VERX - The EngageSmart Buyout Doesn't Feel Right

2023-10-26 13:50:57 ET

Summary

- EngageSmart, Inc. has agreed to be acquired by Vista Equity Partners in a $4 billion deal, representing a 13.9% premium to the closing price before the announcement.

- The company has shown strong growth, with revenue increasing from $109 million in 2020 to $303.9 million in 2022, driven by both segments of its business.

- The transaction raises questions about the company's potential for further growth, as well as the decision of the majority shareholder to retain a 35% stake in the combined company.

Whenever you own shares of a company that ultimately agrees to be bought out, odds are that you have mixed feelings. On the one hand, the premium that almost always accompanies that announcement is nice to see. It's great to have a nice bit of upside, especially if you haven't held the stock for long, in your portfolio. On the other hand, if that premium is not large enough, it can leave a bitter feeling in your mouth because of the prospect of leaving too much money on the table.

Generally speaking, I am supportive of buyouts. This is because the premiums are often enough for a value investor like myself to be satisfied. But this is not always the case. One company that just agreed to sell itself free premium that I don't quite feel the most comfortable about, is EngageSmart, Inc. ( ESMT ). Relative to the current valuation of the company, the purchase price is quite lofty. But given how small the company is, how fast it's growing, the market size that it has an opportunity to capture, and management's own rhetoric earlier this year, I would argue that there probably was some additional upside on the table had investors held the stock for the long haul.

A simple buyout

According to a press release issued by EngageSmart, the company agreed, on October 23rd, to be acquired by private equity firm Vista Equity Partners in a deal valued at $4 billion. This translates to $23 per share and is being done completely with cash. Management claims that it represents a 30% premium to the 30-day unaffected volume weighted average price of the stock. But relative to the closing price seen just one day before the announcement, it's a premium of only 13.9%.

Although management states the value as being $4 billion, I get something slightly different. Using the most recent share count available, I get a market capitalization at the buyout price of $3.91 billion. However, the company has no debt on its books and it enjoys $332.8 million in cash and cash equivalents. That brings us to an enterprise value of $3.58 billion.

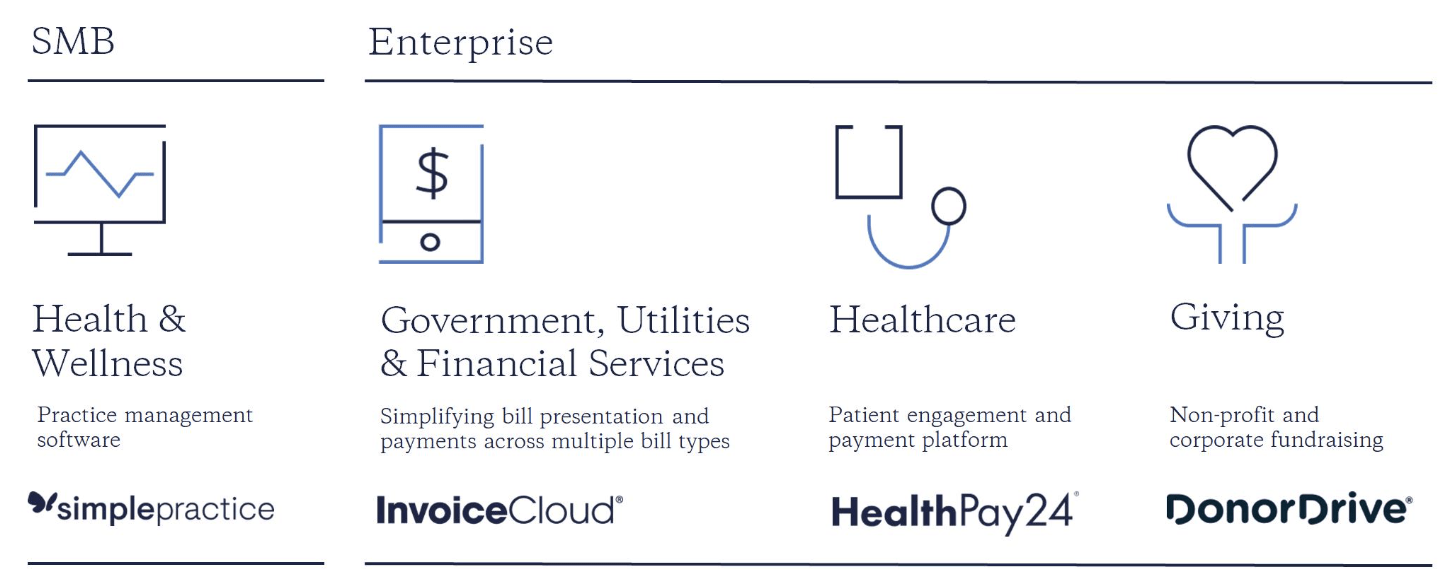

Although a 30% premium over what shares were over the span of 30 days might seem great, a better understanding of the business and where it's at can give us some perspective. For those who don't know about the company, it operates as a software provider and an integrated payments solutions firm. Operationally, it has two different segments. The first of these is the Enterprise Solutions segment, which largely provides bigger customers certain SaaS solutions aimed at simplifying customer client engagement through electronic billing and digital payments. And the second is the SMB Solutions segment that provides and practice management solutions centered around the health and wellness industry.

