CHK - The Dividend Investor's Natural Gas Export Playbook - Part 1

2023-09-22 03:03:05 ET

Summary

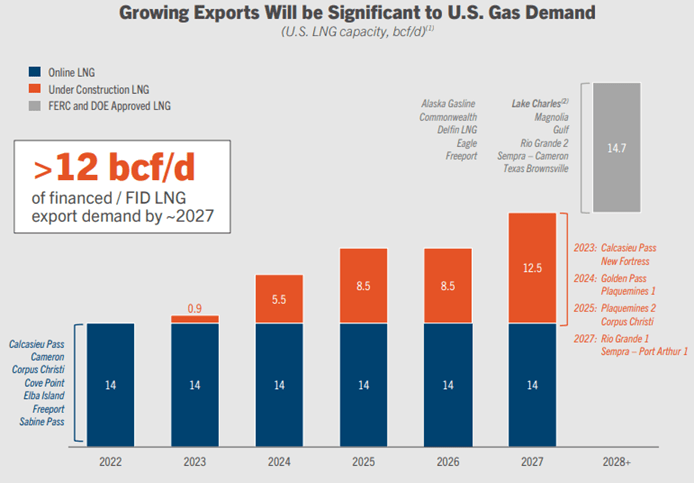

- Multiple natural gas export terminals are set to begin operations, increasing LNG exports from 14 BCF/d to over 26.5 BCF/day by 2030.

- Projects such as Golden Pass, Plaquemines, and Corpus Christi will come online in the next few years, adding 5 BCF/d of capacity.

- Investors can benefit from investing in producers, midstream companies, export terminals, and maritime transportation companies in the natural gas value chain.

- Part 1 of my natural gas playbook will explore my top picks for natural gas producers.

Thesis

Over the next 5 years, a multitude of natural gas export terminals are scheduled to commence operations. This will expand exported volumes of liquified natural gas ((LNG)) from roughly 14 BCF/d to over 26.5 BCF/day by 2030. The first projects (shown below)are slated to come online one year from now and will culminate in the first wave of an additional 5 BCF/d in 2024 and a total of 8.5 BCF/d by 2025.

- Golden Pass Trains 1-3 - Capacity of 2.6 BCF/d, in service 2H 2024

- Plaquemines Phase 1 & 2 - Capacity of 3.4 BCF/d in service 2H 2024

- Corpus Christi Phase 3 - Capacity of 1.6 BCF/d in service 2H 2025

A secondary round of projects that have reached FID will also serve to ensure these are not just one-off events. These supplementary projects will progress demand growth out to the 2027-2028 horizon.

- Port Arthur Trains 1 &2 - Capacity of 1.9 BCF, in service 2027

- Rio Grande - Capacity of 3.6 BCF, in service 2027

LNG Export Projects (CHK Investor Presentations)

{kind=link}

As investors, this is an important market dynamic that can be captured for monetary gain. This can be done in several ways, but also needs to be identified BEFORE the molecules start flowing. In that vein I decided to start a new series to explore how investors can benefit from a variety of investments at different points in the natural gas value chain.

Turning Molecules into Cash

This series will explore and compare both the income and growth aspects of what I consider the top two candidates in several sectors. This series will be broken into at least four segments with a possible fifth reserved for honorable mentions based on reader feedback in the comment sections.

- Producers - includes drillers and royalty companies who own and or produce the molecules (Part 1)

- Midstream - includes companies that transport and process the raw gas stream and separate it into its various components. These include methane (natural gas), propane, butanes, ethane, etc. (Part 2)

- Export Terminals - includes companies that own the infrastructure that receives the process gas stream, cools, and compresses it to liquid form to load cargoes. These cargoes are loaded onto specially designed vessel for international transport, mainly headed for Asia and Europe. (Part 3)

- Maritime Transportation - includes companies that own and operate the vessels to deliver the finished product to the end user. (Part 4)

- Honorable Mention - diamonds in the ruff provided by reader feedback. These can be companies in any of the other four categories or something outside the box.

Ultimately a diversified portfolio of these companies will allow investors to capitalize on all aspects of the value chain without relying on a single company to outperform the market. Identifying these companies early and developing some sense of value will improve our odds of success while also allowing the opportunity to maximize both income and appreciation over the long term.

Let's get started with the first part of this series with my top two picks for natural gas producers.

