IFGL - The Credit Crunch That's Strangling Commercial Real Estate

2023-04-19 06:10:01 ET

Summary

- The next recession was supposed to be different for commercial real estate (“CRE”) – less painful, less focused on CRE. But recent events are challenging that view.

- The problem this time is not operating fundamentals, which remain relatively strong for most property types. Instead, CRE markets are being starved of the credit they need to function.

- A wave of investments must be refinanced in the next two years – just as property market conditions are weakening and banks are becoming weary of lending to CRE.

- Credit availability shrank further in March with strong deposit outflows from the financial institutions that provide much of the debt for CRE borrowers.

- The credit crunch will deepen and extend value declines and losses in commercial real estate.

Every recession is different. Each downturn hurts some sectors, some activities, some regions more than others. As it happens, the last two recessions – in addition to the brief Covid lockdown recession – were especially tough on CRE. Both the dot-com recession that began in 2001 and particularly the Great Financial Recession that started in late 2007 inflicted substantial pain on CRE owners and investors.

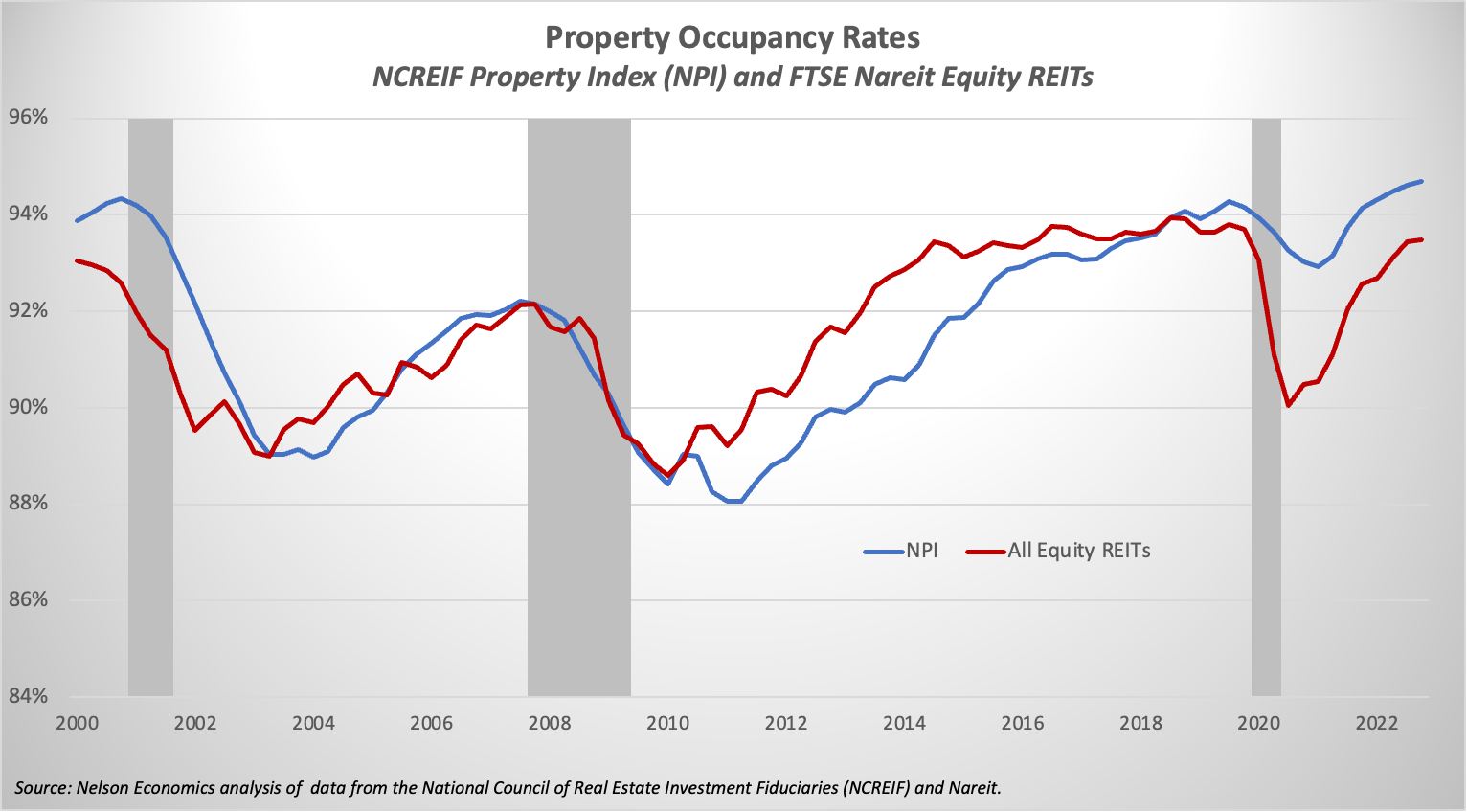

Operating performance in the REIT sector (as measured by Nareit’s All Equity REIT Index) and private institutional-owned real estate (as measured by NCREIF’s Property Index or NPI) both suffered as occupancy and net operating income (NOI) fell significantly in each recession. Peak-to-trough occupancy fell by an average of almost four percentage points (PPs).

