QVMS - The Fed Is Nowhere Near Pivoting

Summary

- Investors continue to remain optimistic that the Fed will pivot and lower rates in 2023.

- Friday's rally was fueled by hopes that the economy was weakening per the December employment report.

- The Fed's own projections communicate their expectations and what they will tolerate.

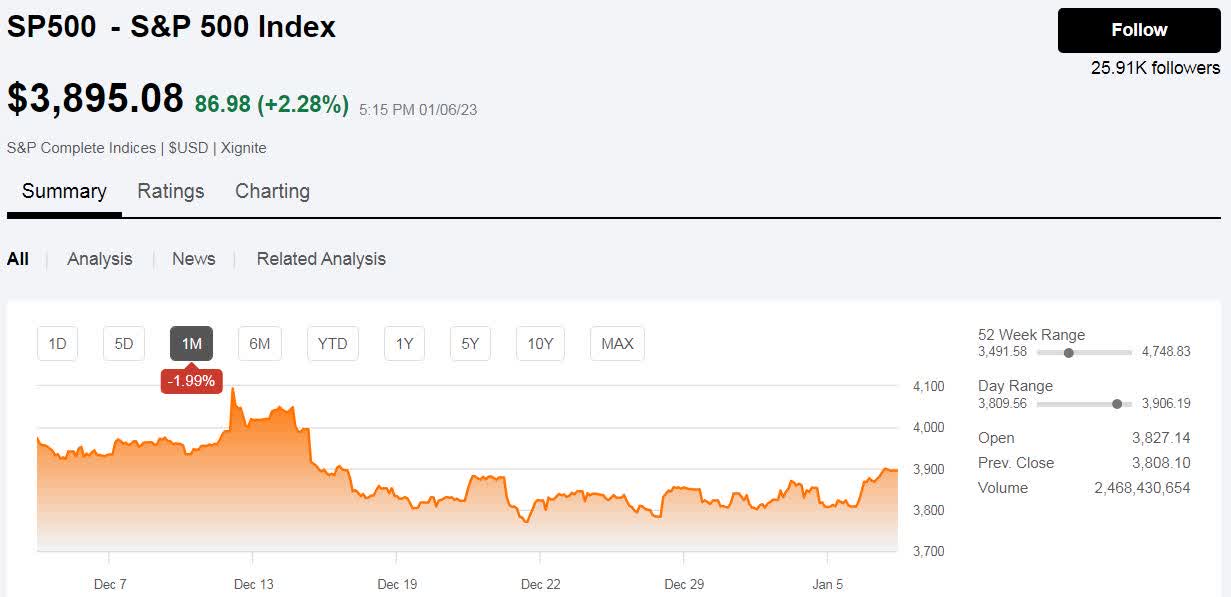

Despite Friday's rally, the S&P 500 ( SP500 ) remains relatively flat compared to where it was when the Federal Reserve met last month. Friday's rally was predicated on the hopes that the December jobs report showed softness in the economy. While bad economic news causing a stock market rally may seem counter intuitive, investors are correlating soft economic news with the hopes of lower interest rates, which are bullish for stock prices. Unfortunately, the reality of the situation places us far from an easing Fed.

{kind=link}

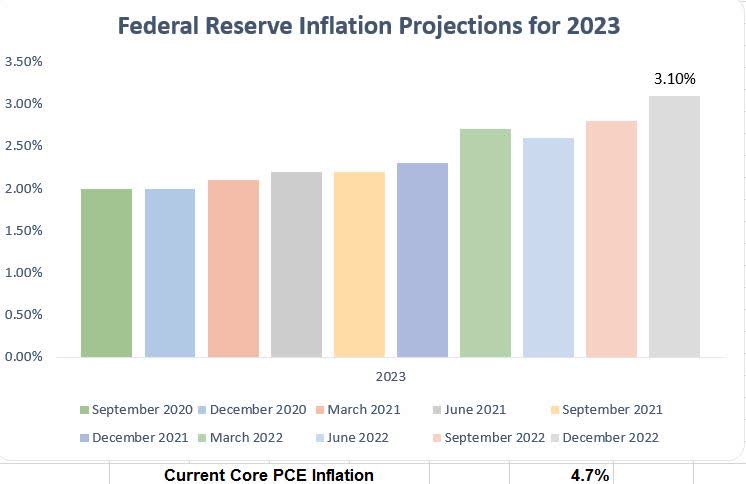

While investors keep pointing to a softening CPI as rationale that the Fed is moving towards easing, many investors need to realize that the Fed utilizes personal consumption expenditures (PCE) as its measure of inflation. More specifically, the Fed removes food and energy from its primary inflation indicator, known as core PCE. The Fed's long term PCE target is 2%. While the current core PCE is 0.7% lower than the high-water mark of 5.4% in February 2022, the current core PCE is a far cry from the 3.1% projected by the committee for 2023.

