STR - The Dividend Investor's Oil Playbook - Part 4

2023-06-21 12:13:44 ET

Summary

- In this four-part series, I will review how to structure a dividend investor's oil and energy portfolio with my oil and energy playbook.

- Part 4 will discuss the general strategy and our fourth position, special teams.

- Both companies have unlocked the potential to spur growth over the long run.

- Just like in football, the playbook has roles for different segments of the industry. Upstream, midstream, and downstream all have their own unique roles to play.

Thesis

In Part 4, we will be concluding on the thesis for dividend investing in the energy industry. For our final component, we are looking for companies to fill the special teams role. This position generates points in ways that are not always considered 'conventional'.

Our goals remain unchanged.

1. Provide a steady and reliable income stream

2. Protect invested capital from market downturns

3. Cues to call an audible and restructure the portfolio to lock in gains and protect the income stream.

The Special Teams

This position needs to be able to put points on the board in a different way than the companies discussed in Parts 1, 2 or 3. To fit this bill, we will be looking at royalty companies. These companies own mineral rights and allow the big producers to drill and extract on their acreage for a set percentage of the total revenue. As a result, these companies have very little invested capital to generate a profit and have extremely low break even prices. I target 10% to 20% of my portfolio for this segment. My top two picks for this position are Sitio Royalties Corp ( STR ) and Black Stone Minerals ( BSM ).

Living Like Royalty

The mineral royalty business model is appealing. From a basic perspective, this is a very passive business. The companies own the mineral rights, while the drilling operators do all the work and investment to extract the oil and natural gas. The operator pays the agreed royalty to the mineral rights owner for the duration of the lease or until operations cease. From a high level, this is certainly a good qualifier for a SWAN investment.

The real work done by the mineral royalty company is completed long before a drill ever hits the dirt. After all, sleeping well at night is only reserved for those who did their homework well ahead of time. These types of companies need to be investing in prime drilling real estate and need to be adept at structuring deals to get operators to drill on their land.

The value of deal making can't be under stated here. All of the oil reserves in the world aren't worth a penny if you can't get someone to drill on your land. In this last edition we will be looking at how Sitio Royalties and Black Stone Minerals are preparing for the future with some unique growth opportunities to bolster their already impressive cash flows.

1. Black Stone Minerals (BSM)

BSM is a natural gas heavy mineral owner that currently sports a screaming 11.8% yield. It has a fairly diverse portfolio, tapping into four of the major US basins. The bulk of the volumes extracted on their properties are out of the Haynesville basin in Louisiana and Eastern Texas.

NOTE: BSM is a publicly traded partnership and issues a K-1 tax form.

BSM Production Profile (BSM 10-K)

You might be a little skeptical. An almost 12% yield from a company that generates the bulk of its volumes from natural gas has to be heading for a dividend cut right? With oil continuing to slip below $70/barrel, you could be right.... at least for now. We'll touch on that in a little bit.

Management has been pretty blunt that it intends to maintain its dividend at its current level for as long as it can. During the Q1 conference call , management gave the following color surrounding the plans for the dividend.

... so right now with a 1.04 times coverage, and really just with where the balance sheet is today. We do feel comfortable, maintain a little bit lower coverage in the near-term. Something that we always look for as we establish our distribution policy and what we look for going forward is something that we can have a stable to slightly growing distribution as we look at our forecasts.

But really, with the Aethon development agreements, and even the Austin Chalk, where we expect to see ramping up production for the second half of the year. We still see growing volumes, potentially from those areas that may mitigate some of the risks and the others. And that gives us confidence in the current guidance that we have outstanding.

I will acknowledge right off the bat that a 1.04 times coverage of the distribution is not great, and I personally would like it to be significantly higher. But I can give you three reasons why we should feel comfortable with management running the company nearly flat out right now.

1. No debt to starve cash flows.

2. Incredible hedge contracts for the rest of 2023.

3. Artful deal making to ensure production grows on its properties even during downturns.

No Debt

BSM has only $10 million in debt and that's it . The miniscule amount of debt currently being carried by the company is immaterial compared to the $4 billion market cap of the company. The debt just doesn't have the horsepower to affect the company's cash flows. Additionally, BSM has $66 million in cash as a nice rainy day fund.

