FLNG - The Dividend Investor's Natural Gas Export Playbook - Part 4

2023-11-03 08:30:00 ET

Summary

- US natural gas exports are expected to increase from 14 BCF/d to over 26.5 BCF/day by 2030, alongside similar projects in Qatar and Australia.

- Natural Gas carriers FLEX LNG and Cool Company offer high cash flows and dividends thanks to rising shipping rates.

- The LNG shipping market will dramatically expand over the next three years as 270 new vessels and multiple export terminals enter service during that time.

Thesis

Over the next 5 years, a multitude of natural gas export terminals are scheduled to commence operations. This will expand exported US volumes of liquified natural gas ((LNG)) from roughly 14 BCF/d to over 26.5 BCF/day by 2030. This growth in US markets will occur in tandem with similar projects in Qatar and Australia. Regardless of the source country, all of these molecules need to hit the open waters.

{kind=link}

Part 4 of this series will be centered on companies that operate LNG vessels. I will examine the delicate balance between additional LNG production and LNG shipping capacity to make a sound investment decision that will span multiple years.

LNG Carrier Business Model

The LNG carrier business is fairly basic. Vessels are contracted either to long-term charters or in the spot market. Long-term charters offer the benefits of continuous employment but can be at lower rates than what is offered in the spot market. The converse is also true, being locked into a long-term contract also protects from dropping spot prices that the shipping industry has seen countless times due to a glut of new vessels.

In the LNG market, very specialized and expensive ships are required to keep the natural gas in a liquid state for efficient transportation. Given the need for natural gas in both heating and electricity generation, the demand for natural gas is robust enough to warrant a long term commitment from consumers.

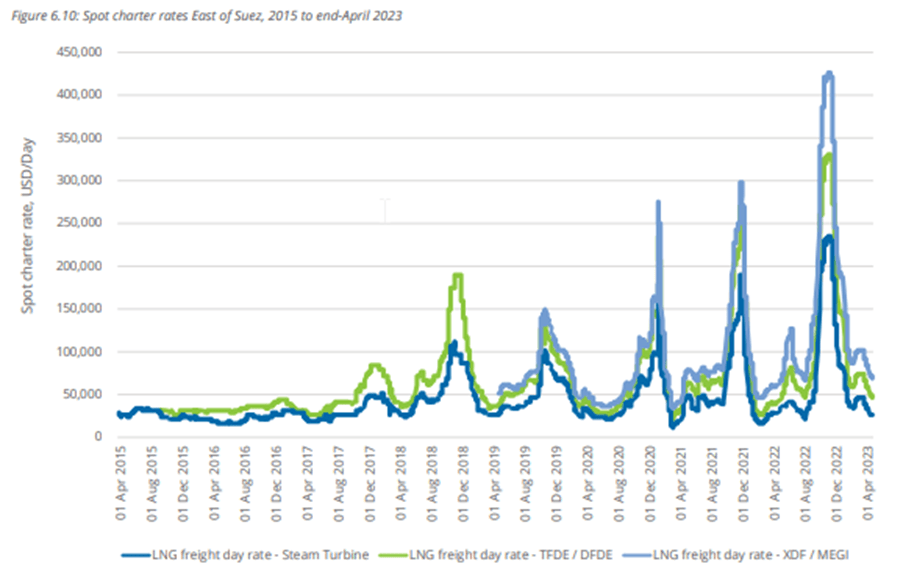

Thanks to the Russian-Ukraine conflict, the market dynamics have shifted. Europe is now required to import its natural gas from the United States and Qatar following the closure of Russian pipelines. This has propelled LNG time charter rates higher, often in excess of $100,000/day. All the while, developing nations like China and India increase their consumption of natural gas as their societies modernize and populations grow.

Modern vessels have operational lives that are expected to exceed 25 years. The newest vessels are highly efficient, making their operating costs fairly low and are able to fetch premium rates. Oftentimes, servicing the debt to construct the vessel is a larger cost than actually operating it. The combination of healthy margins and long-term shipping rates has allowed shippers to generate high levels of free cash flow and in turn, juicy dividends.

Supply and Demand Dynamics

As it stands today, shipping capacity is tight. Spot charter rates continue to skyrocket in the winter months as natural gas demand surges for heating. Further, baseload demand for natural gas is expected to grow as the phase-out of coal in electricity generation progresses.

