KKR - The Diverging Ways Of Two Brookfields And How To Pick Your Way

Summary

- Brookfield Asset Management Ltd. is attractive due to the expected 15-20% annual growth in fee-related earnings, ample and growing dividends, and some remaining expansion in multiples.

- Brookfield Asset Management's growth is not expected to be smooth and investors should be prepared to buy on weaknesses.

- In the short term, Brookfield Corporation will be driven primarily by Brookfield Asset Management's appreciation and possible buybacks mentioned by the management.

- In the longer term, Brookfield Corporation's progress will be dependent on executing both its insurance and real estate strategies. Neither of them will be easy.

The title may seem bizarre. "The new" Brookfield Asset Management Ltd. ( BAM ) (spun off only two months ago) is the main building block and the biggest store of value for Brookfield Corporation ( BN ). Moreover, both can be even considered as different facets of the same company, run by the same people, preaching the same culture, and intermingled in many ways.

Still powerful centrifugal forces are already in place for the two stocks, and recent quarterly filings, earnings calls, and acquisition announcements have given us appetizing food for thought beyond routine updates.

The post assumes familiarity with the Brookfield conglomerate and alternative asset management industry. If you are not familiar with it please read "How Brookfield and Peers Make Money..." .

Brookfield Asset Management

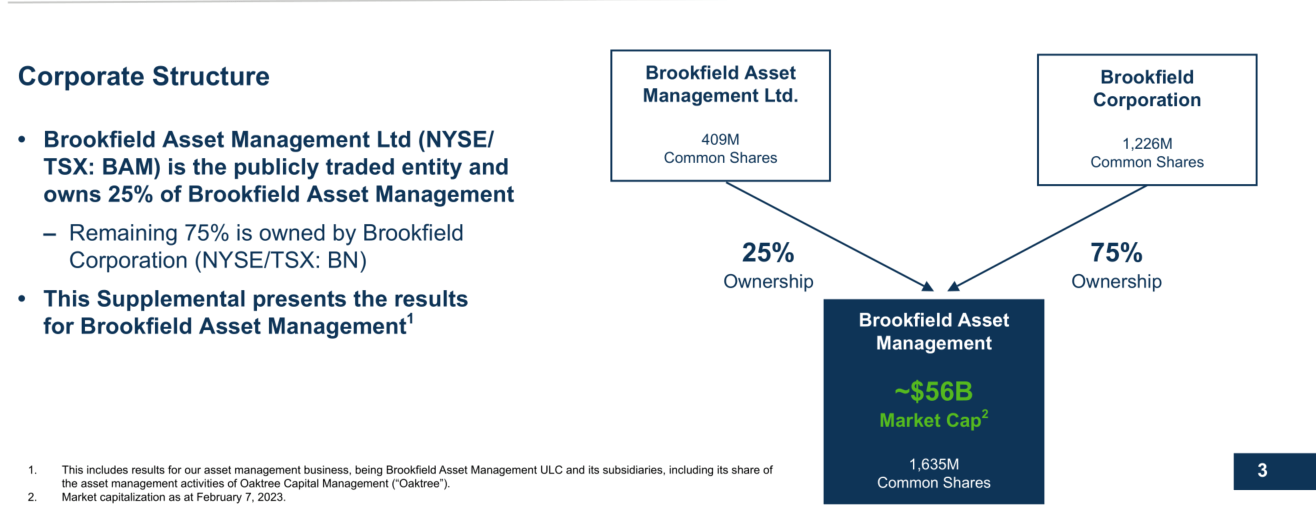

To avoid any confusion, I will reproduce a slide from BAM's supplemental filings that shows the current structure:

{kind=link}

The spin-off of asset-light BAM in December offered investors a delicious opportunity, and I posted several times about it (the publications are available on my author's page ).

It is tantalizingly easy to analyze the company. BAM promised to pay out in dividends ~90% of the preceding quarter's distributable earnings ("DE") which consist almost in full from fee-related earnings ("FRE"). For alt managers, DE is a measure of cash generation similar to cash flow from operations before changes in working capital. Since asset-light managers' capex is extremely low, DE is very close to free cash flow. Because of this tight connection between dividends, DE, and free cash flow, the dividend yield becomes the easiest-to-use metric.

