AFMC - The Financial Deterioration Of World Central Banks - Racking Up The Losses

2023-08-21 10:40:09 ET

Summary

- World central banks, including the Federal Reserve, Bank of England, European Central Bank, and Bank of Japan, are facing significant losses due to their own mistakes.

- The central banks' expansion of balance sheets and exposure to interest rate risk have led to losses as inflation spiked and monetary policies changed.

- The losses incurred by central banks will ultimately be borne by taxpayers and may have political ramifications.

In a press conference on March 22, 2023, ten days after the failure of Silicon Valley Bank (SIVBQ) Fed Chairman Powell was asked what went wrong. He responded:

“Silicon Valley Bank management failed badly-they grew the bank very quickly, they exposed the bank to significant liquidity risk and interest rate risk, didn’t hedge that risk.”

If that is not the pot calling the kettle black!

The Federal Reserve has made the very same mistakes. In fact, all major world central banks have made the same mistakes. And currently, the central banks are paying for those mistakes as they incur large losses.

In a working paper for the National Bureau of Economic Research, Robert Hall and Ricardo Reis published MAINTAINING CENTRAL BANK FINANCIAL STABILITY UNDER NEW STYLE CENTRAL BANKING in May 2015. In it they talk about how the Bank of Japan, the Federal Reserve, the European Central Bank and the Bank of England made dramatic changes to how they conducted monetary policy in response to financial crises.

“They borrowed trillions of dollars from commercial banks by expanding reserves and paying positive or receiving negative interest on them, while using the proceeds to enlarge their holdings of government bonds and other risky investments.”

In doing so, they exposed themselves to significant interest rate risk if interest rates rose.

Hall and Reis posited “Might the double burden of capital losses on central banks’ portfolios and the rising cost of paying market interest on trillions of dollars of reserves threaten the banks’ financial stability?”

This is precisely the situation the world central banks are dealing with now.

As inflation spiked in 2022 and the central banks began changing their monetary policies to combat the higher inflation, they encountered the exact risks Hall and Reis discussed.

Federal Reserve

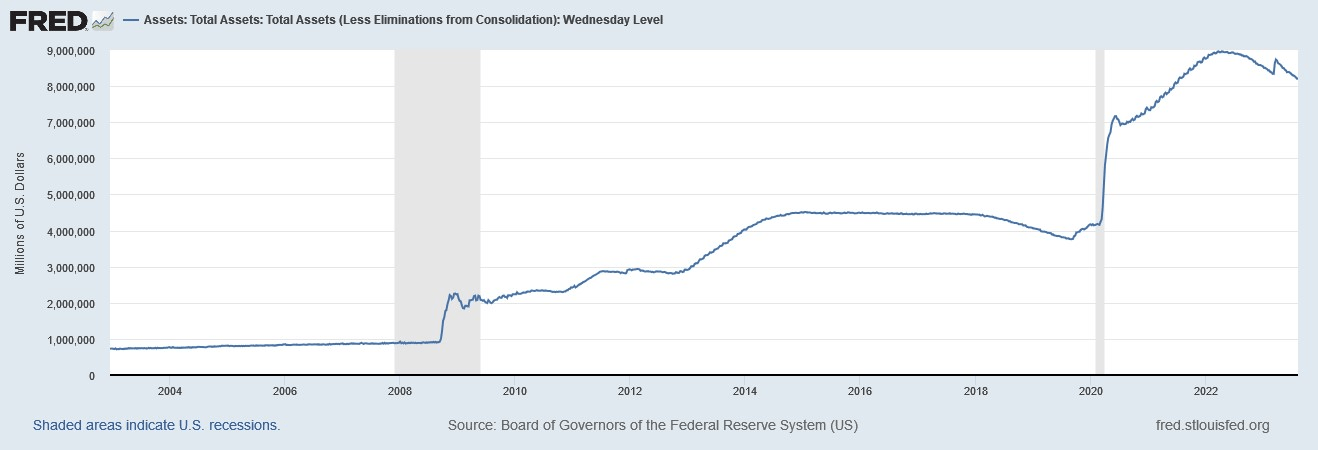

Following the Great Financial Crisis ((GFC)) of 2008 the Fed rapidly expanded their balance sheet. It grew tenfold, from $850 billion pre-GFC to almost $9 trillion at its peak in 2Q22.

{kind=link}

The Fed deviated from their traditional practice of buying only short-term Treasury bills and Treasury notes to also buying longer term Treasury bonds and mortgage-backed securities ((MBS)).

In doing so, they created an asset/liability mismatch, which exposed them to the same unhedged interest rate risk that Chairman Powell criticized SVB management for employing. That is, they funded fixed rate long-term assets with variable-rate short-term liabilities.

The byproduct of this rapid explosion in its balance sheet through a large injection of liquidity was an increase in inflation. While it took some time to materialize, inflation began to appear in 2021. Initially, Fed Chairman Powell felt the inflation was “transitory” but by 1Q22 the Fed acknowledged that inflation was a problem and began to reverse the Quantitative Easing ((QE)) policies of the prior fourteen years.

Core PCE

{kind=link}

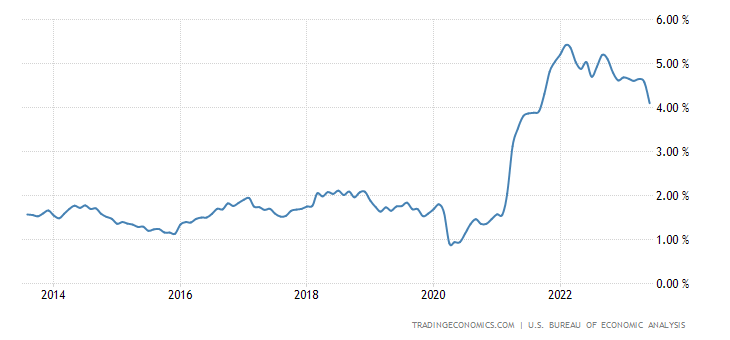

The Fed’s mandate for stable prices has them targeting a long-term goal for inflation of 2.0%. While there are many inflation indicators, the Fed’s preferred method for measuring inflation is the core PCE.

This indicator broke above the 2.0% target in February 2021, and peaked at 5.4% in February 2022. The Fed began their tightening process in March 2022. While core PCE has since fallen to 4.1%, it is still significantly above the Fed’s target of 2.0%.