{kind=link}

This is all kind of vague, so it might be helpful to dig a bit deeper and talk about specific applications. One of the services the company offers is called SimplePractice. It provides end to end practice management and electronic health record services for health and wellness professionals. Its InvoiceCloud offering is an electronic bill presentment and payment solution largely dedicated to helping out government entities, utilities, and financial services customers digitize billing, handle client communications, and handle collections. HealthPay24 is a patient engagement and payment platform that helps those in the medical space drive patient self-pay collections. This is interesting because collecting payments can be a costly business. So any technology that nudges customers to handle their own bills likely has value to it. And finally, we have DonorDrive, which is a fundraising software platform that helps customers produce virtual events, launch branded donation campaigns, and create peer-to-peer fundraising activities.

{kind=link}

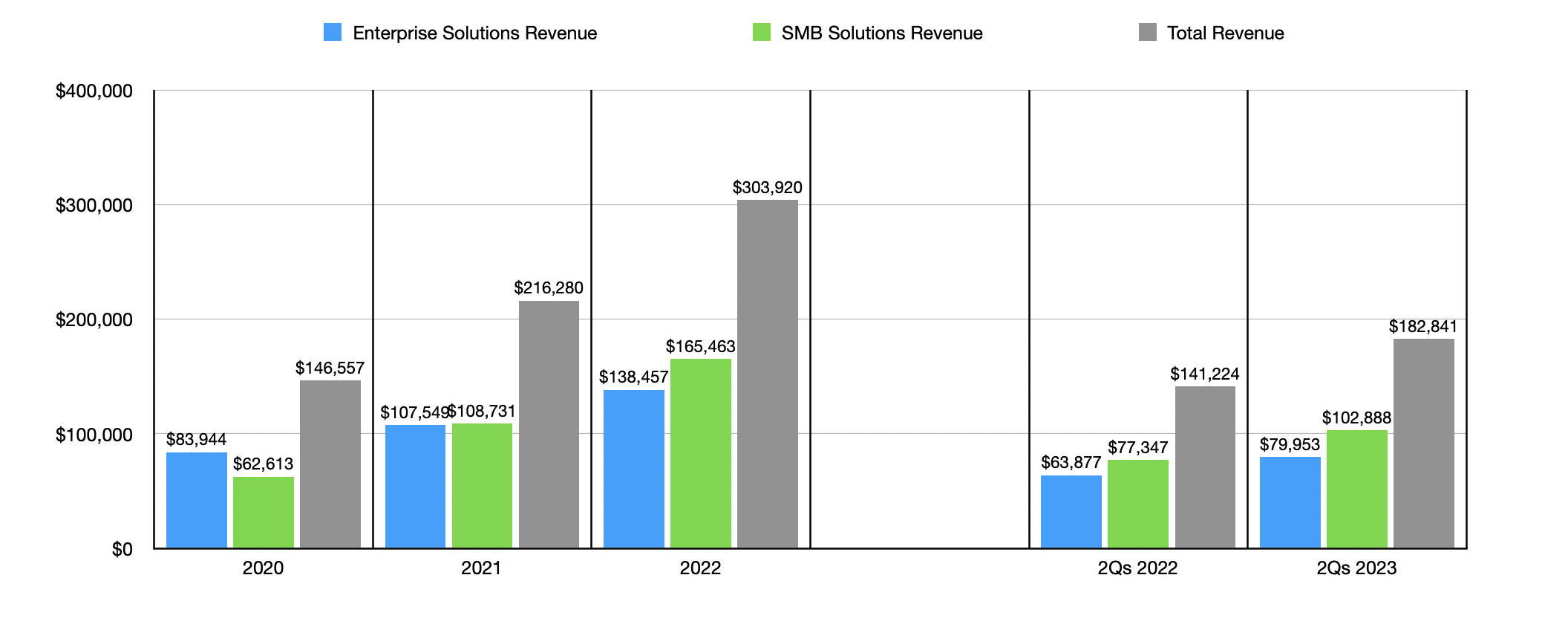

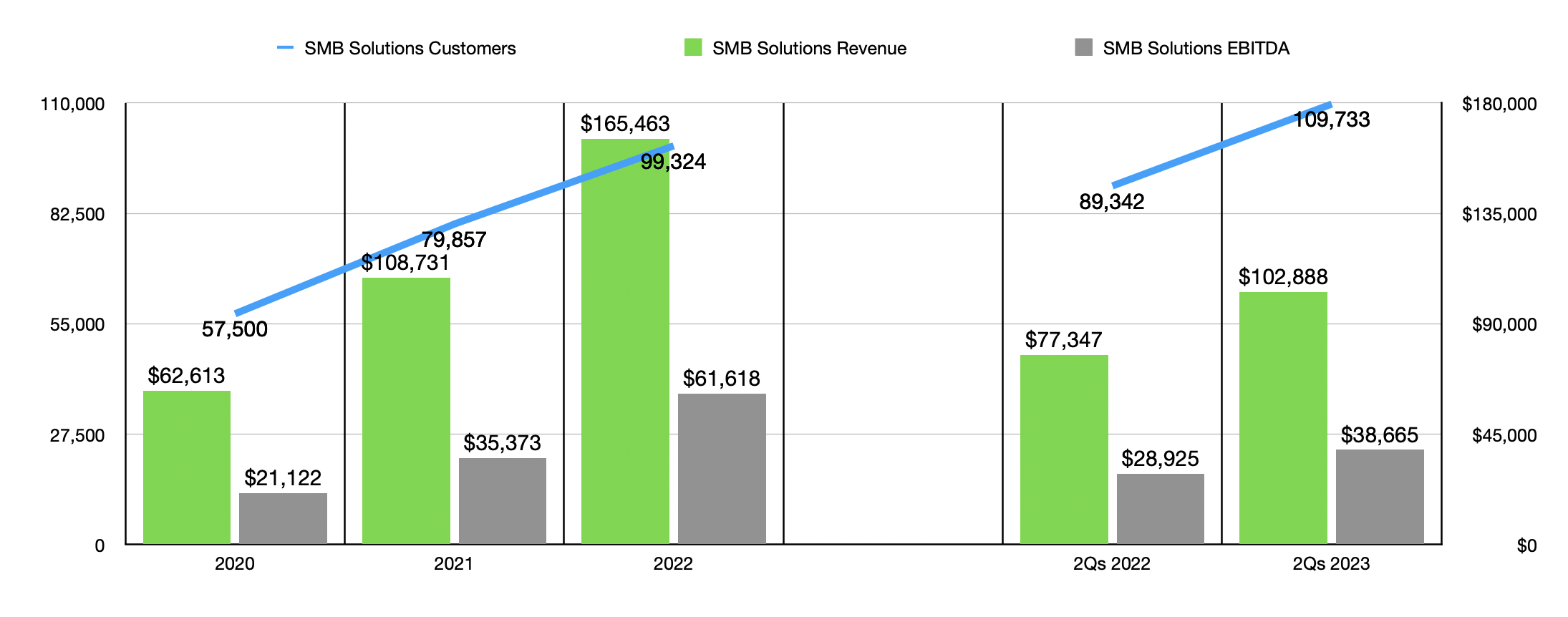

Over the past few years , the management team at EngageSmart has done a really great job. Revenue has grown from about $109 million in 2020 to $303.9 million in 2022. Both of the operating segments expanded nicely during this time. But beyond any doubt, the greatest expansion came from the SMB Solutions business. Revenue almost tripled from $62.6 million to $165.5 million during that window of time. This growth was driven by a surge in customer count from 57,500 to 99,324.

