PXD - The Dividend Investor's Oil Playbook - Part 3

2023-06-14 02:49:13 ET

Summary

- In this four-part series, I will review how to structure a dividend investor's oil and energy portfolio with my oil and energy playbook.

- Part 3 will discuss the general strategy and our third position, the wide receiver.

- The wide receiver position requires discipline in selecting entry points. The investor must understand that the stock price and the dividend will be volatile.

- Just like in football, the playbook has roles for different segments of the industry. Upstream, midstream, and downstream all have their own unique roles to play.

Thesis

In Part 3, we will be expanding on the thesis laid out in Parts 1 and 2 for dividend investing in the energy industry. In Part 1, we examined what I called the offensive line. These were companies who's profitability was materially immovable based on commodity prices.

In Part 2, we examined versatile running backs to consistently hammer out gains. These companies had multiple revenue streams to provide steady and reliable income over a variety of market conditions.

In Part 3, we are looking for quick strike capability. Companies that have the ability to catch lightning in a bottle when energy prices skyrocket.

Our goals remain unchanged.

1. Provide a steady and reliable income stream

2. Protect invested capital from market downturns

3. Cues to call an audible and restructure the portfolio to lock in gains and protect the income stream.

The Wide Receiver

This position needs to be able to deliver big gains when energy prices start their runs. The converse will also be true. When energy prices are on a bottom swing, expectations must also shift for lower cash production. As a result, this position requires the most discipline when it comes to selecting an entry point. Significant volatility should be expected as the stock price and the dividend will follow hand in hand with the crude market. I target 25% to 35% of my portfolio for this segment. My top two picks for this position are Devon Energy ( DVN ) and Pioneer Natural Resources ( PXD ).

The Oil Barrens

The business model here is pretty simple. Both DVN and PXD are independent oil and gas producers. In its simplest form, these types of companies analyze, drill, extract, and sell crude oil, natural gas, and natural gas liquids from several thousand feet below ground.

Modern drilling techniques now include some form of horizontal drilling. Companies have been aiming to stretch these horizontal laterals further and further to increase the capital efficiency of each well. This allows for cost efficiencies to be realized by lowering mobilization, utility, and permitting costs while still optimizing the amount of accessible oil reserves. To be able to continuously execute on this initiative operators must own large uninterrupted sections of property, after all you can't just drill through your neighbors' property.

{kind=link}

It is important to remember that your investment dollars are being spent mainly on one thing, the land owned and/or operated by the company. If they are not drilling in prime locations, you can't expect prime returns. Selecting companies that have the best continuous block of acreage is a key variable when selecting oil producers.