Source: Nelson Economics analysis of data from the National Council of Real Estate Investment Fiduciaries (NCREIF) and Nareit.

{kind=link}

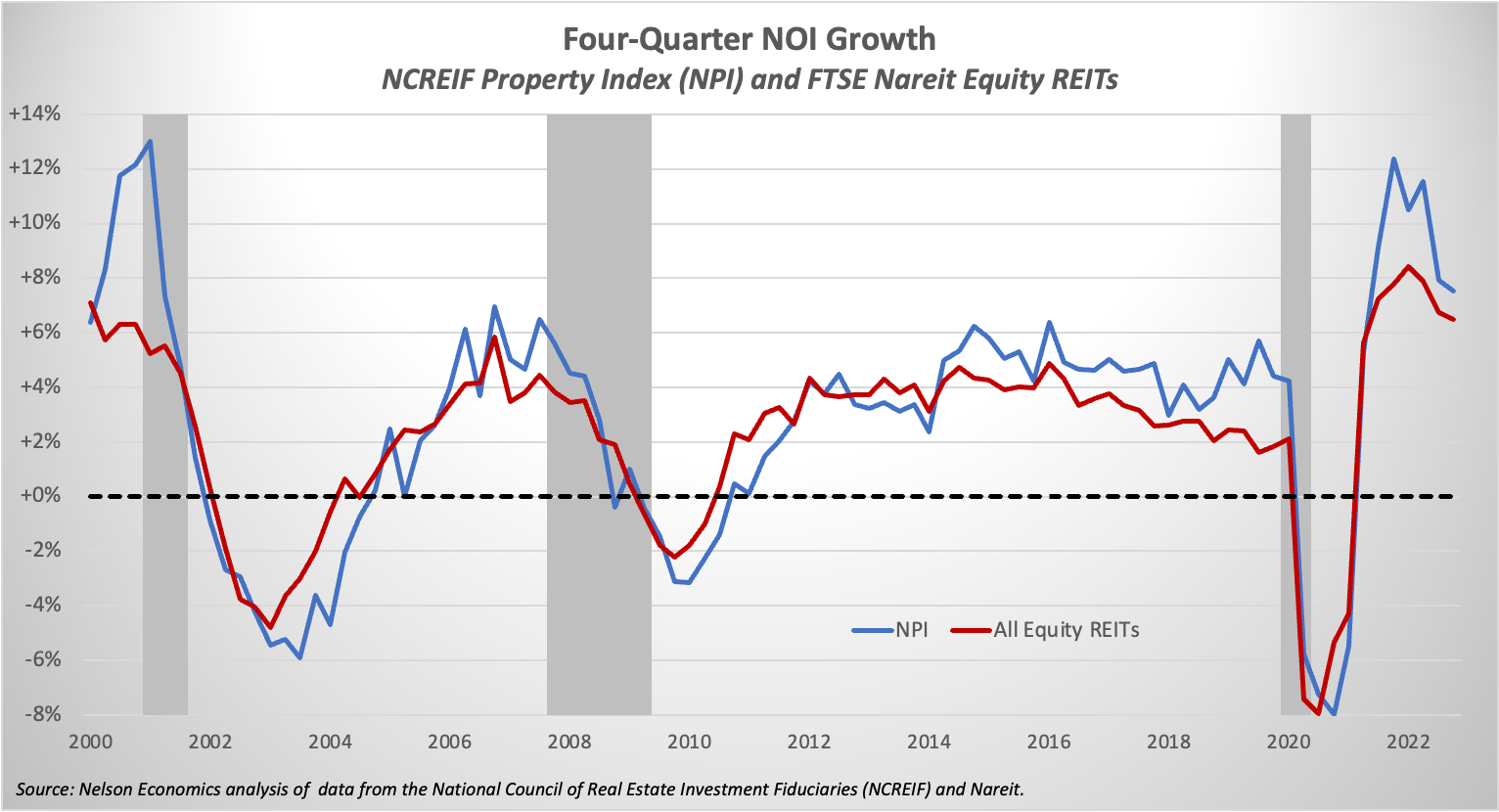

The decline in same-store NOI (controlling for asset composition) has been even more dramatic, with REIT NOI growth dropping by an average of about 10 pps and NPI income growth down by 14 pps. Once it turns negative, NOI growth tends to remain less than zero for about six quarters for REITs and seven quarters for NPI, though these durations have been declining.