The Fed implemented a Policy Normalization plan which included two components. The first was an increase in the Fed Funds rate and the second was a reduction in their balance sheet, commonly referred to as Quantitative Tightening ((QT)).

{kind=link}

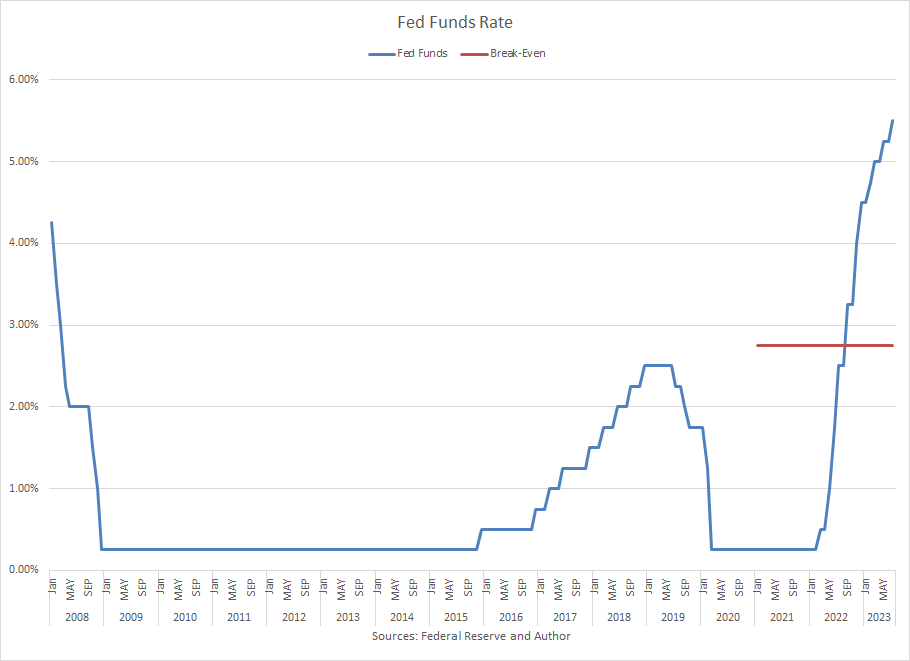

Since March 2022 the Fed has increased the Fed Funds rate eleven times to the current range of 5.25%-5.50%. This represents a 525 basis point increase over a seventeen-month period.

The net effect of this dramatic rise in short rates has been to increase the interest expense the Fed is paying on their variable-rate liabilities, namely bank reserves and reverse repurchase agreements. While their interest expense has been increasing, the income they earn on their fixed-rate assets has not changed. Consequently, the Fed’s net interest margin has turned negative.

The break-even rate for the Fed, when their interest expense on their liabilities would exceed the income they are earning on their assets, is 2.75%. That level was breached on September 22, 2022 when the Fed hiked the Fed Funds rate to 3.00%-3.25%. There have been six additional hikes totaling another 275 basis points since then.

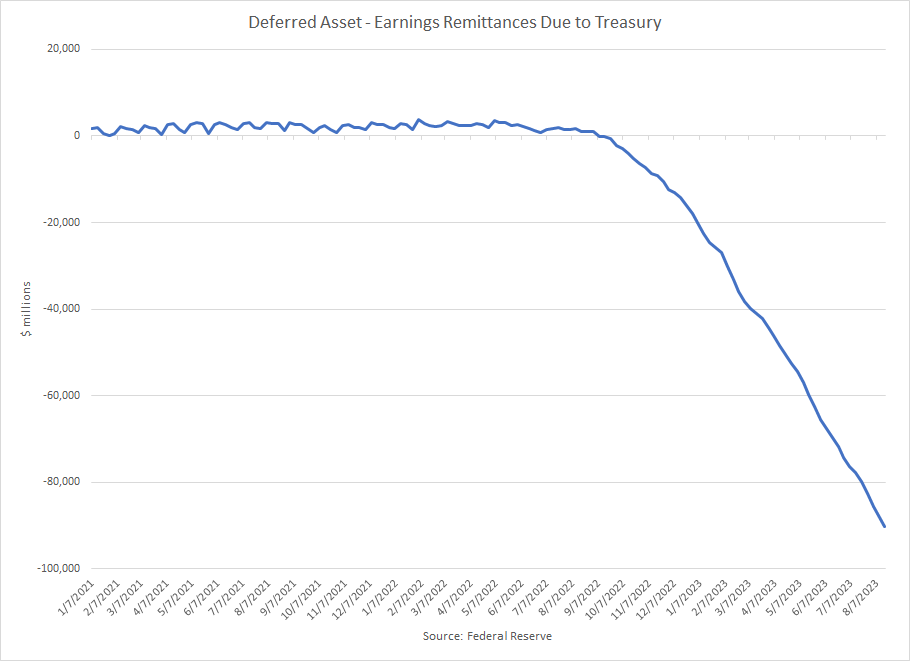

Under the Fed’s accounting policy, their losses are recorded in a deferred asset account called “Earnings Remittances Due to Treasury” as a negative liability on their balance sheet. They therefore, are able to protect their capital account, as the losses have no accounting effect on their capital.

This is fortunate, as their cumulative losses total $90 billion, while the Fed’s capital is only $42 billion.

