VNO - The Fall Of Office REITs

2023-05-22 07:00:00 ET

Summary

- When the oppression of the pandemic on labor became too much to bear, laborers revolted; remote work's convenience and flexibility have created an office exodus.

- Berkshire Hathaway Vice Chairman Charlie Munger said, “A lot of real estate isn’t so good anymore…We have a lot of troubled office buildings.”.

- The banking crisis raises concerns about REITs’ ability to meet financial obligations, and Real Estate (XLRE) has been the worst-performing sector over the last year, down more than 13%.

- A tight labor market, massively revised office rental rates, rising interest rates, and painfully slow return to office have led to a major downside for some companies and office REITs. Using Seeking Alpha’s Quant System and Factor Grades, I highlight three sell-rated office REIT stocks suffering from bearish momentum, poor growth, and downward analyst earnings revisions.

The Downfall of Commercial Office Real Estate

The U.S. commercial real estate market is feeling pressure from the pandemic, inflation, rising interest rates, and a banking crisis that could lead to a potential regional banking debacle. For the first time since 2011, U.S. commercial real estate experienced a decline in the first quarter, citing banking industry chaos and the risk of more volatility in the financial sector. Although the decline was less than 1% and led by office buildings and multifamily residences, many companies have been reeling from an exodus from commercial spaces. Long-time investor and Vice Chairman of Berkshire Hathaway Charlie Munger told Financial Times ,

“A lot of real estate isn't so good anymore…It’s not nearly as bad as it was in 2008…We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There's a lot of agony out there."

When you factor in the convenience and flexibility of remote work environments challenging in-office work, many metro restaurants and businesses shut their doors as their customer number fell. Employees are saving in commute times and work-related costs, and with the expectation of further declines, the once top-performing sector in 2021 is now the worst, raising credit crunch and tenant risk concerns. Morningstar senior portfolio manager Bianca Rose says ,

“There’s a difference between ‘interest rates are rising, my costs will go up, but I can access funding’ versus ‘you just can’t have the funding,” And now that lower interest rates appear a thing of the past, “what happens if all these businesses that were doing well from easy money now go bust? They’re tenants to someone.”

This article is focused on avoiding office REITs. This is not a declaration on all REITs. Traditionally, REITs typically give way to substantial yields and income streams and can provide capital appreciation if appropriately timed. As the third-largest asset class in the United States, REITs’ diversified blend of real estate assets can offer the following benefits:

-

Dividend Benefits

-

Inflation Protection

-

Competitive Long-Term Performance:

-

Portfolio Diversification

-

Liquidity

REITs have typically benefited from unexpected inflation, providing investors with a total return investment and some tax advantages, which is why its key to select Top REITs .

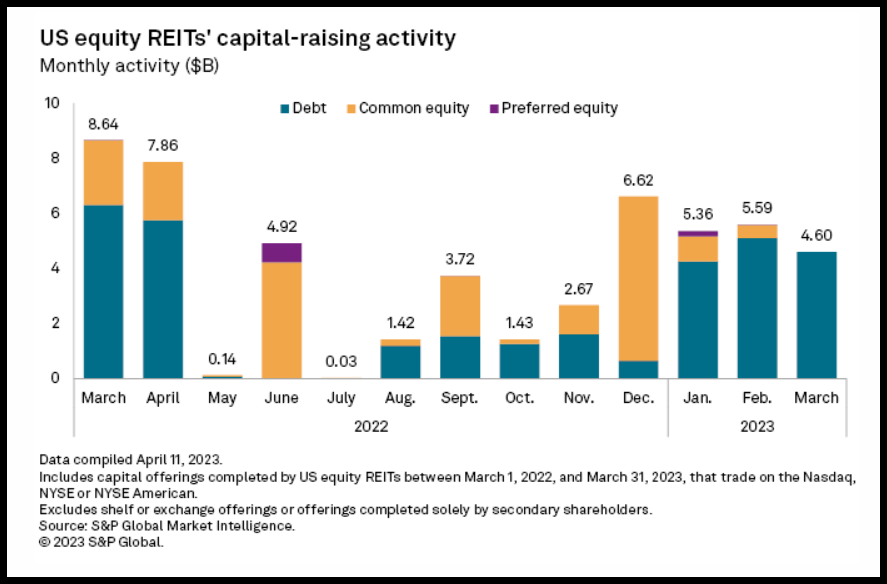

But as we’re seeing, the risks inherent in real estate, particularly the commercial–office segment – are being hit hard, as the effects from banking and inflation have caused dividend yields to fall; office REITs lost more than 40% of their value in 2022; and capital offerings are down 17% M/M and more than 50% Y/Y.

