VEA - The Fed Is Set To Let The Market Burn As Tech Stocks Slide Down The 'Slope Of Hope'

2023-10-30 10:28:56 ET

Summary

- Traders are likely looking for some reassurance from the Fed at this Wednesday's FOMC meeting.

- They're unlikely to get it with inflation still too high and not showing much progress towards the Fed's 2% target.

- Investors who overpaid for stocks and property thinking that interest rates would fall to justify their investments could now be in trouble.

- Without an earnings miracle, the "magnificent seven" NASDAQ stocks that have led the market are likely to slide down the "slope of hope."

- Valuation models indicate that the S&P 500 is overvalued by roughly 20% compared with current levels of interest rates.

Music is the silence between the notes.

-Claude Debussy

With stocks off roughly 10% since their July highs, market participants are watching this week's FOMC meeting closely for signs that the Fed may signal some sort of dovish policy change. The immediate outcome of the meeting is more or less decided, with markets currently assigning a nearly 100% probability of the Fed keeping interest rates unchanged. The big bets aren't necessarily on what the Fed will do for this meeting, but on the future path of monetary policy and what it means for the markets going forward. For these, investors will need to read between the lines and decipher some subtle hints from Wednesday's press conference. It's important to listen to what Jerome Powell says - equally important will be to note what he doesn't say. Contrary to popular belief, the Fed is not going to pivot and cut rates to rescue the stock market in my view.

Stocks Have Fallen As Investors Come To Grips With Valuation Surge

Fall is in full swing in the US, and right on cue, market volatility has risen. This is typical for this time of year . Stocks have fallen in large part not because of what has happened, but because of what hasn't happened. This spring, artificial intelligence was getting saturation coverage in the media, and investors were tripping over each other to see who could bid up AI-adjacent stocks the fastest. A lot of it didn't make sense- you probably wouldn't pay $1 million for a brick-and-mortar business that makes $7,000 to $10,000 per year. But that's exactly what investors were doing during the pandemic " everything bubble " and this spring's AI craze. In a similar vein, you wouldn't buy an investment property with a 6% mortgage and a 3% cap rate, but a lot of people did last year, and now they're probably not too happy about it. What hasn't happened for stocks is the earnings boom needed to justify a rapid rise in valuations. To this point, the fall in stocks isn't about what has happened in terms of the incoming economic data, rather it's been about what hasn't and won't happen, which is an earnings boom in my opinion.

Total 2023 earnings for the S&P 500 ( SPY ) are expected to come in around $219 for 2023, up barely from $218 in 2022. In terms of the P/E ratio, that's about 19x earnings on the S&P 500. The big question mark pertains to 2024 as analysts have priced a huge AI and tech-driven earnings surge. So far, this earnings season is showing that that's not really on track to happen. This is the reason stocks are down over the past few months- it has little to do with Ukraine, the Middle East, China, or who the Republican nominee for president is. The current correction in stocks is all about earnings relative to analyst expectations. AI hype is now fading and now it's time for companies who made big promises to follow through.

{kind=link}

As is typical, a few will but most won't. According to market strategists, "the wall of worry" has become the " slope of hope ." Sell-side analysts are still pricing a 12% increase in earnings for 2024 to $247, at the same time that leading economic indicators are pointing to a moderate recession. This doesn't add up. In fact, earnings should likely fall in 2024 as they do when every business cycle turns. At earnings of $180 and a 15x multiple, the S&P 500 would trade for about 2700, over 40% below its December 2021 highs.