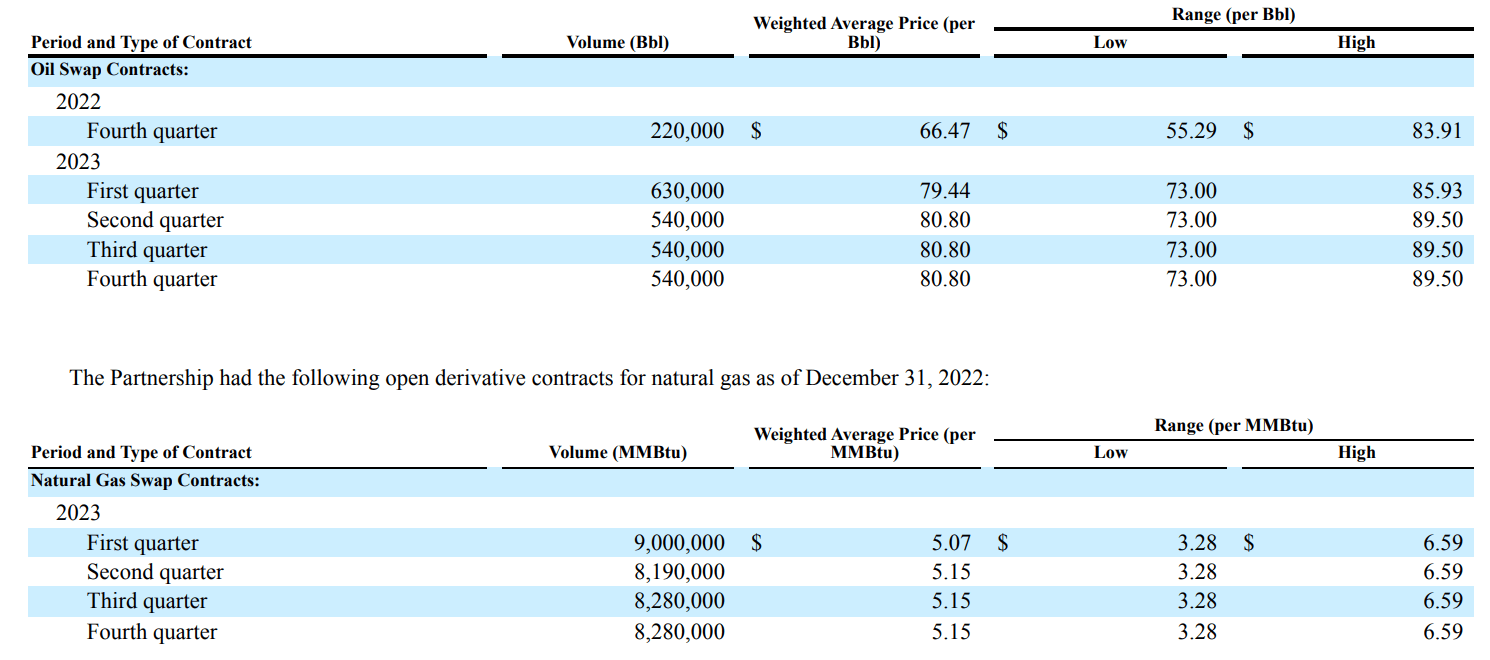

Hedging To Save The Day

BSM is benefiting from some tremendous hedging contracts . The following table shows the hedging contract structure developed by BSM. This accounts for roughly 63% of its oil volumes and 56% of its natural gas volumes.

In Q1, BSM reported a profit of over $13 million thanks to contracts worth over $79/barrel of crude oil and $5/MCF. These contracts are incredibly meaningful to the current success of BSM, accounting for 12% of the total EBITDA generated for the quarter. This benefit will be available through 2023 but will not be as lucrative in 2024 , when the contracts' average natural gas price falls to $3.64.