{kind=link}

{kind=link}

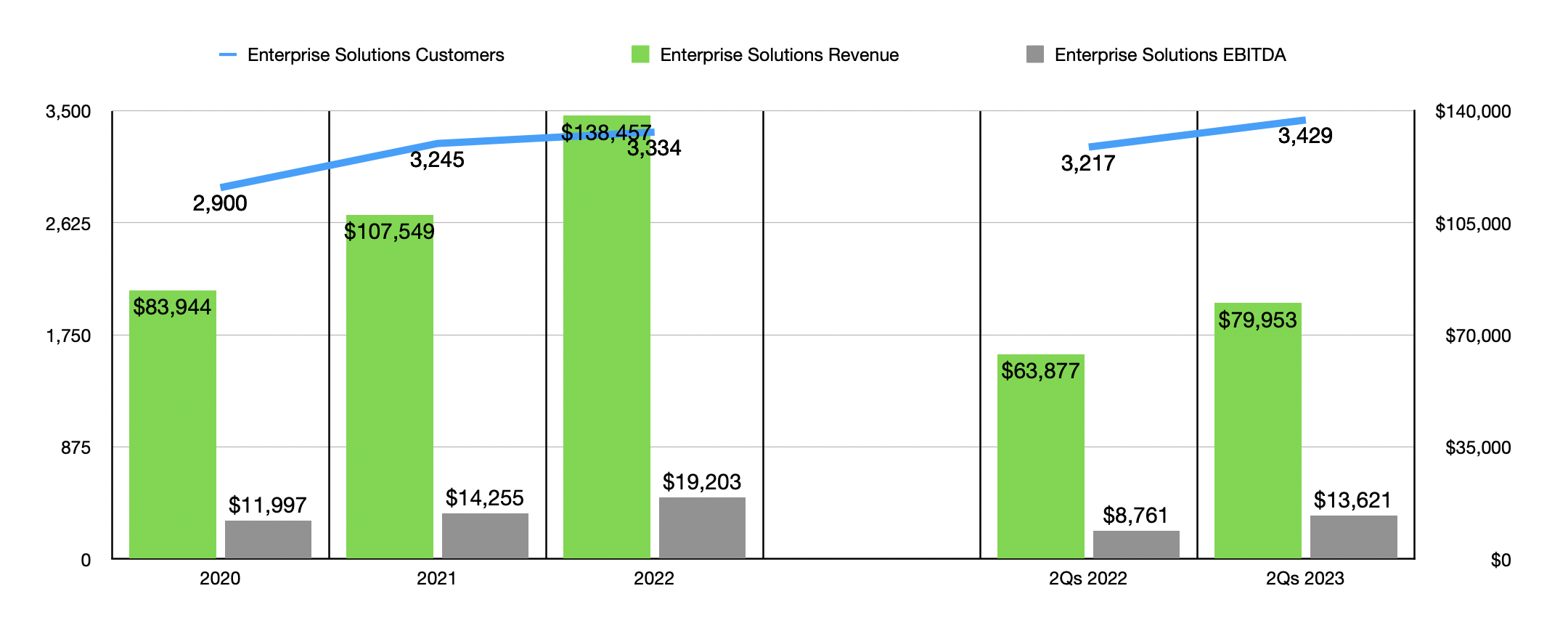

Higher pricing also contributed to expansion during this window of time. This is not to say that the Enterprise Solutions business did not do its share of heavy lifting. It definitely did. From 2020 through 2022, revenue jumped from $83.9 million to $138.5 million. Interestingly, the number of customers increased only modestly from 2,900 to 3,334. Rather, it was greater utilization that really drove revenue growth here. A key part of the company's revenue involves the number of transactions such as credit and debit card transactions, ACH payments, and other types, that its platform handles. This was a huge driver of revenue growth over the past three years, with the number of transactions completed growing from 79.4 million to 146.8 million.