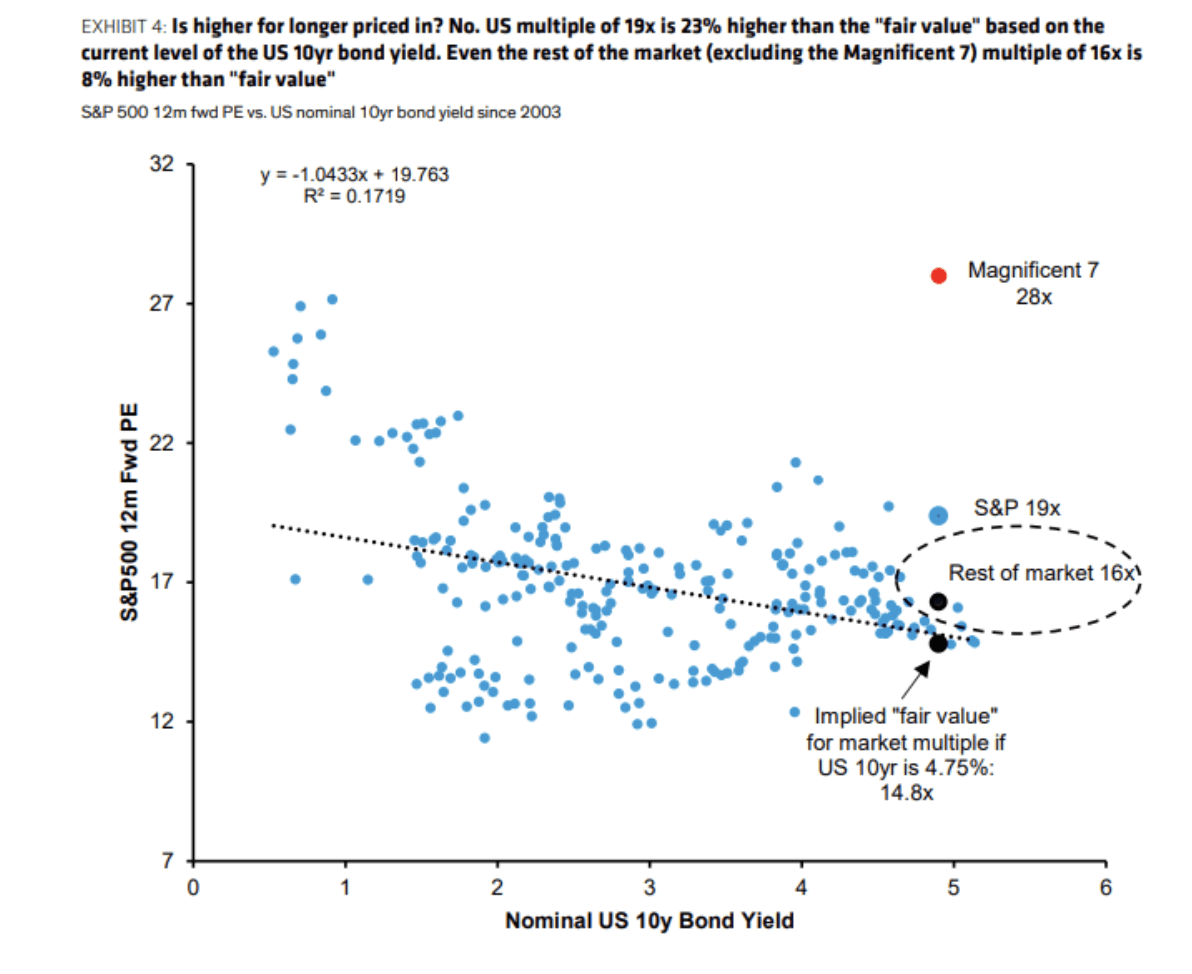

Buying the dip is always a tempting strategy for investors, but basic math on the insane run that stocks had during the pandemic urges caution. On one level, stocks should trade at a higher level than they did before post-pandemic since consumer prices are now about 20% higher. However, the change in interest rates means that stock values often won't be able to keep up with inflation when the Fed is forced to hike rates aggressively to combat inflation. Running a linear regression on current and historical market data implies a fair value for stocks of roughly 15x earnings - about 20% lower than today's multiple. This makes some sense - it's weird to be able to earn more in cash than you can by investing in actual businesses.

S&P 500 Fair Value (Bloomberg)

{kind=link}

At the same time, value stocks have been completely crushed since the Fed started hiking rates. For example, a lot of people don't like Altria ( MO ) for moral reasons, but they're now down under $40 with a 10% dividend yield. It's not as if their cash flow is terribly unstable! Most people will keep smoking. Philip Morris International ( PM ) yields 6%. Don't get too hung up on the individual stock picks- my main point here is that there are some very cheap stocks outside of Big Tech if you know where to look. We can debate various value stocks but we know they're out there. In fact, if you're reading this, please share your favorites in the comments!

After a terrible 2022, small caps ( IJR ) are down another 7% this year as of my writing this, while bonds are becoming a much better value with each 1% rise in long-term interest rates. Small caps outperform the S&P 500 in the long run , in large part due to the crazy valuations that periodically come and go in the large-cap space. International stocks ( VEA ) have gone nearly nowhere in dollar terms for years, indicating investors might be able to pick up some value. In the REIT sector, you can pick up plenty of stocks 50% or more off their 2021 highs, so long as you do your homework to avoid those going bust there's great value. Bank preferreds too are often yielding over 7% with tax-qualified dividends now if you know where to look. There's value to be found if you look in the right places, while Big Tech could be highly vulnerable to earnings coming in below expectations. The safest and best investment of all right now is probably just Vanguard's money market funds ( VMFXX ), paying about 5.5% compounded and invested in risk-free short-term Treasuries.

