SAFE - The Death Of Cognitive Decline

2023-12-19 11:55:29 ET

Summary

- My initial approach to long-term inflation and cognitive decline was to place a quarter of my funds in other hands.

- In the four years since, my portfolio has grown rather than depleting.

- In that context, it made more sense to use those separate funds to buy annuities.

For a few years before retiring in January 2020, I did a lot of reading and research on traditional, portfolio-based strategies for retirement income. These depend on investing for total return and expecting to draw down your portfolio at a slow enough rate to avoid exhausting it too early.

There are a lot of very smart people evaluating the details of such options. My view is that their assumptions are shaky. Even so, there are large number of workers and retirees for whom such a total-returns, Modern-Portfolio-Theory approach is the most sensible one.

One thing that was emphasized by some of these analysts was the challenge of the cognitive decline of the retiree, a not unlikely event. Unsurprisingly their solution was that you should give them your money to manage.

Pondering this aspect led me to write Define A Strategy For Your Own Cognitive Decline , just over 4 years ago. I chose to place my funds with the investing department at a local bank with whom I have had an extensive and long-term relationship.

That article remains relevant today. Key points included

- You face a significant risk of unknowingly losing your cognitive capabilities while maintaining your physical health.

- Your finances and intended legacy are at real risk as a result.

The comments on that article include some true horror stories, such as one about a father who canceled his long-term care insurance during early dementia, a year or so before it was desperately needed. It also was clear that some readers completely missed the point that many people lose their capabilities without realizing it.

In summary, I put 25% (at the time) of the funds I controlled into the hands of the bank. This funded a fairly traditional Modern Portfolio Theory portfolio with an emphasis on GARPy large caps. You can see more details in that prior article, if you like.

Overall, I have been pleased with the handling of me and my funds. I might go back to them again for similar purposes, and may do so as I look to detach myself from managing long-term income generation.

What I’ve been writing for four years is that “In the worst case, my self-invested portfolio needs to last about 20 years, after which the cognitive-decline portfolio can take over.” At a real gain of 3% per year would put its real value at 60% of the initial value of the self-invested portfolio. (And if you think 3% is unduly pessimistic, you have not read enough history.)

That outcome would leave me with funds to support spending into my late 90s. And since I don’t expect to actually live anywhere near that long, it seemed that my wife should have been OK too.

But since then circumstances changed.

These changes have led me to pull the funds out of the bank and use them to purchase several single-premium, joint annuities. Here I will share the reasons, the process, and how my other investing is affected.

What Changed

Four years ago, my thinking was colored by total-return theories and sequence of returns risk was my biggest worry. But instead of seeing my portfolio start to deplete in the interim, my investing has been successful and the portfolio has grown in value instead.

Using the value-investing approach we advocate, I have grown the market value by more than 40% even while withdrawing or encumbering an additional 14% for expenditures, charities, and taxes. Since September that value has been increasing rapidly and I expect this to continue for a while.

There are four other relevant facts beyond that. One is that current dividends substantially support all my spending, thanks to previous successes. The second is that there is little reason to expect outsized performance from the portfolio held by the bank. It is mostly subject to the same risks that endanger total return over the next decade.

The third relevant fact is that the new annuities are joint and so will pay my (younger) wife after I presumably die first. A lot of other current income is tied to my lifespan. The new annuities will greatly reduce her need to tap into the portfolio.

The final relevant fact comes from modeling the additional income from the annuities, which I am purchasing with a 2% COLA. That income markedly improves the long-term survivability of my funds by enabling more reinvestment. Here is a projection of portfolio value for a 5% nominal (not real) total return:

RP Drake

The flattening in the late 2020s reflects my presumed final cessation of all income-producing activity. Long-term, the model is quite artificial as by 2035 I would have outlived all previous adult males in my family.

Naturally if my past investing success continues for the next decade, it will push the totals quite a bit higher than are shown here and perhaps set the stage for long-term explosive compounding. But managing 5% nominal returns is often all one can do when times become difficult.

In this and other models, one sees a likelihood that substantial funds will be available for my children and charities at the end of the story.

There is still work to do to protect my dividend income from bad decisions during a potential cognitive decline. Perhaps I will follow the example of Retired Investor (can’t find the link) and enable my children to monitor and manage my Fidelity accounts.

I did make one other change, after discussing these issues with my estate attorney. I changed my Trusts so that all that is required to remove my own control of my assets is an opinion by my personal physician that I have lost competency. Forcing my very busy (and geographically distant) children to push through two independent neurological assessments just seems silly.

Finding the Annuities

My preferred site for researching annuities has long been immediateannuities.com . One big reason is that they do not hassle you. You can research various scenarios freely.

The contrast with some other providers is remarkable. Once you give one of them an email and phone number, in order to get their material, you face weeks or months of being pestered.

What is really ironic at the moment is that one large investment house is running huge number of adds telling you not to buy annuities but not why. Wanting to see their argument, I clicked on one of them. But to get their story, you have to give them contact information and I know from past experience with them where that leads.

My preference is for simple annuities, in which you pay an up-front, lump-sum premium in return for contractual payouts that are fully defined in advance. There are no ongoing commissions and you know exactly what you are getting.

The simplest annuity is a single life or joint life one. The way that works is this: for one or two people with specified attributes, a known premium generates a monthly payout throughout their life or lives.