{kind=link}

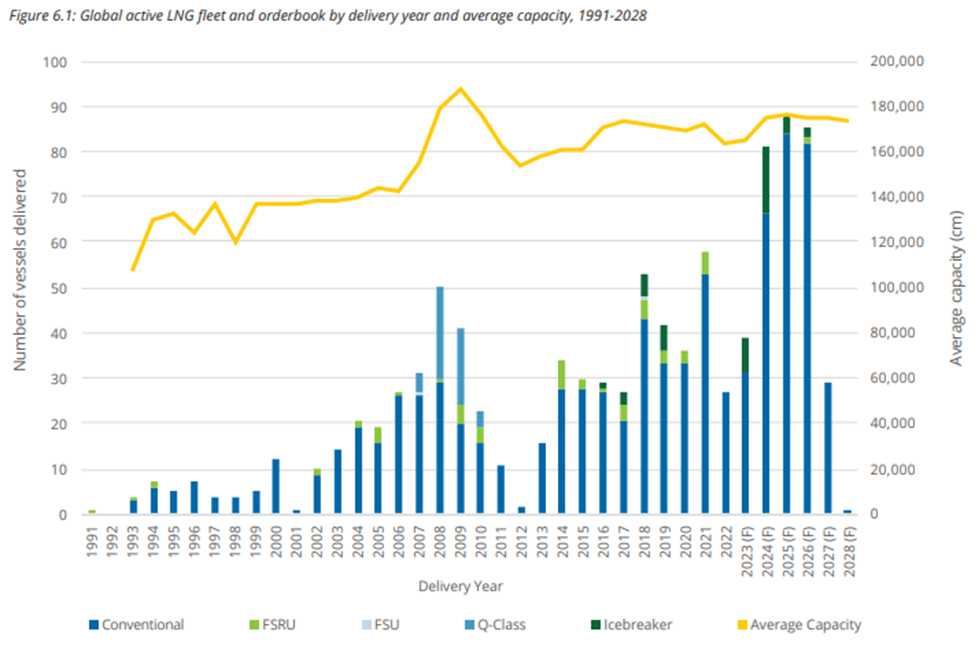

Growing demand has created record-high prices, which in turn has incentivized more shipping capacity to be built. It is expected that 270 additional vessels will enter the market between 2024 and 2027. Will this flood of new vessels cause the charter rates to plummet due to an oversupplied condition? Or will all of these vessels find active employment as a result of numerous global LNG export projects coming online?

{kind=link}

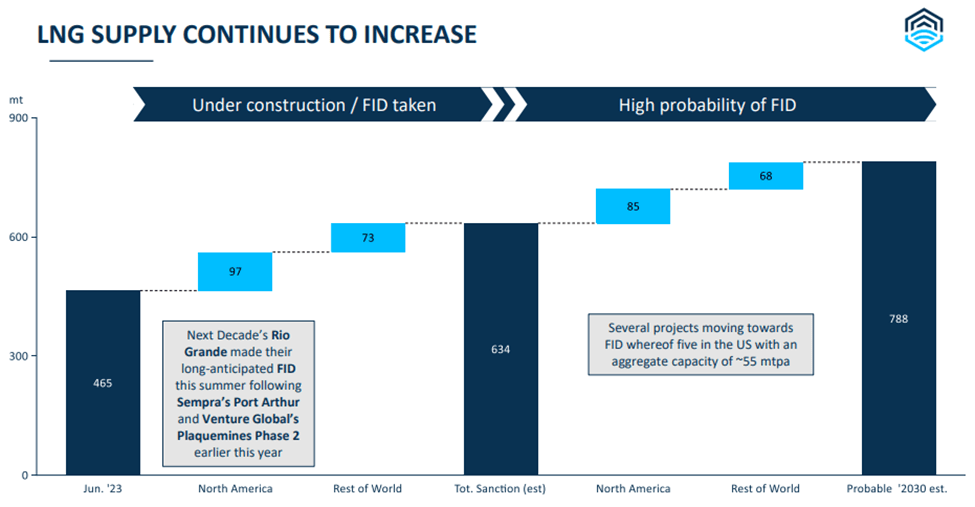

As of April 2023, there are 668 active LNG vessels in the world. The current slate of newbuilds projects stands to increase the available vessel supply by approximately 46%. We must see a reciprocal increase in export capacity to ensure charter rates remain stable. If we consider only those projects that are currently under construction or have reached FID, LNG export volumes will increase by approximately 36%. If all projects were to reach operation, the total LNG market would be seen to expand by 70%.