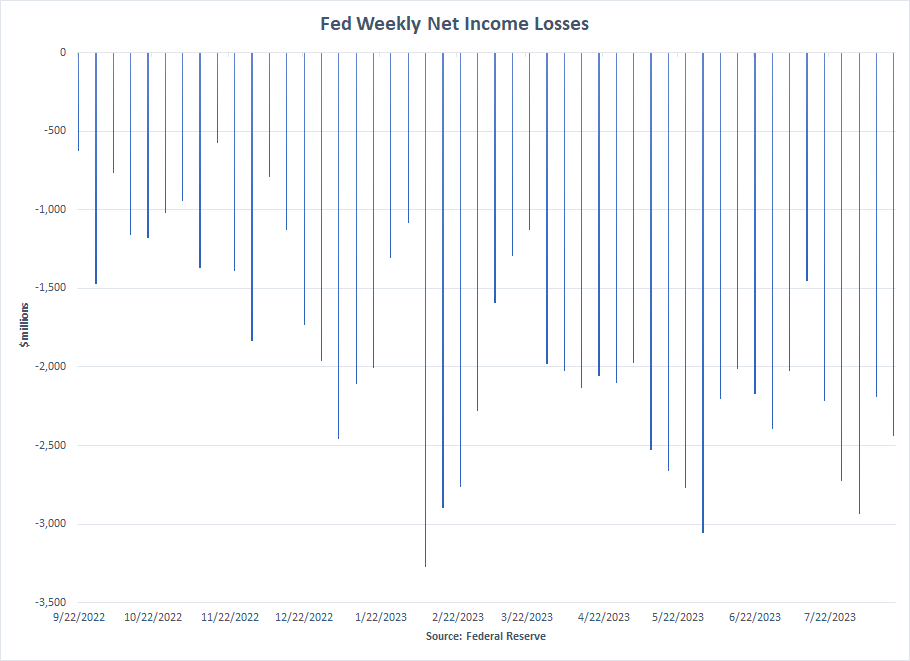

{kind=link}

The Fed has been losing money every week for almost eleven months. The four-week average weekly loss exceeds -$2.5 billion.

{kind=link}

The Fed will continue to lose money every week until the cost of their liabilities drops below the break-even rate. Based on the Fed’s Summary of Economic Projections from the June 2023 FOMC meeting, this won’t happen until 2026. Therefore, the Fed can expect to generate weekly operating losses for another three years.

By then, the deferred asset account may show the Fed hiding more than $300 billion in losses.

Then there are the balance sheet losses.

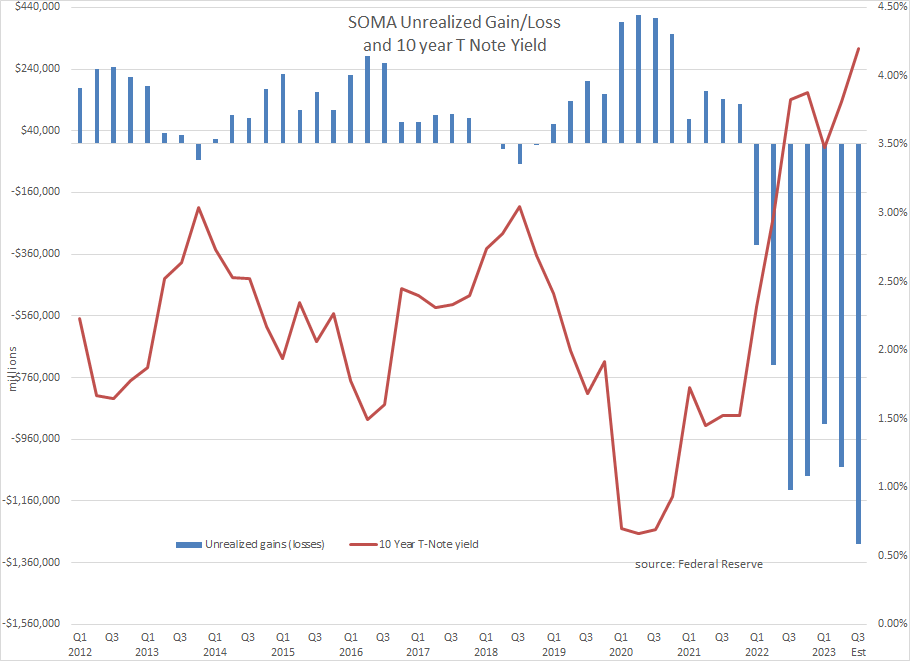

The Fed records their bond purchases at amortized cost. Their entire SOMA portfolio was purchased when rates were much lower than they are today. As a result, the SOMA portfolio is underwater. That is, every single security the Fed owns was purchased at a higher price than its market value today.

The bulk of the Fed’s purchases occurred when yields were below 2.0%. The SOMA portfolio first turned to an unrealized loss in 1Q22 when the ten-year Treasury note climbed to 2.3%. We estimate that the current unrealized loss in the SOMA portfolio is -$1.3 trillion with the ten-year Treasury note at 4.2%.

{kind=link}

Under the Fed’s policy normalization plan they are shrinking the size of their SOMA portfolio through maturity roll-offs. Since the peak in 2Q22 the SOMA portfolio has been reduced by $1 trillion and currently stands at $7.8 trillion. This is only an 11% decrease from the peak.

While some have argued that the Fed should cut their holdings more quickly, they will not actually sell any securities, because to do so would force them to recognize the accounting losses between the current market price and the higher acquisition cost of the bonds. The Fed does not want to record these losses.

