ENSG - The Ensign Group: Screams Quality Resiliency Rated Highly For Equity Portfolios

Summary

- The Ensign Group continues expanding tangible measures of value following its Q2 FY22 earnings.

- Measures of corporate value are attractive in this name even after reconciling GAAP earnings.

- Valuations are equally as supportive and we feel shares are fairly priced at $100 apiece.

- With return on invested capital and forward earnings conducive to further upside capture, we rate ENSG a buy.

Investment Summary

Examining measures of corporate value has become evermore paramount in the forward looking climate. Understanding the highest quality business models will help equity positioning and enable investors to climb up the resiliency spectrum to protect equity returns.

We turn to The Ensign Group, Inc. ( ENSG ) and demonstrate the strengths in its operating model and that valuations are supportive of further upside capture. After reconciling GAAP results to extract true value, we note that both investment and earnings characteristics of ENSG place it near the top of the mantlepiece in service-based healthcare. We feel ENSG is positioned perfectly within its current capital budgeting cycle to deliver further shareholder returns and add a layer of resiliency to equity portfolios. Rate buy on $100 per share valuation.

Exhibit 1. ENSG 6-month price action

{kind=link}

Data: Refinitiv Eikon

Q2 earnings exhibit further upside capture

Second quarter earnings came in strong with upsides relative to consensus at the top and bottom line. Revenue of $732.4 million grew 14.7% YoY and was underscored by a 14% YoY growth in service revenue. Overall revenue was driven by an increase in total patient days and occupancy rates from skilled operations, coupled with revenue accretion from acquisitions. Consolidated occupancy rates gained 250bps YoY as the case mix shifted away from Covid-19/Medicare cases to long-term care patients.

Meanwhile, new acquisitions [subsequent to 1 Jan FY21] increased ~$35.5 million over the 12 months to $56 million. As seen in Exhibit 2, transposed from ENSG's Q2 FY22 10-Q, each transaction added another ~$4 million in revenue per acquisition, and another 16,445 patient days on average. This saw occupancy rise by 6.3 percentage points to 71.2%. Standard Bearer added another 6 sites [to be leased to ENSG on affiliate basis], whereas ENSG itself entered into another 7 long-term leases with 3rd parties. At present, Standard Bearer is now made up of 101 owned properties, and 73 are leased to affiliates whereas the other 29 are leased to the Pennant Group.

Rental income derived from these properties delivered $17.6 million for the quarter and $12.1 million in funds from operations ("FFO"). Importantly, ENSG's realized Medicaid rates also spiked 480bps YoY backed by state reimbursement and Medicaid payment programs.

Exhibit 2. New acquisitions [post-Jan FY21] have been accretive to the top and bottom lines

Data: ENSG 10-Q Q2 FY22

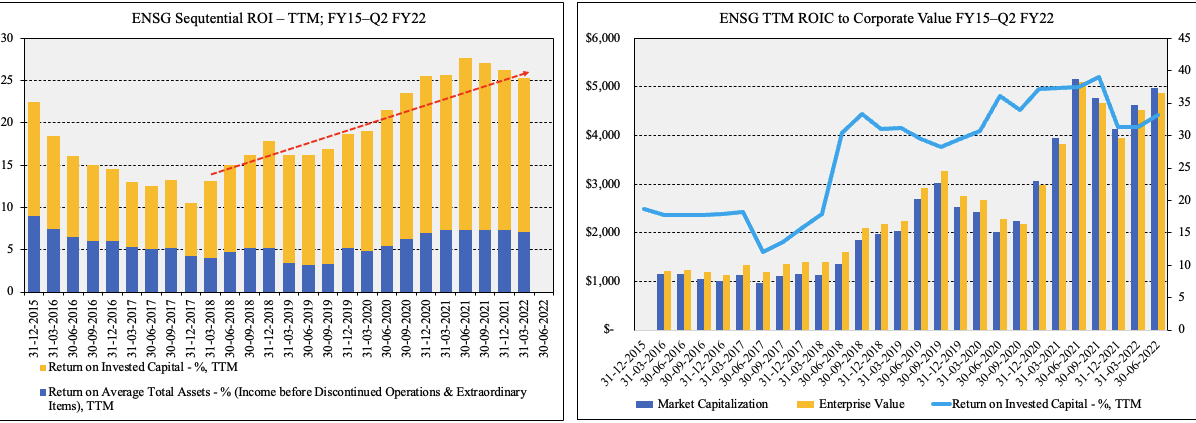

In this vein, we note that quarterly operating performance has been a standout for the company since FY15–date. As seen in Exhibit 3, both revenue and gross profit have grown sequentially, whilst operating profit has remained equally as robust.

The result has been consistent growth of FCF whilst FCF yield has remained cyclical in-line with the company's capital budgeting cycle. It printed FCF of $62 million [$1.18/share] for the quarter, and we forecast FY22 FCF of $148 million [$2.70/share]. Noteworthy however, is that it bought back $20 million of its own stock during the quarter, and debt increased by 35% or $41 million YoY. Stock-based compensation ("SBC") was also $10.8 million for the quarter.