{kind=link}

{kind=link}

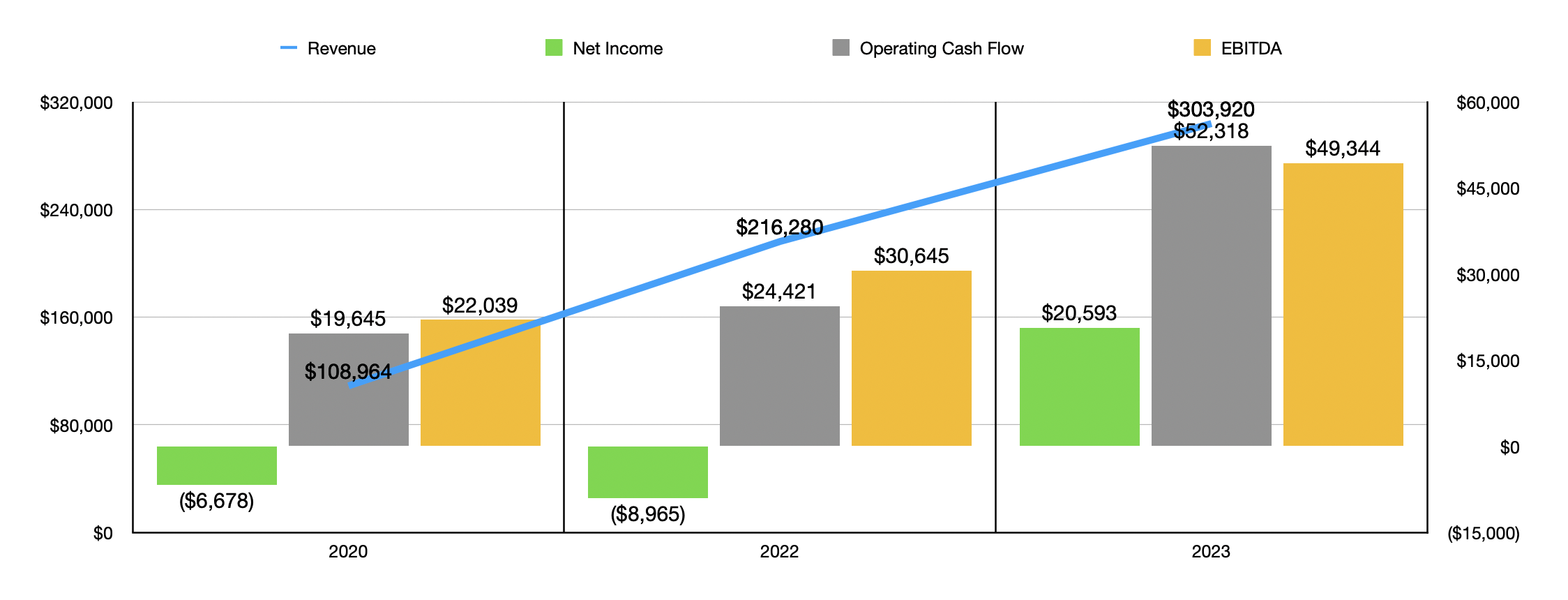

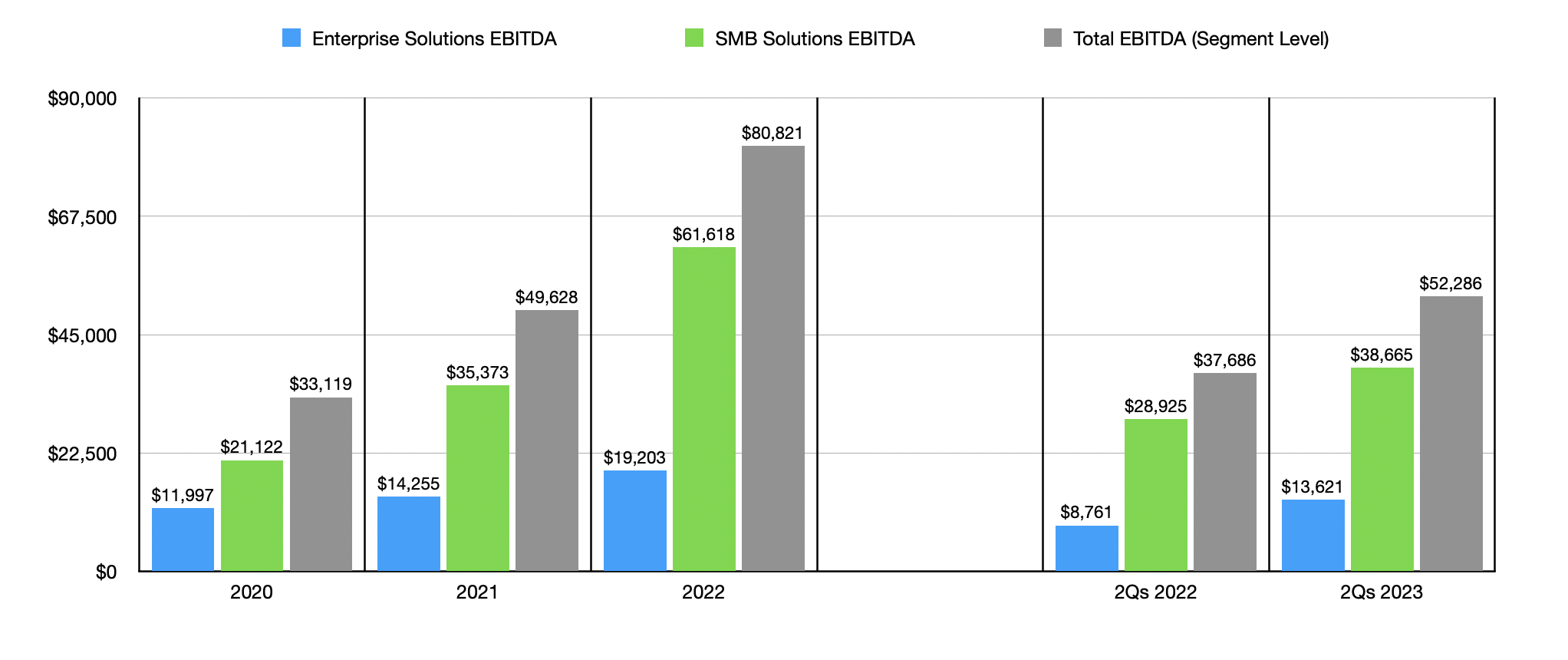

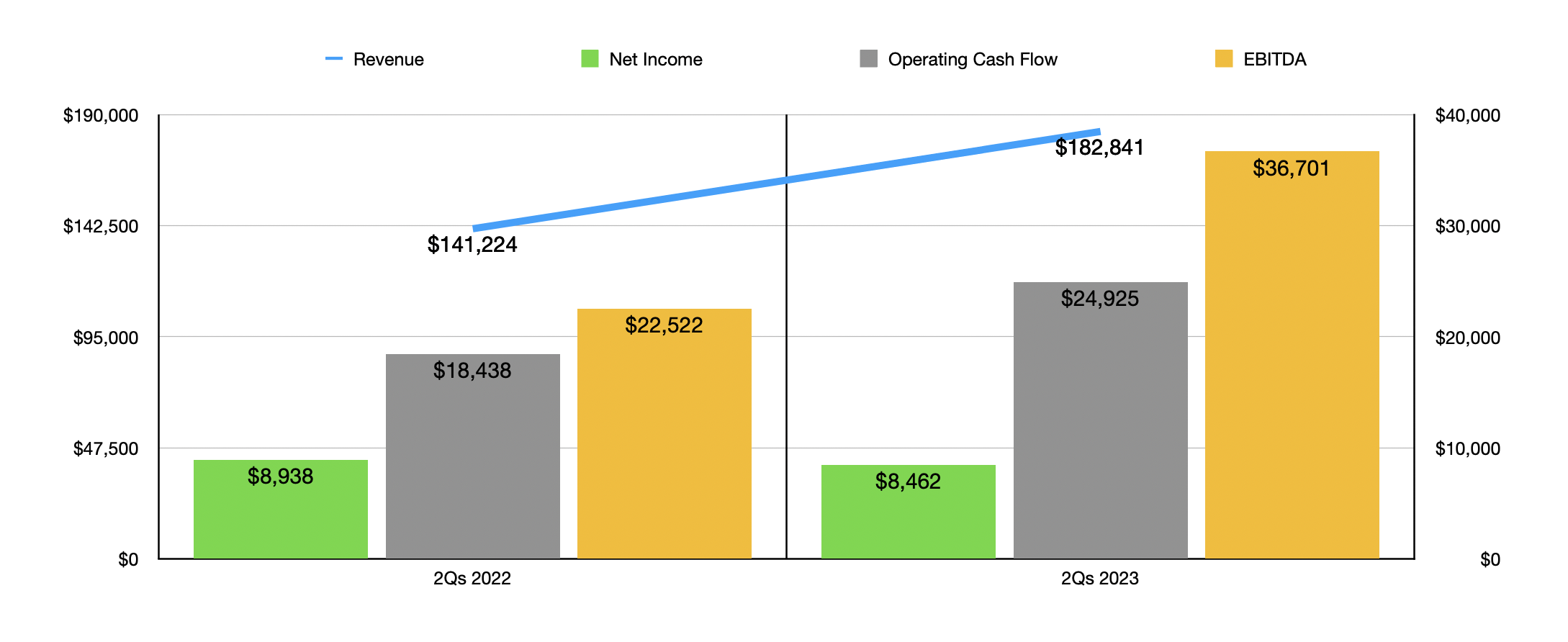

Profitability has also come in strong. The company went from generating a net loss of $6.7 million in 2020 to generating a profit of $20.6 million last year. Operating cash flow well more than doubled from $19.6 million to $52.3 million. Meanwhile, EBITDA for the company expanded from $22 million to $49.3 million. As you can see in the chart below, financial performance for the business continued to come in strong this year. Revenue in the first half of the year was 29.5% higher than it was last year. Growth occurred across both segments, with the SMB Solutions segment once again leading the way. And by the end of the most recent quarter, the company had a total of 113,162 customers on its platform.

