VTI - The Fed Likely To Hike In May June And July To 5.75%

2023-04-28 11:45:13 ET

Summary

- The core PCE inflation continues to be sticky at the 4.6% level.

- The consumer spending will continue to keep inflation sticky, as long as asset prices remain elevated, and the unemployment rate remains low.

- Thus, I expect the Fed to keep hiking, and the S&P 500 to enter Phase 2 of the bear market.

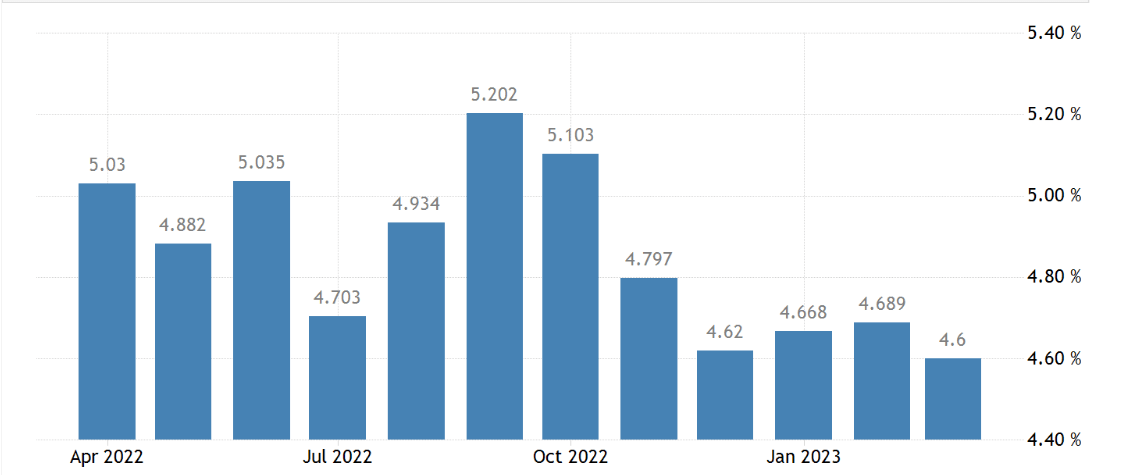

The current market expectations for the Federal Funds rate

Let's start with what everybody already knows, and that's the current market expectations for the Fed's interest rate policy. Based on the Federal Funds futures, the market currently expects the Fed to:

- Hike in May (next week) by 25bpt to 5-5.25% target range (about 90% probability).

- Pause after the May meeting.

- Cut interest rates in September by 25bpt (about 51% probability) or in October by 25bpt (about 82% probability).

- Cut interest rate in December by 25bpt to 4.50-4.75% (about 80% probability).

- Continue to cut the Federal Funds interest rate in 2024 down to 2.75-3%, which appears to be the expected terminal rate, since no cuts or hikes are currently expected in 2025.

The current market expectations contradict the Fed's guidance. The Fed expects the Federal Funds rate to be at 5.1% in 2023, which supports the expectations of the hike in May and then pause.

However, the Fed has been clear that it does not expect to cut in 2023 and expects the Federal Funds rate to be at 4.3% in 2024 (much higher than the market currently expects) and at 3.1% in 2025, which is essentially what the market expects, but the market expects the Fed to get there in 2024.

But the reasons behind the expectations differ

Most tend to agree on the current expectations for the Federal Funds rate. However, the reasons behind the expectations differ.

The stock market bulls expect the Fed to pause and start cutting in Sep/Oct because the inflation will fall much faster than expected in the second half of 2023, mostly due to the fall in rents. Market rents are falling, and the official data will start reflecting that soon. Further, the labor market will remain resilient, and the economy will avoid the recession. Thus, the S&P 500 Index ( SP500 ) likely bottomed in October, and the new bull market is in the making.

The stock market bears understand that the monetary policy tightening works with the long and variable lags, and the aggressive monetary policy tightening in 2022/23 will cause a recession in the second half of 2023 and force the Fed to cut, as inflation falls. As the supporting evidence, the bears point to the March Banking Crisis and expect that the resulting credit tightness will reduce the consumption and cause an increase in the unemployment rate, all consistent with the recession. Thus, the bears expect the recessionary selloff in S&P 500 as the earnings get downgraded.