US capital offerings are down (S&P Global Market Intelligence)

{kind=link}

With capital raising decreasing by nearly 71% in the first quarter and many of the metropolitan cities experiencing muted demand, while higher quality assets continue to experience stronger, global vacancies have experienced the largest rise recorded in North America of 15.3% for Q1, according to JLL, global commercial real estate company. As uncertainty looms and a slowdown in economic growth and activity persists, there are many office REITs to reconsider as investments in 2023.

REIT Stocks To Avoid in 2023

REITs tend to be highly leveraged, and the Fed’s stance on taming inflation and reducing its balance sheet has created significant fear of financial instability. Where fears of the economic state are widespread, expectations of recession, continued geopolitical factors that include energy prices, Russia, Ukraine, and China symptoms will likely create more volatility. The three REIT stocks I’m covering today showcase the current ugly side of the industry. The stocks not only face a poor macroeconomic backdrop but possess a poor showing of collective metrics on growth, profitability, momentum, and analyst revising estimates down.

1. Paramount Group, Inc. ( PGRE )

-

Market Capitalization: $1.01B

-

Dividend Yield ((FWD)): 7.14%

-

P/FFO ((FWD)): 4.76

-

Quant Rating: Sell

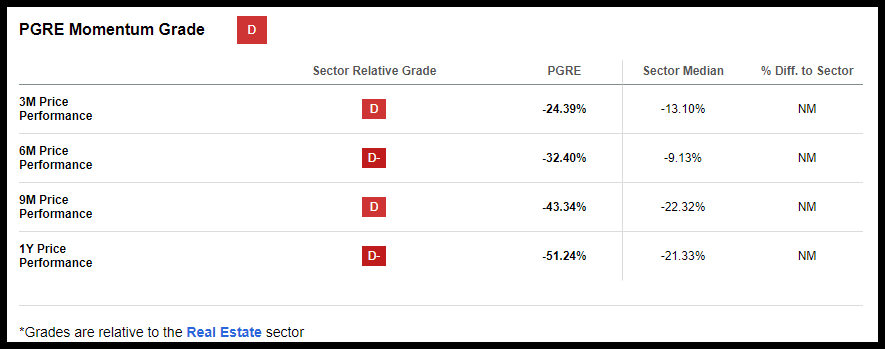

New York City-based Paramount Group, Inc. is the renowned landlord of choice, focused on high-quality tenants in some of the largest financial, legal, and professional services industries. With tenants in the central business district submarkets of NYC and San Francisco, fire sales and the woes of a potential “doom cycle” are accelerating as city centers turned ghost towns put a financial strain on office REITs. Showcasing characteristics, which have historically been associated with poor future stock performance, PGRE’s sell warning comes from decelerating momentum and negative EPS revisions.

PGRE Stock Valuation & Momentum

Paramount Group is trading near its 52-week low, -24% YTD, and down nearly 50% over the last year. Although this sell-rated stock looks cheap and possesses a forward P/AFFO of 8.68x compared to the sector 14.09x, it is at high risk of performing worse.

PGRE Stock Momentum (SA Premium)

{kind=link}

Although undervalued, the stock is on a longer-term downtrend, as evidenced by the momentum performance . Trading below the 200-day moving average, gradual decelerating momentum from a six-month price performance of -32.40% to a nine-month of -43.34% and falling is a key aspect for its fall in sector and industry ranking. The continued weakness of office space, which includes its largest market, New York, which comprises over 70% of its business, near-term tenancy risk poses headwinds for the company, whose growth figures are already suffering.

PGRE Stock Growth & Profitability

With solid Q1 2023 earnings , Paramount Group raised full-year 2023 guidance following an FFO of $0.26, beating by $0.03, and revenue of $188.47M beating by $7.25M. And while their New York portfolio of buildings and leases continues to perform well, with +90% leased, PGRE’s west coast properties in San Francisco are another story.