{kind=link}

It's fair to assume that the 70% figure is probably unrealistic but it gives a significant amount of margin to accommodate the 46% increase in shipping volumes needed to sustain shipping rates. However, the sheer number of vessels entering service in 2024, 2025, and 2026 still holds the potential to shock time charter rates as markets adjust.

{kind=link}

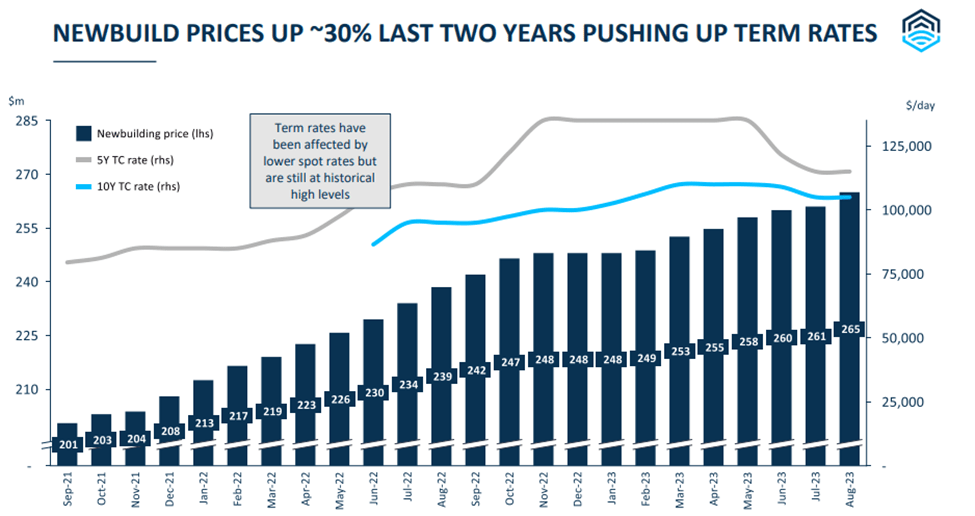

Fortunately, life has a unique way of always achieving balance. Any hot product will be sure to see its fair share of price escalation and LNG vessel construction is no exception. Shipyard prices for new builds have escalated drastically, increasing 30% in the last two years. This increase in cost is forcing up long-term rates to ensure vessel owners are able to achieve their desired rate of return. Many of these newbuilds are only able to achieve financing if these vessels are signed into long-term contracts prior to ever leaving the shipyard.

Ultimately, I see some risk in having an oversupplied shipping market in the next 3 to 4 years. This is largely based on the fact that there remains a large regulatory risk to getting any LNG export terminal approved. Building a vessel has no such regulator hurdle to compare to. Should several projects stumble on regulatory roadblocks, the necessary LNG may not develop to keep all vessels actively employed.

Now that we have examined the market dynamics, let's take a look at my picks for top performers in the shipping industry.

1. FLEX LNG Ltd. (FLNG)

FLEX is the name brand in LNG shipping. It has a fleet of 13 young vessels with the oldest vintage built in 2018. 12 of these vessels are contracted out under long-term contracts to provide predictable levels of cash flow. The average contract value is $77,218/day in Q2 against an operating cost of $17,293/day.

This high margin allows FLNG to send nearly almost all of its excess cash to shareholders. FLNG currently supports a 10% yield that should grab the attention of any dividend-seeking investor.