LNG Producers

Our first group will experience the highest degree of volatility. These stocks often trade following crude prices. In many respects this is illogical and can be frustrating to the common shareholder. We however need to be trained to identify when this illogical behavior is occurring and how to exploit it. Buying into weakness both decreases our risk but boosts yield and capital gain potential.

1. Chesapeake Energy Corporation

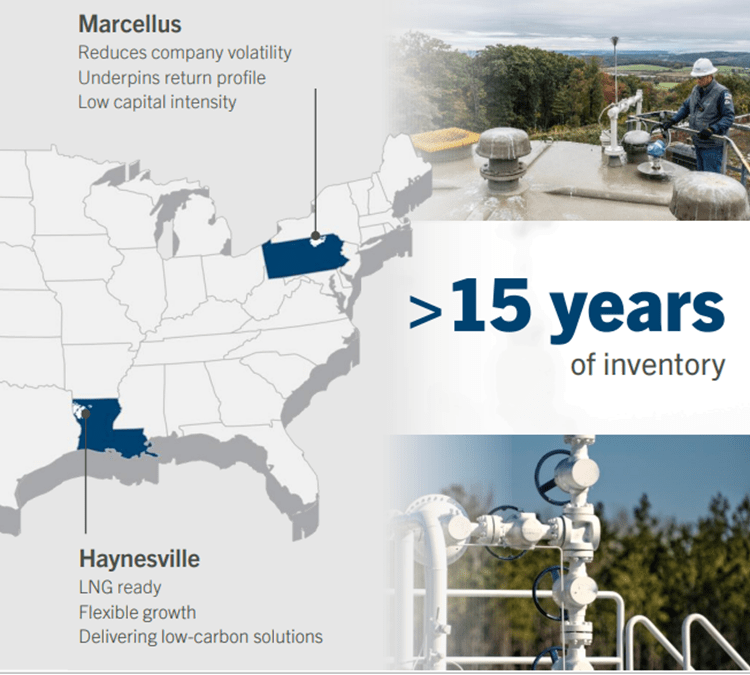

Chesapeake ( CHK ) operates out of two major natural gas basins, the Marcellus and Haynesville basins. The production is split between the two basins with 45% of the production coming from the Haynesville and 55% from the Marcellus.

CHK's Marcellus and Haynesville Operations (CHK Investor Presentations)

{kind=link}

This split provides valuable market diversification. The Marcellus is well positioned with excellent economics and located ideally to service the bulk of the US Northeast where a significant portion of the US population resides for consumption associated with heating and electricity production. Western Europe is also a potential sales point to help replace the supplies that are no longer available from Russia via the Cove Point export terminal in Maryland.

Meanwhile, CHK's Haynesville acreage provides some counterbalance to the steady profile of the Marcellus. CHK is operating under the model of being "LNG Ready", which indicates the purposeful and tactical investment to capitalize on the upcoming expansion of LNG exports. CHK is emphasizing prudent capital investment in this shale to flex its muscles only when demand signals are created by these export terminals becoming operational.

LNG Ready

CHK's Haynesville acreage is ideally located near the US gulf coast that is being slowly cultivated to ensure it is ready to capitalize on the robust demand that will unfold over the next 5 years and beyond. CHK has guided for reduced rig counts for the duration of 2023 to allow the Haynesville to operate at or below maintenance levels of activity.

In the meantime, the company is working on optimizing its asset. CHK is trading acreage to allow for longer drilling laterals, building out midstream assets, and arranging long term contracts with customers. Specifically, CHK has contracted with Gunvor, a commodity trading company, to allow exposure to the Japan Korea Marker for natural gas, which historically trades at prices significantly higher than US markets.

Additionally, CHK has agreed to be a 35% equity partner with Momentum Sustainable Ventures for the construction and operation of a 1.7 BCF/d natural gas pipeline to deliver its product from the Haynesville shale to the gulf coast. This pipeline schedule to complete at the end of 2024 and is expandable up to 2.2 BCF/d. Having an ownership stake in the pipeline will ensure the CHK has offtake capabilities, as well as a cost-effective delivery system.