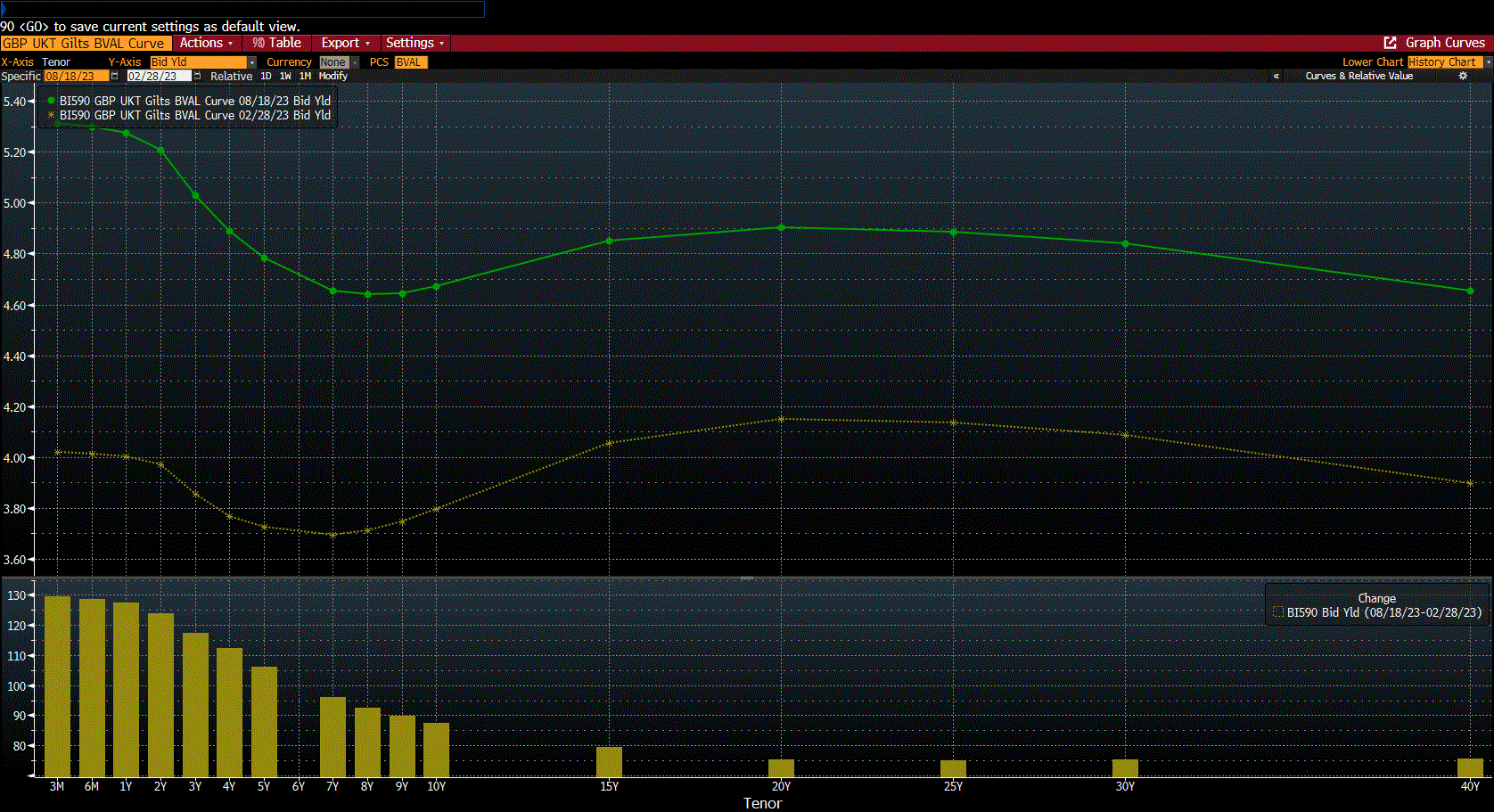

Bank of England

The Bank of England ((BOE)), which was established in 1694, is the oldest central bank in the world. It has been the model on which most modern central banks have been based.

Following the GFC, the BOE also embarked on a monetary policy of balance sheet expansion. Having dropped the Bank Rate to almost zero, the BOE needed another method to stimulate the economy. Like the Federal Reserve, the BOE employed the new tool of QE.

In 2009 they created a new entity called the Asset Purchase Facility ((APF)) to ease corporate credit conditions. Through the APF the BOE implemented their monetary policy by purchasing UK government bonds.

The first year they purchased GBP 200 billion gilts. Over the ensuing 10 years the APF doubled in size, then during the pandemic it doubled again. In total, the APF purchased GBP 875 billion gilts. At its peak, the APF owned 46% of the gilt market.

Office For National Statistics

Like at the Federal Reserve, the APF has an asset/liability mismatch. The BOE purchased fixed-rate bonds and funded them with short- term variable-rate liabilities, mainly central bank reserves.

QE injected a tremendous amount of liquidity into the UK economy. Initially this new cash led to rising asset values in stocks, bonds and housing. Eventually, though, it caused inflation to surge.

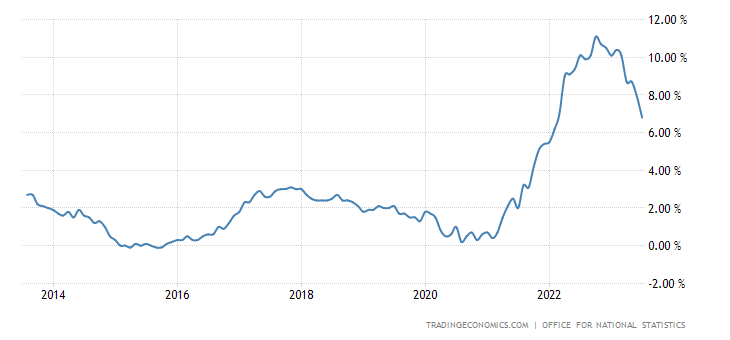

The BOE has a target inflation rate of 2.0%, but by 2021, the inflation rate broke above that threshold. The surge in inflation was caused by post-pandemic supply chain bottlenecks, and rising food and energy prices. The inflation rate continued to climb, peaking at 11% in 3Q22, its highest level in forty years. While the CPI has fallen to 6.8%, it is still significantly above the 2.0% target and remains a cause for further tightening.

UK CPI

{kind=link}

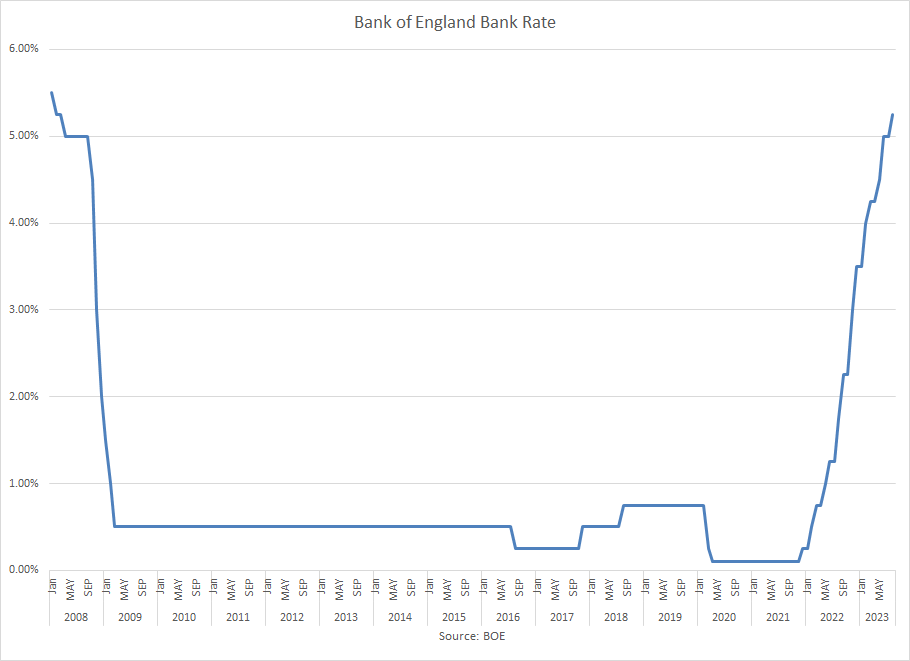

The BOE was the first major central bank to act to counter the spike in inflation when they raised their Bank Rate by 15 basis points in December 2021. Since then, there have been thirteen additional hikes for a total increase of 515 basis points to the current Bank Rate of 5.25%.