Occupying a 460,726 square foot space in the financial district of San Francisco, First Republic Bank, which accounts for an approximately $43 million or 6.4% annualized rent share, remains a tenant of the space. Providing a ~$3.5M per month GAAP rental revenue.

“On May 1, FDIC took control of First Republic, and JPMorgan Chase subsequently acquired the majority of the assets. Many of the details regarding the transaction remain unknown. To date, First Republic remains current on its rent payments, and its offices remain open, but we are watching this closely as I’m sure all of you are,” said Albert Behler, President & CEO of Paramount Group.

First Republic remains current on its rent and has indicated plans to continue to honor its obligations under the lease agreement. Overall, leasing activity in San Francisco is muted amid tight economic conditions contributing to higher vacancies.

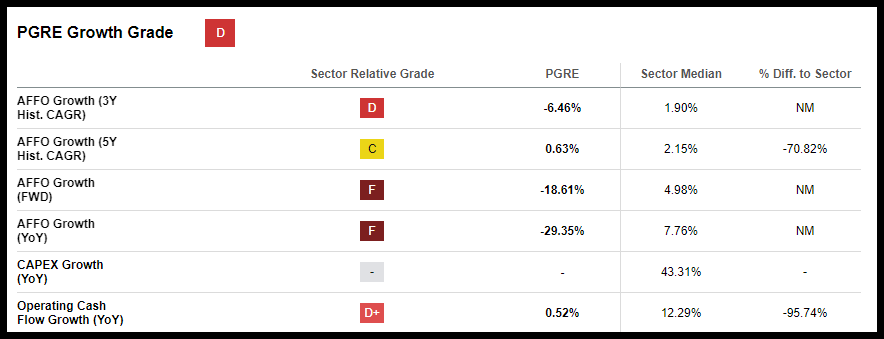

PGRE Stock has poor growth

PGRE Stock has poor growth (SA Premium)

{kind=link}

While PGRE’s San Francisco portfolio is 88.7% leased, it’s still down 20 basis points quarter-over-quarter, and the company has sizable lease expirations approaching, which include tenants like Uber and Credit Agricole. With more than $200M near-term maturities in 2023 and +$478M maturing in 2024, and AFFO/Total Revenue ((TTM)) that’s a -61% difference to the sector, it's surprising that its management remains so optimistic about guidance, that it would increase. Despite increasing its Core FFO guidance between $0.90 and $0.94 per share, this high-quality landlord should consider further de-risking given the challenging outlook, as this sell-rated stock is likely to experience more headwinds, along with the next stock, Brandywine Realty Trust.

2. Brandywine Realty Trust ( BDN )

-

Market Capitalization: $629.37M

-

Dividend Yield ((FWD)): 20.88%

-

P/FFO ((FWD)): 3.20

-

Quant Rating: Sell

Where Paramount Group focuses on high-quality assets, Brandywine Realty Trust is one of the biggest full-service real estate companies in the U.S., focused on urban, town center, and transit-oriented properties.

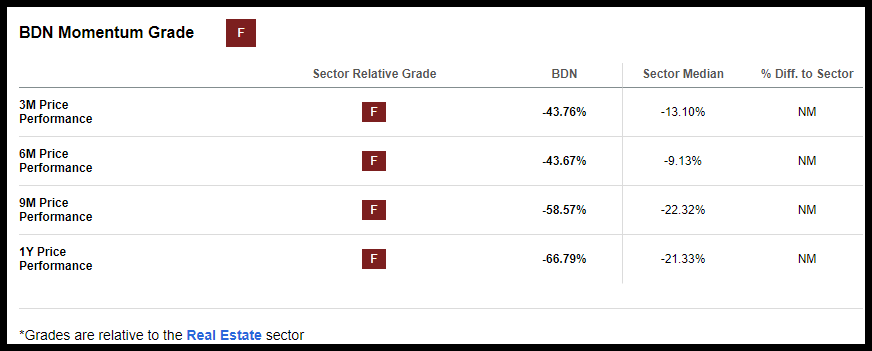

With a portfolio of more than 163 properties contributing to its whopping 20.82% forward dividend yield, the company is at high risk of performing poorly. Not only is its dividend safety a D+, an indicator that it may be cut in the future, but decelerating momentum and declining growth when compared to other Real Estate stocks indicate why this stock is rated a sell. Despite its A+ valuation, which includes a forward P/AFFO at a 66.71% discount to the sector, its Momentum Grade is an ‘F.’