Source: Nelson Economics analysis of data from the National Council of Real Estate Investment Fiduciaries (NCREIF) and Nareit.

{kind=link}

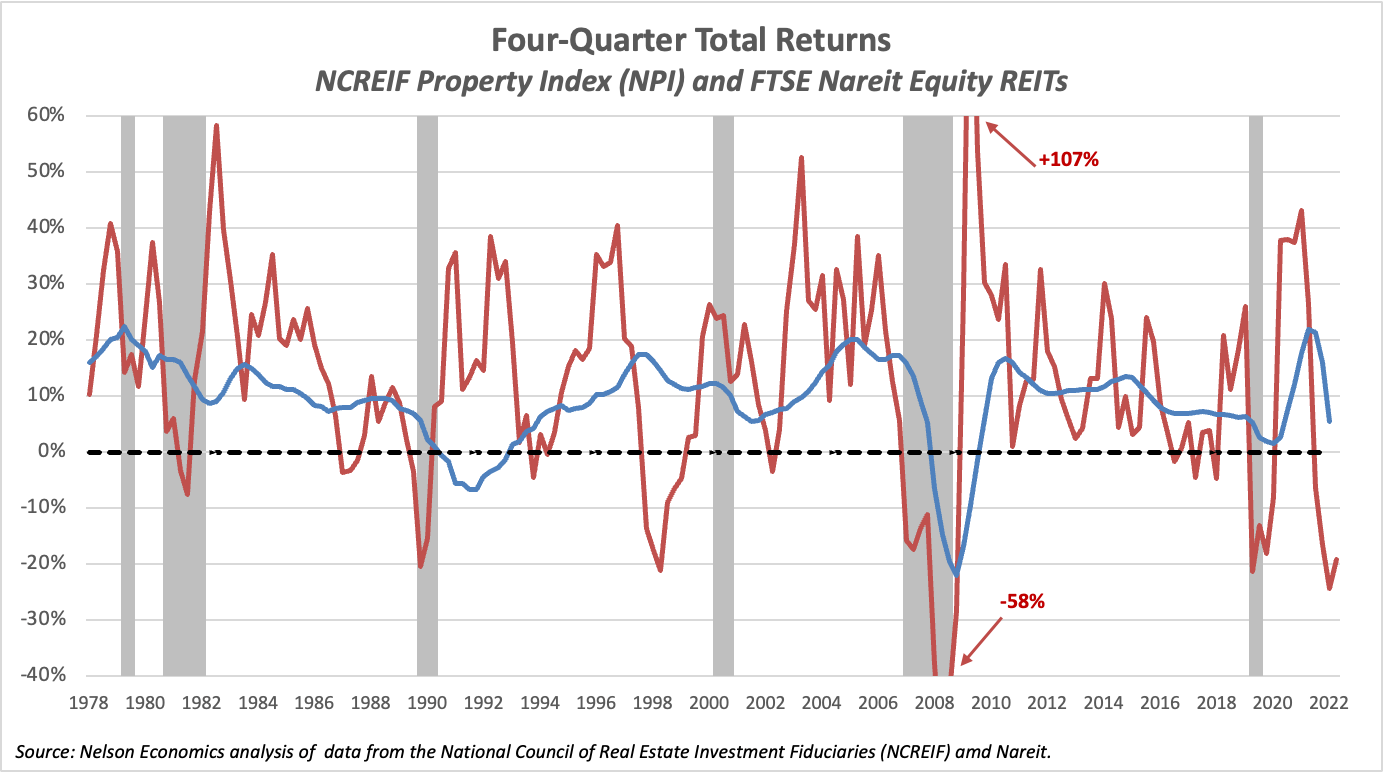

Property Returns Dive During Recessions

The impact on returns differs significantly between the private and public sectors. Valuations move slowly in the private markets compared to the relatively volatile REIT markets, where portfolios effectively reprice daily. This divergence can be seen clearly in the following chart comparing returns in the REIT sector (in red) versus the NPI (in blue) over time. REIT investors tend to amplify income swings, while private institutional investors dampen and delay value and return movements.

Source: Nelson Economics analysis of data from the National Council of Real Estate Investment Fiduciaries (NCREIF) and Nareit.

