VTI - The Fundamentals-Based Consumer Nowcast: Expansion Continues

2023-08-10 09:25:28 ET

Summary

- The consumer nowcast system analyzes consumers' ability to spend and predicts recessions based on their spending patterns.

- Real consumer earnings have been increasing since June of last year, indicating a positive outlook for consumer spending.

- Refinancing options are currently limited, but appreciating assets like houses and stocks may provide a new source of consumer cash.

- Until inflation overtakes wage growth, consumers are very unlikely to cause a recession.

Introduction

As you may already know, I have a variety of systems for tracking the economy - including high-frequency weekly indicators, an array of short leading indicators, and the primary system of long leading indicators which I typically update at least twice a year.

In most recent weekly high-frequency updates, I have promised a comprehensive update of all of my systems, "marking them to market" against current conditions. I have already done so with the long leading indicators, showing that a majority of them are still negative...

Most of those systems rely on a cycle of long-leading, then short-leading indicators, followed by coincident, short-lagging, long-lagging, and finally mid-cycle indicators - and then around to long leading indicators again. But I also have a fundamentals-based system which I call "the consumer nowcast." That is the subject of this post.

The consumer nowcast looks at the ability of consumers - 70% of the economy - to spend. When that ability is temporarily tapped out, and consumers pull back, a recession quickly follows. I have been writing about this "consumer nowcast" system for over 15 years, when it did not signal a problem in 2005-06, but did signal trouble in 2007.

Here's how the consumer nowcast works: in order to spend, consumers have to be making more money in real, inflation-adjusted terms. If they can't do that, they can refinance debt at lower interest rates, thus freeing up additional cash to spend. If they can't do that, they can cash in appreciating assets like houses and stocks. But if all of those avenues are closed off, consumers have no choice but to pull back; and when they spend less, manufacturers and suppliers quickly notice, cutting back production and supply; and a recession ensues.

So how does the consumer nowcast stand now?

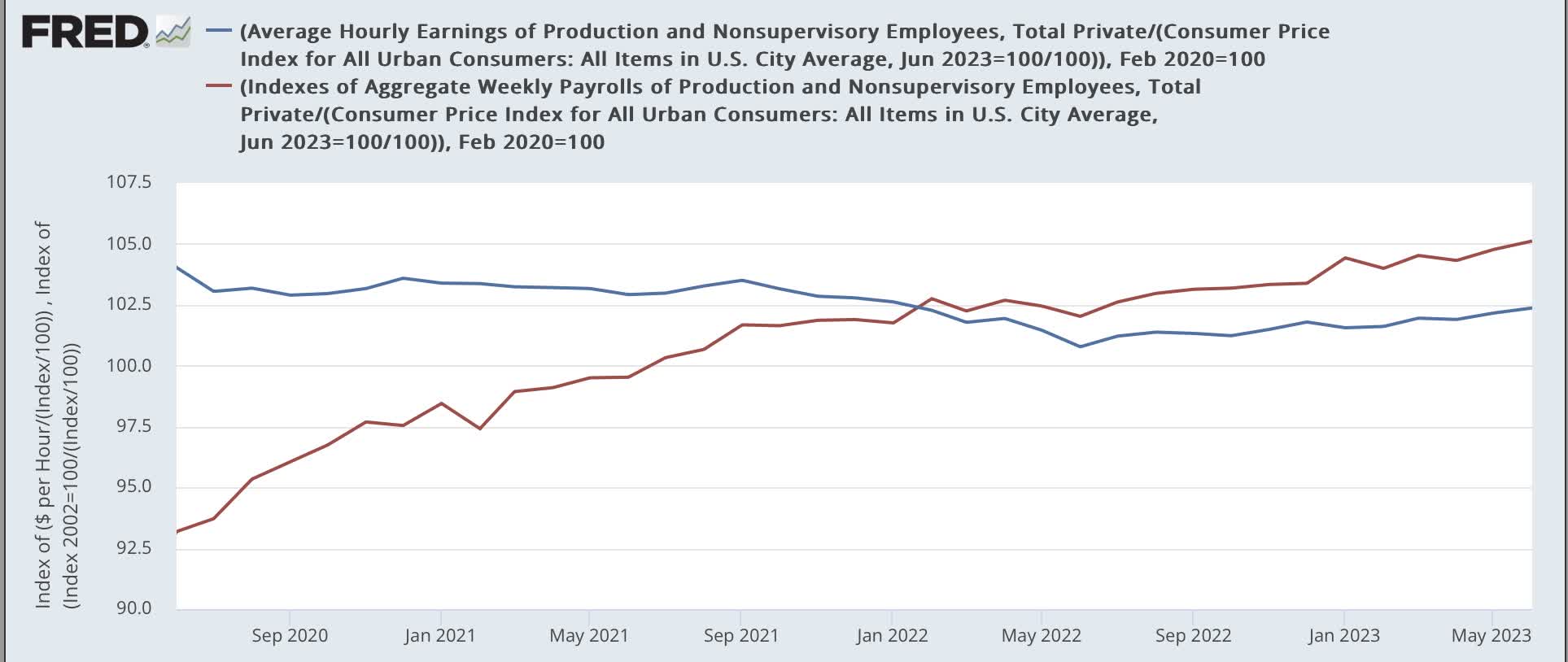

To begin with, real consumer earnings, whether measured as real average hourly earnings, or real aggregate payrolls, have increased since June of last year:

Real average hourly wages, real aggregate payrolls, 2022-23 (FRED)