{kind=link}

Like with the Federal Reserve, the BOE’s rate hikes had an impact on earnings. For Fiscal year end 2/28/23 (FYE23) interest income from the APF’s fixed-rate assets declined modestly to GBP 17.1 billion from GBP 18.1 billion the previous year. But their interest expense on their liabilities skyrocketed. Interest expense shot up to GBP 17.4 billion from GBP 1.3 billion the previous year, increasing by 13.4 times (or by 1,200%.)

The net operating losses have continued to accrue weekly since.

As for their balance sheet, the spike in interest rates caused the value of the BOE’s gilt holdings to decline.

The BOE’s accounting structure, however, differs from the Fed in two significant ways. First, they carry their securities on a mark-to- market basis, while the Fed uses amortized cost.

By using mark-to-market, any gains or losses are immediately recognized on their financial statements. In the BOE’s case, this meant a substantial mark-down in their assets.

The second significant difference, is that the BOE has an indemnity agreement with the Treasury. When the APF was created in 2009 one of the provisions was that the Treasury would indemnify the BOE for any and all losses. This means that if the APF records losses, the Treasury will reimburse them for the lost amount.

The first indemnity payment was made by the Treasury in October 2022.

For the full FYE23, the mark-to-market of the APF showed a large loss due to the rise in interest rates. The holdings had a market value of GBP 637.3 billion, while the indemnity payment from the Treasury was GBP 169.1 billion. Because of the indemnity agreement, the financials will never show an overall loss.

The loss, however, is covered by fiscal outlays, and ultimately is paid by the taxpayer.

Since FYE23 interest rates have continued to rise. The yield on the 2-year gilt has climbed 128 basis points, while the yield on the 10-year gilt has risen 86 basis points. According to the APF’s annual financial report, a 1 basis point increase in rates results in a 0.08% drop in market value of the portfolio. Based on the higher yields since FYE we estimate that the APF portfolio has lost another GBP 45 billion in value through the close on 8/18/23.

{kind=link}

As part of their QT policy the BOE is also reducing their security holdings. A portion of the decline will come from maturity roll-offs, but in addition, the BOE is selling securities. They are the first central bank to execute QT with security sales. Unlike at the Fed, the BOE is not concerned with losses on the sale of their holdings because of their indemnity agreement with the Treasury.

Their plan, going forward, is to reduce their gilt holdings by GBP 80 billion per year. Under an updated projection, the bank is expecting a loss of GBP 150 billion on the sale of gilts over the next ten years. They are forecasting transfers from the Treasury of GBP 40 billion per year for 2023, 2024 and 2025.

Bank of England and Economist

These payments are a burden for the government.

European Central Bank

The European Central Bank (ECB) is the world’s youngest central bank, having recently celebrated its 25 th anniversary.

Unlike the other central banks, which are national, the ECB conducts monetary policy for the European Union and its 19 member countries that have adopted the Euro as their common currency. It is the main component of the Eurosystem and the European System of Central Banks.

The relationship within the Eurosystem between the ECB and the National Central Banks (NCBs) of the EU is complex. One example is the risk sharing system that the ECB implemented for its asset purchases. The ECB retains 20% of government debt purchases while it splits the risk with the NCBs, and the remaining 80% of the government debt purchases are held by the NCBs.