Using Cash for Both Offense and Defense

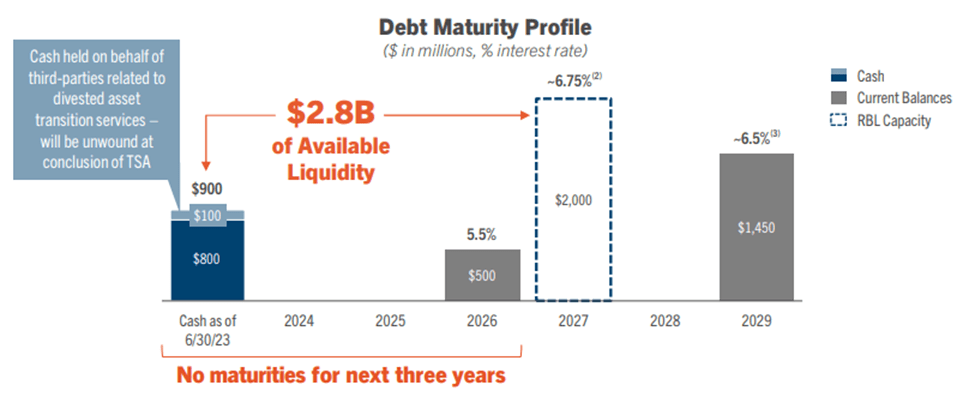

Everyone is familiar with the phrase, "It takes money, to make money". Any producer that is going ramp up production will need to invest heavily in drilling wells and building the associated infrastructure. This obviously can be a short-term stressor to the balance sheet of any company. Having a robust balance sheet will allow CHK to have a shock absorber to weather the current depressed natural gas market.

With a $2.0 billion credit revolver, and nearly $900 million in cash, CHK is also equipped to be able to invest when called upon. When the market needs more gas, it will be able to answer that call. Additionally, with no debt maturities in 2023, 2024, or 2025, there is nothing to rob the company of its momentum as it heads into this potential market upswing.

CHK debt profile (CHK Investor Presentations)

{kind=link}

Shareholder Returns

CHK has employed the variable shareholder return model that is becoming increasingly popular in the E&P space. This model utilizes a base dividend plus a variable component. This variable component alternates between variable dividend or share repurchases depending on the point in the operating cycle.

When the share price is elevated due to high commodity prices (think mid to late 2022), shareholders will receive 50% of the remaining free cash flow as an additional dividend. In periods of depressed share prices, the company will divert the excess FCF toward share repurchases.

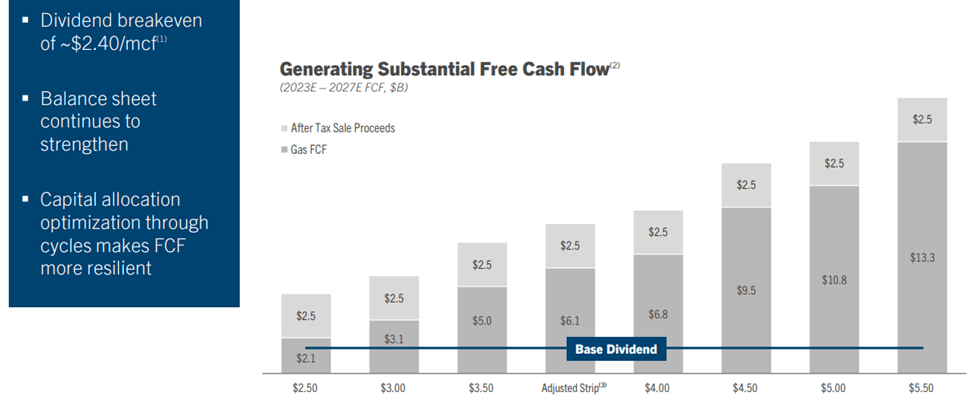

The base dividend is competitive with the general market, coming in at $2.30/share annually or 2.7%, with the potential to become significantly higher if natural gas prices rebound. Currently, CHK projects a $2.40/MCF breakeven price to sustain the base dividend, which the current market supports.

CHK Free Cash Flow Model (CHK Investor Presentations Q4 2022)

{kind=link}

In contrast, CHK returned $9.5875 in dividends during 2022 while experiencing record natural gas prices. This creates somewhat of a boom/bust dynamic that must be fully understood prior to initiating a position with CHK. It also stresses the importance of getting in early at the bottom of the cycle.

