LEVI - The Gap Surges On Strong Q3 Earnings: Why I Am Cautious

2023-11-17 00:36:28 ET

Summary

- The Gap, Inc. shares rose sharply following a better-than-expected Q3 2023 report.

- The company delivered impressive gross margin and operating margin improvement during the quarter.

- GPS is trading at a premium valuation compared to peers and historical norms, but I believe consensus estimates will be raised, bringing GPS' valuation back inline.

- GPS has not repurchased any shares over the past year, despite the fact that the company is sitting on a significant amount of cash.

- I am initiating GPS with a hold rating.

Shares of The Gap, Inc. ( GPS ) are trading higher by ~14% following the company's better than expected Q3 2023 earnings report. This move comes on top of what has already been a strong past few months for the stock.

As of this writing, based on the current trading price of $15.67, GPS shares are up ~117% from the 52 week low of $7.22 which was reached on May 25, 2023.

While the Q3 results were impressive, I believe the rally presents a selling opportunity as the secular themes that have resulted in long-term underperformance remain in place. Even after the recent rally, GPS shares have still delivered a 5 year total return of -35% compared to a return of 79% delivered by the S&P 500.

Following the Q3 earnings beat, GPS now trades at ~17.4x consensus FY 2024 earnings. While consensus FY 2024 numbers are likely to be raised to some degree, the stock will likely still be trading at a premium valuation to most peers and at a forward earnings multiple which is only modestly less than the S&P 500. Simply put, I believe GPS shares are now fully valued and do not represent a buying opportunity.

Q3 2023 Results

GPS reported Non-GAAP EPS of $0.59 which beat estimates by $0.39. However, the $0.59 represents a ~17% decline from the $0.71 reported during the same period a year ago. Revenue came in at $3.8 billion which beat estimates by $190 million, but represents a 7% decline on a year-over-year basis. The sales decline is inclusive of an estimated 2% negative impact from the sale of Gap China. Comparable sales were down 2%.

Store sales decreased by 6% compared to the same period a year ago. Online sales decreased by 8% from the same period a year ago and accounted for 38% of total sales.

In terms of brand performance Old Navy fared the best with comparable stores sales up 1% on a year-over-year basis, while Athleta fared the worst with comparable store sales falling 19% on a year-over-year basis.

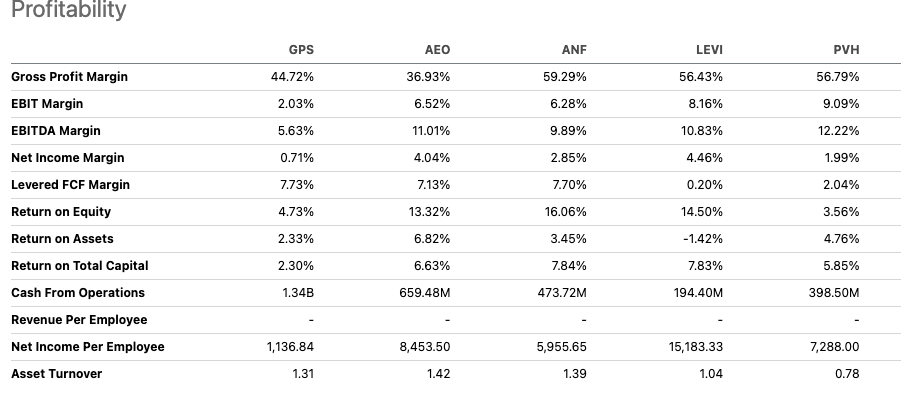

Gross margins came in at 41.3% which was a 390 basis point improvement vs the same period a year ago. Adjusted operating margins came in at 6.8% compared to 3.9% during the same quarter a year ago.

GPS CEO Richard Dickson noted the company's strong operational performance during the quarter on the conference call :

Let’s start with maintaining operational and financial rigor.

As you know, this has been a core priority, and we’ve made significant progress which has strengthened our financial footing. Examples of this work include, actioning over $550 million in expected annualized cost savings, realizing margin expansion through lower air costs, improved discounting and more effective sourcing strategies combined with recovery of commodity costs, and we’ve reduced our inventory by nearly $800 million versus last year’s peak.

Our efforts to date have resulted in better working capital and a stronger balance sheet, and this discipline of controlling the controllables will continue to be a priority for us as we aim to increase the consistency of our performance both near- and long-term. Our focus on operational and financial rigor benefited our third quarter results, particularly in terms of improved margins, expenses, and cash flow

In terms of guidance GPS reaffirmed prior guidance which called for FY 2023 sales to be down in the mid-single digit range compared to FY 2022 sales of $15.6 billion which included ~$300 million in sales for Gap China. GPS expects gross margin expansion for FY 2023 by ~200bps compared to FY 2022. The company expects to open a net total of 15 to 20 Old Navy and Athleta stores in FY 2023 while closing a net total of 50 Gap and Banana Republic stores. With these store closures the company will complete its previously announced plan to close 350 Gap and Banana Republic stores in North America by the end of fiscal 2023.

Highly Competitive Industry Leads to a Thin Moat

GPS operates in a highly competitive apparel retail industry. Gap competes with companies such as Macy's ( M ), Nordstrom ( JWN ), PVH ( PVH ), Kohl's ( KSS ), American Eagle ( AEO ), Abercrombie & Fitch ( ANF ), Lululemon ( LULU ), Zara, Ascena Retail Group, J Crew, and many others.

As a result of high levels of competition it is difficult for companies to create a sustainable competitive advantage. Additionally, the entire industry has faced secular challenges relating to a shift away from physical shopping towards online shopping.

