SRE - The Dividend Investor's Natural Gas Export Playbook - Part 3

2023-10-23 09:09:24 ET

Summary

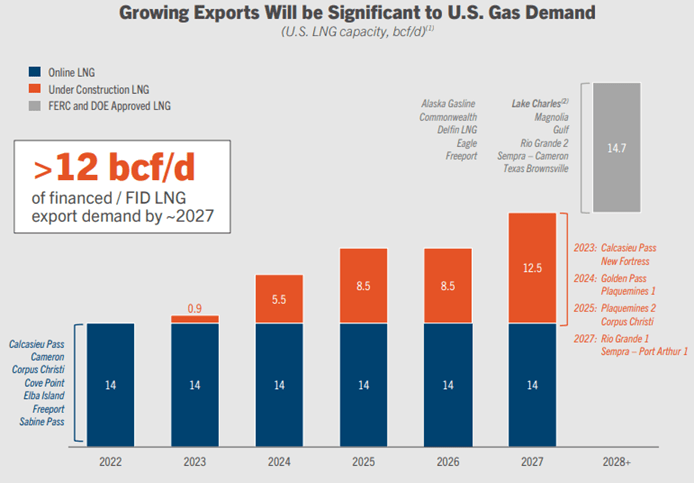

- Multiple natural gas export terminals are set to begin operations, increasing LNG exports from 14 BCF/d to over 26.5 BCF/day by 2030.

- Projects under construction such as Corpus Christi Stage 3, ECA Phase 1 and Port Arthur Phase 1 headline meaningful growth for Cheniere and Sempra.

- Both Cheniere and Sempra's LNG export divisions are in growth mode which can translate into high levels of free cash flow in the next 3 to 5 years.

- Cheniere and Sempra both have the potential to be strong dividend growth investments as LNG exports continue to ramp.

Thesis

Over the next 5 years, a multitude of natural gas export terminals are scheduled to commence operations. This will expand exported volumes of liquified natural gas ((LNG)) from roughly 14 BCF/d to over 26.5 BCF/day by 2030. The first projects (shown below)are slated to come online one year from now and will culminate in the first wave of an additional 5 BCF/d in 2024 and a total of 8.5 BCF/d by 2025.

- Golden Pass Trains 1-3 - Capacity of 2.6 BCF/d, in service 2H 2024

- Plaquemines Phase 1 & 2 - Capacity of 3.4 BCF/d in service 2H 2024

- Corpus Christi Phase 3 - Capacity of 1.6 BCF/d in service 2H 2025

A secondary round of projects that have reached FID will also serve to ensure these are not just one-off events. These supplementary projects will progress demand growth out to the 2027-2028 horizon.

- Port Arthur Trains 1 &2 - Capacity of 1.9 BCF, in service 2027

- Rio Grande - Capacity of 3.6 BCF, in service 2027

{kind=link}

As investors, this is an important market dynamic that can be captured for monetary gain. This can be done in several ways but also needs to be identified BEFORE the molecules start flowing. Part 1 of this series focused on the producers of natural gas. Part 2 focused on the midstream companies that will transport natural gas from the well heads to the export terminals.

Part 3 will be centered on companies that own the infrastructure that receives the process gas stream, cools, and compresses it to liquid form to load cargoes. These cargoes are loaded onto specially designed vessel at export terminals for international transport, mainly headed for Asia and Europe.

Export Terminals

LNG export terminals are the central theme to this entire series. They are the hubs that provide the rest of the world with cost advantaged US natural gas. These terminals are no easy feat to develop. They cost billion of dollars and years to construct. To make matters more complicated, there are numerous regulatory approvals ranging from FERC to the DOE, to local states and counties that are potential road blocks to their eventual construction.

As a result, the terminals that are existing and in operation today are extremely more valuable than those who have only reached FID. These terminals have a valuable characteristic that all shareholders want....cash flow. Cash flow combined with the existing infrastructure opens the door for further expansion in a cost effective manner while also lowering regulatory risk.

Both of the companies discussed are still in growth mode. As a result, they are better suited for a dividend growth portfolio than for high yield. My top companies in this space are Cheniere ( LNG ) and Sempra ( SRE ). Let's see what each company brings to the table.