{kind=link}

Production Growth

The growth strategy of BSM is the key differentiator between it and the rest of the pack. And it has all been done internal to the company. Blackstone has partnered with natural gas producer Aethon Energy to ensure gas flows out of its Haynesville acreage.

In 2020 it signed agreements to give Aethon Energy exclusive access to its Angelina County acreage and reduced royalties in exchange for contracted well development. In 2021, a follow up agreement was signed for BSM's San Augustine County acreage. Both of these footprints are in the Haynesville Basin.

To ensure the acreage is developed and the wells are tapped to become productive, BSM structured a deal Aethon Energy can't refuse. Black Stone partners with 3rd parties to foot the development costs for Aethon. In exchange for this upfront capital expense, the 3rd party gets a fraction of the working interests in the wells productivity. Blackstone is willing to share a portion of its royalty income in exchange for contracted development on its acreage. The contracted number of wells required to come online each year is shown below.

| Acreage Position |

| Year 1 |

| Year 2 |

| Year 3 |

| Year 4 |

| Continuation |

| San Augustine County |

| 5 wells |

| 10 wells |

| 10 wells |

| 12 wells |

| 12 wells per year |

| Angelina County |

| 4 wells |

| 10 wells |

| 10 wells |

| 15 wells |

| 15 wells per year |

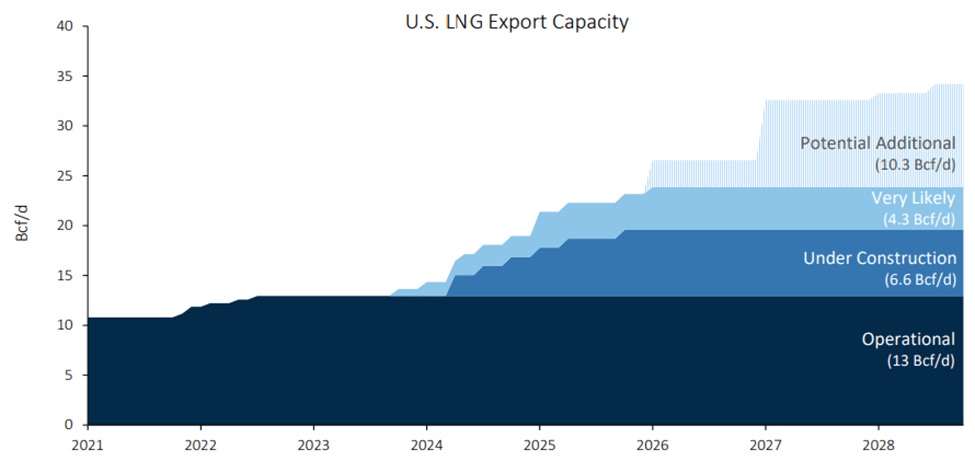

In the next 18 months, I believe we will see a large boost in the demand for natural gas. There are significant projects under development for the exportation of LNGs that could potentially double export volumes in just a few years. These projects are expected to go into operation starting in 2024 through 2027 and will meaningfully increase demand for US LNGs. Additionally, being located near the gulf coast, the Haynesville basin is uniquely positioned to benefit from these projects.

Further, multiple pipeline projects are under development to ensure gas from the Haynesville is available to support this export demand. Enterprise Products completed a 400M cf/day expansion of its Acadian Haynesville Extension natural gas pipeline. In addition to that, 5.0 BCF/day of pipeline capacity is expected to come online by the end of 2024.

