonBay a Buy and assign it a quality score of 89.7.

{kind=link}

FAST Graphs

Essential Properties Realty Trust ( EPRT )

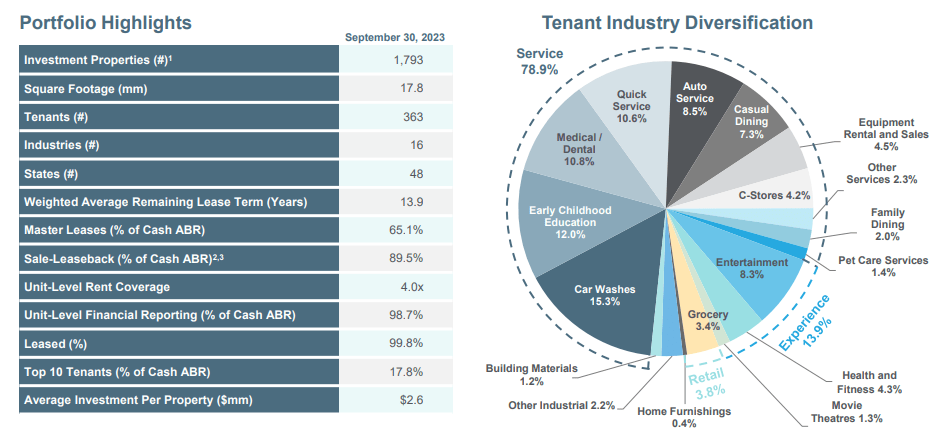

EPRT is a net lease REIT with a market cap of roughly $4 billion and a 17.8 million SF portfolio comprised of 1,793 commercial properties that are leased to 363 tenants across 48 states.

They own and manage a portfolio which primarily consists of single-tenant properties that are leased to middle-market companies which operate in experienced-based and service-oriented industries.

Some example industries that EPRT targets are restaurants, including family dining and quick service, car washes, convenience stores, early childhood education, auto services and medical services.

Their largest industry is car washes which represented 15.3% of their annualized base rent (“ABR”), followed by early childhood education and medical / dental offices which made up 12.0% and 10.8% of their 3Q ABR, respectively.

At the end of the third quarter, EPRT’s portfolio was 99.8% leased with a weighted average lease term of 13.9 years.

{kind=link}

EPRT - IR

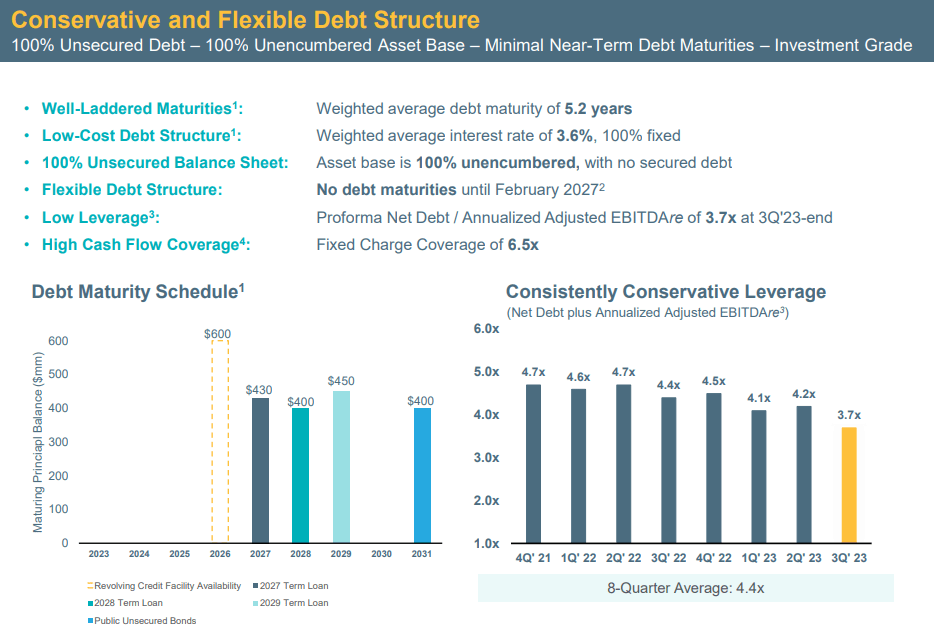

EPRT has an investment-grade balance sheet with a BBB- credit rating and healthy debt metrics including a pro forma net debt to adjusted EBITDAre of 3.7x, a long-term debt to capital ratio of 36.12%, and a fixed charge coverage ratio of 6.5x.

Additionally the asset base is fully unencumbered with no secured debt and 100% of their debt is fixed rate with a weighted average interest rate of 3.6% and a weighted average term to maturity of 5.2 years.

{kind=link}

EPRT - IR

EPRT is the least leveraged in its net-lease peer group when measured by net debt plus preferred to EBITDAre. EPRT’s leverage ratio was reported at 3.7x, compared to its closest peer NetSTREIT at 4.2x, Agree Realty ( ADC ) at 4.8x, and Realty Income at 5.0x.