Free Cash Flow Analysis

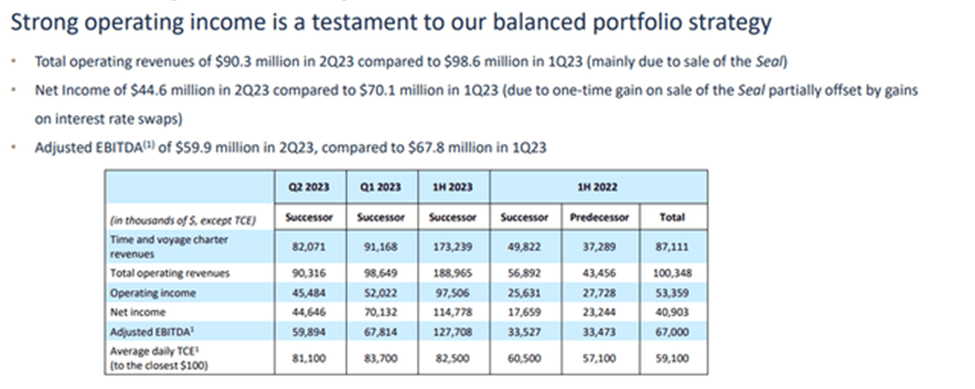

For the first 6 months of 2023, FLNG was able to produce roughly $180 million in revenue and produced $74.6 million in net cash from operations. This figure includes four drydocks at a cost of approximately $5 million each and debt repayment of $10.2 million.

During this time, FLNG paid out $94 million in dividends which exceeded the cash generated due to a large $1.00 dividend declared for Q4 of 2022. Since then, a dividend of $0.75/share has been declared for the first three quarters of this year. To adjust for the impacts of the timing of the actual dividend payment, I have adjusted the cash outflow to investors to be only $80.5 million for the first half of this year.

With no additional drydocks scheduled for the remainder of the year, the $20 million expense can be considered not to be reoccurring for 2H2023. Therefore, excess cash available by year-end should be around $15 million. This number can also fluctuate based on the performance of the spot market. Rising winter rates will boost the financial performance of the FLEX Artemis vessel.

Cash flows in 2024 should be slightly improved from 2023. The main drivers will be the number of drydocks and any changes in interest rates. Only two vessels will be required to visit the drydocks in 2024. This should reduce costs by another $10 million.