{kind=link}

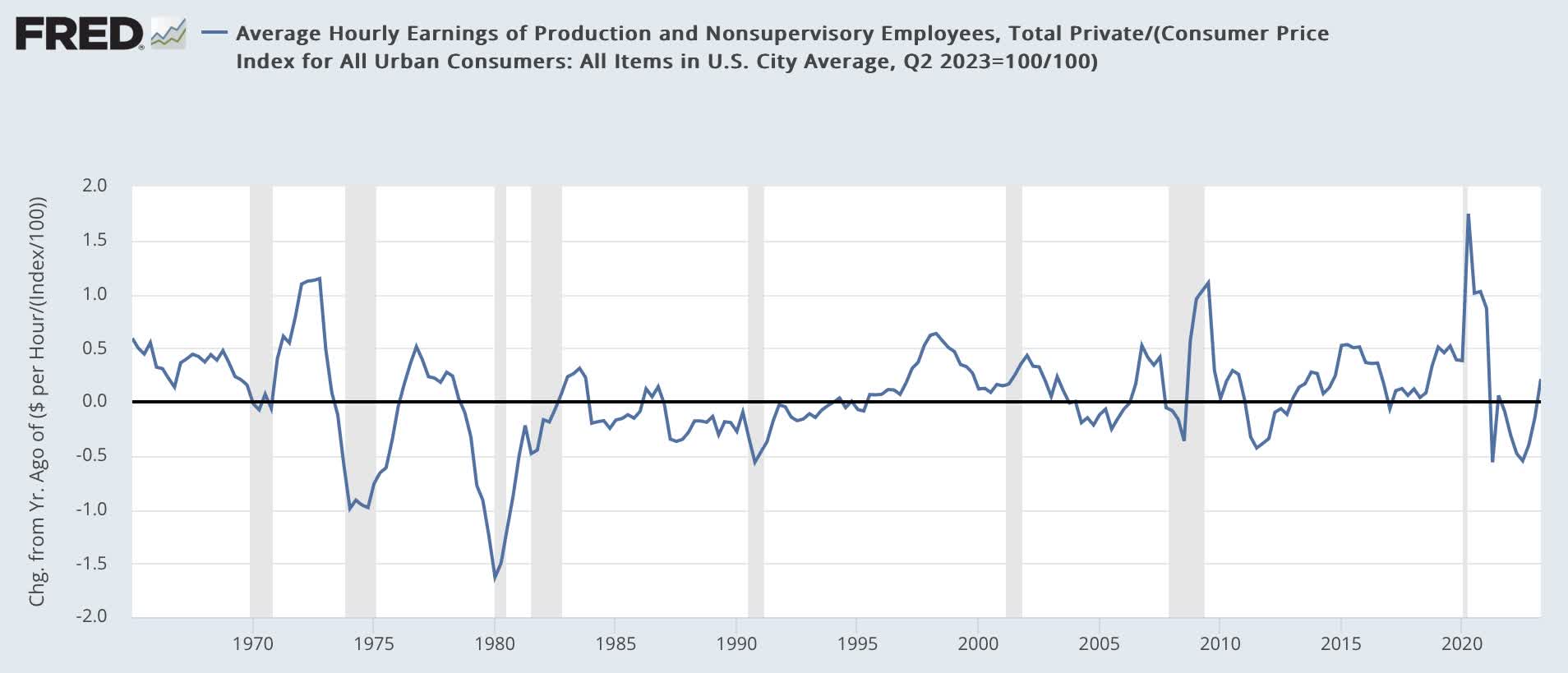

In the case of hourly earnings, the decline is a reversal from 2021-22, but real aggregate earnings, with the exception of the first half of 2022, have been increasing since the worst days of the pandemic. Looking back 60 years to the inception of the series, real average hourly earnings have almost always either been in the midst of a long-term downdraft, or else have turned flat or down shortly before the onset of every recession, as shown in this YoY comparison:

Real average hourly wages, Q/Q % change (FRED)