1. Cheniere ( LNG )

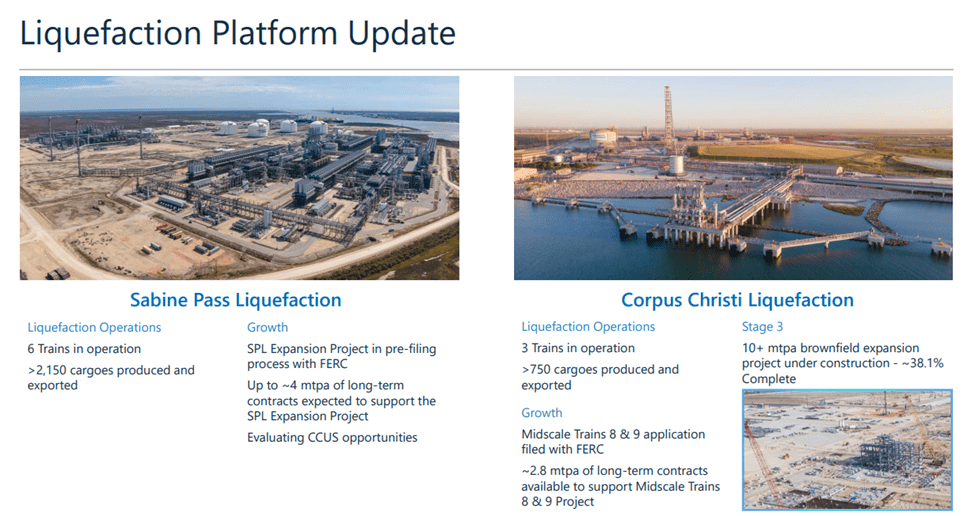

Cheniere is one of the most obvious choices to make this list with two terminals currently in operation and active expansion projects underway. Cheniere has both the Corpus Christi (15 Mpta capacity) and Sabine Pass (30 Mpta capacity) export terminals under its operating umbrella.

The corporate structure of LNG is slightly unusual. The Sabine Pass terminal is owned and operated by subsidiary Cheniere Energy Partners ( CQP ), of which LNG has a 50.6% ownership stake. The Corpus Christi terminal is owned outright by LNG. Therefore, from a simplistic point of view, LNG shareholders own a stake in 30 Mtpa of LNG export capacity, 15 Mtpa from each terminal.

Projects Under Construction

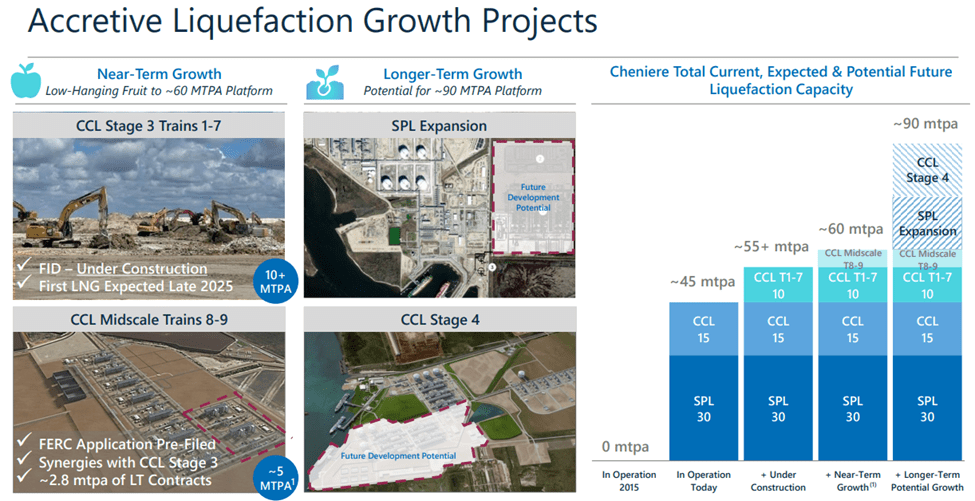

Corpus Christi ((CCL)) is currently expanding by building a Stage 3 consisting of 7 midscale trains. This will increase production by an additional 10 Mpta of capacity. This project is 38% complete with Train 1 over 50% complete . This project is expected to place its 10 Mpta of capacity into service in late 2025 with full capacity being reached in 2026. This would boost the owned capacity of LNG shareholders by 33%.

{kind=link}

Development Projects

LNG has a full docket of projects under development. These projects include further expansion at both CCL and Sabine Pass (SPL).