As a result of these challenges GPS has been able to generate only mid single digit profit margins on average. GPS has also struggled to grow revenue and earnings over the past decade.

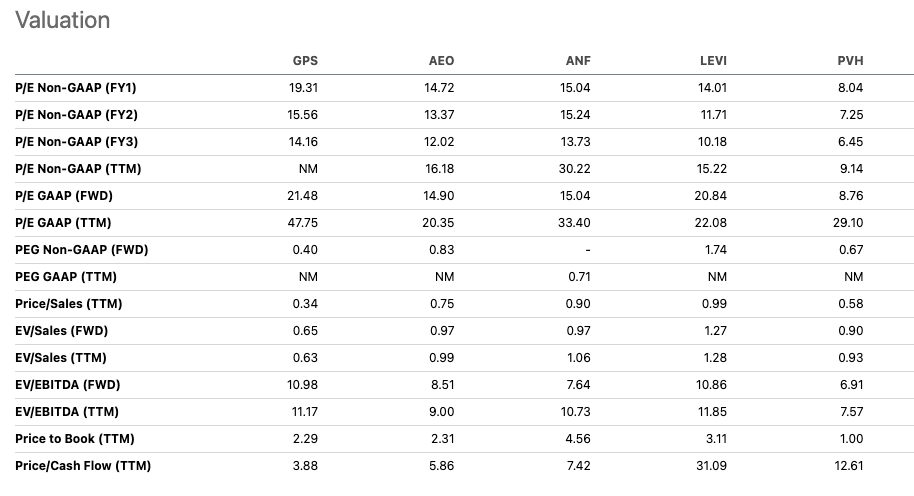

Valuation

Based on a current stock price of $15.67 GPS is trading at 17.4x consensus FY 2024 earnings of $0.90 per share and 21.5x consensus FY 2023 earnings. Comparably, the S&P 500 is trading at ~18.4 consensus 2024 earnings. Thus, GPS is currently being valued at essentially a market multiple. However, I expect analysts to raise FY 2024 earnings estimates over the next few days in response to GPS's margin improvement.

Currently, consensus net profit margin estimates for FY 2024 are ~2.2% (based on a $0.90 EPS estimate and $14.79 billion revenue estimate). I believe a net profit margin of closer to 3% may be attainable for FY 2024 which would imply EPS of ~$1.20 per share. Based on this level of EPS GPS would be trading at closer to 13x 2024 earnings.

I believe this valuation is too high given GPS failures to deliver revenue and earnings growth historically. While GPS Q3 results were better than expected, the company continues to report declining sales and earnings on a year-over-year basis.

As shown by the table below, GPS is now trading at a premium valuation to its peers based on key metrics such as forward P/E (even assuming a 13x rate). I don't believe this premium is warranted as GPS has generally underperformed is peers historically. Moreover, GPS has of late struggled operationally which has resulted in lower margins vs peers.

In addition to trading at a high valuation relative to peers, GPS is also now trading at an elevated valuation vs its recent historical norms. However, I expect this GPS's forward P/E to move closer to the average historical value after analyst estimates are raised.

{kind=link}

{kind=link}

Capital Allocation

Despite significant share price weakness over the past year, GPS has not bought back any stock. However, the company has continued to pay out a $0.15 per share quarterly dividend.

At current levels, GPS stock yields ~3.8%. While this is a nice dividend, the company's continued decision to focus on the dividend as opposed to share repurchases suggest that management does not view GPS stock as undervalued. Additionally, GPS is currently sitting on $1.4 billion of cash (relative to a ~$5 billion market cap) which could have been used to repurchase shares if the company thought that its stock was undervalued.

Potential Upside Catalyst

The biggest potential upside catalyst I see in the near term would be if GPS is able to maintain recent profit margin improvements. Historically, the company has struggled to do so but even a small improvement in margins has potential to drive a significant improvement in earnings over the near-term.

Prior to the covid disruption GPS had been able to achieve profit margins in the mid single digits. Given the recent margin improvement it does not seem impossible that GPS could return to that level of profitability. Moreover, peers have generally been able to operate at margins closer to 3% and thus that level of profitability may be obtainable in the near-term for GPS.

That being said, margin improvement can help financial performance in the near-term but only to a degree. If revenues continue to decline going forward it will be difficult for GPS to hand onto any near term margin improvement.

Conclusion

GPS reported excellent Q3 results which easily surpassed Wall Street expectations. In response to this, GPS shares have rallied sharply and are now trading at a premium valuation relative to historic norms and other apparel retail companies.

The most impressive part of GPS earnings report was the significant improvement in operating margins from the same period a year ago. Over the past few years GPS has struggled to generate positive profit margins and has underperformed peers which have been able to generate low single digits profit margins.

While GPS appears to be very expensive based on current consensus 2024 earnings, I believe analysts will raise FY 2024 numbers. The result of this is that GPS will be more reasonably valued compared to peers and its own history.

I believe that the long-term outlook for GPS remains challenged due to high levels of competition in the apparel industry and a secular shift away from in store shopping towards online. However, GPS has made significant progress with its online business which accounts for 38% of total sales.

The fact that management has prioritized dividends over buybacks despite a very high level of balance sheet cash suggests that the management team does not view GPS stock as highly undervalued. I believe this is an important indicator as the management team has the best insights into what the future looks like for GPS.

For these reasons, I am initiating GPS with a hold rating. I would consider downgrading the stock if the company fails to hold onto recent margin improvements in the coming quarters. I would consider upgrading the stock if the company is able to continue improving margins and return to revenue growth.

For further details see:

The Gap Surges On Strong Q3 Earnings: Why I Am Cautious