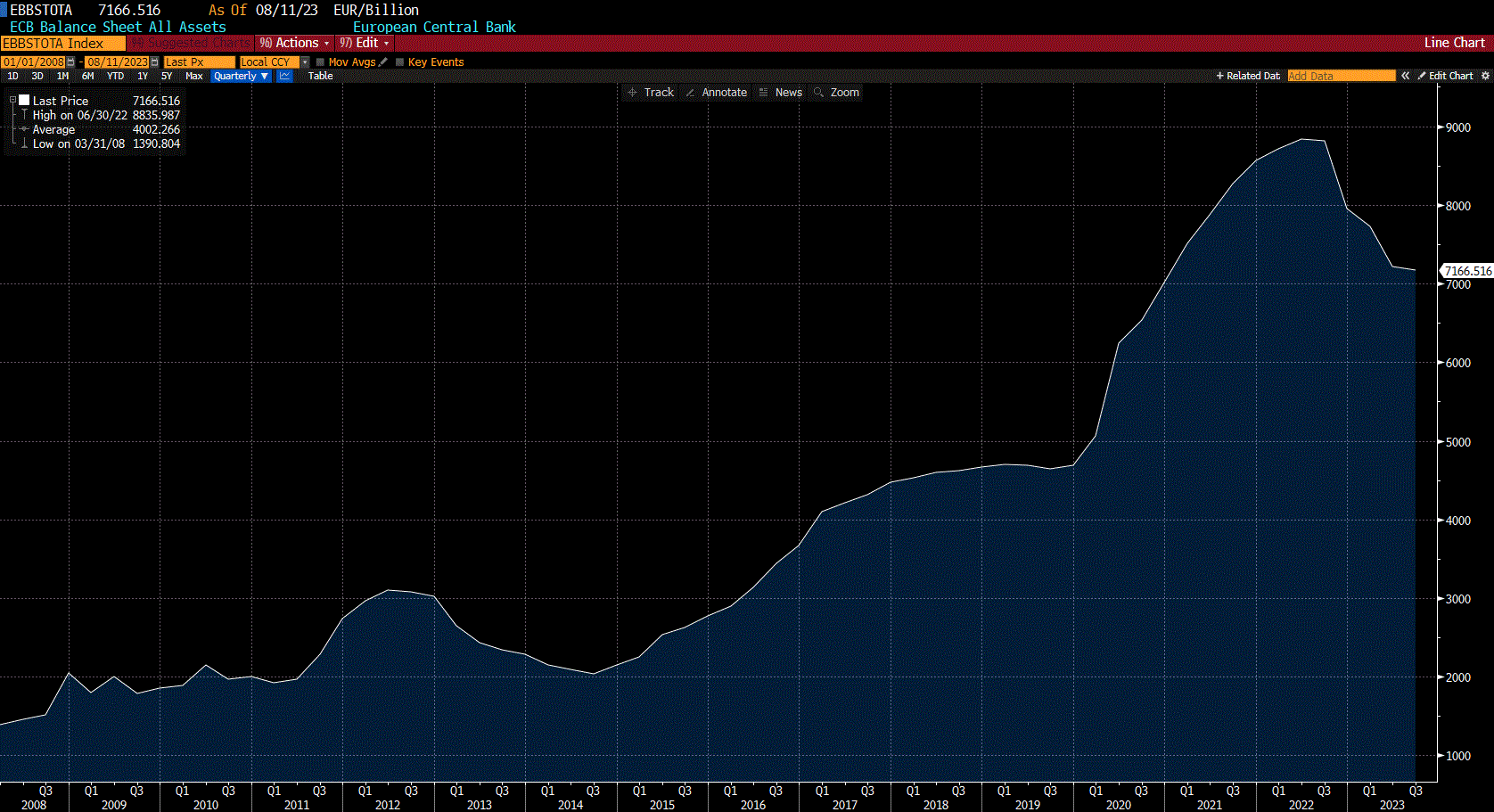

During the GFC the ECB also began expanding their balance sheet through QE. They started a Securities Market Programme ((SMP)) to deal with the sovereign debt crisis in Europe. Then in 2015 they created a new Asset Purchase Program ((APP)). In 2008 the ECB had 1.5 trillion euro of assets, which by the peak in 2022 has grown to almost 9 trillion euro.

{kind=link}

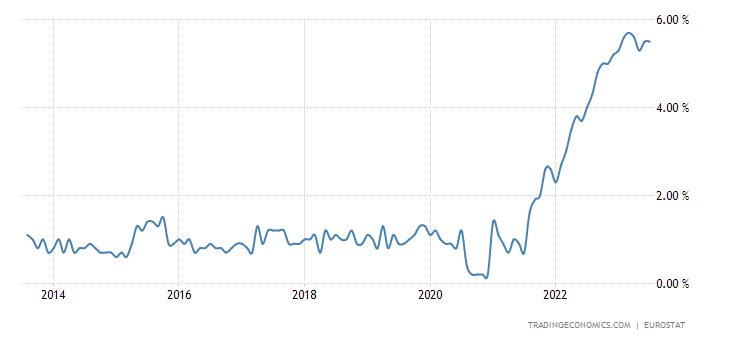

The ECB’s primary monetary policy objective is to maintain price stability. The Governing Council believes that price stability can best be sustained by aiming for 2.0% inflation over the medium term.

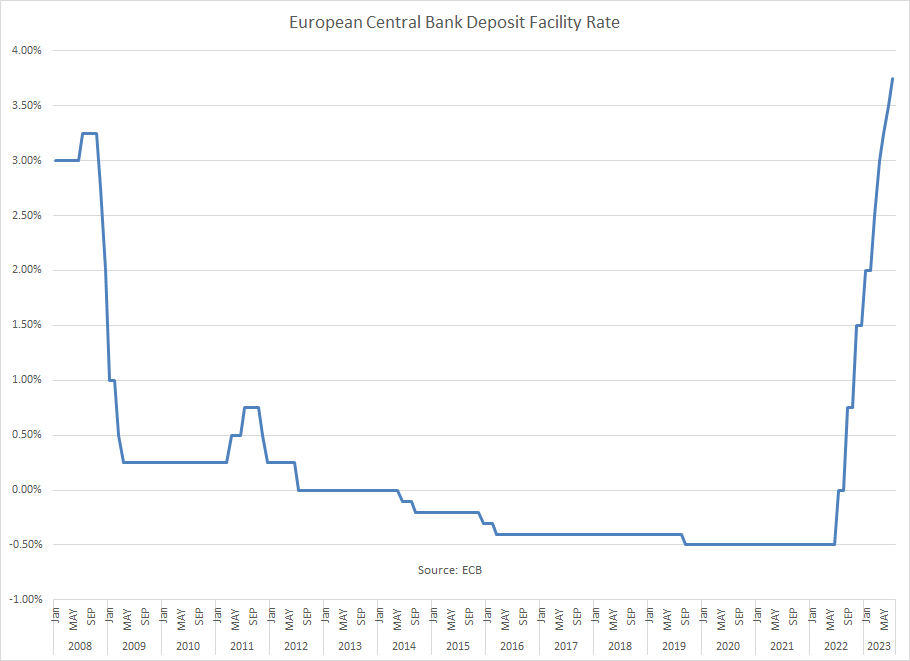

In 2014 the ECB was the first central bank to use negative interest rates when they cut their Deposit Facility Rate to -0.10%. They were concerned about deflation.

Core Euro Area CPI

{kind=link}

Prices remained stable until late 2021 when inflation flared up. It continued to climb, but the ECB was slow to respond. It wasn’t until July 2022 when the core Euro area CPI hit 4.0% that the ECB reacted by raising rates for the first time in eleven years.

{kind=link}

Over the past 13 months they have hiked their Deposit Facility Rate nine times for a total of 425 basis points. The rate hikes have only had minimal impact on the core CPI as it remains at the elevated level of 5.5%.

In their 2022 annual report the ECB states “The higher rates in turn affect the profits of the ECB and of the national central banks of the euro area countries, and may even result in financial losses. This is due to the fact that, in the short and medium term, the cost of the liabilities on central bank balance sheets is more sensitive to interest rates than the income generated by their assets.”

The ECB and their Eurosystem NCBs also have an asset/liability mismatch.

In 2022 the ECB incurred a loss from operations of 1.6 billion euro due to the mismatch and the rise in interest rates. Fortunately, they were able to offset this with their loss provision that they had accrued on their balance sheet. They reported a net income of zero.

While they still have a loss provision of 6.6 billion remaining, it is not clear if it will be sufficient to cover the expected operating losses going forward.

One problem the ECB has with its APP portfolio is that a large number of securities were purchased during the pandemic when yields were negative. They don’t earn income on those holdings. Now that the cost of their Deposit Facility is 3.75%, and rising, their interest expense is much greater, so their losses will be larger.