The exponential factor of the above chart should not be underestimated. Using the projected long term adjusted strip of nearly $4.00/MCF, you can see that a 60% increase from today's prices ($2.50/MCF to $4.00/MCF) will yield roughly 325% increase in FCF to $6.8 billion. This level of FCF generation is supportive of significant growth in the dividend through the variable dividend.

Valuation

It is also important to note that even before the Russian-Ukrainian conflict, natural gas prices averaged roughly $4.00/mcf in 2021. Given the projected increase in demand, the $4.00/mcf mark looks to be a realistic number long term. Comparable performance for CHK would be the second quarter of 2022 , where the realized price was limited to $4.03/MCF. The table below shows proof of the exponential factor I discussed earlier. Even a moderate rise to $4.00 has a dramatic impact.

| Income From Operations |

| Dividend Payment |

| Earnings Per Share |

| Q2 2023 ($2.36/MCF) |

| $517 million |

| $0.575/share |

| $2.73/share |

| Q2 2022 ($4.03/MCF) |

| $1,341 million |

| $2.32/share |

| $8.27/share |

By comparison, most of the independent oil producers such as Devon Energy, Diamondback Energy, or Pioneer Natural Resources trade on a rough multiple of about 8 times earnings. To account for the volatility that natural gas will experience, I would base an investment on obtaining a long term average quarterly EPS of $4.50/share, and an earnings multiple of 6. This conservatively implies a price of $108/share and therefore, I believe CHK is significantly undervalued at current prices.

2. Black Stone Minerals L.P.

Black Stone ( BSM ) is a slightly different take on the producer space. First off, it is not a producer at all, but a royalty company. Secondly, nearly 58% of its revenue comes from the sales of crude oil, not natural gas. However, BSM is making a dedicated effort to make sure its natural gas resources carry their own weight. In the image below you can see that the Haynesville shale makes up a significant portion of its total acreage, and thus carries significant potential.

It is important to note that as a royalty partnership, the company has little to no capital expenses to foster growth. It needs to structure deals with producers in a way that is mutually beneficial to drill on their land. This aspect creates a different dynamic than investors are used to in the E&P space.

Note: BSM is a publicly traded partnership and issues a K-1 tax form which has different tax treatment than a 1099-DIV.

Black Stone Mineral's Permian and Haynesville Acreage (BSM Website)

Teamwork to Make Dreams Work

BSM's management has very creatively structured deals with producers to foster growth starting back in 2020. Blackstone has partnered with natural gas producer Aethon Energy to ensure gas flows out of its Haynesville acreage.

In 2020 it signed agreements to give Aethon Energy exclusive access to its Angelina County acreage and reduced royalties in exchange for contracted well development through 2028 . In 2021, a follow up agreement was signed for BSM's San Augustine County acreage through 2031. Both of these footprints are in the Haynesville Basin.

To ensure the acreage is developed and the wells are tapped to become productive, BSM structured a deal Aethon Energy can't refuse. Black Stone partners with 3rd parties to foot the development costs for Aethon. In exchange for this upfront capital expense, the 3rd party gets a fraction of the working interests in the well's productivity. Blackstone is willing to share a portion of its royalty income in exchange for contracted development on its acreage.

The Aethon development agreements are summarized below. These provide predictable revenue streams for BSM.

| Acreage Position |

| Year 1 |

| Year 2 |

| Year 3 |

| Year 4 |

| Continuation |

| San Augustine County |

| 5 wells |

| 10 wells |

| 10 wells |

| 12 wells |

| 12 wells per year |

| Angelina County |

| 4 wells |

| 10 wells |

| 10 wells |

| 15 wells |

| 15 wells per year |

A Different Business Model for a Different Dividend

BSM pays a traditional dividend of $0.475/unit that sports an eye-popping yield of nearly 11%. The immediate reaction is to view this as unsustainable, which in some respects, isn't far from the truth.