{kind=link}

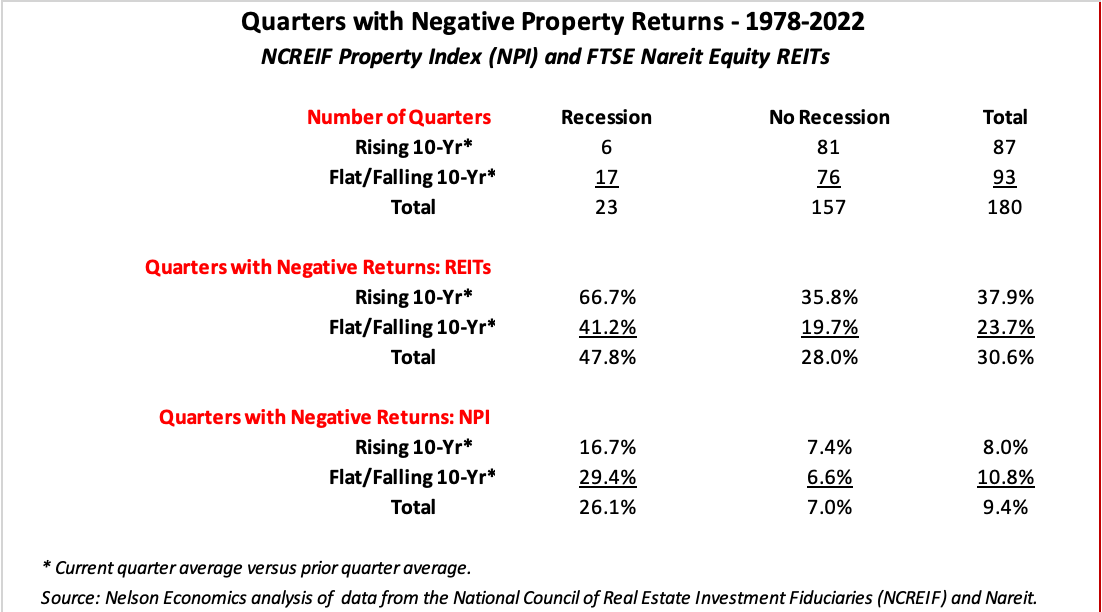

In the 45 years for which we have historical return data for both equity REITs and the NPI going back to 1978, the economy has been in a recession during 23 quarters. REIT returns have been negative in almost half of those recession periods (11 of 23), compared to just a fourth (5 of 23) for private real estate. (Property investment also can be highly sensitive to interest rates, especially in the REIT sector, where returns have been negative in 38% of the quarters with rising interest rates versus 24% in quarters with flat to falling interest rates.)

Sources: Nelson Economics analysis of data from the National Council of Real Estate Investment Fiduciaries (NCREIF) and Nareit.

{kind=link}

This Time was Supposed to be Different

But that was then. This next recession was supposed to be different. When we seemed to be possibly heading into a mild recession in 2019, I would advise clients to avoid recency bias and resist the fear that history would repeat itself with the next downturn. There was ample reason to be optimistic that the next recession would be kinder to CRE:

- construction levels were restrained compared with other recent expansions, so supply was generally balanced with demand;

- most property types were enjoying either record- or cycle-high occupancy and rents, as tenant demand remained healthy but not wildly strong;

- leverage was moderate relative to asset values (low Loan-to-Value Ratios) and revenues (low Debt Service Coverage Ratios);

- underwriting standards were generally sensible, particularly in light of the long (10-year) expansion that typically gives rise to risky lending as returns fall; and,

- capital markets were highly liquid as both equity and debt capital were ample.

In short, commercial real estate seemed well-positioned to weather the next economic storm, which in any case was widely anticipated to be mild, especially compared with the last recession. All the financial regulations put into place in the aftermath of the GFC helped to protect the CRE sector – and its financial enablers – from its worst instincts.

And with the conspicuous exception of the office sector, the Covid recession did not fundamentally alter CRE’s outlook. The economy recovered surprisingly quickly, and property fundamentals for most real estate types in most markets followed suit. Indeed, as shown in the first two charts above, property occupancy rates, and especially NOI growth, remain at historically high levels overall in both the public ((REIT)) and private real estate markets.

Yet there is growing cause for concern. This next downturn likely won’t be as hard on CRE as recent recessions. Still, it’s looking like real estate the impacts will be greater than might have been expected even a few months ago, particularly in the multifamily (apartment) and hard-hit office sectors.