{kind=link}

Of course, these securities are also suffering from a loss in market value as interest rates have risen. The ECB, though, like the Fed, utilizes an amortized cost accounting method, so the losses are unrealized on their balance sheet. Nonetheless, the losses are significant.

The ECB is also reducing their balance sheet through QT, although the process is slow. Since the peak in 2Q22, the balance sheet has shrunk by 19% to 7.2 trillion euro.

Bank of Japan

The Bank of Japan (BOJ) was the first central bank to implement QE, and they’ve been employing it for more than twenty years. It was used because of weak economic growth and deflationary pressures.

Core Core CPI

{kind=link}

In 2016 the BOJ adopted a Yield Curve Control ((YCC)) plan where the Policy Rate was cut to -0.10% and the 10-year Japanese Government Bond ((JGB)) yield was fixed at 0.0%. The BOJ stated that they would maintain YCC as long as was necessary to achieve its 2.0% inflation target in a stable manner.

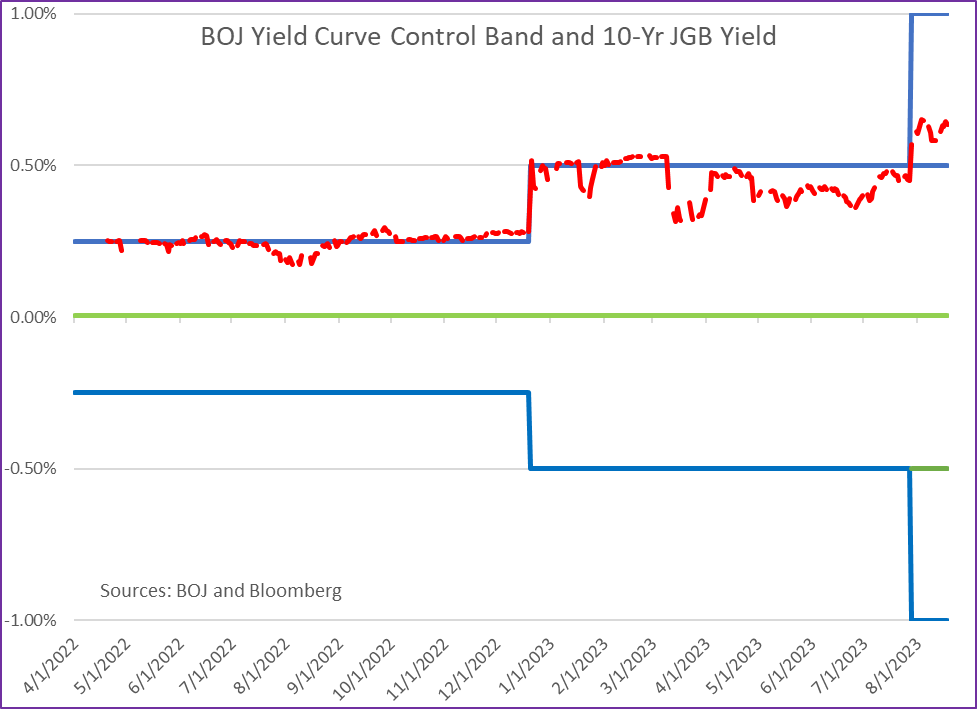

In establishing the 0.0% 10-year yield target, the BOJ created a +/- 10 basis point band around it, to accommodate fluctuations. The BOJ promised to intervene with unlimited amounts of JGB purchases to defend it. Over the years, when pressure mounted against the band, it was widened without changing its target yield of 0.0%

YCC was created in a deflationary environment as a way to bring inflation up. That didn’t happen until 2022 when Japan’s preferred inflation indicator, the Core Core CPI surged above the 2.0% target. With high inflation, speculators began making big bets that the BOJ would have to abandon their QE policies and tighten by raising rates.

But the BOJ remained steadfast, and maintained their easy policies.

The pressure from speculators forced the BOJ to intervene heavily in the markets to keep the yield on the 10-year JGB within the band. When pressure became too intense and interventions in the market forced greater purchases than desired, the BOJ made small concessions and widened the band. In 2018 the band was expanded to +/- 20 bps, then in 2021 it was widened to +/- 25 bps, then in 2022 it was widened to +/- 50 bps, and finally in July 2023 it was widened further to +/- 100 basis points.

These changes to the band were referred to as “tweaks” by the BOJ and not a change in policy. Throughout, the BOJ’s Policy Rate has remained at - 0.1% and the target rate for 10-year JGBs had remained at 0.0%.

The past two “tweaks” came as complete surprises to the market, as the BOJ wanted to keep the speculators at bay and catch them off-guard. Nevertheless, the pressure to change policy remains.

{kind=link}

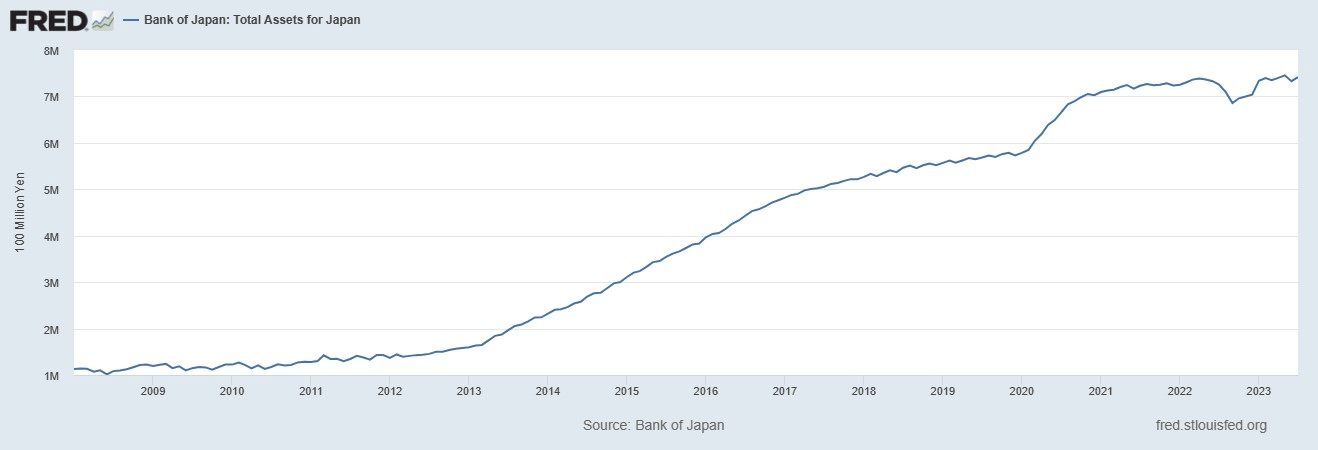

Despite the fact that inflation is 4.3%, more than double the desired level, the BOJ has remained the only central bank in the world with QE still in force. While other central banks are reducing the size of their balance sheets through QT, the BOJ’s balance sheet continues to grow.