The Fed will likely hike beyond the current expectations

I actually think that the Fed will have to hike beyond the current expectations. This is a very objective assessment, based on the real data.

The Fed has the dual mandate: 2% inflation target and full employment. So, what data will the Fed see at the meeting next week:

- The unemployment rate is at 3.5%, the lowest in over 50 years. On top of that, there are still nearly 10M job openings. Obviously, the labor market is very tight - and this is inflationary.

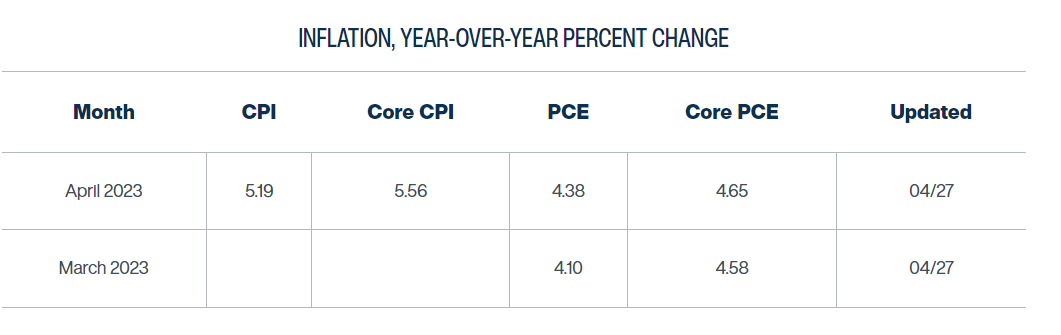

- The Fed's preferred inflation measure is the core PCE, so let's look at the core PCE, it is at 4.6% for March, about the same as in Dec 2022. The core PCE inflation has been "stuck" at 4.6% for 4 months. That's the fact, here is the chart:

{kind=link}

- Obviously, the Fed will see the recent data and hike in May, no question about that, and that's expected and priced in.

- But what happens in June? The Cleveland Fed Inflation Nowcast is forecasting the core PCE for April at 4.65%, which could be rounded to 4.7%, which means equal or even higher than the March core PCE.

{kind=link}

- The new claims for unemployment are gradually rising, but there are no indications of a seriously weakening labor market to justify the pause in June. So, at the June meeting, the Fed will likely be looking at the 5 months of the core PCE at 4.6% without any signs of slowing, and still a very tight labor market. So, why would the Fed pause? No, the Fed is likely to hike in July again, and this is not priced in.

- So, what happens in July? The Fed will meet again in July and likely be forced to hike again to 5.5-5.75%. Why? Inflation is not showing any signs of slowing, and it's stuck at a 4.5-4.6% level - that's the fact until the data shows otherwise.

- Going even further into the fall? The Fed will keep hiking for as long as the unemployment rate is below 4%, or possibly even 4.5%. Does this mean we are looking at 6% and higher in Fall for the Federal Funds rate? It depends on the data, it's too early to look that far.

What's causing this "sticky inflation"?

Yes, everybody knows by now that the low unemployment rate is causing the high wage growth, which is causing the sticky service ex-housing inflation. But this is only a small part of the story.

The real story is that the U.S. consumer is extremely wealthy, and doesn't really care about paying whatever the price is for most goods/services. Just try to get out, go to a restaurant, get on the flight, go to Las Vegas, and you will see it.