Nevertheless, profitability is therefore a standout for the company [discussed later] and net-net, ENSG's efforts see it compound cash in the double-digits on an annual basis. This is an attractive feature and separates ENSG from many other names operating with a revenue mix split between service and rental income. It is equally as attractive heading into the forward looking economic climate.

This fundamental momentum heading into FY22 full has prompted ENSG management to raise FY22 guidance by ~12% at the upper bound, calling for $2.96–$3 billion in revenue for this year. It also forecasts GAAP earnings of $4.05–$4.15 per share.

Exhibit 3. Quarterly operating performance continues to walk higher on a sequential basis

Meanwhile, FCF yields continue to cyclically head north, demonstrating the quality in ENSG's business model.

Data: HB Insights, ENSG SEC Filings

Long-term cash compounder

Our findings also demonstrate that ENSG is a long-term cash compounder that provides investors real-return in the form of net operating profit after tax ("NOPAT"), return on investment ("ROIC") and FCF. These measures of ENSG's continuing value are essential in understanding just exactly what we are buying in ENSG, in terms of tangible value and future cash flows.

As seen in Exhibit 4, the company has embarked on a cyclical ROIC schedule that has grown to record highs on a TTM basis. The buoyancy of ENSG's return on investment has also been accretive to market value, with changes in ROIC explaining ~57% of the changes in its market capitalization [RSQ = 0.57].

Exhibit 4. Quarterly return on investment [TTM] for ENSG continues to cyclically shift higher on a sequential basis

ROIC has been equally as accretive to the company's market value from FY15–date.

{kind=link}

Data: HB Insights, ENSG SEC Filings

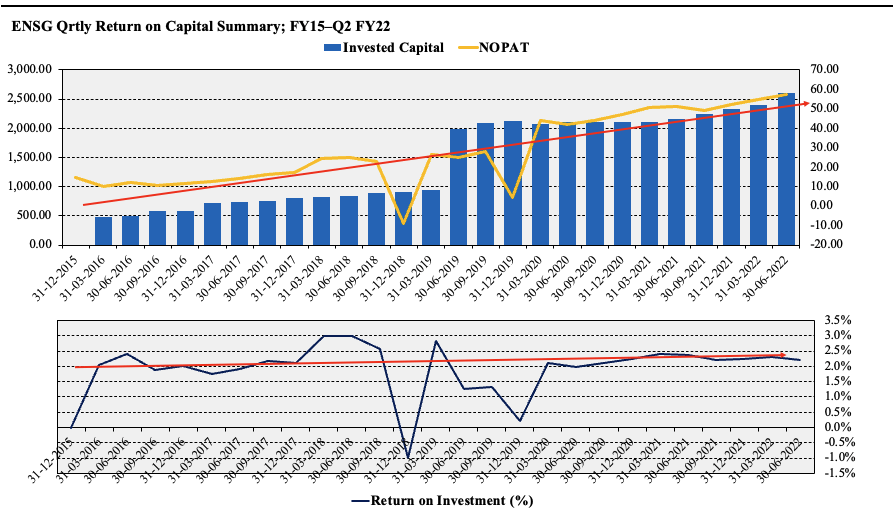

This data is supported by quarterly ROIC measures as seen in Exhibit 5, illustrating how quarterly NOPAT shifts higher from the previous period's invested capital on a sequential basis. TTM NOPAT earnings per share [NOPAT EPS] totals $3.88 for Q2 FY22 and this adjusts to $4.30 in NOPAT EPS after making the necessary reconciliations from GAAP earnings [discussed later].

Nevertheless, these are more than attractive features in the company's investment debate and have us trigger heavy on the name. It compounds capital at a TTM 18.2% and annualized 9.09% from Q2 FY22's result, well above the WACC of 7.56%, meaning return on investment comfortably covers the cost of capital by 1.2–2.4 turns. The size of ENSG's ROIC exhibits it has a low capital intensity when compared to ROIC and cash earnings. We envision these trends to continue based on Q2 earnings macroeconomic conditions.

Exhibit 5. Quarterly NOPAT return on investment continues to exhibit resiliency

In all instances, ROIC [TTM, quarterly and annualized] comfortably surpasses ENSG's cost of capital and therefore creates a cash-compounding machine for the long-term.