{kind=link}

For a detailed description of YCC, please see my Seeking Alpha article “How the Bank of Japan Lost Control of Their Yield Curve Control Policy” here.

Because the BOJ has not raised short rates, unlike every other central bank, they are not suffering from net operating losses.

However, they do have a balance sheet problem with unrealized bond losses (they too use amortized cost accounting.)

For FYE 3/31/23 the BOJ reported an unrealized loss on JGB’s for the first time in 17 years amid rising bond yields. The paper loss was 157 billion yen, versus a paper profit of 4.373 trillion yen the prior year. This is a 4.53 trillion yen decline in value over the year, as the 10-year JGB yield increased by 12 basis points.

As seen in the chart below since FYE23 the 10-yr JGP has increased by 30 basis points, so we estimate that the unrealized portfolio loss year-to-date could approximate 9 trillion yen. This is more than double the BOJ’s capital. Further increases in yields will only intensify the problem.

{kind=link}

In recent testimony, BOJ Deputy Governor Amamiya stated that if the entire yield curve shifted by 100 basis points the BOJ’s unrealized loss would increase by 29 trillion yen.

Conclusion

World Central Banks have been raising short-term interest rates aggressively for the past eighteen months to fight inflation. All of this tightening, however, has created a problem for the central banks.

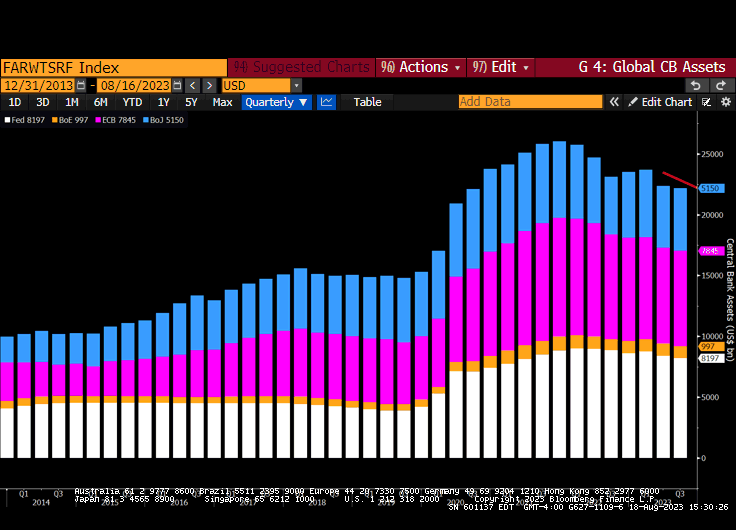

Over the past 15 years, the central banks, through the execution of their QE monetary policy, have become the largest asset managers in the world. For the Federal Reserve, the Bank of England, the European Central Bank and the Bank of Japan, their cumulative holdings now total $22 trillion.

These four entities together own 33% of the entire Bloomberg Global Aggregate Bond Index.

{kind=link}

The central bank earnings, after covering operating expenses, are remitted to their respective Treasuries. Over the past twenty years the Fed has given back an average of $63 billion a year to the US Treasury, while the BOE has transferred GBP 123 billion to the Treasury since QE began. Starting last year, however, due to the asset/ liability mismatch, the higher short-term rates have turned those earnings into losses.

This year the Fed, for the first time since 1915 will not transfer its earning to the US Treasury, while the Bank of England, for the first time ever, received an indemnity payment from the Treasury to cover losses.

Additionally, the rise in interest rates has caused the value of the central bank portfolios to decline. Whether the central bank uses amortized cost accounting or mark-to-market accounting, the value of the central bank portfolios have fallen sharply.

We estimate that the Fed has an unrealized loss of $1.3 trillion in their SOMA portfolio, with the other central banks also suffering significant declines in the market value of their holdings.

Many central banks are now normalizing their policy through QT to reduce their balance sheets in order to minimize the asset/liability mismatch.

Many argue that central bank losses don’t matter because the central banks can always create reserves to meet their obligations. They will always remain solvent.

While this is true, it does not tell the whole story. Creating reserves is inflationary and it exacerbates the problem the central banks are trying to control.

The central bankers downplay this situation and act as if this is business as usual. It is not.

They say the operating losses and balance sheet losses will not impair their ability to conduct monetary policy.

In the short run, this may be true.

But the losses do have consequences.

Ultimately, it is the taxpayers who will bear the brunt of these losses in the form of higher taxes.

Currently, the public is not well informed about the problems the central banks are experiencing, as they are not mentioned in the financial press, and the central bankers won’t talk about them.

The Kansas City Fed will be hosting their Annual Economic Symposium in Jackson Hole, Wyoming on August 24-26, which will be attended by central bankers from around the world and will feature an address from Fed Chairman Powell. Don’t expect a discussion of central bank losses to come up.

Another consequence is the political ramifications of the losses. Once congress grasps the impact the Fed’s losses will have on the Treasury by widening the budget deficit, they will make waves. This is already beginning. Senator Rick Scott, R-FL, recently penned an op-ed chastising the Fed and Chairman Powell for losing $1 trillion in taxpayer money. Further pressure from congress will hamper the Fed’s independence.

The situation is best summed by Jacques de Larosiere, a former Managing Director of the IMF, Governor of the Banque de France, and President of the European Bank for Reconstruction and Development, who said:

“By their management of monetary policy, central banks have contributed to inflation and helped to undermine the financial system.”

“Central banks have weakened their own balance sheets, as well as their reputation and independence.”

For further details see:

The Financial Deterioration Of World Central Banks - Racking Up The Losses