Here is an example of the first page of results, refined by company and details for the next step. This is for an annuity based on a 69-year-old man that will start paying out in 5 years:

{kind=link}

If you analyzed the numbers on offer a month ago, they corresponded roughly to making payouts with a 5% discount rate that would end at age 90. Any deviation from a fixed payment would change the size of the initial payout, but always in ways roughly consistent with those numbers.

Examples:

- If one added a COLA, increasing the payout at some rate, the initial yield would be reduced by roughly the size of the COLA.

- If one added a return of funds to one’s heirs if one died too soon, the initial yield went down.

- There are other more complicated options again decreasing that yield.

- If one delayed the start of payouts, as in the example shown, the payments went up. The amount paid corresponded to roughly a 5% rate of return on the premium you paid.

So the next thing was to identify the annuities that best fit my needs. I wanted several suppliers all with high credit ratings, to diversify the (small) risk of default. That was easy to do with the information provided.

The Logistics Suck

Then I called immediateannuities.com. They were friendly and helpful throughout, but the process is not.

Unfortunately, annuities are offered by insurance companies, which remain stuck somewhere like 1950. So rather than having an e-form to fill out, I first had to provide extensive and detailed information to the agent by phone.

After that they sent me prefilled, printed applications needing only minimal information from me but some dozens of signatures per company. This aggravated some lingering tendonitis; writing by hand is rare for me. My wife escaped with only about a dozen signatures per company.

(I really do appreciate the prefilled forms, but it feels like appreciating a roadside stables in the 19th century that would not only house but also feed your horse. You still had the aches and pains of riding all day, instead of being able to drive.)

This started a process that locked the yields. Eventually a clock started such that the premiums had to be paid within 30 or 60 days to keep that rate.

What came up next, after I had sent the forms back to the agent, was word from my bank that the rollover forms had to be “signature guaranteed.” What was that?

Despite engaging in many real estate transactions and IRA rollovers, and sometimes needing a notary, I had never heard of what in full is called a “Medallion Signature Guarantee.” Think of it as the equivalent of a notarized signature but from someone who can understand the details of the transaction and accepts some financial risk in guaranteeing the signature.

A hidden challenge of dealing with a bank is that they are subject to FDIC regulations that brokerages and insurance companies are not. So while mere signatures (or notarized ones) suffice for the other players, the bank may have to impose more challenging requirements.

Dealing with this was an aggravating and time-consuming hassle, which likely would not apply to you. But if you are trying to pull funds from a bank, beware that the process may be complex and learn about it in advance.

The funds used to buy the annuities were in a Rollover IRA. The result will be that the payments are taxable but I will avoid RMDs (Required Minimum Distributions) on that money.

Portfolio Implications

Nearly all Americans have Social Security as fixed income. It comes with a COLA and political risks. Some of us have a pension of some sort. And some of us have annuities.

None of these are usually thought of in the same bag as investments, but for retirees they should be. In simple terms, the larger the fraction of your expenses that is already covered, the more you can accept volatility or fundamental risk in pursuit of larger investment gains.

My lifetime spreadsheets (for 3% inflation), including the income from these new annuities, show that my dividends would only need to grow at a CAGR of < 2% to support spending into my 90s. The point here is not any specific number but that the margin of safety has improved and is comfortable.

Perhaps more significantly, my wife will now be able to live the life she has now after my likely demise, without depleting the portfolio.

But returning to investments, my present target portfolio structure has 20% in an Upside Bucket and 80% in an Income Bucket. There is no need to change that at the moment.

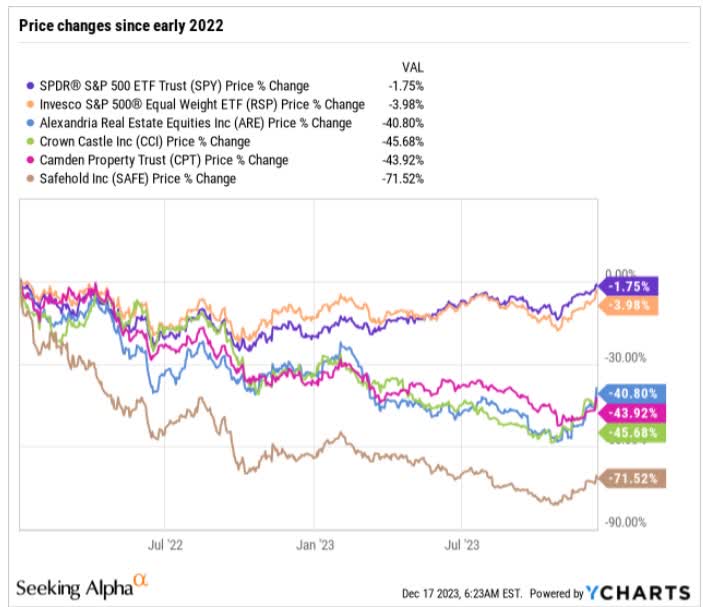

My Upside Bucket today includes no energy positions and only four REITs. These are Alexandria Real Estate ( ARE ), Camden Property Trust ( CPT ), Crown Castle ( CCI ), and Safehold ( SAFE ). It seems to me that those have plenty of room to run.

{kind=link}

Considering the uncertainty of how much interest rates will come down and what will happen to valuations, I haven’t seen a lot of other opportunities in REITs or energy.

In any event, opportunities will come, and with the oil price cratering at the moment, perhaps sooner rather than later. Following the changes described above, it would be sensible to push a larger fraction into the Upside Bucket in response to the next great opportunistic market.

For further details see:

The Death Of Cognitive Decline