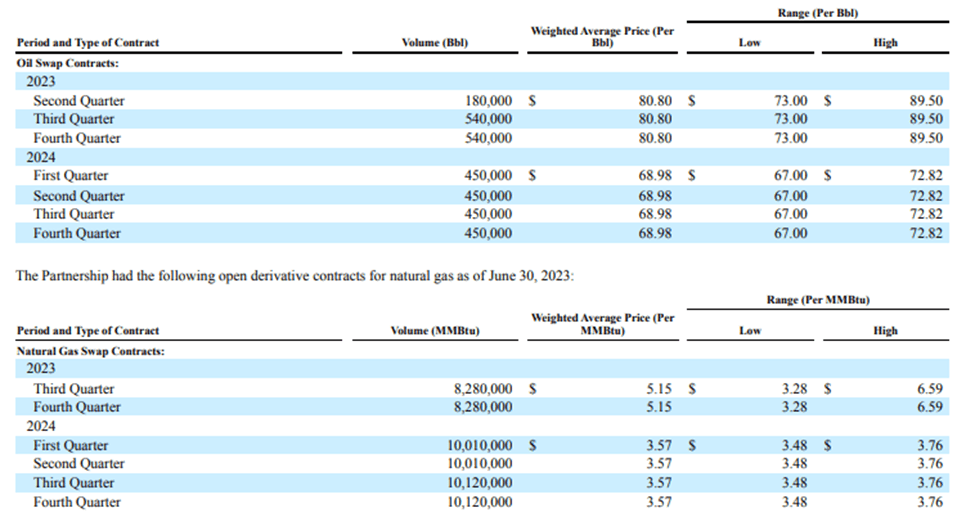

For the first two quarters of 2023, the distribution coverage has sat at 1.04x , which is alarmingly low. The biggest knock on BSM in 2023 has been that it is relying on its hedging program to generate sufficient revenue to support the dividend. However, now that oil has recovered from its June lows, the firm should have significant breathing room.

BSM Hedge Contracts (BSM 10-K)

{kind=link}

Turning to 2024, some challenges may arise due to a tightening hedge program. However, only half of its crude and two-thirds of its natural gas is hedged. There are multiple drivers that will ensure BSM's profitability remains intact.

1.OPEC+ is determined to keep crude over $80/barrel with production cuts. The unhedged portion will still be exposed to this upside.

2. 20 natural gas wells are contractually required to be completed in 2023, followed by an additional 25 in 2024. These additional volumes will provide incremental profits.

3. BSM is debt free to ensure a lean operating profile.

Valuation

So far, we have detailed mechanisms that BSM has to be able to sustain the current dividend and possibly grow its revenue base due to expanding natural gas production. To compound on this, BSM entered into an agreement with Longroad Energy to deploy solar panels on its property in a mineral rights deal. This provides the company with another potential source of revenue growth.

With those factors in mind, I believe BSM is more likely to grow in the medium to long term than it is to contract. I therefore view BSM as being fairly valued on a risk adjusted basis. Any pullback under $17/share would be a buying opportunity.

Risks

Natural gas has a variety of uses that more often than not, are impacted by the weather. This results in a very high level of volatility that often exceeds that of crude oil. As shown below, natural gas prices have swung over 200% since the beginning of 2021, while crude experienced only a 100% swing over that same time frame.

This dynamic can cause periods of extreme highs and extreme lows. Investors must plan on them being a reality and be prepared to stomach the rollercoaster. As mentioned, CHK has seen its annual dividend fluctuate from nearly $10/share to now a meager $2.30/share, so the volatility will show up in your pocketbook as well.

Buying now at the bottom of the cycle will help minimize risk. I recommend due to the level of volatility they create, that producers account for only 20-30% of your energy portfolio. If this level of volatility is too high for your personal tastes, I would recommend looking into a more oil focused producer that still has natural gas exposure. My favorites in this category are Devon Energy ( DVN ) and Pioneer Natural Resources ( PXD ).

Summary

In Part 1 of my natural gas playbook, we have explored two vastly different takes on natural gas production. Chesapeake Energy is a pure natural gas play that has the acreage and balance sheet to ramp up production when the market signals it is ready to pay up for its product. The variable dividend policy will give the company the tools to handsomely reward shareholders when profits start to rise in next 12 to 18 months.

My second candidate was slightly off the beaten path by exploring a royalty play in Black Stone Minerals. BSM has a healthy exposure to both natural gas and oil, so it is not a pure play on natural gas. BSM has the acreage and contracts in place with drillers to ensure its properties are tapped and cash flowing when natural gas exports start pulling molecules out of the Haynesville shale.

In Part 2, I will explore the midstream sector that will serve as an anchor to our energy portfolio.

For further details see:

The Dividend Investor's Natural Gas Export Playbook - Part 1