Banks Are Cutting Credit to CRE

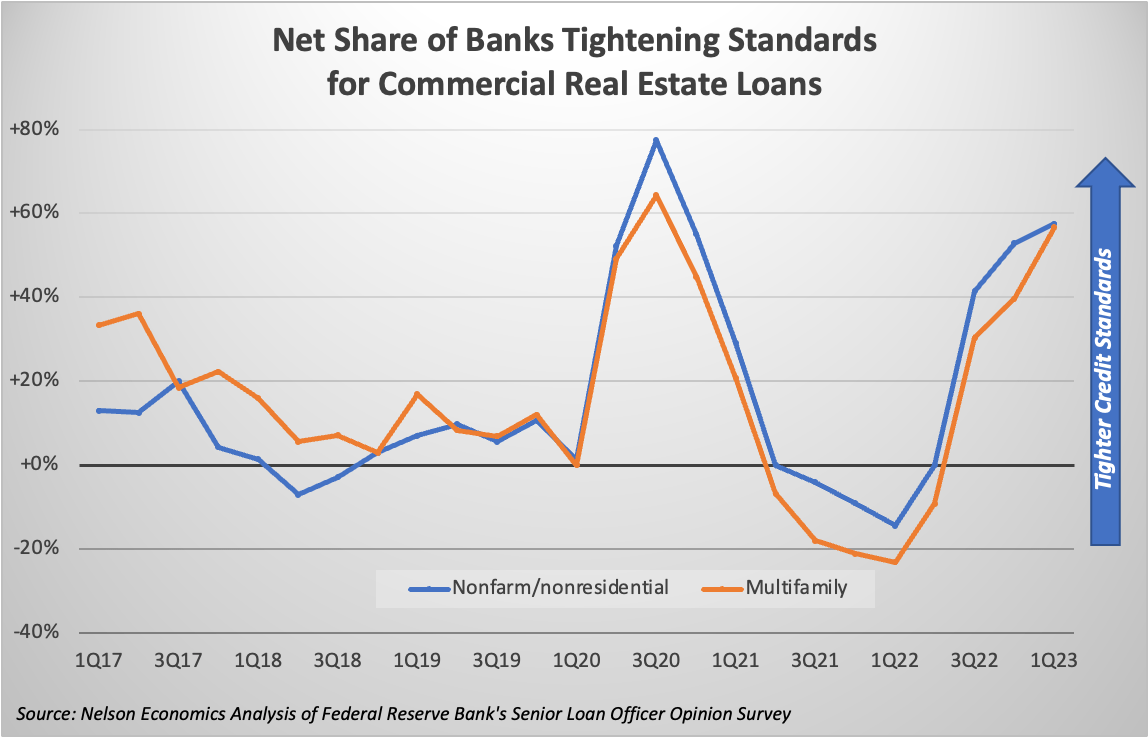

What’s changed? Commercial real estate markets are being starved of the credit they need to function. CRE is a debt-driven business, and most acquisitions are funded by short-term debt (less than ten years) that must be refinanced regularly. Moreover, landlords rely on debt to finance building and tenant space improvements needed to attract or retain new tenants. Banks started to tighten lending standards a year ago, in early 2022, when the Fed began to slow the economy by hiking rates. The Fed’s Senior Loan Officer Opinion Survey on Bank Lending Practices shows that lenders have been equally leery of multifamily ( orange line ) and commercial assets like offices and retail ( blue line ).

Source: Nelson Economics Analysis of Federal Reserve Bank's Senior Loan Officer Opinion Survey