{kind=link}

2. Sitio Royalties Corp. (STR)

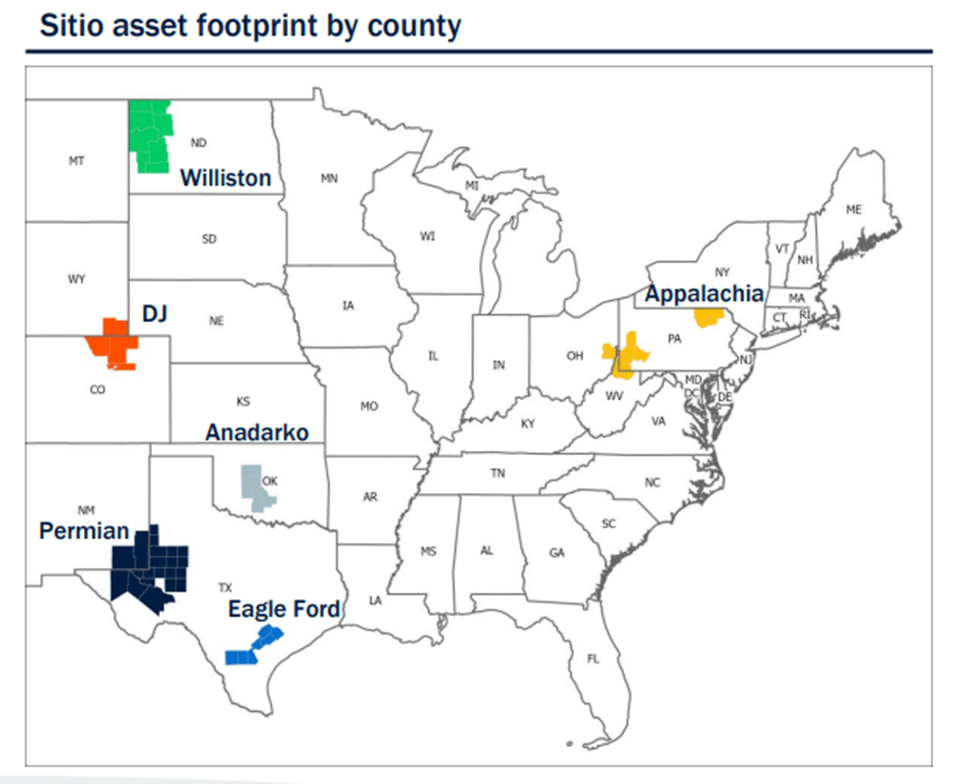

Sitio has a rather diverse portfolio, with properties in 6 different basins. The bulk of its properties reside in the Permian basin which is a very clear growth basin for the oil and gas industry. Beyond that, the DJ and Eagle Ford basins comprise 10% and 8% of the company's net royalty acres (NRAs) respectively.

Having a high intensity in the Permian has allowed Sitio's production profile to be roughly 50% oil and 25% natural gas and NGLs respectively. This production profile lands Sitio as the third largest producing mineral interest company in the industry.