{kind=link}

Data: HB Insights

Reconciliations to extract true value

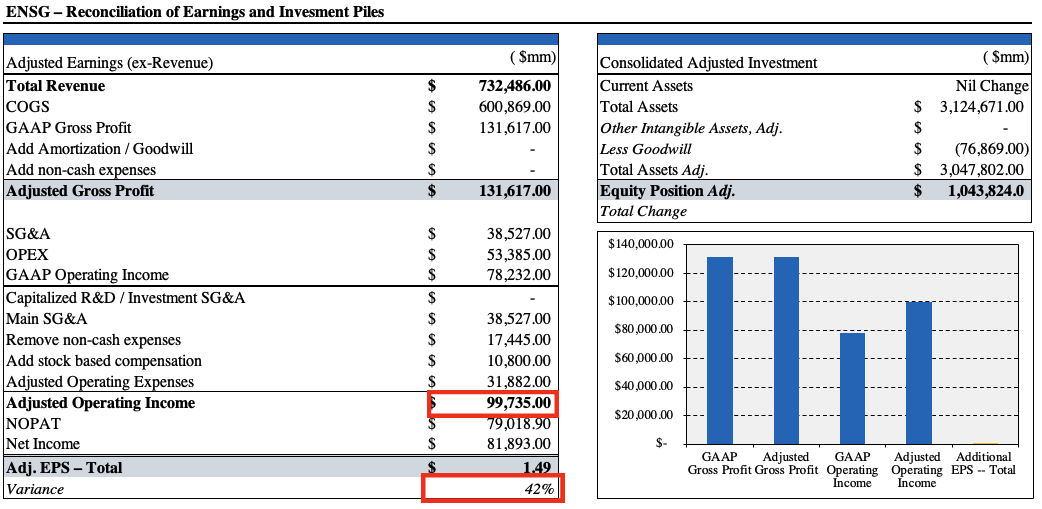

We've made several reconciliations to GAAP reporting to gauge a more accurate snapshot of corporate value for ENSG, to see how much we are paying, and understand exactly what we're paying for (Exhibit 6). After adjusting non-cash expenses and adding stock based compensation of ~$11 million we observe non-GAAP operating profit lift to $99.7 million, that carries down to a 42% increase in EPS to $1.49.

Meanwhile, post-acquisitions to date, the company records a $76.8 million goodwill impairment on the balance sheet. Depending on how one treats goodwill – a non-cash, non-amortizable, non-tangible asset – this has substantial impacts on measures of corporate value and to the price we'd theoretically be paying.

Exhibit 6.

{kind=link}

Data: HB Insights US Equity Fund

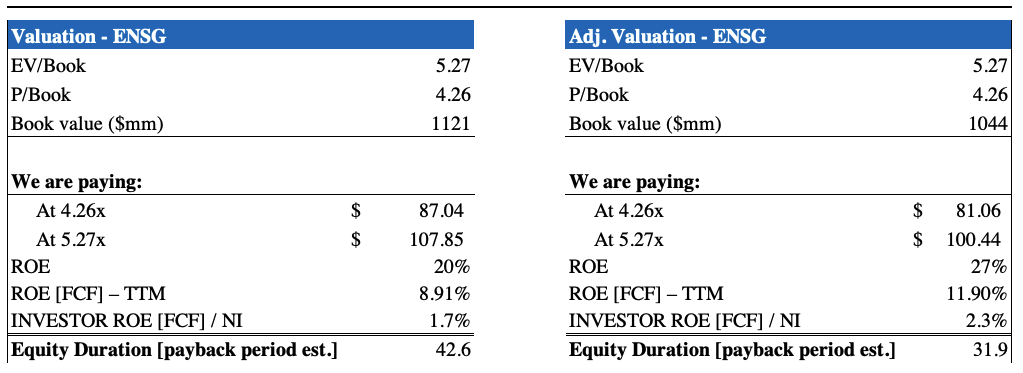

As seen above, adjusting for goodwill reduces shareholder equity to $1.04 billion, down from $1.12 billion reported. Shares currently trade at ~4.3x book value and at nearly 5.3x enterprise value ("EV") to book value of equity. On GAAP values, we'd be paying an implied $87–$107, depending on which measure used. Post adjustment, the implied paying price shifts to $81–$100 per share. Noting that corporate value is made up of investment and earnings, ENSG's double-digit ROIC is a bullish weight to the valuation debate.

Exhibit 7. Measures of investment/book value change drastically with post-adjustment figures

{kind=link}

Data: HB insights Estimates

Valuation

We've acknowledged that shares are potentially valued at a premium on 4.3–5.3x book value, as seen above. The question then turns to if this multiple is worth it based on what's expected. Below is our valuation model that looks at continuing value as measured by earnings. It looks at a range of estimates that cover a breadth of empirical drivers, ranging from fair value estimates, market consensus forward multiples and historical/normalized performances.

Adjusting the equity risk premium [earnings yield minus real risk-free rate] to reflect the fair cost of equity suggests shares are overvalued. As a full picture, however, shares look to be fairly priced at ~$100, with generous contribution from consensus forward P/E and normalized P/E inputs.

Exhibit 8.

Data: HB Insights US Equity Fund. Image: HB Insights

In this case, there is a range of value to be considered, depending on use of EV of market cap in the calculation. Paying $81–$87 to receive 14–23% upside [$13–$20 per share] is arguably a valuable proposition for the next 12 months. Paying $100–$107 to receive $100, not really so. Moreover, is the present value of returns greater than the cost? If judging by the cost of equity above – then yes, absolutely. If using market price of ~$84, then not so much.

Regardless, there is a serious case for further upside capture based on measures of corporate and market value for ENSG. With these points in mind, we rate ENSG a buy with a $100 per share valuation.

For further details see:

The Ensign Group: Screams Quality, Resiliency, Rated Highly For Equity Portfolios