{kind=link}

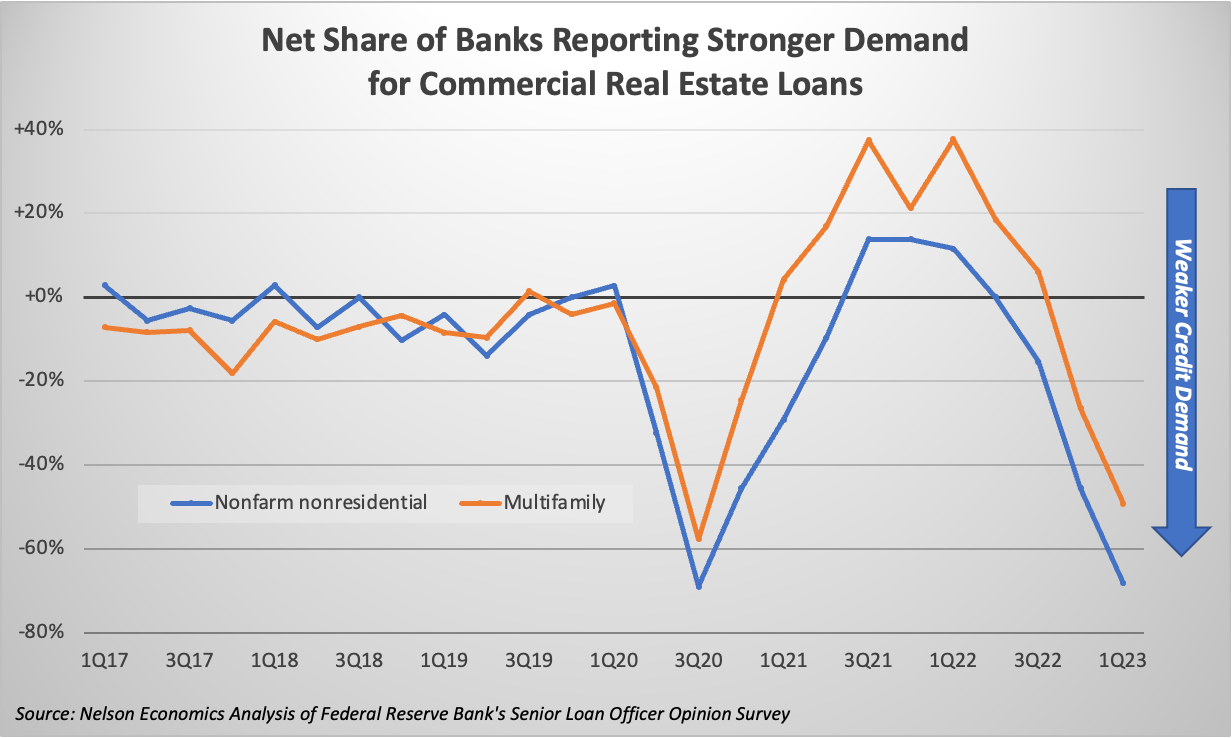

As it happens, this credit tightening – think of it as pulling back on credit supply – has been mirrored by an equivalent drop in credit demand as transactions have plunged while rising interest rates discourage discretionary refinancing.

Source: Nelson Economics Analysis of Federal Reserve Bank's Senior Loan Officer Opinion Survey

{kind=link}

Unfortunately, these figures are a bit dated. They were last updated in early February, reflecting surveys completed mostly in January – well before the March banking distress – and won’t be revised again until May. Whether or not this distress develops into an actual crisis, and whatever the eventual fallout within the banking sector, more recent indicators show it’s already having a material impact on CRE. Part of the evidence is anecdotal. Major owners are reporting they are being cut off from credit. Vornado Realty Trust’s April 8-K report that “There is no new debt available . . . When a loan comes due, the only refinance available (and that with a fight) is from the existing lender.”