Exponential Profitability

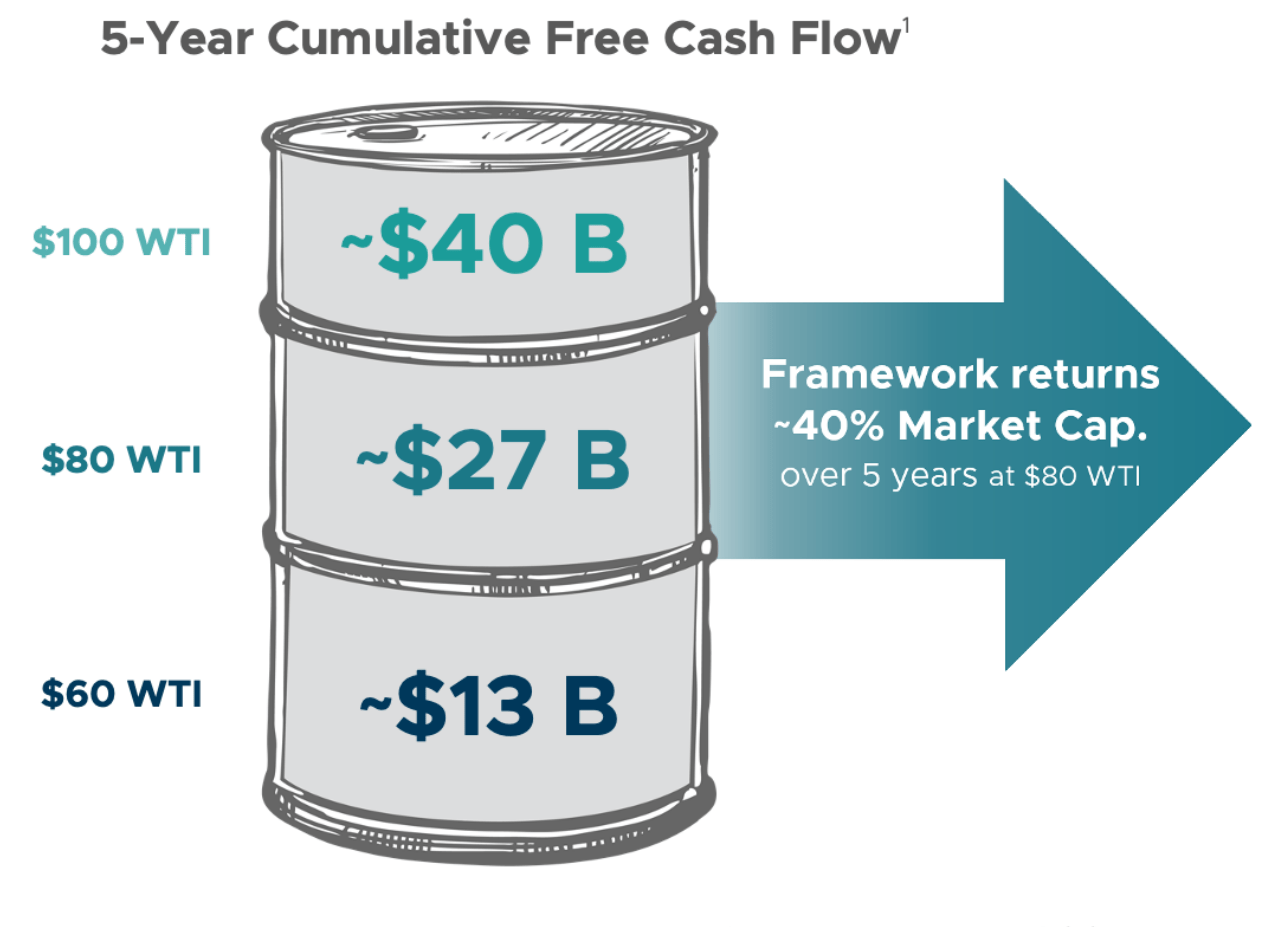

As in my other articles, I look to highlight areas where the company performance becomes dislocated from its price performance. The oil producer space benefits from exponential profitability as crude prices rise. As shown in the example below (provided by Pioneer) a $20 change in WTI oil price (33% change), translates into greater than 100% FCF growth.

{kind=link}

Let's put this thought process into practice in the graph below. This graph shows the cash generated from operations for both DVN and PXD. This metric, which I think of as pure profitability, shows cash generation grow to roughly 130% from a 70% increase in crude prices from July 2021 levels.

Now, we can all acknowledge there is no oil crystal ball out there to tell us what the next 6 months or even 1 year will be. What we can do, is look at history for an idea of what to expect. Below is a chart of WTI price of the last 10 years. For the last 10 years, oil has been significantly lower than today's prices, averaging somewhere around $60/barrel. That does not bode well for establishing a position in an oil producer does it? There have been two key changes in market dynamics that I believe will create a 'normal' price range that is higher than what the last decade has provided.

First, sanctions on Russia have, at a minimum, created a market disruption that makes it somewhat harder for the country to export its product. Russia is essentially restricted to selling to China and India as its main customers. The rest of the world effectively has a lower supply pool to get the resources that it needs.