BDN Stock Momentum Grade (SA Premium)

{kind=link}

Brandywine is -42% year-to-date; over the last year, it is down more than 66%. The one-year price performance for the sector median is only 21%, and when you compare the figures for each quarter, it should be no surprise that BDN is trading under $4/share, near its 52-week range. With the difficult capital market conditions, BDN has expressed efforts to address their overall liquidity, refinance two non-recourse loans that will mature in 2023, and focus on tenant demand drivers. Although the company indicates a strong pipeline and earnings have been flat over the last two quarters, Brandywine’s D+ growth and underwhelming profits may face greater challenges.

BDN Stock Growth & Profitability

Despite Q4 2022 leasing volumes that include 226,000 square feet of signups and Q1 2023 FFO of $0.29 in-line with expectations, revenue of $129.23M beat by $2.15M. Brandywine’s shares remain down over the last year. Default by a large Austin tenant, lower occupancy levels, and concerns about the banking crisis causing stricter processes and a credit crunch could affect BDN’s growth.

“There’s a general credit crunch on commercial real estate, and that the issue is systemic, not specific, and how they deal with that will be within their own investment committees. But our approach is to get these loans extended, get them restructured for a capital structure that provides an opportunity for both the borrower and the lender to win. And we’ll see how that works its way through the process,” said Gerard Sweeney , BDN President & CEO.