LNG has no plans to stop at 7 trains for Stage 3 at CCL. A bolt-on project will use the same midscale technology used in Stage 3 to construct Trains 8 and 9. The final two trains of Stage 3 are expected to add an additional 3 Mpta of capacity to the LNG portfolio, bringing the total CCL capacity to nearly 28 Mpta. Trains 8 and 9 have only entered the regulatory approval process and therefore should not be expected to be online until the 2nd half of this decade.

To expand Sabine Pass, LNG is also developing an expansion project to add an additional 3 trains of liquefaction. This project will increase total production capacity from 30 Mtpa to 50 Mtpa. Pending regulatory approval, this project would make Sabine Pass the largest export terminal in the world by leaps and bounds.

{kind=link}

Business Model

LNG is designed to operate similar to a midstream operator, extracting fees under long term contracts for volumes processed and having minimal commodity exposure. However, there are a few caveats that investors need to understand when looking at LNG's financial statements:

1. Revenue and expenses are tied to the change in commodity price. Both of these components fluctuate with the price of natural gas but higher revenue does not usually manifest itself in higher earnings. This is fairly common for midstream companies.

2. LNG uses SPA (LNG sale and purchase agreement) and IPM (Integrated Production Marketing) agreements to structure many of its contracts with customers. Accounting rules require LNG to realize the changes in contract value to reflect the change in commodity price. If you never heard of IPM agreements, you are not alone. Follow the link above for a quick and easy summary.

In the following two images you can see how three major metrics shift drastically.

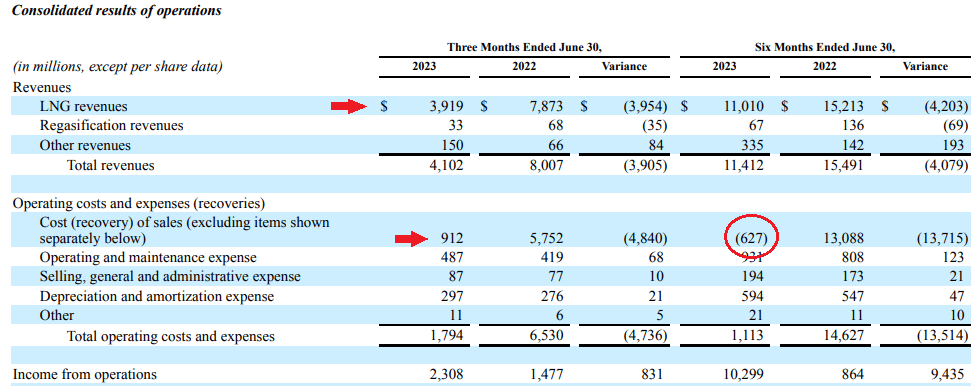

1. The first image shows LNG's earnings per share fluctuating from a net loss of $10 per share to a profit exceeding $20 per share over a one year period. This doesn't look like a midstream company at all.

2. The second image shows revenue and operating costs fluctuating by nearly $4 billion and $5 billion respectively on a quarterly basis. Furthermore, you can see that for the first six months of 2023, LNG's cost of sales was actually negative . This causes the reported earnings of LNG to be artificially high (reference the EPS of $20/share in Q1 2023).

{kind=link}

If taken at face value, LNG made $10.3 billion of operating income on $11.4 billion in sales so far in 2023. That obviously is not an accurate representation of reality. The traditional way of evaluating revenue and EPS growth just won't work here. We need to find a different metric that filters out the noise created by the changes in contract value.

The company acknowledges this fact and makes the following disclaimer on all conference calls, most recently in Q2 of this year.

As we have noted in prior earnings calls, our reported net income is impacted by the unrealized, non-cash derivative impacts to our revenue and cost of sales line items, which are primarily related to the mismatch of accounting methodology for the purchase of natural gas and the corresponding sale of LNG under our long-term IPM agreements.