Before the spin-off, BAM announced the Q1 dividend of $0.32 per share, and its Q4 DE was $0.35 - in line with its dividend policy. In this regard, the earnings release did not have any surprises but the stock responded positively nevertheless.

The yield is 3.6% now. The best (and perhaps, the only) comp is asset-light and management fee-centric Ares Capital ( ARES ) which is trading at a 3.7% yield after the very recent dividend increase of 26%. Before the increase, it was trading at ~2.9%. Please take a look at the ARES's variability of the dividend yield over the last several years since the current policy of year-to-year dividend changes was established:

Company, author

The table is supposed to give you a feeling of what may be in the offing for BAM - the ride is unlikely to be smooth. High yields in 2019 and 2020 did not last long (in 2020, it was related to the pandemic) and it was extremely beneficial to buy shares during these short spells. Most of the time ARES was trading at a 3-4% yield.

BAM has several advantages vs ARES. While ARES specializes in private credit, BAM is diversified across infrastructure, renewables/transition, real estate, and credit. Infrastructure and renewables are particularly promising since they enjoy secular tailwinds of decarbonization and infrastructure build-out.

BAM also relies on the support of asset-heavy BN which makes it unique among all asset-light alt managers. This can be easily illustrated by a recent development. BN has just announced a $1.1B acquisition of Argo Group ( ARGO ), a specialty P&C insurer. Being an insurer, ARGO has investments (about $5B) and at least a part of these investments will end up under BAM's management generating FRE. To achieve this growth, BAM will not spend a penny. Sales and marketing are not required either. Growth will be achieved without any effort due to BN's support!

But even this example is underestimating what is going on. One of the most promising lines of business for Brookfield is renewables. Today, consolidated Brookfield has enormous generating assets and a phenomenal development pipeline across the globe in multiple technologies. Many thousands of operating employees are working hard to make this line of business successful. Their efforts will benefit BAM but BAM will not pay a dime to these employees as all renewable assets are on BN's balance sheet. This inherent advantage of the BAM/BN structure is impossible to overestimate.

Due to the above, BAM may be trading at a lower yield than ARES eventually. But it is likely to happen only when BAM establishes a convincing record of growing dividends (differently from ARES, BAM seems to have a quarter-to-quarter dividend policy that should be also taken into account).

Summing up, I expect further albeit slow appreciation of BAM shares due to the gradual expansion of multiples (i.e., trading at a lower dividend yield) besides the growth of dividends. The latter is expected at 15-20% annually and is locked in for the next 2-3 years at least per Bruce Flatt.

In case of market turmoil, the shares can temporarily trade lower, and this will be the best outcome for investors as they can scoop more shares cheaply.