{kind=link}

{kind=link}

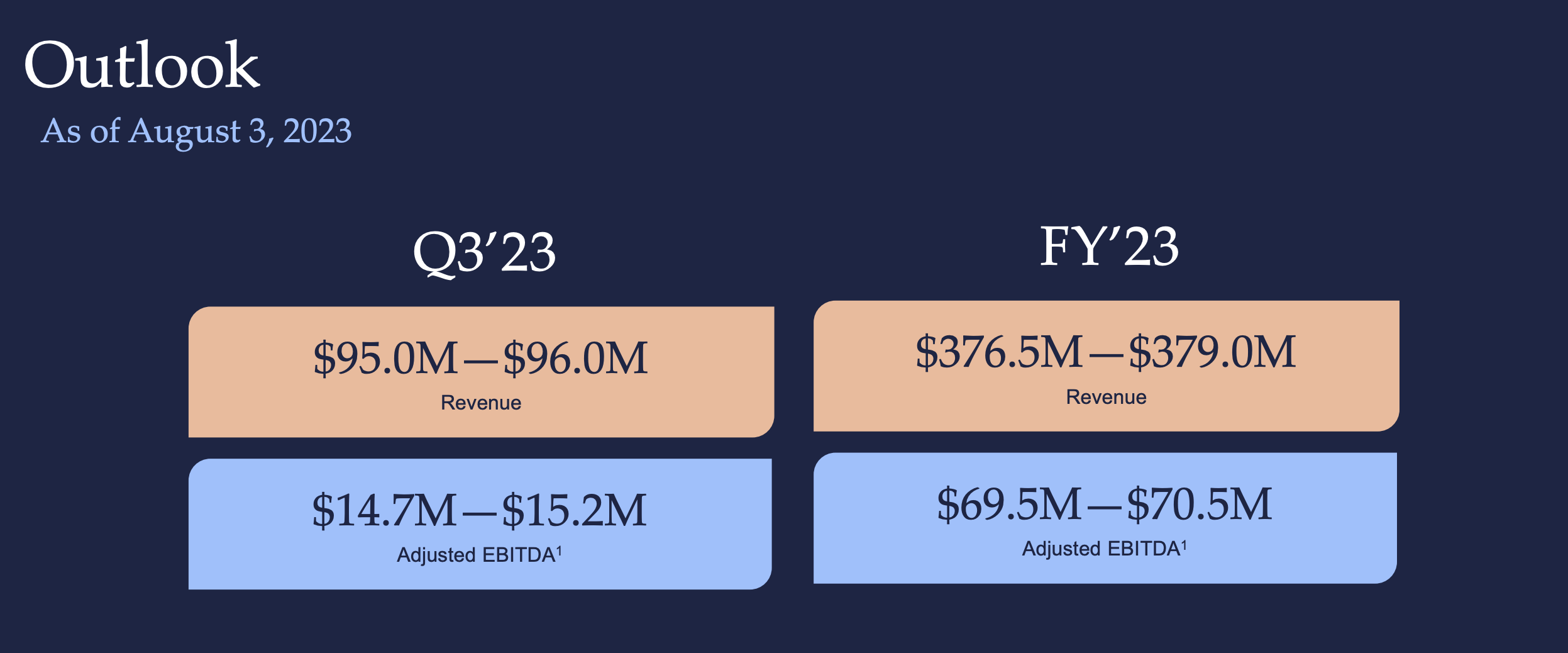

One of the really exciting things about EngageSmart is the fact that management was predicting continued revenue growth throughout the rest of this year. At the midpoint, guidance called for sales of $377.8 million. That would represent an increase of 24.3% over what the company achieved in 2022. Profitability was expected to soar, coming in at around $70 million for EBITDA compared to the $49.3 million generated last year. And the company has no debt and it enjoys a surplus of cash.