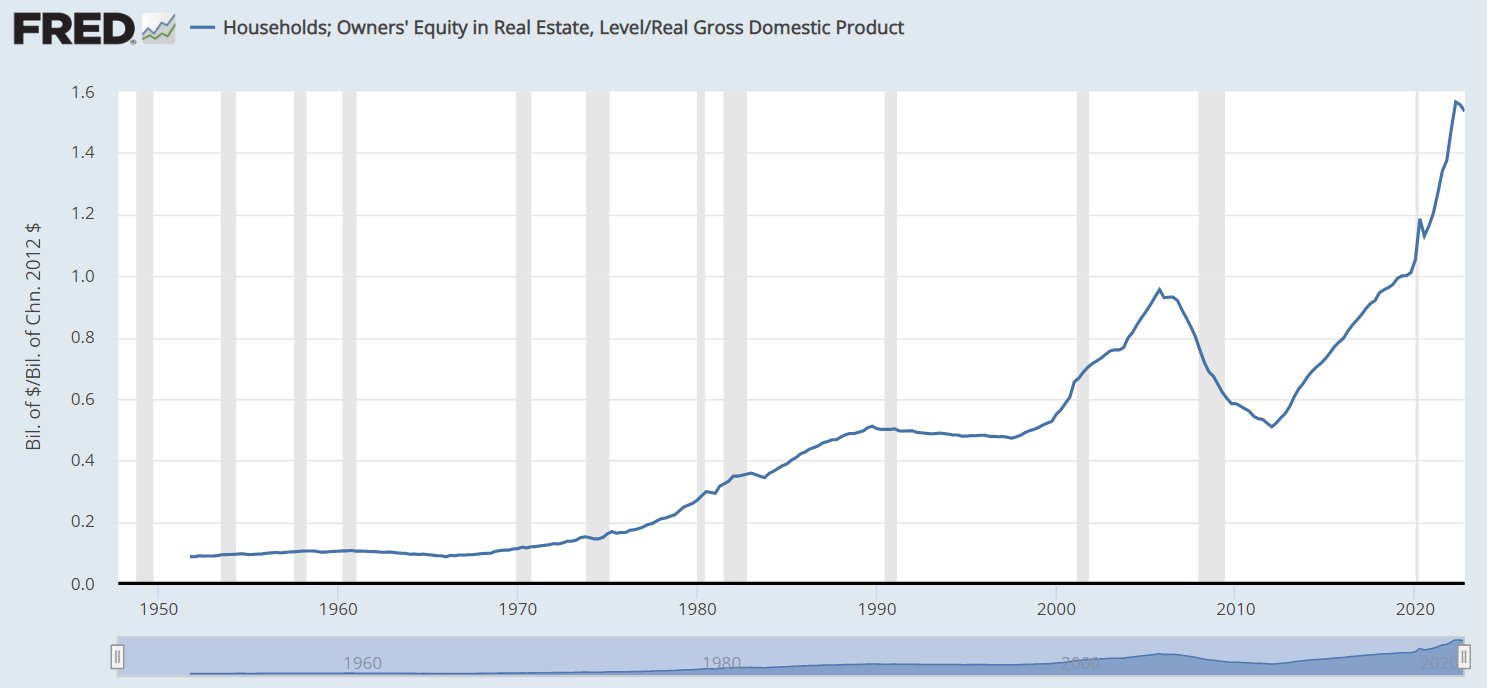

Here is the chart that explains my thesis - it's the Owner's Equity in Real Estate as the percentage of real GDP. The home prices spiked after the Covid-19 stimulus, and now the homeowners are sitting on this excess "equity" wealth, which they can tap at any time, and take that the trip to Las Vegas, or whatever else. That's causing the excess demand and the sticky inflation.

{kind=link}

In addition to this home equity wealth, also note that the stock market is still near all-time highs, which is adding not only to the wealth but also to the sentiment. Just how many investors reading this article expect the Fed to cut and push the market higher? That's the problem. If the stocks go up, you will all fly to South of France this summer and push the flight tickets higher. That's the service ex housing inflation.

Implications

The Fed has to continue hiking until: 1) unemployment rate increases; and 2) the asset price bubbles deflate, which includes the real estate prices, and the stock prices. Otherwise, inflation is not going down. The alternative is to just abandon the 2% inflation target, but that's unlikely at this point.

Thus, I expect a deep selloff in the S&P 500 ( SPX , SPY ), and the beginning of Phase 2 of the bear market.

For further details see:

The Fed Likely To Hike In May, June And July To 5.75%