Brookfield Corporation

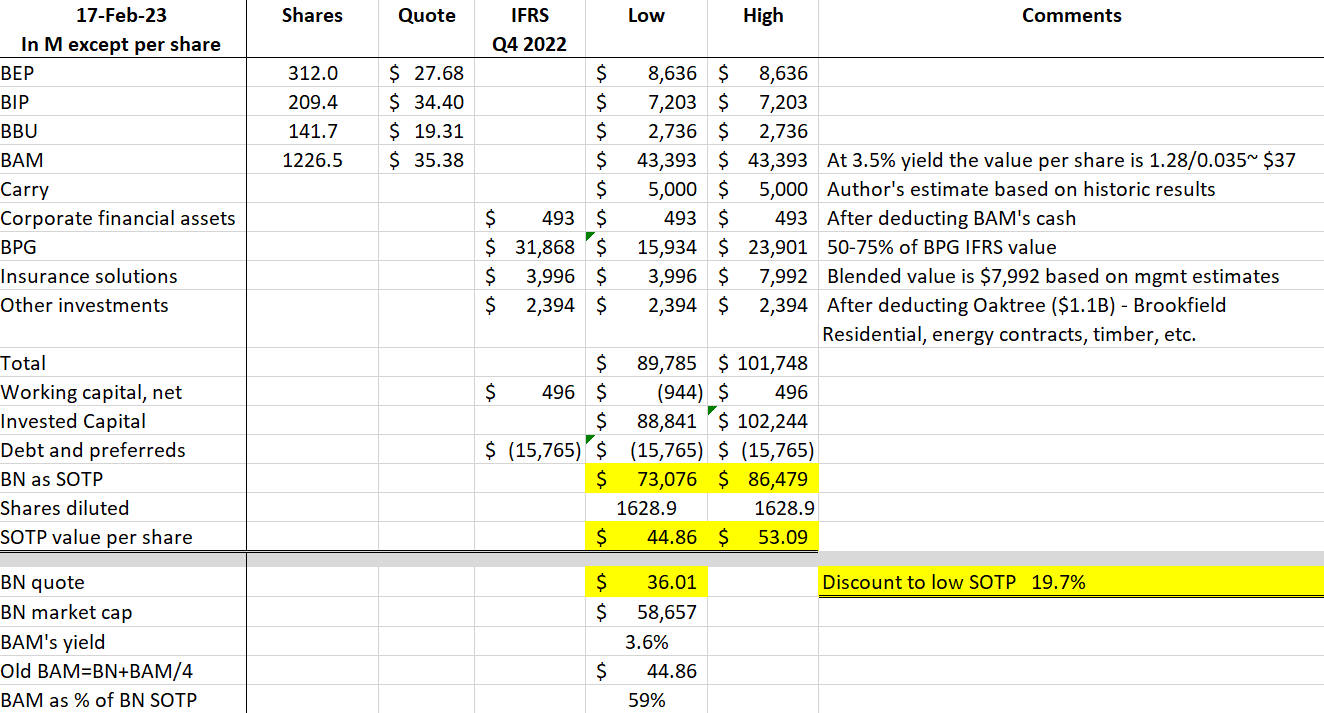

In contrast to BAM, BN made several conspicuous announcements. To appreciate their significance, we will present a table with BN's SOTP valuations. This is the best metric now, as BN has become a pure holding company with many pieces trading publicly. The data in the table are taken from BN's Q4 Supplemental filings on the company's site.

{kind=link}

There is plenty of info in this table. Since I presented a similar one in my previous publications, I will focus on major issues only.

BN keeps trading consistently at a significant discount to the low end of its SOTP value. Per my observations, this discount was never smaller than 15%. It may remain this way at least until we see a clear upside to either real estate or insurance which should take time. Meanwhile, BN's progress will be dependent almost exclusively on BAM's appreciations and possible buybacks or even a tender offer that Bruce Flatt talked about at the earnings call. So far, the market has not responded to this talk.

BN's market cap is close to $60B. Several billions of persistent buybacks extended over several quarters are likely to narrow or close the discount. But I am doubtful that any short-term burst of repurchase activity will have a long-lasting effect. BN's capital structure has flaws that should not be susceptible to quick treatments.

Here is a long quote about real estate from Mr. Flatt's quarterly letter:

- $8 billion of our capital is invested in our real estate private funds, which are highly diversified by both geography and by sector, and where our asset management business has a proven track record of delivering upwards of 20% returns over the long term. These assets are turned into cash in a 5 to 10-year period.• $15 billion of our capital is invested directly in our top 35 trophy office and retail complexes globally. These are amongst the best in the world and get better and better over time.• $3 billion of our capital is invested in our residential land development business in the U.S. and Canada. This business has delivered very strong financial results for decades. Over time, these assets all turn into cash as we build out developments (unless we choose to reinvest it).• $7 billion of our capital is invested in other real estate assets which, as we have discussed before, will be liquidated over time.