{kind=link}

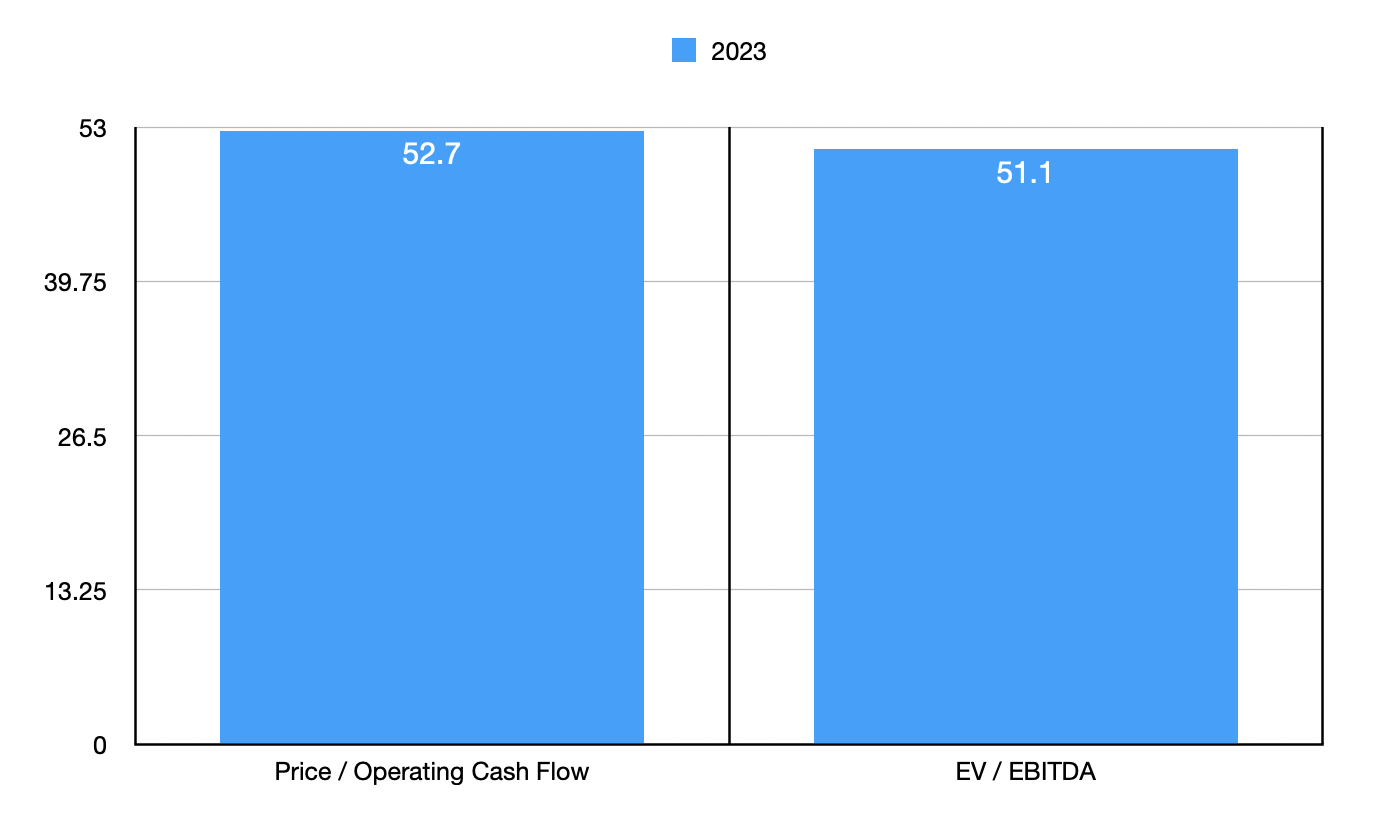

A case could be made that the transaction makes sense because shares are not exactly cheap. Honestly, I wouldn't expect them to be cheap. Using the forward estimates for 2023, the firm has agreed to be sold out at a price to operating cash flow multiple of 52.7 and at an EV to EBITDA multiple of 51.1. In the table below, you can see some comparison to five similar firms. But given the extreme disparities in how they are valued, I don't think this adds a lot of insight. Using the price to operating cash flow approach, for instance, four of the five companies were cheaper than EngageSmart. But using the EV to EBITDA approach, only one of the four with positive readings looks cheaper.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| EngageSmart |

| 52.7 |

| 51.1 |

| Box ( BOX ) |

| 11.6 |

| 36.8 |

| Pegasystems ( PEGA ) |

| 22.7 |

| N/A |

| Vertex ( VERX ) |

| 51.4 |

| 72.2 |

| BlackLine ( BL ) |

| 33.8 |

| 52.8 |

| Sprinklr ( CXM ) |

| 63.0 |

| 303.3 |

Instead of focusing too much on relative valuation, I would say that the absolute value of the company is more reasonable to emphasize. But as you can see, that is a very high trading multiple. As a value investor and somebody who, in general, tries to stay away from growth unless it can be purchased at an attractive price, I would normally be the first person to applaud this transaction. But something doesn't sit right with me. For starters, the rapid growth and positive earnings and cash flows, particularly at how small the company is, makes me believe that further upside exists around the corner. But there's also management's own claims that makes this a difficult circle to square.