The Fed Won't Hike Much More, But Likely Isn't Coming To Rescue The Stock Market

There is a longstanding internal debate at the Fed on whether they should raise interest rates to counteract speculative activity. The theory is now pretty well-aligned that the Fed should simply ignore speculative stock market activity and only focus on the underlying consumption and fixed investment trends. In every stock market bubble, a few people get rich, a few people lose their shirts, and the net effect on the economy is basically zero. The upshot to this is that when stock market bubbles deflate, the Fed should also mostly ignore it because paper gains evaporating doesn't hurt anyone. This is different from a credit bubble like 2008, where there were millions of bad loans, half-finished construction projects, and mass unemployment. The Fed's mandate here is to focus on price stability, and on that front, the recent news hasn't been great.

Core PCE, the Fed's preferred inflation measure, rose 0.3% in September for an annualized gain of 3.7%. That's nearly double the Fed's 2% target. Worse, market-based inflation expectations have been creeping up at the same time as Fed pause bets. The US personal savings rate came in at 3.4% for September, indicating that consumers are collectively living above their means (estimates for sustainable savings rates are about 8-12% annually to maintain your standard of living in retirement, and the long-term US average is about 8% ). The Fed really needs to keep rates high to encourage people to save and discourage borrowing.

Here's the thing - the Fed can't really declare victory on inflation because the most recent September data is telling them that inflation is above their target and spending is rising faster than income. The UAW strikes and the oil situation with Iran put further pressure on the Fed to hike one more time before the end of the year. That's exactly what I think they'll do, pausing at this meeting before making one final hike in December.