Secondly, after the shale boom of 2014 and 2015, Saudi Arabia was content to maintain prices low to keep its market share. As a result, the market was flooded to keep prices low. After several years of that effort, Saudi Arabia has shifted gears and has been more inclined to protect its profit margins by altering the supply of oil production. This has been most recently demonstrated by two successive production cuts . I view the long term average for crude to be between $70 and $75 based on these two points.

Buyers Beware

After all of that, we still have to acknowledge the truth of the matter. Energy is cyclical industry and we should be prepared for a down turn. In fact, if you want to start a position or add to it, you should be looking for a down turn. We aren't the average investor after all and have the big picture in mind.

The average investor isn't buying oil producers when oil is $60 or $70/barrel. They are buying when oil prices are in the news every morning and headlines are rolling of record profits. They want a piece of the action, but are too late to the game.

Ultimately, these investors don't stand a chance. Once market conditions rebalance, these investors will be stuck with lower dividends and slashed share prices. Being selective and understanding the underlying value of the company allows us to invest with confidence when prices crater. Let's get started with my top two picks for Wide Receiver, DVN and PXD.

1. Devon Energy

The Permian basin is made up of two major regions, the Delaware Basin and the Midland Basin.

Devon produces roughly 67% of its output from the Delaware Basin. The rest of its production is sprinkled amongst the Eagle Ford, Anadarko, Powder River, and Williston Basins.

The key difference between the Delaware Basin and the Midland Basin is in the depth of the oil reserves. The same oil producing layers of the Delaware (namely the Wolfberry and Wolfcamp layers) are 2,000 ft deeper than the equivalent oil producing layers of the Midland. This presents a pro's and con's scenario.

1. Higher drilling costs from having to drill through 2,000 feet of more rock versus the Midland Basin.

2. Higher pressures are seen in the Delaware basin thanks to being 2,000 feet deeper. This aids in improving the amount of oil that can be extracted from a given well.

The higher upfront costs in exchange for higher levels of oil production works out to allow Devon to achieve a break-even price of roughly $40/barrel.

Permian Basin Profile (Search and Discovery Article #10412)

To further drive margins, Devon acquired Validus Energy in September of 2022. This move allowed DVN to acquire its neighbor in the Eagle Ford Basin. The Eagle Ford is a rather mature basin compared to the Permian that exhibits higher margins than the Permian .

This higher margin is driving a new wave of investment. On top of the efficiencies of buying neighboring acreage, a significant number of these existing wells are candidates for refracturing. This allows the original well to be reused to restimulate the shale rock and improve the well's performance. These activities will help maintain profit margins by being capital efficient versus drilling a new well.

For investors, all of this needs to be turned into free cash flow and dividends. Since 2021, Devon has implemented a variable shareholder return program. The total shareholder return package is a quarterly base dividend of $0.20/share plus 50% of free cash flow paid out as a variable dividend. Share buybacks are executed opportunistically beyond this model as cash balances permit.

I like the structure of this program for two reasons.

1. It's very defined on what shareholders should expect from a cash perspective.

2. Leaving 50% to be retained within the company is a meaningful amount that can be deployed for a variety of uses. Over the past year, management has executed two acquisitions, repurchased shares and retired debt with its portion of FCF. These have all increased the value of the company.

Paying out more to shareholders is too restrictive for management to execute on deals that can boost inventory levels, production, or both. An example of this would be the Validus acquisition and the Rim Rock acquisition in 2022.

More importantly, I believe DVN has the best program that can be sustained for the long term. Several other peers with variable dividends have either altered their programs or have structured them to be less strictly defined for cash generation or buybacks.

I view DVN as a buy below $48/share. I view this as a price point to sustain a 5% yield in a $70/barrel crude and $2.50/MCF price environment.