{kind=link}

A Little Known Secret

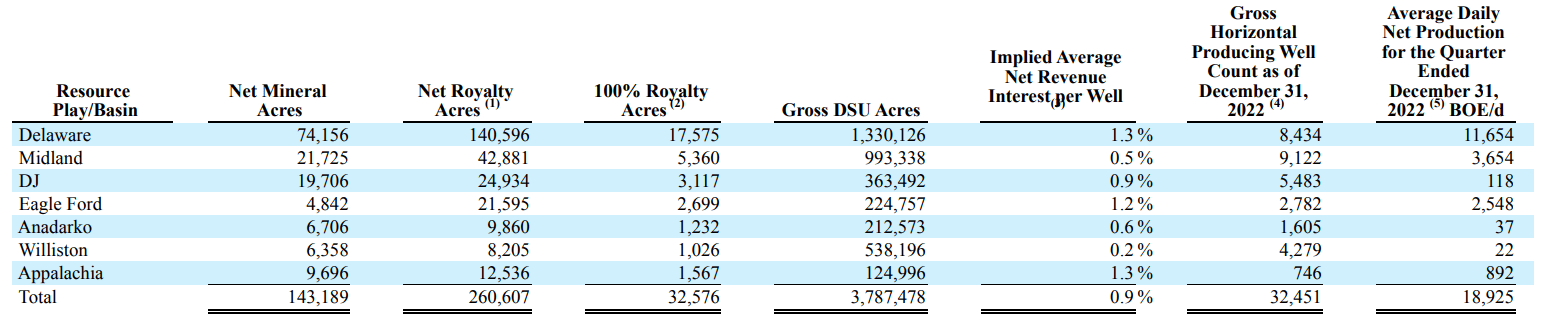

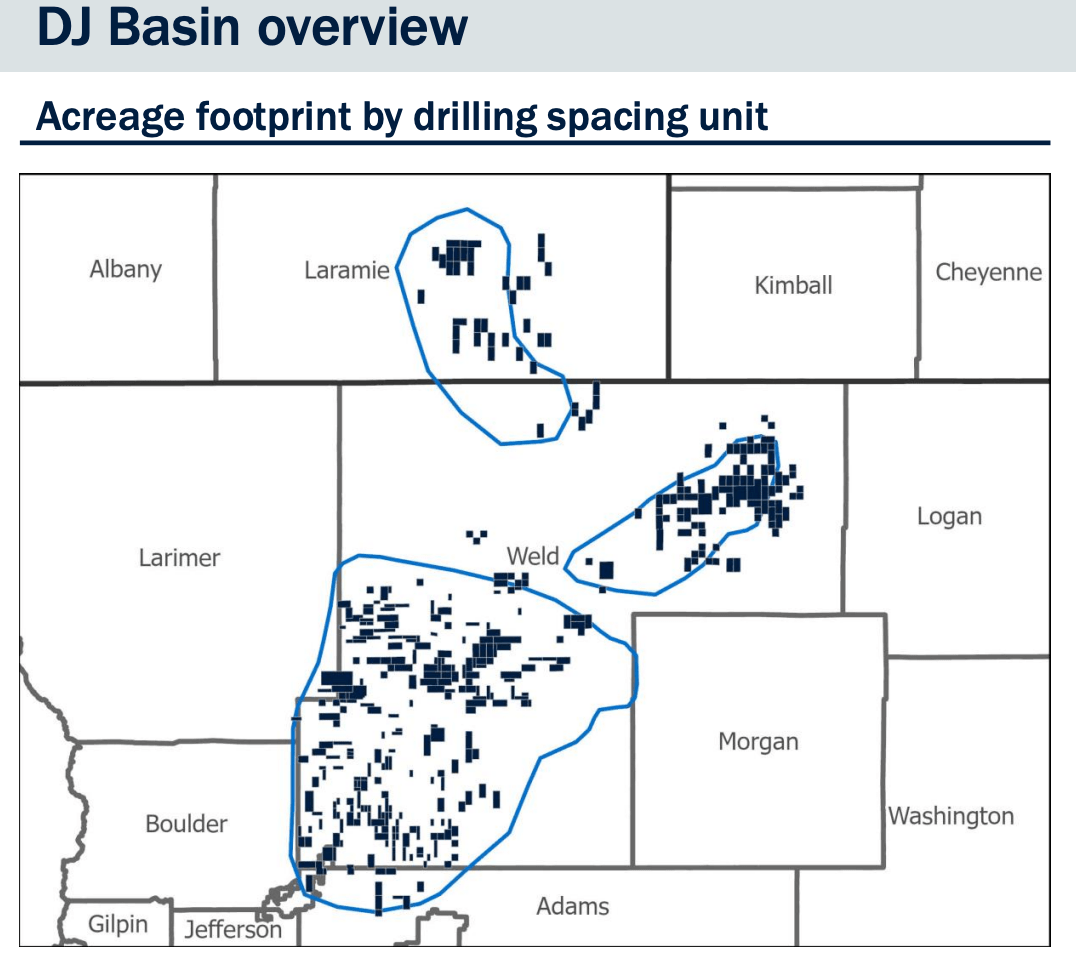

One of the diamonds in the rough for Sitio is its DJ basin assets. From the 10-K annual report figures below, you can see that the DJ basin accounts for just shy of 10% of its NRA property but accounts for just 0.6% of its daily production. Here in lies a built in growth opportunity.

{kind=link}

For those who are unfamiliar with the DJ basin, it is located in Weld County, Colorado. Since 2019, the DJ has seen all but zero growth as a result of regulation changes that completely changed the way the state regulated drilling permits (Bill SB-181). SB-181 was originally passed in 2019 and went into full effect in 2021. Finally, after almost two years, permits have begun to work their way through the new process.