{kind=link}

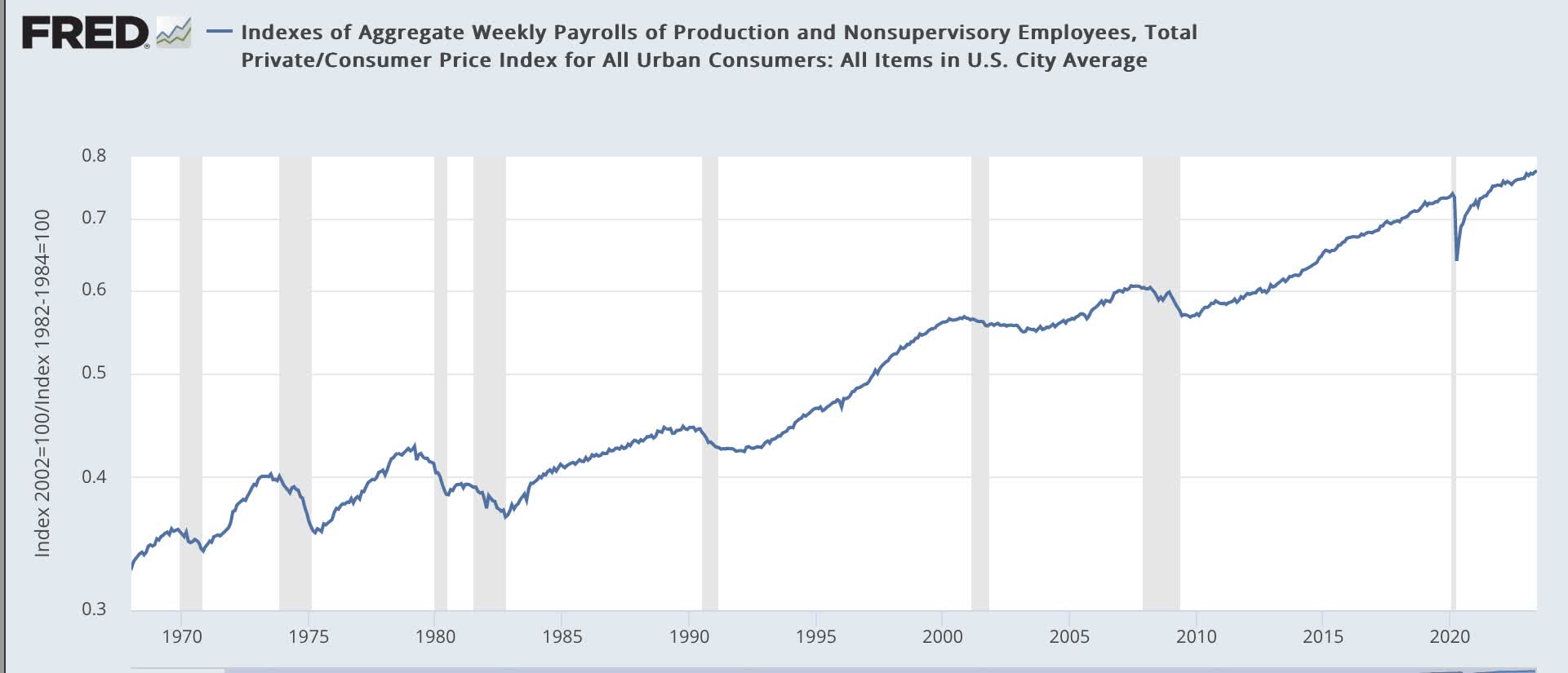

Even more important, going back over 50 years, so long as aggregate payrolls are increasing more than consumer inflation, no recession has occurred. It is only once inflation has caught up with payrolls that consumers have cut back and a recession has started. The lag between the real payrolls peak and the onset of recession has varied between 4 and 10 months:

Real aggregate payrolls (FRED)

{kind=link}

The consumer nowcast further posits that, if wages aren't going up, do consumers have other options, like refinancing or equity withdrawal, to fund new purchases?

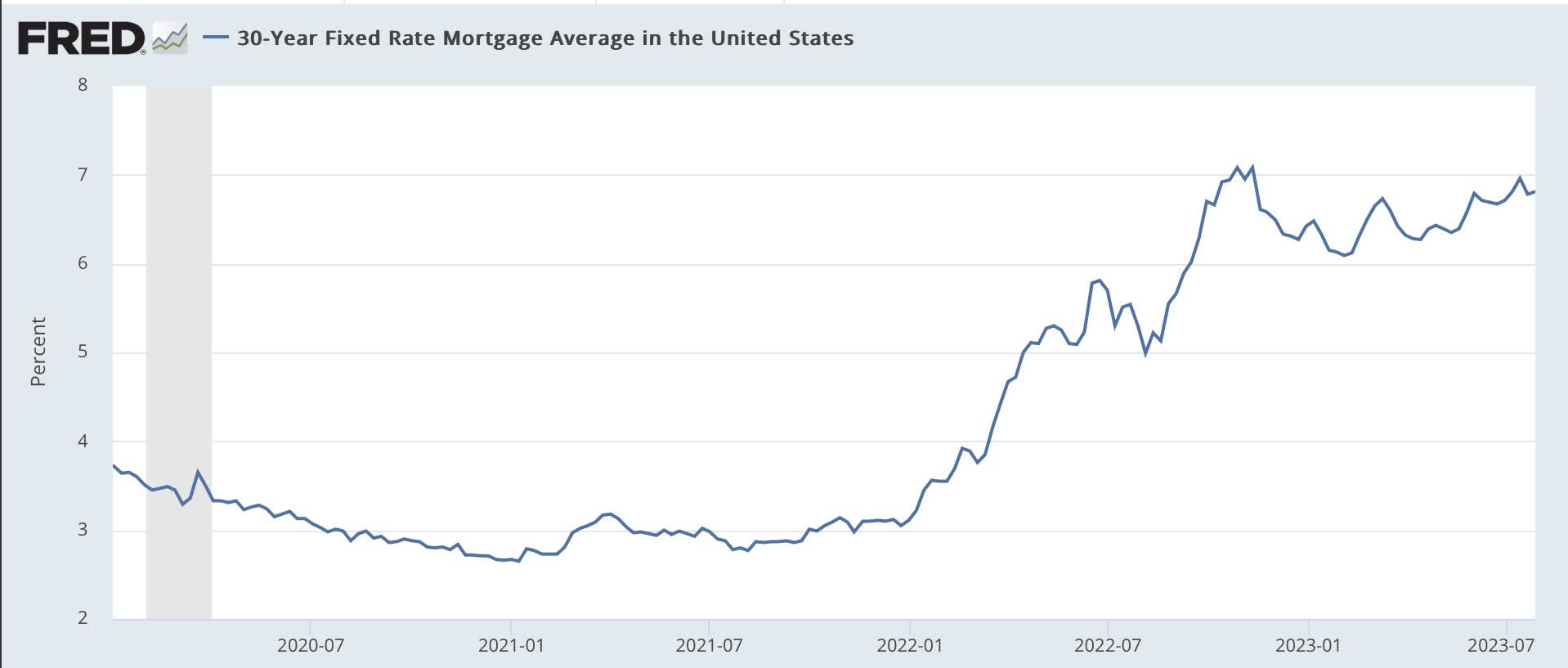

So let's consider the ability of consumers to refinance debt or cash in appreciating assets in order to free up cash to spend, in case there were a reversal in real earning power.