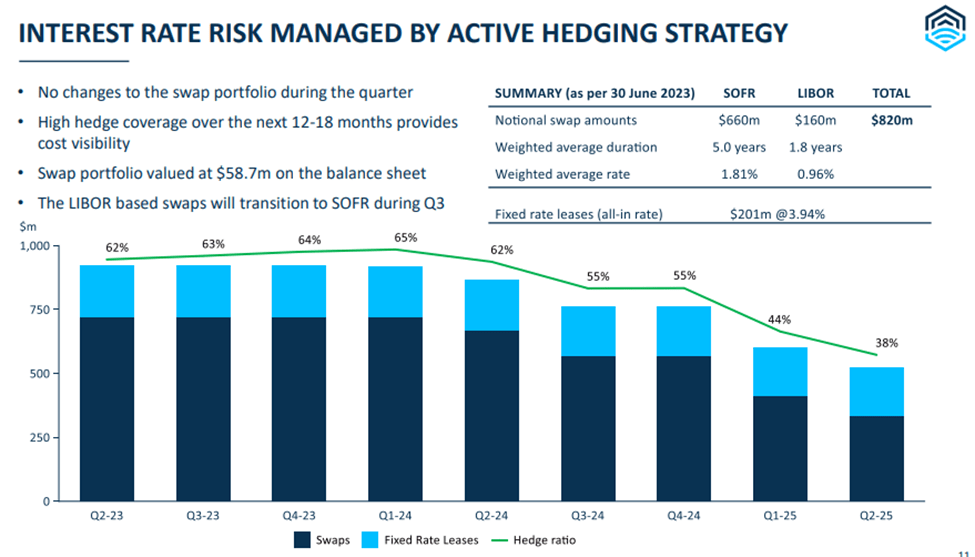

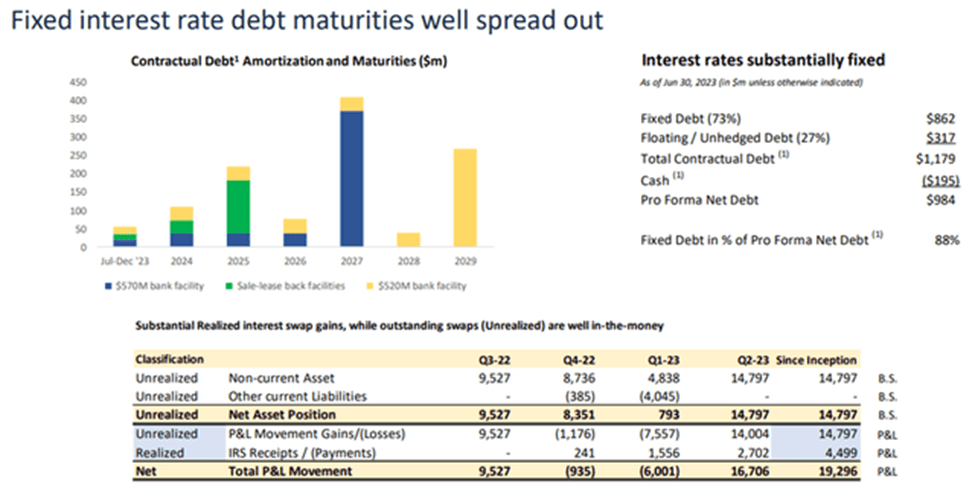

FLNG should be able to minimize the potential impact of interest rates rising higher with nearly 62% of its debt hedged. Therefore, I am fairly confident that the current payout ratio is sustainable. However, with most cash being allocated to dividends, any balance sheet maintenance will be difficult. With only $15 million in excess cash a year, the next debt maturity in 2028 ($353 million) may create a cash flow challenge.

{kind=link}

With a dividend yield of nearly 10%, it's safe to assume that most investors in FLNG are in it for the dividend. Cutting it to repay debt would not go over well and would certainly incur the wrath of many shareholders. So, is there any way to improve the balance sheet over the long term without cutting the dividend?

Unfortunately, FLNG's contracts do not include any inflation escalators to help increase revenues. Thus, FLNG has two choices to build cashflows between now and 2028.

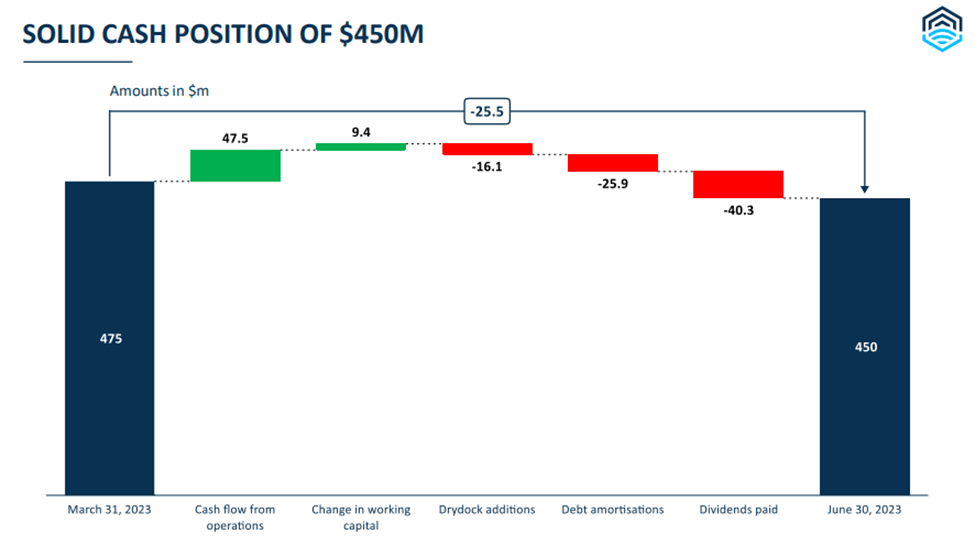

1. Leverage its cash balance of $450 million to pare down some of the debt load.

2. Assume that interest rates will not stay this high forever. If FLNG is disciplined, it can whittle away at the principal with small amounts of FCF until the loan comes due. At this time it can be refinanced out into the future to preserve its cash flow stream.

Option 2 is the more likely option. Long-term shareholders should be looking for FLNG to reduce debt opportunistically should spot market prices spike and/or interest rates fall. Both of these options can generate incremental FCF to be deployed to improve the balance sheet.

{kind=link}

FLNG Wrap Up

FLNG certainly falls into the steady and boring investment category, but that is okay. With a yield of 10%, it's hard to find much wrong with FLNG. With no debt maturities until 2028 there appears to be a fairly clear runway to maintain the current dividend for several years. I believe monitoring management's use of any discretionary cash is important here. FLNG has four-plus years to whittle away at the debt balances to slowly improve its overall health and profitability.

Despite this, I see limited opportunity for share price appreciation. The lack of inflation adjustments means what you're getting this year with FLNG is locked in with the exception of one vessel. Therefore, the opportunity for revenue growth is very limited. Share appreciation will be tied to the company's ability to grow the dividend over the long term.