Fed Data in Author Spreadsheet

{kind=link}

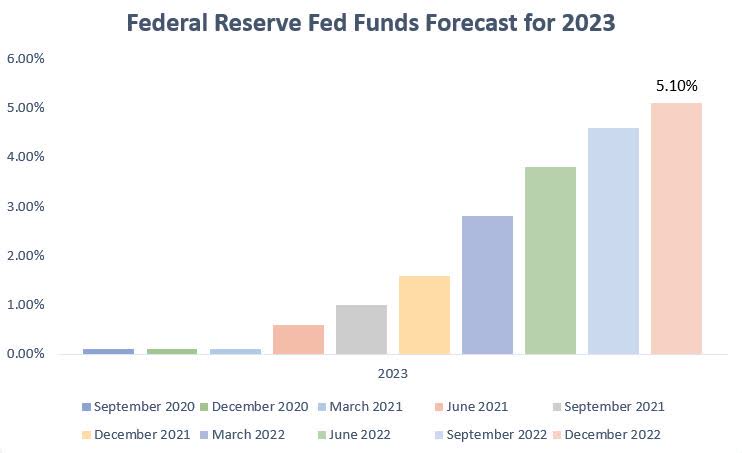

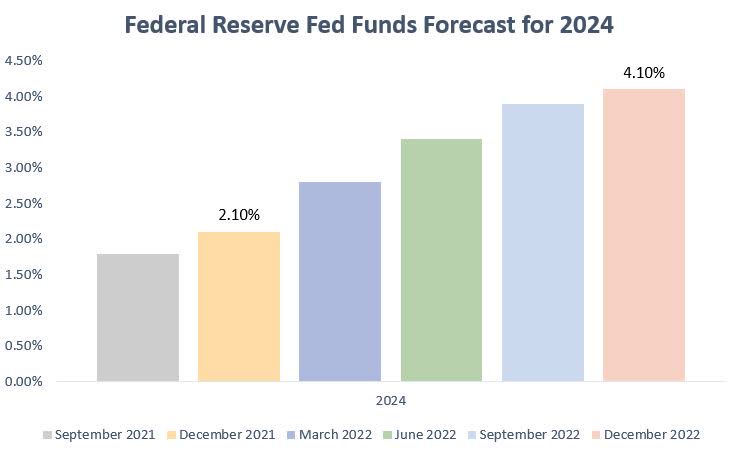

The stubborn trend of Core PCE is also a primary reason as to why the Fed continues to increase its interest rate expectations for 2023 and 2024. For the last five meetings, the Fed has raised its 2023 rate expectations from below 1% to above 5% and its 2024 rate expectations from under 2% to over 4%. What's more concerning is that Fed funds futures are fairly consist in pricing Fed funds rates below 2023 and 2024 expectations, with the widest variation of nearly 100 basis points in late 2024. The Fed seems determined to keep rates higher until core PCE improves, therefore, I believe it is investor expectations that will change to meet the Fed and therefore lead to more volatility in the equity markets.