As of now, the refinancing option is firmly shut down. In case you've been hiding under a rock, here are mortgage rates for the past several years:

{kind=link}

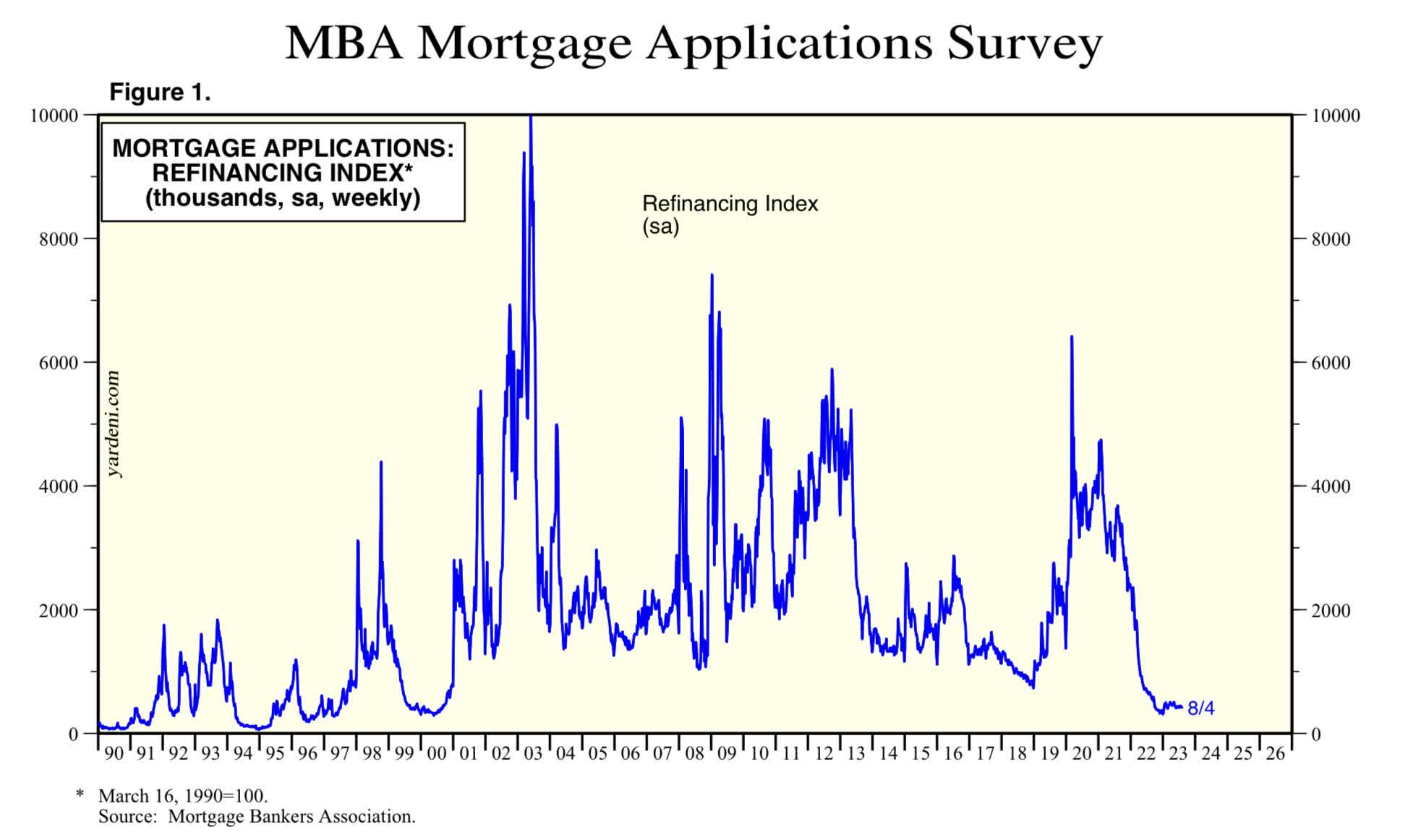

Further, according to Edward Yardeni , refinancing of mortgages since late last year has been at 20+ year lows:

Mortgage Refinancing (Yardeni.com)

{kind=link}

So, for the moment, refinancing at lower interest rates is not a significant driver of new consumer cash.