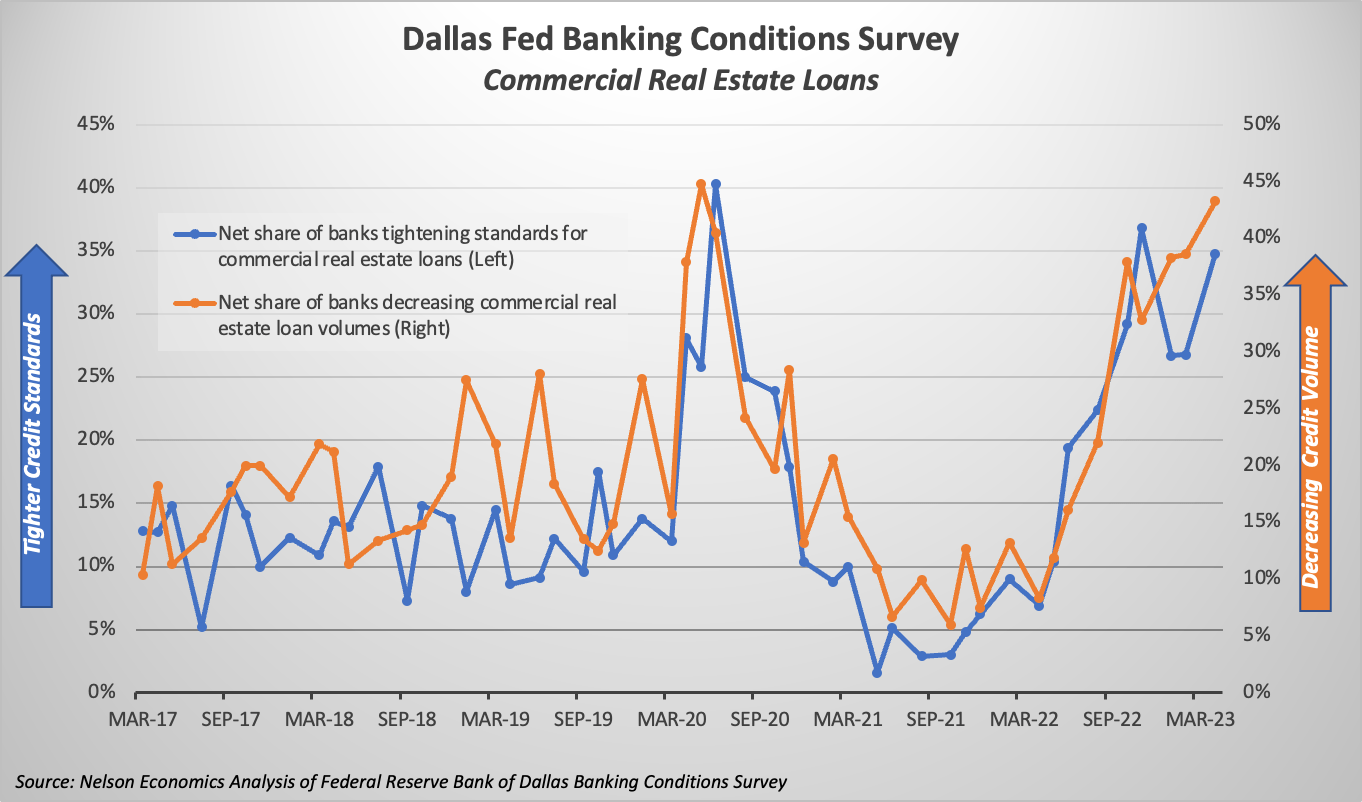

Vornado was referring specifically to office buildings, but the problem extends broadly throughout the property sector. The Dallas Fed publishes its own Banking Conditions Survey , and the latest report was based on surveys conducted March 21–29, so after the recent banking stresses peaked. The report shows that CRE credit availability continued to fall in March, with more banks reporting tighter credit standards ( blue line ) and more banks decreasing their CRE loans ( orange line ).

Source: Nelson Economics Analysis of Federal Reserve Bank of Dallas Banking Conditions Survey

{kind=link}

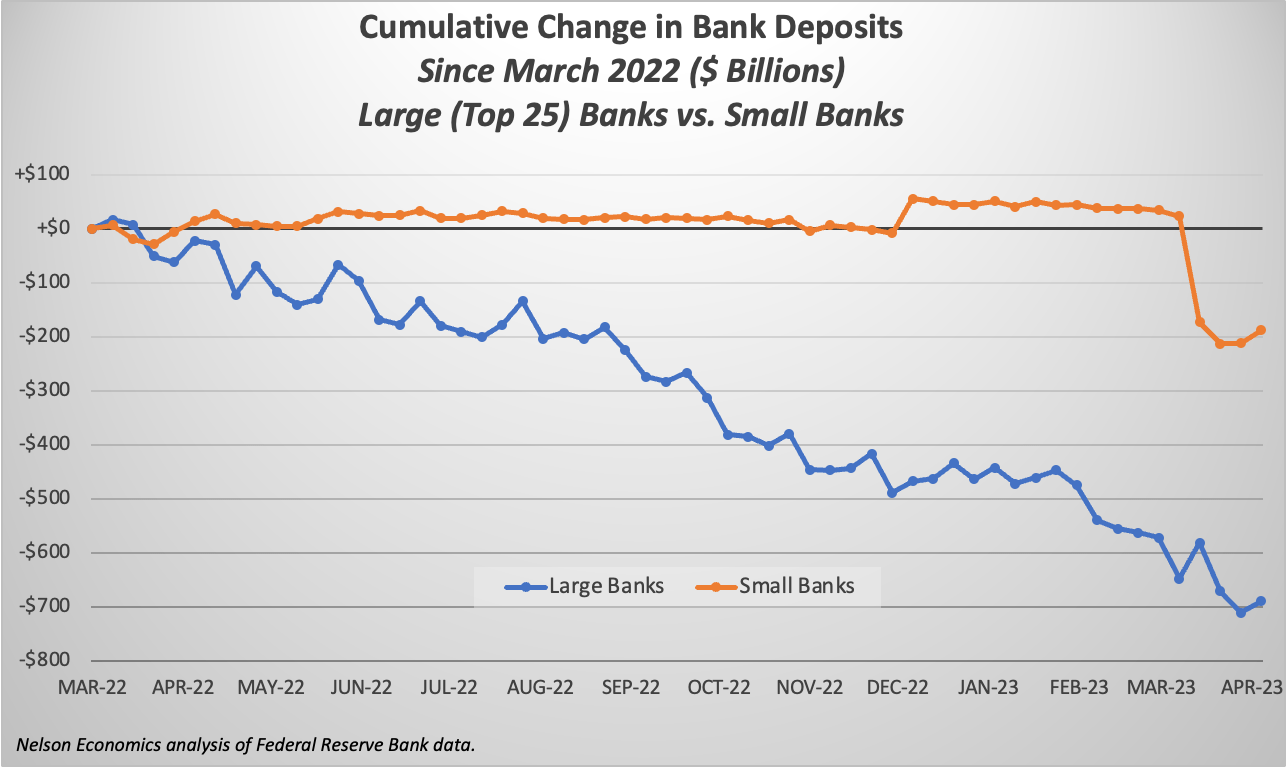

Lenders are getting more risk-averse as the CRE market outlook darkens. Plus, influential institutions like the Fed and the International Monetary Fund ((IMF)) are putting at least indirect pressure on banks to dial back their CRE lending through warnings about the growing risks in property markets. Now, their increasing reluctance to lend is being compounded by their declining capital capacity due to capital deposit outflows from their institutions. Federal Reserve data shows that “large” banks (the Fed term for the 25 largest banks ranked by assets) have been losing deposits over the past year to money market funds that offer more compelling yields ( blue line ). However, “small” banks (all other banks) were holding their own and even increased deposits in late 2022 ( orange line ).