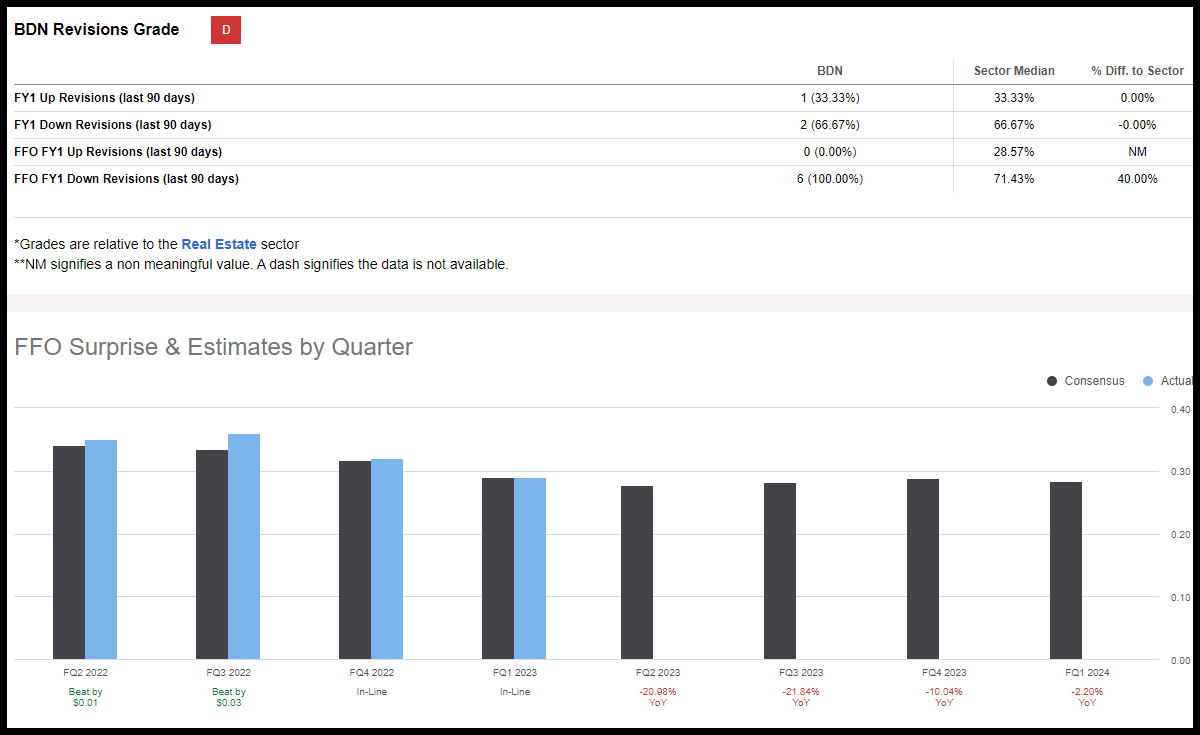

And while BDN has a leasing pipeline in Austin of 538,00 square feet, many of the larger tenants have pulled back, which has prompted some increases in subleasing, as other tenants in developing their commercial spaces put construction on hold. While BDN hopes to limit its downside risk and has bolstered its liquidity by executing a $70M unsecured term loan, and the company has no consolidated debt maturities until October 2024, six analysts revised FFO FY1 Down in the last 90 days.

BDN Revisions Grade (SA Premium)

{kind=link}

Forecasting sequential decreases due to higher interest expenses, refinancing, and shifts in banking and lending, Brandywine has its work cut out for itself in curtailing the fall of office spaces within its portfolio. Brandywine Realty is quant-rated a sell, but nothing spells concerns like top-and-bottom-line earnings miss and a strong sell rating.

3. Vornado Realty Trust ( VNO )

-

Market Capitalization: $2.7B

-

Dividend Yield ((FWD)): 10.90%

-

P/FFO ((FWD)): 5.18

-

Quant Rating: Strong Sell

I saved the worst for last! With the end of last week's earnings season, REITs finished down along with the broader market, despite REITs delivering strong Q1 results overall.

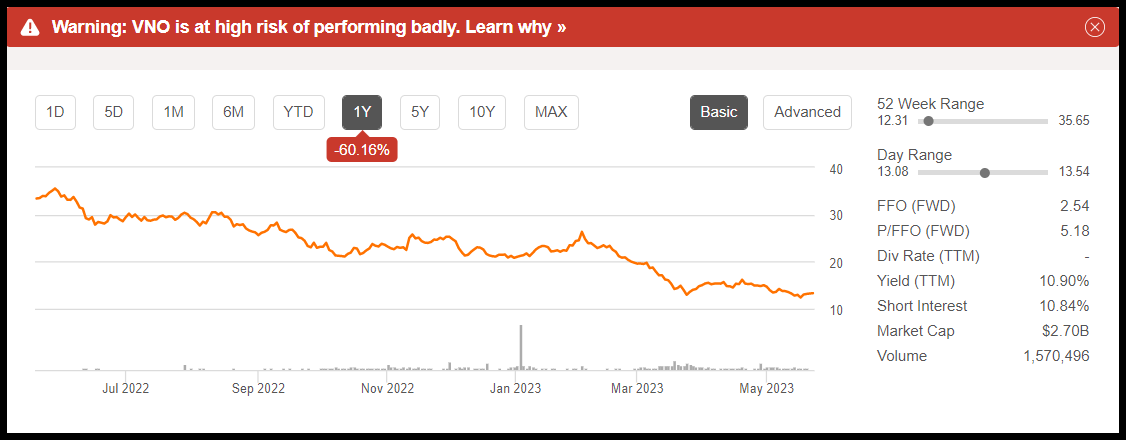

VNO Stock Price Performance (SA Premium)

{kind=link}

Vornado Realty Trust, however, has continued its downtrend. I last wrote about VNO stock in March, down nearly 30% since then, and missed top and bottom-line earnings for Q1.

A commercial real estate industry leader with portfolio concentration in key markets like New York, Chicago, and San Francisco, this high-yielding stock may come at a discount. Still, it also comes at a high risk, experiencing increases in office vacancies amid the work-from-home revolution and banking concerns. These factors pose tenant risks, and banks' financial instability comes into play, potentially trickling down to companies like Vornado. As pressures mount, it's crucial to pay attention to poor metrics, which have continued to be highlighted by VNO as to why the stock is at high risk of performing poorly.