Barchart and the Federal Reserve

{kind=link}

{kind=link}

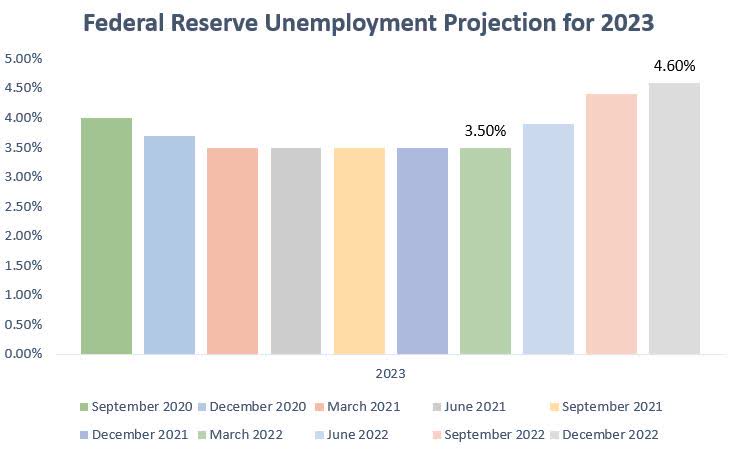

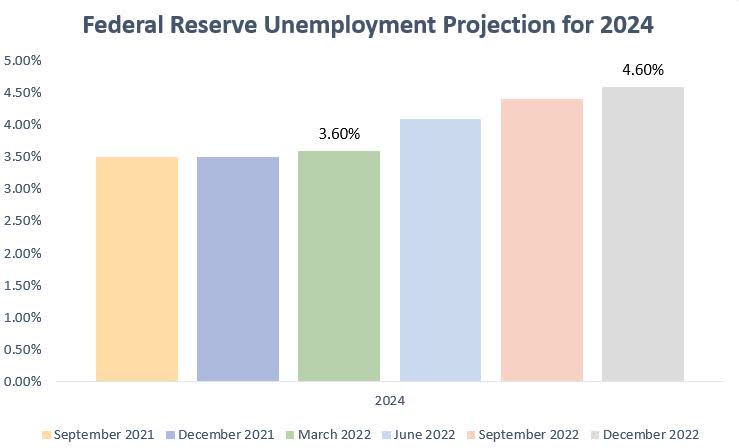

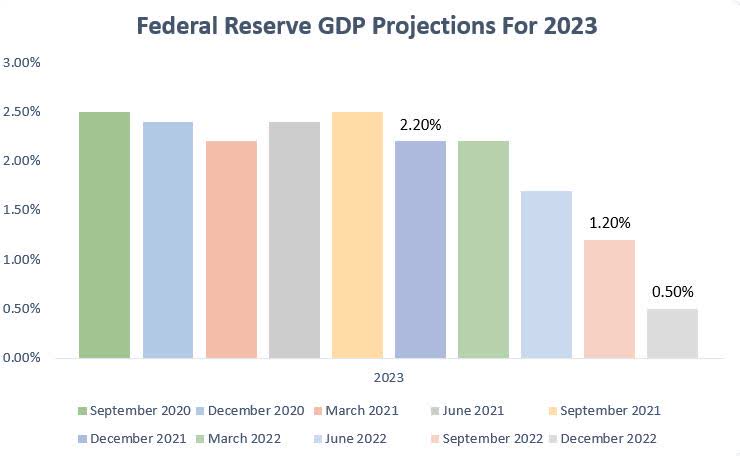

Inflation may be the primary driver behind Fed policy, but the committee's projections on growth and unemployment should not be ignored. While the Fed has raised its inflationary and interest rates projections, it has simultaneously lowered its growth forecast and increased its unemployment forecast. The Fed's 2023 GDP forecast currently stands at 0.5%, which is 150 basis points under its long-term target and 170 basis points lower than what was forecast a year ago. For unemployment, the Fed now projects a 4.6% unemployment rate for 2023 and 2024, which is 110 basis points higher than the current unemployment rate.

What I think is important here is not what the Fed is projecting, but what the Fed seems to be willing to tolerate in its fight against inflation. By projecting a higher unemployment rate, the Fed seems prepared to watch the economy shed more than 1.5 million jobs in order to achieve price stability. Additionally, the Fed seems content if economic growth flirts with zero during this time.

{kind=link}

{kind=link}

{kind=link}

Finally, I believe the overvaluation of the equity markets can be best expressed by looking at the bond market, specifically the 10-year Treasury. Currently, the 10-year Treasury yield is trading at an inverse relationship (or lower than) the current Fed funds rate. We know that the Fed is going to raise rates by 50 to 75 basis points in the early part of 2023. I doubt that investors will tolerate a 10-year yield of more than 100 basis points below the Fed funds rate, which has not happened in at least 21 years.

With the likelihood of Treasury rates rising, we can deduce that equity prices will fall, which is a basic correlation of financial markets. All this data points to higher Treasury yields, lower equity prices, and the need for far more economic deterioration before the Fed decides to pivot. As an investor, I am preparing for future volatility by increasing my cash position and investing in short term Treasury bonds for income. This will give me the optimal liquidity to buy into the upcoming volatility.

For further details see:

The Fed Is Nowhere Near Pivoting