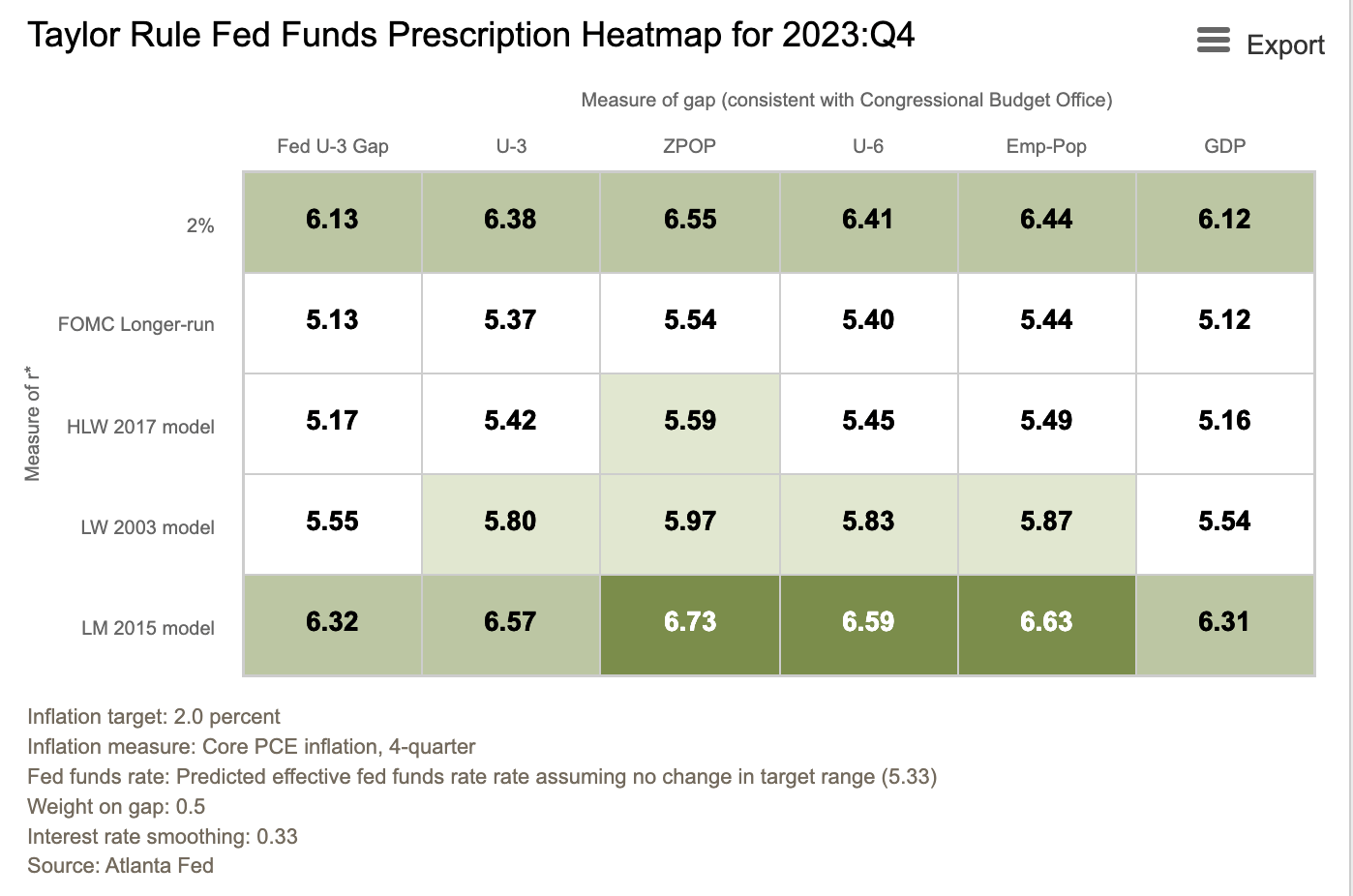

I did some quick modeling using the Taylor Rule to see where the Fed funds rate should be. I was actually a bit surprised to see that the model now thinks Fed policy is closer to a decent place. Most of the model runs are still indicating one more hike is necessary to get monetary policy in line (with many runs indicating a necessary rate over 6%), so barring some bad non-farm payroll numbers over the next 6 weeks, my guess is they'll put the final hike in at December's meeting before pausing for 6-12 months.

Taylor Rule Utility (Atlanta Fed)

{kind=link}

We have an interesting recent precedent here from 2018's stock market. There, the Fed had hiked rates and the market started to really get the message, falling about 20% in a matter of weeks. Nothing really happened in the underlying economy, either before or after. For example, if you look at leading economic indicators from then, there was no cause for alarm.

Donald Trump had been firing off threats to the Fed chairman via Twitter for months, and Powell finally threw in the towel, with the Fed soon indicating that they would reverse course after a December hike and following through with cuts. Of course, then the stakes were much lower for the Fed. Inflation was near the 2% target and they didn't have the credibility issues that they have today. Stocks were quite cheap on a P/E basis as well in December 2018. I still think this set a bad precedent. It's not a coincidence that I think prices could return to similar levels as then. The "everything bubble" started soon after with stocks like Tesla ( TSLA ) going crazy even before the pandemic when the Fed started cutting rates.

The Fed likely learned some lessons in 2018, one being that there are negative long-term consequences to bailing out the stock market in the short run. Another lesson is in dealing with political pressure- there is an eternal conflict of interest where politicians want the Fed to print money before an election to fire up the economy in the short run, leaving the inevitable hangover for later. Withstanding this type of pressure is important for long-term growth and prosperity. The final lesson is more technical and relates to the Fed's quantitative tightening program. In 2019 the Fed was forced to cut rates and inject money in large part due to a glitch in the plumbing of the financial system. In my opinion, this wasn't very targeted and fueled speculative money going into the NASDAQ ( QQQ ) at nosebleed valuations, into second and third homes, venture capital, and all kinds of other speculative bets. Now the Fed has a better process in place to handle the internal mechanics of the banking system. This means that they can and will continue applying targeted pressure on inflation with QT, which should lower asset prices and help bring inflation back in line with the Fed's target. Lower stock market valuations are a feature, not a glitch of the Fed's inflation-fighting campaign.

Bottom Line

Jerome Powell and the FOMC are likely to let the market burn here. Traders will be looking for some reassurance from the Fed with stocks down 10% from July. I believe they're unlikely to get any. With inflation still above target and recent PCE data indicating inflation is no longer moving in the right direction, the Fed will likely reiterate its higher-for-longer stance and keep a December interest rate hike on the table. That's a problem for investors who overpaid for various assets thinking that interest rates would fall and put their cash-flow negative purchases in the black. While there are pockets of value in the market, the broad market is still likely to fall 20% or more due to valuations not being in line with business fundamentals.

For further details see:

The Fed Is Set To Let The Market Burn As Tech Stocks Slide Down The 'Slope Of Hope'