2. Pioneer Natural Resources

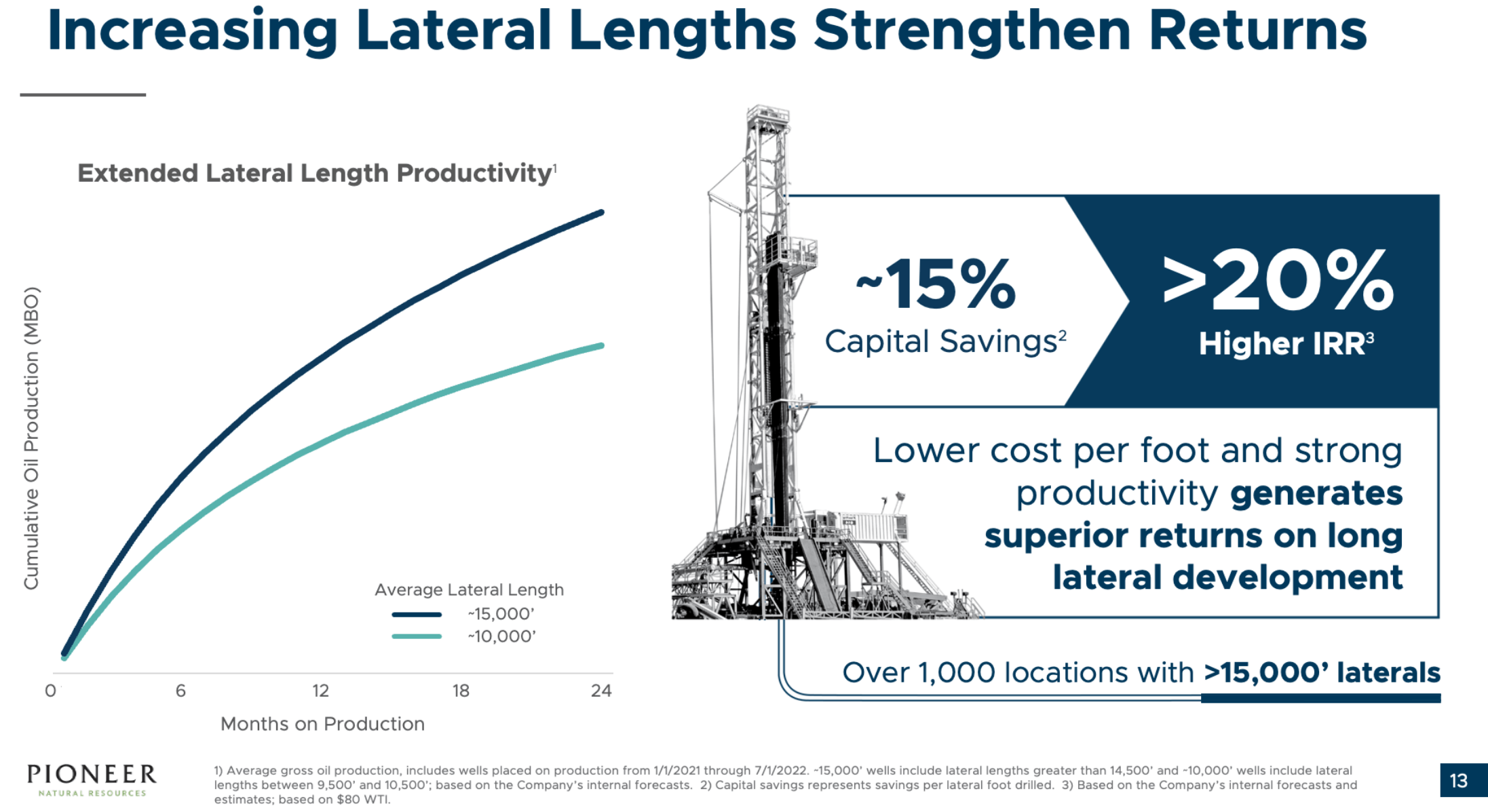

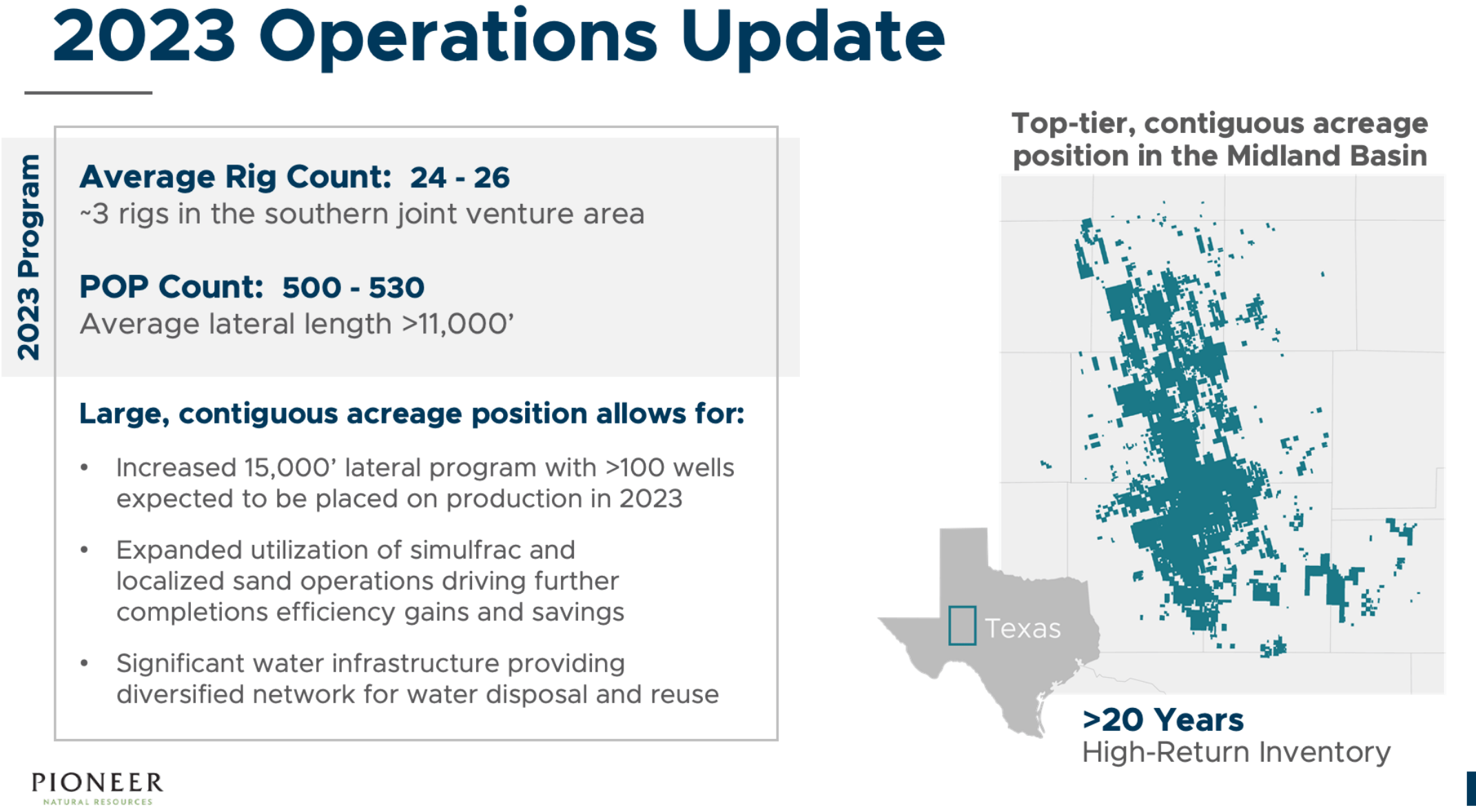

On the eastern side of the Permian, lies the Midland basin. As already stated, the midland basin benefits from lower upfront drilling costs. Pioneer is fully committed to this region with 100% of its production focused in this area. Committing to this region has allowed Pioneer to assemble its acreage to optimize operational efficiency as shown below.