Any opportunity to buy FLNG shares under $30/share provides a reasonable return for yield-seeking investors who are prepared for long-term positions.

2. Cool Company Ltd. ( CLCO )

Yes, despite the corny name, CLCO is an actual company with a market cap of $700 million. CLCO is a relatively new company to the NYSE, with 2023 being the first year being listed on the exchange. It is co-listed on the NYSE and Norwegian Oslo index. While I'm not necessarily a fan of the company's cheesy name, its assets are much more desirable. CLCO has a fleet of 11 VLGC vessels with two additional vessels on track for delivery in 3Q and 4Q 2024. The average age of the fleet is about 7 years, so slightly older than FLNG.

Currently, 10 of the 11 vessels in the fleet are operating under medium-term charters. The average rate for the fleet is $82,500 per day which is well above the operating costs of $18,785 per day. CLCO is profiting about $4,000 more per day per vessel than FLNG. To see how this translates to the bottom line, let's take a look under the hood.

Free Cash Flow Analysis

In the first six months of 2023, CLCO was able to generate revenue and net cash from operations of $173.2 million and $117.6 million, respectively. CLCO distributed $43.5 million in dividends, leaving significant levels of distributable cash flow remaining. The current rate of distribution supports a yield of 12.2% which is meaningfully larger than the yield supported by FLNG.

CLCO is budgeted to spend $40 million in drydocking expenses this year, of which $25 million will be spent in the second half of the year. While this will be an increase in expenses, there is adequate margin to absorb this overall cost without impacting the dividend.

{kind=link}

As with FLNG, one of the biggest risks to the dividend payment is the debt maturity profile. CLCO has large maturities due in 2025 and again in 2027. These have the potential to strain the balance sheet if not managed properly. CLCO has made meaningful efforts thus far to reduce the debt load of the company, having retired $144 million in debt during the first half of 2023. With fairly low levels of debt payments required over the next 12-18 months, CLCO should have a solid opportunity to get ahead on its debt payments to prevent a credit crunch.

{kind=link}

One notable difference between CLCO and FLNG is the duration of its time charter contracts. CLCO carries significantly shorter-term charters. 2024 contracts are nearly full but as the books begin to open up some in 2025 and are only 60% full in 2026. At a minimum, this will guarantee some volatility in earnings potential as contract rates shift. The delicate balance between shipping capacity and export capacity will be an important factor to monitor.

{kind=link}

As mentioned earlier, there remains a fair amount of cash margin to sustain the dividend at its current levels. That being said, CLCO does provide itself with some flexibility by considering the dividend program variable. Therefore, the cash return aspects of an investment in CLCO have serious potential for expansion but would certainly not classify as a "set it and forget it" style investment.

CLCO Wrap Up

Cool Company may have an awkward name but certainly has the cash flow aspects to back it up. CLCO is slightly more profitable with less debt than compared to FLNG. However, the contract structure and debt maturities will certainly introduce volatility in the bottom line. Investors stand to reap higher levels of cash returns through the variable dividend program because of these factors but market conditions will need to be closely monitored starting in 2025 when the contract backlog starts to open up.

CLCO can also expect revenue growth from the two additional vessels that will enter service in 2024.

Summary

Both FLEX LNG and Cool Company are cash-producing machines. Neither company is shy about returning that to shareholders but also conduct themselves in opposite ways. FLNG implements very long-term contracts to provide a highly visible road of revenue and dividends. Conversely, CLCO is more profitable with a higher yield of over 2%. The downside is that the dividend program is variable and based on shorter contract durations. The CLCO fleet is also slightly older than FLNG's but will be partially refreshed with two new vessels.

The LNG shipping industry will undergo significant change over the next several years which may lead to some turbulence for CLCO if the market ends up with excess shipping capacity. FLNG is the safe and steady approach to LNG transportation, while CLCO has larger potential but will be more volatile.

As a reminder, Part 5 of my series is designated for honorable mentions. This will be based on reader's suggestions in the comment section. Suggestions for analysis on natural gas producers, midstream, export terminals, and shipping companies will all be given serious consideration. Thanks for reading, I hope you enjoyed the series thus far.

For further details see:

The Dividend Investor's Natural Gas Export Playbook - Part 4