To extract $7B of capital from leveraged real estate assets which are not in high demand (non-prime malls and office buildings) will take time in the BEST POSSIBLE SCENARIO. Since the assets are leveraged, some capital might be lost in these transactions. We, as investors, do not have a clue about what is going on within this part of the portfolio. For example, several days ago Brookfield defaulted on two LA office towers. Is it good or bad or does not matter? Nobody but Brookfield knows. Watching Brookfield rather closely, I have not noticed particular transparency on an asset-to-asset basis. Certainly, BN investors can hope for the best knowing Mr. Flatt's magic touch. But I'd rather prefer knowledge over hope.

Let us assume that $15B of capital in the top 35 trophy assets is doing well as Mr. Flatt indicated. At the very end of BN's earnings call (for some reason its transcript is not available), it was mentioned that ALL these assets will be transferred gradually to Brookfield Reinsurance ( BNRE ) (if you check BNRE's filings, half a billion of real estate is already there). It reveals the scale of BN's insurance ambitions. $15B of capital implies, say, $25B in trophy assets taking leverage into account. It means that total insurance assets will be at least $250B. The current number is lower than $50B. How to get from $50B to $250B? Brookfield has already indicated the path.

(The following discussion assumes that the readers are familiar with alt managers' insurance strategies. If not "Why Brookfield And Peers Followed Apollo Into Insurance..." will be helpful.)

The already-mentioned acquisition of ARGO has clarified BN's intentions. Differently from the well-established strategy of Apollo ( APO ), BN is going to grow both the life/retirement and P&C businesses. Some of this growth will be organic but it is insufficient to close the $200B gap. BN is planning big acquisitions in insurance including P&C.

Since P&C is a part of the solution, a simple question is timely: does Brookfield have any edge in underwriting? Neither American National (that has P&C lines) nor Argo is famous for extraordinary combined ratios (I suggest you search for "combined ratio" in BNRE filings - you will not find it even after the American National acquisition). It took many painful years for Buffett to achieve this superior underwriting and Brookfield should not be different.

Here is the next question: can Brookfield use its investment skills for outperformance in short-term and liquid fixed income? (that is how most of the P&C float should be invested). Maybe. However, Brookfield's references to proprietary liquid strategies without detailed explanations and/or presenting the results of these strategies have not convinced me. (Please note that achieving outperformance in short-term fixed income is more difficult than in long-term fixed income.) Brookfield Reinsurance is currently riding the rising rates environment and is expected to have strong investment income in 2023 but it is only a one-off.

And finally: ARGO's assets-to-equity ratio is about 5:1. Apollo's Athene assets-to-equity ratio is about 11:1. From the FRE standpoint, it is preferable to have it as high as possible. Again, the P&C strategy seems inferior to the life/retirement strategy of Apollo.

So why did BN decide to pursue P&C business? Perhaps, it is too difficult to gather $250B in insurance assets without P&C today. Apollo, KKR ( KKR ), and others have already grabbed inexpensive retirement assets (this reason was originally suggested in private discussions by the author of Red Deer Investments ).

It took more than 13 years for Apollo to reach the same scale of $250B in insurance assets. If BN achieves this scale quicker (which seems to be the intention), the quality of these assets and related insurance liabilities may not be the same. Possible buybacks at scale will slow down the growth in insurance.

Conclusion

My readers may have already guessed the meaning of the title. Brookfield Asset Management Ltd. stock appears very transparent and easy to understand. Nothing should be taken for granted in investments, but BAM's growth seems very likely and its dividend is appealing.

On the contrary, Brookfield Corporation's position is far from clear. I have great respect for Brookfield's management and hope they will overcome the issues. But as I already mentioned, knowledge is better than hope.

And the final, unrelated comment for my readers. I am publishing 1-2 articles a month and do not intend to change it. Occasionally I see a clear actionable opportunity that I would like to quickly share with followers without writing a full article (the last time was several days ago, when Apollo went down 7% after the Q4 earnings release). Since I am not on any social platform except for Seeking Alpha, I may post these ideas at the top of the comments section on my own articles. Please keep it in mind and follow in real time if interested.

For further details see:

The Diverging Ways Of Two Brookfields And How To Pick Your Way