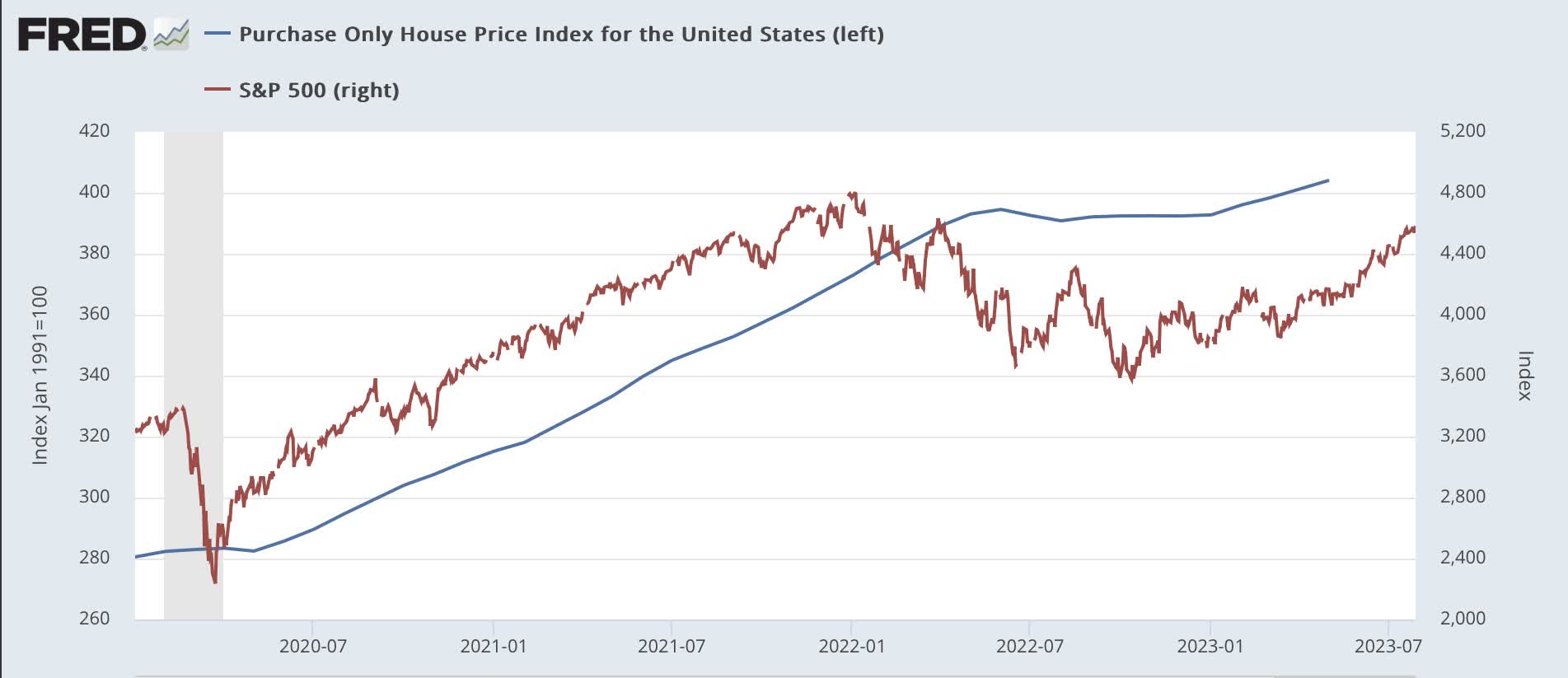

But appreciating assets are also on the cusp of opening up a new source of consumer cash. Here's what house prices as measured by the FHFA (blue) and stock prices (red) look like:

FHFA house price index. S&P 500 (FRED)

{kind=link}

After declining through earlier this year, house prices, depending on the measure, are either just slightly below, or just slightly above their recent records from earlier 2022.

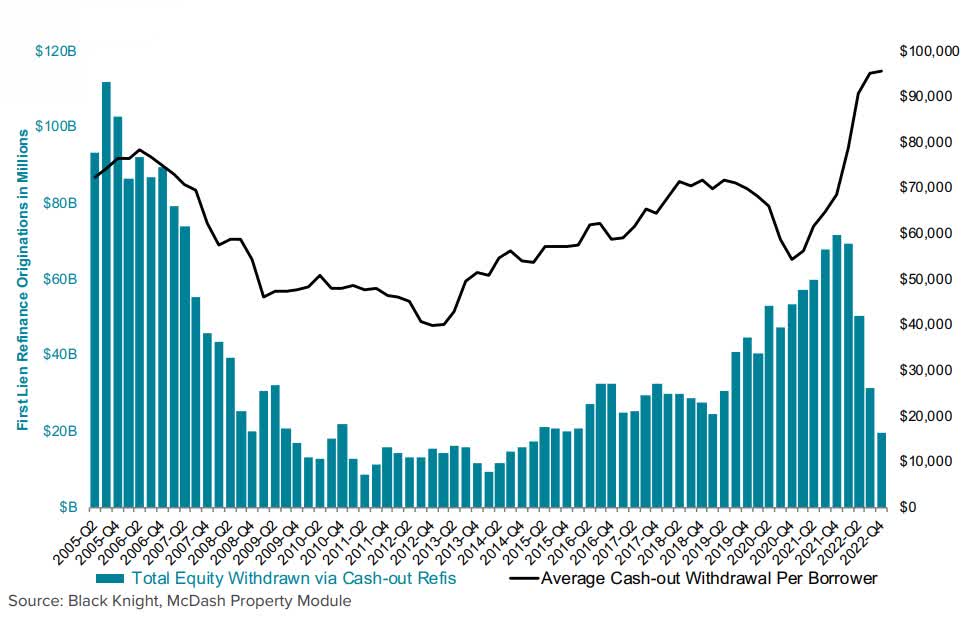

As of earlier this year, cash-out home refinancing had declined sharply:

Cash out refi's (Black Knight, McDash Property)