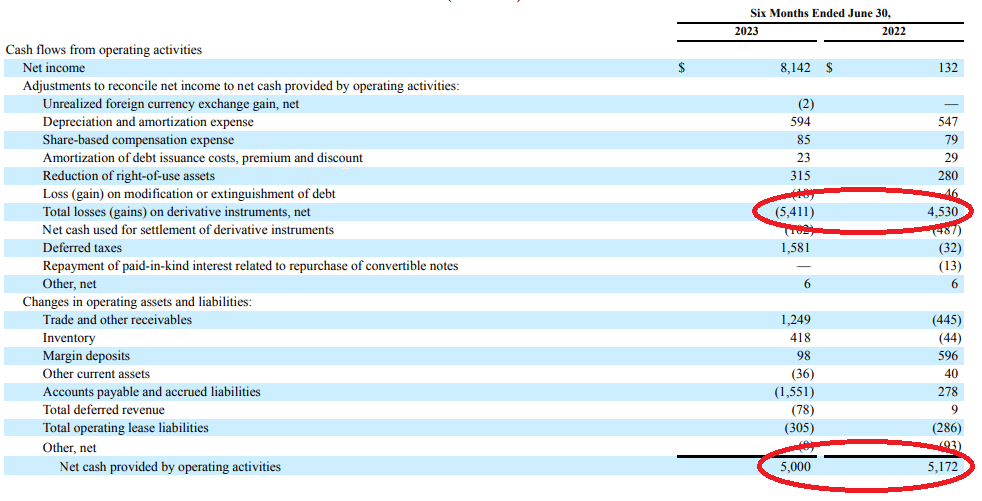

To give an accurate measure of its cash generating capabilities, LNG reports 'net cash provided by operating activities'. This reconciliation process adjusts for the change in value of its derivative instruments (SPA/IPM contracts). Using this method, we can see that net cash provided by operating activities has held relatively steady between 1H 2023 and 1H 2022 despite a drastically different natural gas price environment. This consistent performance is more typical for a midstream model.

{kind=link}

Valuation

Now that we have a useable metric, we can dive into how Cheniere is actually using its $5 billion in operating cash flow. Thus far in 2023, LNG has spent $788 million in stock repurchases, $195 million in shareholder dividends, while investing $750 million on CCL stage 3 to advance the project. That leaves us with around $2.5 billion in excess at the half way mark through the year. Management has thoroughly detailed how it plans to spend its discretionary cash flow in the quarterly conference calls.

We probably have around another $1 billion to spend on the Corpus Stage-3 project this year and then the dividend that were set to increase in Q3, like the guidance that we had last year.

...we are intent to catch up on the one-to-one cumulative ratio between debt paydown and share buybacks over time.

So there will be, over time, billions of dollars allocated to our buyback program.... eventually get to that $20 per share of run rate cash flow.

LNG has an incredible runway of opportunities for investors. With only $400 million in debt maturities in 2024, the company will have ample cash to repurchase shares while funding construction of CCL Stage 3 and increasing the dividend. As Stage 3 enters operation, incremental cash flows can support financing other projects in the pipeline.

Ultimately LNG is a cash flow powerhouse, but it needs some time to grow into its own shoes. By the end of this decade, volumes can grow by over 60% on an already high cash flow business. This cashflow can be deployed to retire debt and shares over the next 5 years. What will emerge, is a stable cash generation machine with a significantly improved debt profile as it prepares to enter the 2030s.

With a yield of only 0.89%, some may be wondering how LNG qualifies as a quality dividend stock. For the investor looking to pay bills with dividends today, LNG may not be the right fit. For those who are looking at retirement in 5-10 years, or potentially longer, LNG will be approaching the transformation phase from rapid growth to cash distribution. I believe LNG has the potential to be a dividend aristocrat in the making.