{kind=link}

This continuous block allows for an inventory of over 1,000 well locations that can support 3 mile lateral wells. This will help ensure that PXD's breakeven cost stays as low as possible and maximize free cash flow from an operational standpoint.

The other operational driver is found from being located in the Midland basin. As mentioned earlier, the Midland basin requires less drilling to access the targeted reservoirs. This allows for lower upfront capital costs to establish a well head. These two factors combined support a break-even price of $40/barrel for PXD.

When it comes to shareholder returns, Pioneer's total shareholder return package is structured slightly different. Effective starting in Q2 of 2023, the return package will target returning 75% of free cash flow to investors . This 75% will include the base dividend, a variable dividend, and share repurchases. This is a throttled back version of the 2022 program which saw the company paying out over 100% FCF in 3 of the 4 quarters in 2022. This obviously could not be sustained for the long run, and has stemmed the most recent change.

The base dividend is a quarterly base dividend of $1.25/share, which is a healthy 2.4% yield at current prices. The remainder of the 75% payout is split between the variable dividend and share repurchases. The company has not provided any information how those two categories will be managed. Investors may see the variable dividend fluctuate based on share price. This potentially could mean lower share prices leading the company to repurchase more shares or high share prices leading to more cash being disbursed.

The lack of specifics on how FCF will be allocated is somewhat frustrating but may become more defined once the company gets some run time with the new program. Returning 75% of FCF to shareholders may be slightly too aggressive for investors looking for more long term growth. It's my opinion (as someone who is a way off from retirement) that this does not give management enough ammo to grow over the long term.

I view PXD has a buy below $200/share for a long term position. I view this as a price point to sustain a 5% yield in a $70/barrel crude and $2.50/MCF price environment.

Risks To Capital

Risks to overall performance are elevated when crude prices rise. It is worth a cautionary tale of chasing yield in this particular business. Yields will skyrocket as energy prices rise. In 2022, yields were seen to surpass 10% at the peak of the crude price curve. Investors who purchased at this time are probably regretting their investment choice now, less than 12 months later. Both share price and dividends have fallen during this period of time. This is natural for this business model and should be anticipated.

As mentioned earlier, we are hovering around the 10 year average for crude prices in this current environment. By virtue of being the average, one can expect prices to be lower as much as one can expect them to be higher in the future. Buying on dips from here not only allows buying quality companies at a lower price but also improves the odds of a successful investment from a statistics standpoint.

When to Stock Up and Lighten Up

These are companies that participate in a cyclic industry, and it would be foolish to expect these companies to perform otherwise. To keep it simple, remember to "lighten up when on top" to harvest profits. Buying when crude is below historical averages and selling when it is above historical averages is the best way to have a gauge for success. Investors can continue to reap the dividends along the way.

I do not advocate for totally liquidating a position when crude prices are high. After all, this is when the dividends will be the most lucrative. In this scenario, I recommend trimming roughly 10% to 20% of the position for later reinvestment.

It may also be worthwhile to consider putting a pause on a dividend reinvestment program when crude is at the top of its price curve. Your dividends will work harder for you if reinvested at a lower share price.

Summary

In Part 3 of the playbook, we have discussed understanding the relationship between crude prices, share prices and profitability for oil and gas producers. I proposed two solid companies that are both significantly off their highs from a year ago.

Since these stocks can be highly volatile, ownership of these stocks does require some aptitude for trading the stock. Buying and holding forever would let far too many opportunities to slip by for capital gains. I have recommended trimming back on positions in these companies when crude prices are significantly above historical averages.

In Part 4, I will review my top picks for the special teams position. These companies are slightly speculative in nature and have the potential for large growth in future earnings. Stay tuned for the last chapter in this four part series.

For further details see:

The Dividend Investor's Oil Playbook - Part 3