{kind=link}

That changed abruptly in mid-March when depositors withdrew some $250 billion from small banks. Some of that initially flowed to the perceived safety of the largest banks, but that proved temporary. Even the large banks sustained net deposit outflows of almost $150 billion in deposits in March, for a total drop of over $400 billion among all banks, including foreign-related institutions. Small net inflows in April so far have restored only a tenth of those losses.

This sudden loss of deposits – in the smaller banks especially – is further reducing the credit available for commercial real estate. Small- and medium-sized regional banks originate an outsized share of CRE lending. There’s been a lot of confusion and debate in real estate circles about just how significant that share is due to the Fed’s misleading definition of “small” bank (all but the largest 25 banks) and because banks account for less than half of all CRE loan originations, according to MSCI . Still, there is no doubt that regional banks account for a big chunk of CRE lending, so anything that limits their lending capacity is worrying. Mezzanine debt is picking up some of the slack but is more expensive and doesn’t work in many situations.

Terrible Timing for CRE Owners

One tough challenge for CRE owners is that a wave of investments must be refinanced in the next two years. The Mortgage Bankers Association (MBA) estimates that “of approximately $4.4 trillion of outstanding commercial and multifamily mortgages, $728 billion (16%) matures in 2023 with another $659 billion (15%) maturing in 2024.” A quarter of that is in the beleaguered office sector, where the move to remote working has sharply reduced both tenant and investor demand for all but the best product, as I explained in a previous article . And market conditions have weakened further since then, with vacancies continuing to rise while a record amount of space available for sublease portends yet further increases.

It’s not just offices. Market conditions are softening for the formerly high-flying multifamily sector, which enjoyed historically low vacancy rates and record rent growth during the pandemic. But rent growth peaked a year ago (in March 2022), and now Redfin reports that rents posted their first annual decline nationally in three years. That’s great news for renters and the economy overall: rent increases have accounted for a large share of consumer inflation over the last year, so the weaker rents will reduce inflation and perhaps ease Fed pressures to keep hiking interest rates.

But these rent trends pose problems for the landlords that bought a record number of multifamily units in recent years. These deals frequently assumed robust rent growth to justify their lofty transaction prices. Moreover, apartment construction (both started and completed) is near its highest levels in three decades. This new supply will put more pressure on rents.

And as with offices, the timing is bad for owners. The MBA reports that almost a tenth of all multifamily mortgages is maturing this year – the highest of any property sector – just as market fundamentals are slumping.

Further denting refinancing prospects is that property values are falling. Green Street estimates that public CRE values are down 15% since peaking in May 2022, led by 25% declines in office and 21% in apartments. Cap rates are rising as investors discount future NOI growth expectations. These lower values will therefore only support lower debt levels.

Rising Rates Slows Deal Flow

Finally, what credit is available is much more expensive than the loans that need to be refinanced. Higher interest rates are also killing deals as transactions now need lower prices to pencil for buyers. Owners had been content to ride out the market for a while rather than dropping prices, resulting in wide bid-ask spreads that are grinding deal flows to multiyear lows. But with loans maturing and leases expiring, owners cannot wait any longer. Little wonder that delinquencies are rising , and more owners are defaulting on their loans , while others are finally liquidating holdings through fire sales of distressed assets .

So far, this distress has been firmly focused on the office and multifamily sectors, though hospitality and retail had their share of pain earlier in the pandemic. But with CRE credit tightening across the board and values dropping across all property types, we can expect to see these issues broadening to more assets in more property sectors.

What to Expect

Investors should understand that conditions are likely to deteriorate further before they improve. This credit crunch is occurring as property fundamentals remain relatively strong overall thanks to an economy still growing moderately and operating near full employment. Even a mild downturn will magnify the financing challenges as vacancies rise and rents fall, providing less support for new debt. In short, the credit crunch is sure to deepen and extend value declines and losses in commercial real estate.

History won’t repeat itself, but it will rhyme: We should not expect to see the devastating losses of other recent recessions, but owners will nonetheless endure further pain. Of course, such losses will create opportunities for savvy investors. But investors must factor in healthy discounts for continued turmoil in property capital markets on top of declining property fundamentals. Caveat emptor.

For further details see:

The Credit Crunch That's Strangling Commercial Real Estate