VNO Stock Growth & Profitability

Seeking Alpha’s Factor Grades rate investment characteristics on a sector-relative basis. Although VNO is undervalued, its bearish momentum, downward analyst revisions, and lackluster growth and profitability indicate why this is a strong sell.

VNO Factor Grades (SA Premium)

As I highlighted in my previous article :

“When you factor in that office REITs typically buy office buildings through bank loans, given the banking debacles we’ve seen lately, Binary Tree Analytics outlines the scenario well, noting that higher interest rates can have dual impacts.

Higher rates drive lower valuations for office properties, thus making the asset side of SLG (and VNO) less valuable.

Higher rates will be responsible for higher financing costs, making SL Green (and VNO) less profitable unless it sells buildings.

Both stocks are highly leveraged, and in the event of refinance/exit, there could be difficulties and impacts on common equity.

Where shareholders appreciate a steady income stream, the commercial real estate risks are mounting, especially amid banks’ exposure.”

Falling growth and profitability are prompting analysts to revise estimates. Vornado has suspended dividends , which sent shares of the stock -9.5% following the announcement. Factor in a Q1 2023 FFO of $0.60 missing by $0.02 and revenue of $445.92M missing by $6.78M that sent shares down, eight analysts revised their estimates down within the last 90 days.

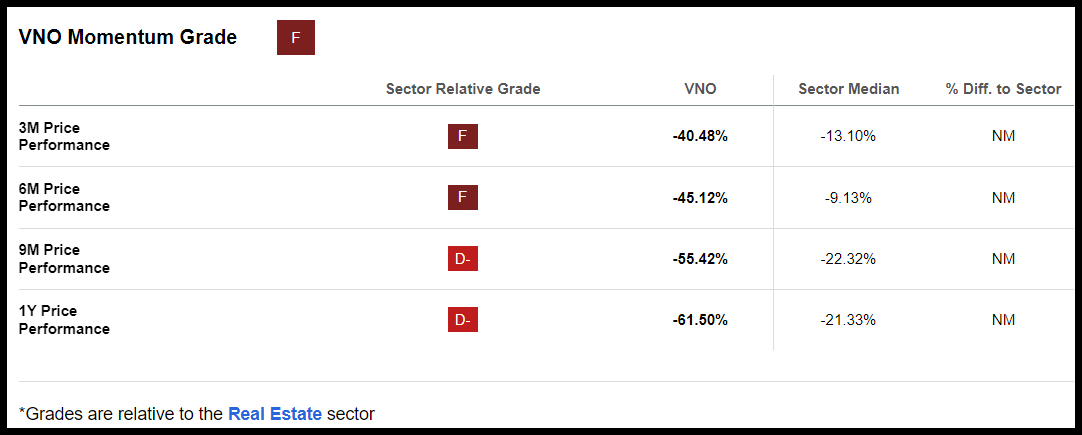

VNO Stock Momentum Grade (SA Premium)

{kind=link}

With declining momentum resulting in an ‘F’ grade, as VNO’s quarterly price performance substantially underperforms the real estate sector, VNO is at high risk of continued poor performance. High-interest rates, falling occupancy rates, dampening rent growth, and work-from-home negatively impact office real estate. Consider looking at Top Rated Stocks versus poorly performing office REITs for a portfolio.

How to Invest in REITs? Pick Strong Buys, not sells.

There was a time when REITs were excellent buys, especially in an inflationary environment, with fears of an impending recession. The ability to buy a stock at a discount is always a bonus, and as inflationary hedges and income-producing securities, many REITs have proven resilient. But not the three I’ve highlighted.

Since the pandemic, office exoduses have taken place. Where many REITs offer dividends and reliable income streams from these real estate investments, the new normal and work-from-home revolution is turning office REITs into a troubled sector. When you factor in buying or possessing this type of investment during a banking crisis, when the industry is already experiencing substantial declines in stock prices, it's well worth re-evaluating.

Seeking Alpha’s quant ratings and factor grades highlight that PGRE, BDN, and OPI possess weaker metrics than the sector median. Rather than purchasing sell-rated stocks with poor fundamentals, consider Top REITs or Top Real Estate Stocks that share the strong collective attributes of valuation, growth, profitability, momentum, and EPS revisions, for potential upside.

For further details see:

The Fall Of Office REITs