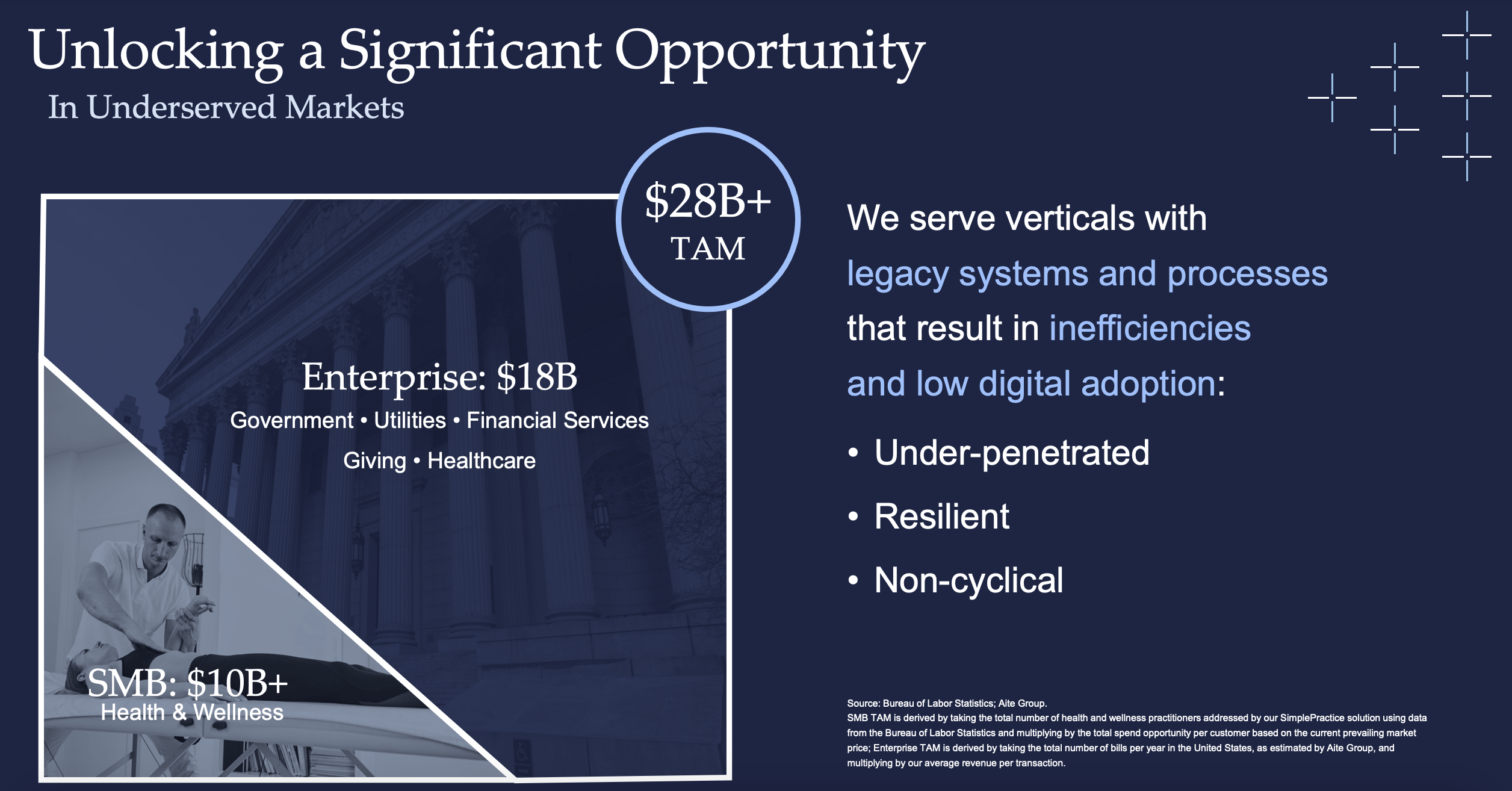

For starters, there is the issue of overall market opportunity. Management has made it a priority to focus on key markets. The Enterprise Solutions segment, for instance, focuses only on government entities, utilities, financial services, charitable organizations, and the health care sector. Combined, they view this as an $18 billion market. And the SMB Solutions segment prioritizes the health and wellness market, which management pegs at $10 billion or more. Although management has not provided any growth estimates for these markets in the years to come, they did state in their most recent annual report that

"our verticals are large, under penetrated, and generally non-cyclical with significant whitespace, low digital adoption, and growing usage of software and payments. Many verticals are only just beginning their digital journeys, providing an attractive runway for growth."

To see an enterprise that's growing rapidly, that has achieved profitability and positive cash flows, that operates in a sizable market, and that believes wholeheartedly that strong prospects exist around the corner, I find selling out, even at the price paid, peculiar.

{kind=link}

This feeling is further complicated by the fact that not everybody is going to be forced to unload their ownership. Everybody who owns publicly traded shares outside of one certain party will be forced to unload their shares. That party is General Atlantic, which is a global investment company that has around $77 billion in assets. As of the end of 2022, it owned a 59% stake in EngageSmart. By the time the transaction was announced, this ownership had dipped slightly to 52%. It is selling some of its ownership in this deal. However, it will retain a 35% stake in the combined company despite the fact that it is not an acquirer. To see the majority shareholder of a rapidly growing company divest only a sizable portion of its majority stake is uncommon and it is uncomfortable knowing that they will continue to benefit from the company's growth moving forward.

Takeaway

As things stand, EngageSmart is going to be coming off the market. I don't think anything will change that. To some investors, this may seem like a great move. And at the end of the day, it could be. I'm not terribly enthusiastic about the deal, and I believe that the circumstances surrounding it are unfortunate for investors. As for current shareholders, I don't really see much reason to retain ownership at this time. The spread between the buyout price and where shares are now indicates further upside of only 1.7%. And that's a pretty small spread when you consider that the deal is going to close sometime in the first quarter of next year.

Because of this, I have decided to rate EngageSmart, Inc. a "hold" for now. But the main reason for that rating has less to do with the modest upside and more to do with the fact that there is still a small chance of a better deal coming through. That is because the company has a 30-day go shop period that will expire at midnight on November 22nd. If nothing materializes at that point, I would consider this a "sell" since there are better places to allocate capital from that point on.

For further details see:

The EngageSmart Buyout Doesn't Feel Right