{kind=link}

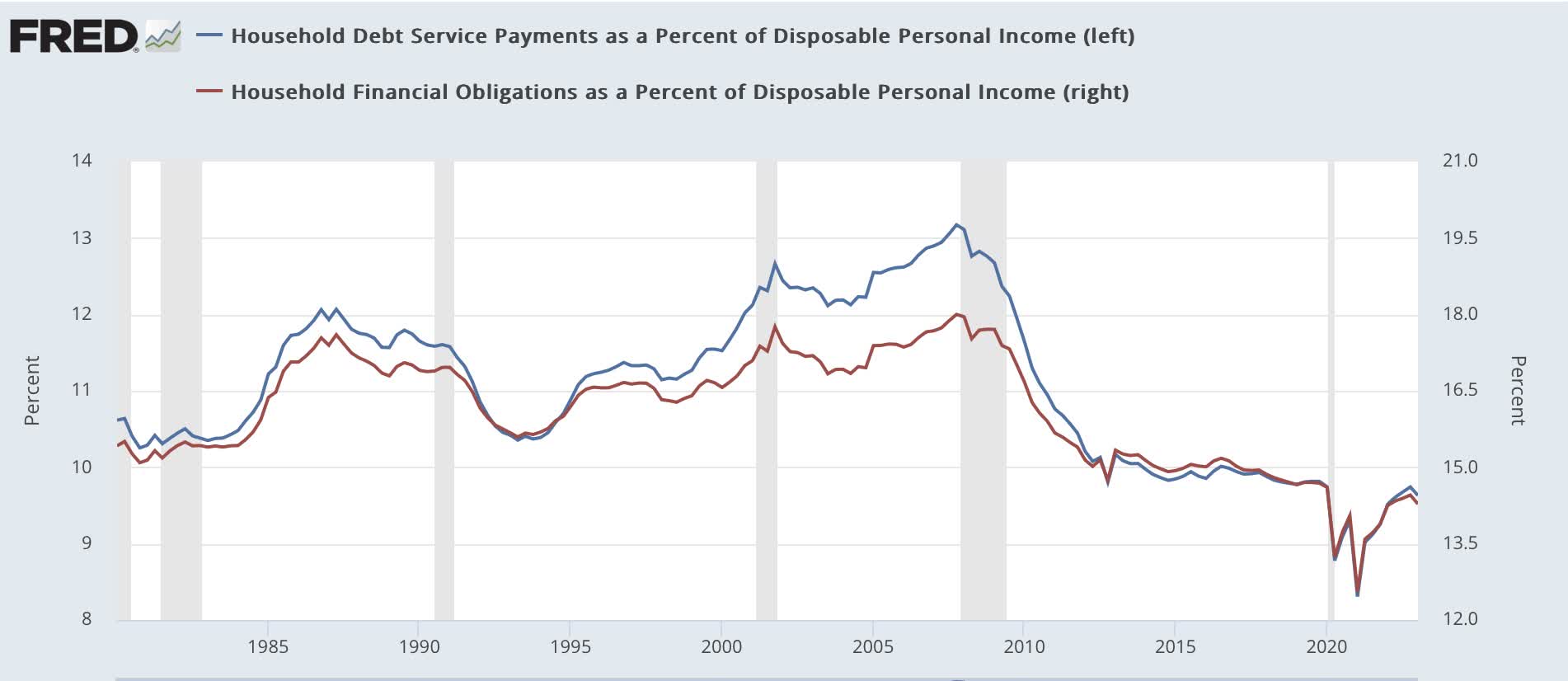

Finally, household debt obligations, although low by historical standards, increased sharply as a percent of income in 2021-22. As of the most recent update for Q1 of this year, households had become slightly more conservative:

Household debt measures (FRED)