2. Sempra ( SRE )

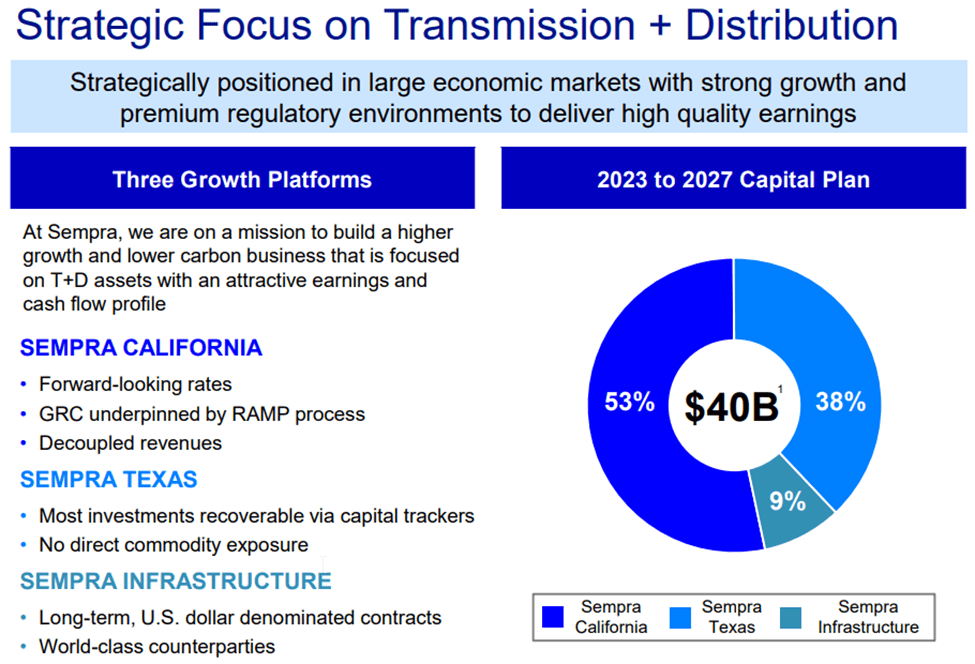

SRE is a utility company with operations mainly in California and Texas. Its California divisions are made of San Diego Gas & Electric (SDG&E) and Southern California Gas Company (SoCalGas). Texas operations are under the Oncor Electric Delivery Company. Finally, Sempra is rounded out by Sempra Infrastructure which includes its LNG portfolio.

For the first half of 2023, the infrastructure division has accounted for roughly 30% of the company's earnings. Being that the remaining 70% of the company is related to electricity and natural gas distribution, those businesses will be outside the scope of this article. SRE is worthy of further due-diligence.

{kind=link}

Sempra is less mature in the LNG game than Cheniere but has significant traction in the space. Anchored by the Cameron LNG terminal, SRE has a current export capacity of 12 Mtpa consisting of three separate trains. SRE owns a 50.2% ownership stake in the terminal which is operated under a joint venture.

Projects Under Construction

Sempra is taking a more broad approach to LNG exports than most of the companies we read about in this space. It has two projects under construction, Port Arthur LNG in the Gulf Coast, and ECA LNG located on the west coast of Mexico.

Port Arthur LNG has a projected capacity of 13.5 Mtpa, of which SRE will own a 28% equity stake. This terminal is projected to have Train 1 operational by 2027 and Train 2 operational by 2028. SRE has partnered with private equity firm KKR and ConocoPhillips to fund construction of Trains 1 and 2. SRE's share of output capacity is approximately 3.78 Mpta.

SRE is also advancing the ECA LNG terminal. Phase 1 of construction is scheduled to place 3 Mtpa in service by mid 2025. This project is coupled with the supporting GRO expansion project that will build out a 300 mile pipeline to support the ECA LNG terminal. The GRO Expansion pipeline is expected to enter service in 2H 2024 in preparation for the ECA LNG terminal to enter commercial operation.