The rapid expansion of approved well drilling permits in Weld County can be found on the COGCC website . As of this writing, there are 374 new well permits approved since January 1st of this year, and 872 since June 3rd of 2022. I have plotted a few of the locations of the larger well sites (greater than 6 wells in one general location) using Google Earth. You can see that these well sites align extremely well with Sitio's territories.

{kind=link}

It may take some time for these permits to be fully turned into online wells but there certainly is potential to be had here. If the acreage in the DJ can pull its weight by increasing its production to be equivalent to the second tier properties such as the Midland or Eagle Ford basin, we could see an overall growth of 10% or more.

Some of the biggest players in the DJ Basin are Occidental ( OXY ), Civitas ( CIVI ) and Chevron ( CVX ). If there are big fish in the pond, there must be big food. And as a result, these big fish are committing to the basin with OXY budgeting $750 million in CAPEX for 2023. One of the highlights for the quarter for OXY was a nearly 5 mile long well (the longest ever drilled in the DJ) in just 8 days.

The other big fish, Chevron, made the following statement .

DJ Basin is the other primary growth. We've got rig lines being added there and activities. We're going to add almost 70% more POPs in 2023 than we did in 2022. Still a flexible base

DJ Basin Properties (STR)

{kind=link}

Working Down Debt

In contrast to BSM, Sitio is far from debt free. With $938 million in debt compared to a market cap of $4.2 billion, it has a somewhat large but not insurmountable debt level. The most notable aspect of their debt is their 2026 Senior Notes worth $450 million. These notes restrict the company from buying back shares and also caps distributions at 65% of discretionary free cash flow.

I don't feel this agreement is overly restrictive to shareholders. In Part 3 of this series, I advocated that a 75% distribution for Pioneer Natural Resources may be excessive for the long term benefit of the company. A 65% model is more ideal for STR for two reasons.

1. It gives management more leverage to pay down debt and potentially remove the 65% covenant down the road.

2. As a royalty company and not an independent producer, STR has little to no CAPEX requirements to sustain the business.

Additionally, the company's 35% share still has enough meat on the bone to pay down debt and fund the occasional acquisition.

Risks to Capital

This space largely trades with yield. Therefore, from a general perspective, the entry price will ultimately determine the success of investment. I discussed in Part 3 how I believe energy prices are at or below what I view as the going forward long term average. By virtue of being roughly at the average, one can expect prices to be lower as much as one can expect them to be higher in the future. Buying on dips from here not only allows buying quality companies at a lower price but also improves the odds of a successful investment from a statistics standpoint.

When to Stock Up and Lighten Up

Since this group of companies trades with yield, we should identify an expected level of consistent performance that each company can achieve.

For BSM, the current dividend is $0.475/quarter and we have discussed how management is running with only a minimal amount of margin. Therefore, for safety we can assume a 20% dividend cut is possible, which would take the distribution to $0.38. To achieve a long term return of 10%, I believe a price action level of $15.20 is appropriate to develop some safety margin. BSM has traded below this value three times this year and thus I believe there is reason to be patient and wait for prices to recede from current levels.

For STR, being a C-Corp makes the 10% level unrealistic. 7% is certainly a high level for a C-Corp structured company. Considering the near term growth opportunities in the DJ basin, a 15% reductions from Q1's dividend provides some degree of safety margin. This would equate to a long term sustainable dividend of $0.425/quarter. To achieve a long term return of 7%, I believe a price action level of $24.25 is appropriate. Similar to BSM, this value has appeared multiple times so far this year and investors will be rewarded to be patient.

Summary

In Part 4 of the playbook we looked at two royalty companies that are currently producing solid yields and have some long term potential to grow cash payments to shareholders. The price action levels outlined in this article are slightly lower than today's prices but I believe are achievable for the patient investor waiting for the right opportunity.

This concludes my four part series for dividend investors in the oil patch. Thanks to everyone for the comments and the follows. I have received a lot of good feedback from this series and am looking forward to the next project. I hope all of the readers benefited from this series.

For further details see:

The Dividend Investor's Oil Playbook - Part 4