The strength and flexibility of EPRT’s balance sheet is one of their strongest features and is a significant factor in its quality rating.

EPRT - IR

Having filed its IPO in 2018, EPRT is a relatively new company with a freshly assembled portfolio of net lease properties that are under long duration leases with an average unit-level rent coverage of 4.0x.

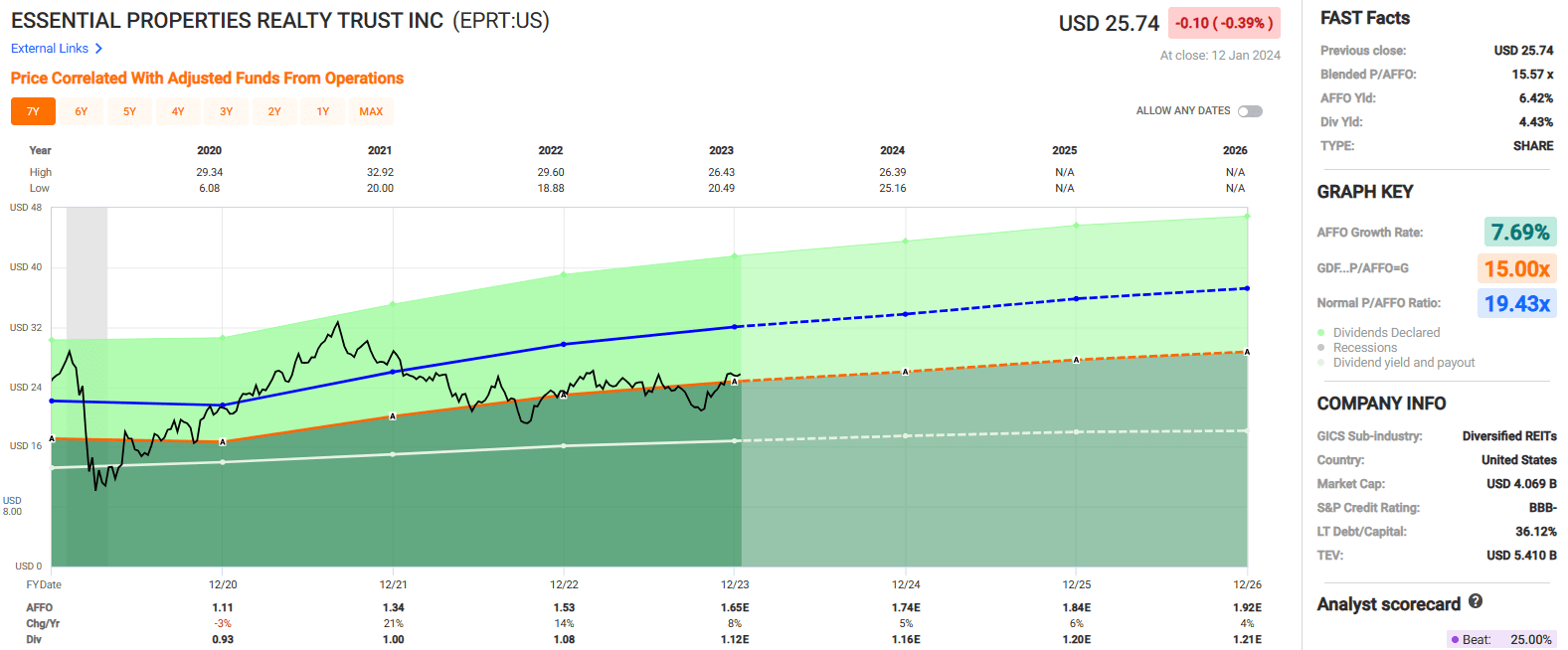

Since 2020, the net lease REIT has had an average AFFO growth rate of 7.69% and an average dividend growth rate of 6.22%. Analyst expect steady AFFO growth with AFFO per share expected to increase by 5% in 2024, and then by 6% the following year.

EPRT pays a 4.43% dividend yield that is well covered with an AFFO payout ratio of 67.88% and trades at a P/AFFO of 15.57x, compared to its average AFFO multiple of 19.43x.

We rate Essential Properties Realty Trust a Buy and assign it a Quality Score of 88.

{kind=link}

FAST Graphs

In Closing

These four REITs screen attractive based on quality and value:

{kind=link}

iREIT®

While some investors are reaching for double-digit yield, we believe a more sensible approach is to focus on quality.

There’s simply no need to be too cute, especially now.

If I can persuade just a few of them to avoid dangerous investment strategies and adopt sound ones (designed to preserve and maintain their hard-earned capital) I’m happy.

Stay tuned for “ The Rotten REITs That Stink ”.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

The Cream Always Rises To The Top: Always Insist On Quality