Sempra

Projects Under Development

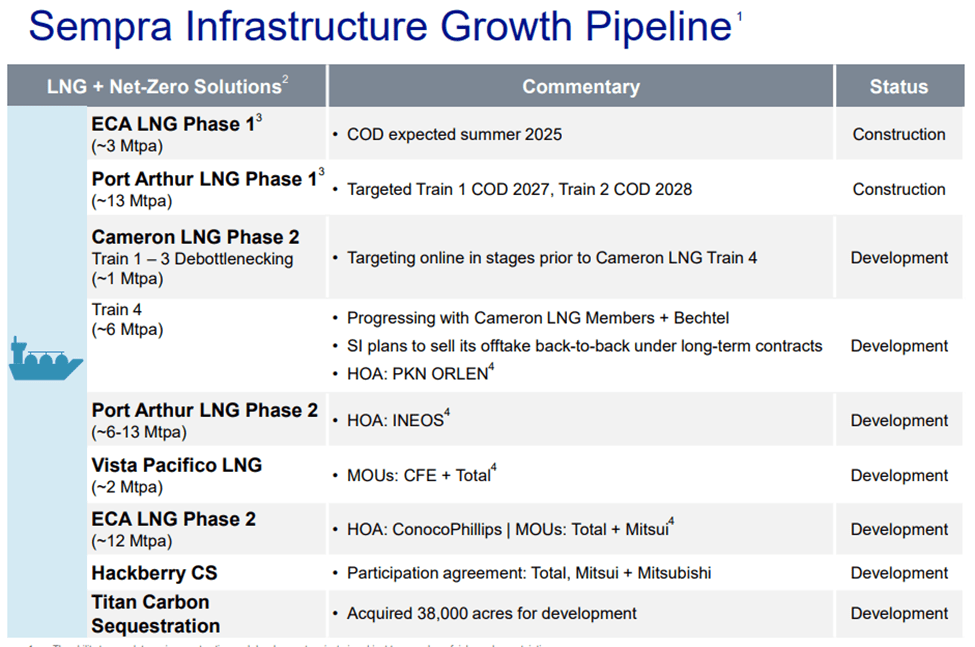

Sempra has several projects under development that will continue to expand its existing assets by building phase 2 projects at all three sites. The combined potential capacity of all three projects could exceed 30 Mtpa under current estimates. If these projects make it through FID and regulatory approvals, SRE would theoretically expand its export capacity by nearly 200%.

{kind=link}

Valuation

Since this isn't a comprehensive analysis of all of the components of SRE, how does all of this impact the bottom line for SRE? Is it enough to move the needle for the entire SRE portfolio? To keep this discussion practical, I will only account for the projects under construction. The total net increase in export volumes from the ECA and Port Arthur projects can be expected to grow by roughly 6.5 Mpta or over 100% from its current capacity.

Let's start by making the broad assumption that the infrastructure division is capable of doubling its earnings by doubling its volumes. To equate that to 1H 2023 dollars, infrastructure earnings could reach $1 billion or an increase of 30% for the entire company.

At the end of the day, SRE is still a utility stock. The growth potential of the Infrastructure segment gives it a unique advantage over its peers. You can see from the graph below, SRE trades generally inline with its peers. To be conservative, I will assume SRE's multiple shrinks to 16x. Assuming a 30% bump in earnings, the future price target of $79.87/share, indicates an approximate upside of 15%. All the while investors can collect the modest dividend yield of 3.4%.

While this is significant, the bulk of SREs planned investments are in its California and Texas operating companies which will continue to grow the other business segments. These businesses operate largely in a regulated environment and thus provide for consistent earnings growth.

{kind=link}

In an opposing fashion to LNG, SRE may be better suited for the more conservative investor looking to capture the growth of LNG exports that is built into a utility style business model. SRE is a more diversified export play that will be a steady performer in your dividend growth portfolio.

Risks

The largest risk to these companies (particularly Cheniere) is regulatory risk. A significant portion of the thesis developed here is based on regulators approving of expansion projects and pipelines. Unfortunately regulatory issues can be unpredictable once they hit a snag. Delays become costly to resolve, reduce overall project profitability and test investors' patience.

Should any of the projects proposed by LNG be unable to reach operation, the ability to be a significant cash producer will be hindered until it can work through its debt maturities. With over $9 billion in debt due by the end of the decade, LNG's priority of funding growth and share buybacks may need to moderate to service and/or retire debt.

In SRE's case, I view the regulatory risk as higher because of the complications associated with exporting through Mexico. That higher risk does not carry the same impact, however. With only 30% of the company's profits deriving from LNG, and significantly higher investment rates in its regulated business segments, the overall monetary risk is lower to achieve a reasonable growth rate.

Summary

In Part 3 of my natural gas playbook, we have explored two different companies that own and operate natural gas export terminals. Cheniere is a pure export play that has healthy cash flows coupled with a healthy pipeline of expansion projects underway or in development. The yield of 0.89% is meager at best. However, significant free cash flow will develop as projects reach commercial operation. LNG is an attractive dividend growth opportunity for investors on a multi-year horizon. These investors need to be willing to be patient to allow LNG to fully develop.

My second candidate was Sempra, but only the Infrastructure segment was analyzed. It was shown that the current projects under construction stand to raise the company's earnings by 30% over the next 5 years. This does not factor in growth from the companies other three divisions. SRE may be ideal for investors who have the desire for a modest and reliable dividend while the ECA and Port Arthur projects progress. As noted earlier, SRE's other divisions warrant further due diligence.

In Part 4, I will explore shipping companies that transport the liquified natural gas to its final destination.

For further details see:

The Dividend Investor's Natural Gas Export Playbook - Part 3