{kind=link}

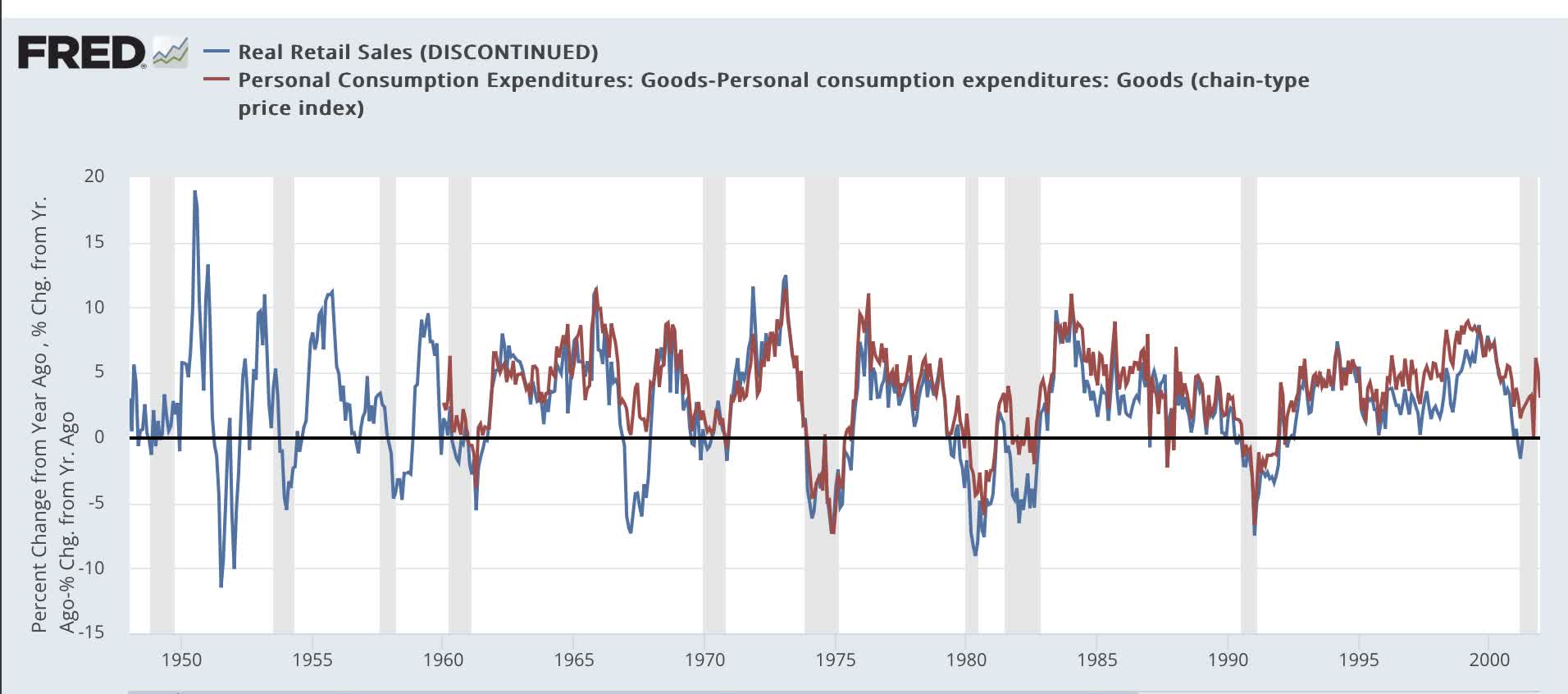

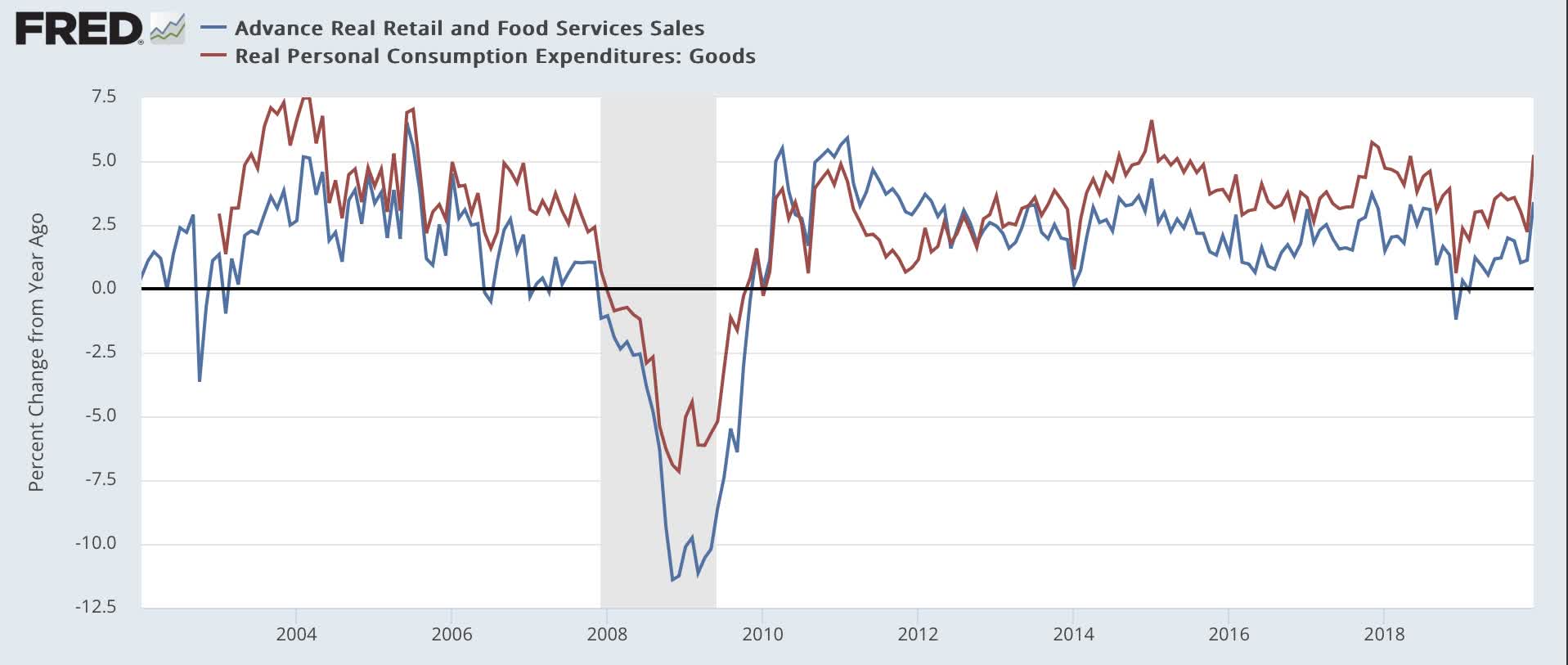

Perhaps unsurprisingly, given this mixed picture, measuring real retail sales vs. real personal spending on goods gives somewhat differing results. Real retail sales have always been negative YoY before the start of a recession, with few false negatives. Real personal consumption on goods has typically been negative or at least soft, at 1.5% higher YoY or less, when recessions have begun:

Real retail sales vs. real personal spending, 1948-2000 (FRED) Real retail sales vs. Real personal spending, goods, 2001-19 (FRED)

