NAPA - The Duckhorn Portfolio: Consumer Weakness Finally Showing Up In The Stock

2024-01-02 13:07:42 ET

Summary

- The weak consumer demand is affecting NAPA business performance.

- Revenue declined 5.2% with a decline in volume and price/mix.

- Management's lowered FY24 guidance and remarks about slowing demand raise concerns about NAPA's ability to meet expectations.

Investment action

I recommended a hold rating for The Duckhorn Portfolio ( NAPA ) when I wrote about it the last time , as I remained concerned about the near-term uncertainties regarding the business performance outlook and the lack of a proper CEO. Based on my current outlook and analysis of NAPA, I recommend a hold rating. It is pretty clear that weak consumer demand is affecting the business, leading to NAPA missing consensus estimates for the first time in 10 quarters and also a downward revision in guidance that signals weak velocities. I also do not see any possible catalyst in the near term that can drive the stock up.

Review

NAPA reported a revenue decline of 5.2%, driven by a 3.4% decline in volume and a 1.8% decline in price/mix. The decline was in line with management’s guidance of a mid-single-digit to high-single-digit decline. Revenue came in at $102.5 million. Gross margins saw 52.1%, which expanded 151 bps annually, beating the consensus estimate of 50.4%. Better cost management also led to an EBITDAS margin expansion of 34.2%, translating to an EBITDA of $34.7 million. Adj EPS came in at $0.15 vs. 1Q23 of $0.17.

My concerns about the near-term performance outlook appear to have crystallized into actual headwinds. Let me remind readers that neither category saw any growth, even though management is certain that there isn't much trade-down happening and that luxury wine is still outperforming the broader category. The direct-to-consumer [DTC] channel also encountered growth headwinds. One thing that stood out to me was when management mentioned that hotel occupancy in Napa Valley was soft. I take that as more proof that the aspirational consumer is cutting back on their spending.

According to Circana, growth in total wine softened as did the luxury wine segment defined as $15 and above. In the last 12 weeks, the luxury wine segment was flat and total wine overall declined 1.6%.

Our Q1 results are emblematic of broader post COVID trends in consumer behavior. Across Napa Valley, hotel occupancy rates have dipped, but room revenue has continued to grow as strong demand at the highest end has buoyed average room rate. 1Q24 call

Perhaps a more concluding factor that NAPA performance is not going to see any recovery in the near term is that management has lowered its FY24 guidance to the low end of its initial range while also lowering the top end. Specifically, management now expects net sales at the low end of $420 to $427 million, from $420 to $430 million previously, or about 4-6% y/y growth vs. the previous 4-7% y/y growth. At first glance, it seems like management guidance has not made much difference. However, that is not the case. Considering that the outlook was supposed to be strengthened by both increasing labels per account and account growth (which was expected to grow at a CAGR of 7 to 8% through FY27), the lowered low-end sales outlook is worrisome. What the guide is implicitly saying is that NAPA is experiencing worsening velocities.

I would point out also our account growth, which I think that the first of the three key vectors to wholesale growth going from 59,000 to 64,000 as of June 30, 2023, and a projection that we take out at a CAGR of 7% to 8% over the next four years for growth. 4Q23 call

Softer trends for the Decoy red varietals and remarks from management regarding a slowdown in demand while customers process pricing actions are supporting evidence of weak velocities. Doing the math, this weakening velocity headwind is about 250 bps (7.5%–5% FY24 guided growth). With the current consumer spending backdrop and management comments, I am also uncertain whether NAPA can grow accounts at 7 to 8% in the near term (remember this is a CAGR projection, so growth need not be linear). Suppose account growth slows. I think there is a good chance that NAPA might miss its FY24 guidance. All it takes is for account growth to slow by >100 bps (750 bps accounts growth guide minus 100 bps decline = 650 bps at the midpoint minus 250 bps headwind = 400 bps growth).

Aside from weakness in NAPA fundamentals, I also think there is a near-term impairment to the stock narrative, as this is the first time NAPA missed consensus estimates after 10 consecutive quarters of revenue beat. Over the past 10 quarters, the market and consensus generally align their estimates with management guidance because it has a strong track record. As to all aspects of life, once the “trust” is broken, it is harder to believe in the next round. As such, I believe the market is going to take a much more conservative approach in their estimates, at least for the next few quarters, until it gains confidence in management’s guidance. From a valuation perspective, the stock is unlikely to see any upside rerating until NAPA shows sufficient evidence that the demand backdrop has recovered and NAPA can meet its guidance.

Valuation

{kind=link}

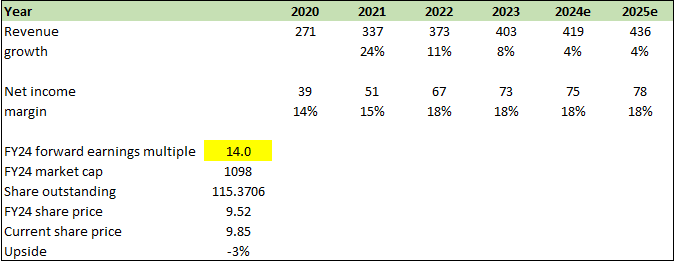

My revised model target price is $9.52 in FY24. I now expect growth to come in at the low end of the management-guided range over the next 2 years, as there are visible signs of demand weakness. Likewise, I am expecting margins to remain flat over the next 2 years, as management likely needs to step up on promotion (to improve DTC sales) and invest in its Decoy product line. I am also assuming valuations to stay at 14x for the rest of the year, as I do not see any positive catalyst in the near term to drive this up. As you can tell from my model, I am making very conservative assumptions. I acknowledge that I could be wrong; however, I think it is safer to be conservative and turn bullish when NAPA performs than to take a gamble at this point. Note that NAPA used to trade at a 20+x forward PE, so there is a lot of room for NAPA to recover, which means investors will have many opportunities to buy the stock if it performs better than expected.

Risk and final thoughts

A potential risk to my hold rating is that NAPA may see stronger-than-expected demand for its premium and ultra-premium wines if the overall economy shows signs of improvement. Furthermore, if it is successful in passing through additional pricing or if higher-margin ultra-luxury wine grows at a faster rate, margins could end up ahead of my expectations.

In conclusion, I recommend a hold rating for NAPA due to evident consumer weakness impacting its financials and the lack of near-term positive catalysts. Management's revised guidance at the lower end, implying worsening velocities, also make me feel uncertain about the business's ability to meet guidance. Additionally, the stock’s narrative is not great after its first consensus miss (after 10 quarters).

For further details see:

The Duckhorn Portfolio: Consumer Weakness Finally Showing Up In The Stock