{kind=link}

{kind=link}

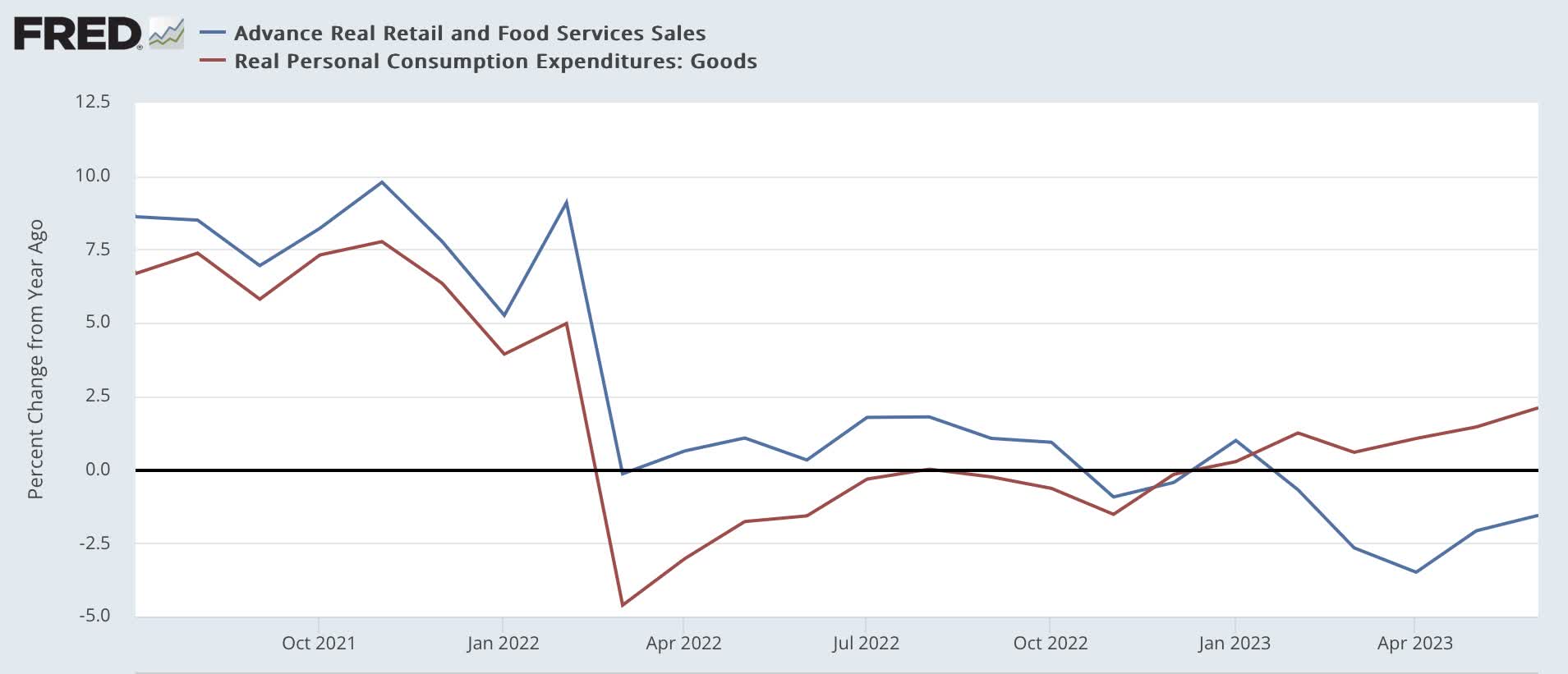

Real retail sales have declined almost relentlessly since spring of 2022 and are at recessionary YoY levels, while real personal spending on goods is positive, slightly exceeding levels at which recessions have started previously:

Real retail sales vs. real personal spending on goods, 2022-23 (FRED)

{kind=link}

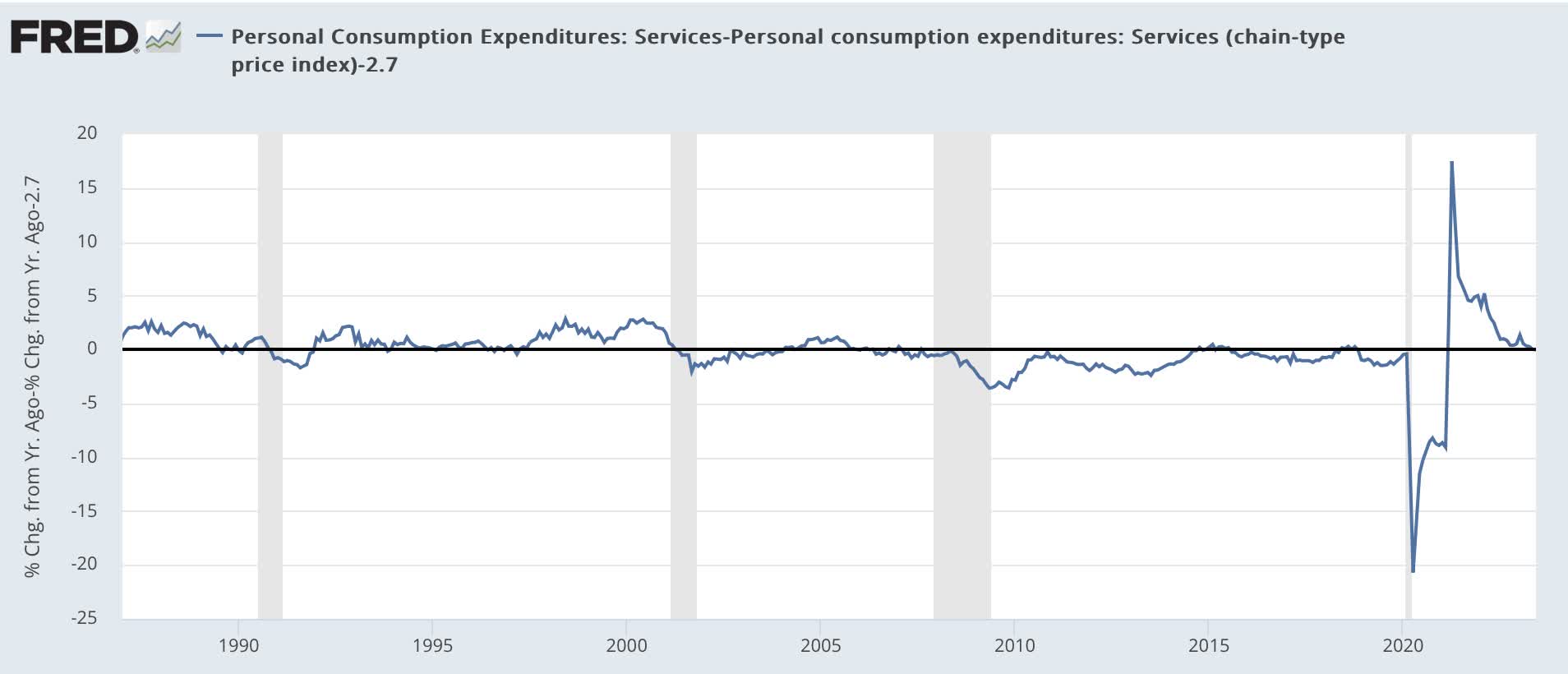

If consumer spending on goods has not been strong, real consumer spending on services, at 2.7% higher YoY, is still growing at rates rarely seen since the turn of the Millennium:

Real consumer spending, services (FRED)

{kind=link}

Conclusion

The consumer nowcast shows just how important the big deceleration in consumer inflation has been since its peak, along with $5 gas prices, in June 2022.

Although their ability to refinance debt at lower rates is virtually non-existent, rebounds to near record highs in both stock prices and real estate prices are opening the doors to another round of cashing in stock options and cash-out refinancing. While there is some sign of increased consumer caution, in real terms they have had more money to spend almost every month in the past 12 months.

Remember, this is not a forecast, but only a fundamentals-based nowcast. But to put a bullet point on it: so long as inflation continues to decelerate more than wage and payroll growth, consumers are not going to start a recession.

For further details see:

The Fundamentals-Based Consumer Nowcast: Expansion Continues