GEO - The GEO Group: The Stock Looks Cheap With Title 42 Upside Optionality

2023-03-09 13:38:11 ET

Summary

- GEO could see a huge boost if and when Title 42 border regulations expire.

- The company faces renewal risks, but has managed to navigate them despite a Biden executive order aimed at private prison operators.

- GEO stock looks cheap based on historical levels.

While controversy surrounds prison stocks such as The GEO Group ( GEO ), the stock looks inexpensive and an eventual end to Title 42 border regulations could be a huge boost for the stock.

Company Profile

GEO owns, leases, and manages prisons, processing centers, and community reentry facilities in the U.S., Australia, and South Africa. The facilities can range from minimum security to maximum security. The company operates in four segments: U.S. Secure Services segment; Electronic Monitoring and Supervision Services; Reentry Services; and International Services.

In some cases, GEO will own and operate a detention facility, while with other contracts it may just manage a facility that it does not own. The company also has other services such as electric monitoring, as well as post-release support services.

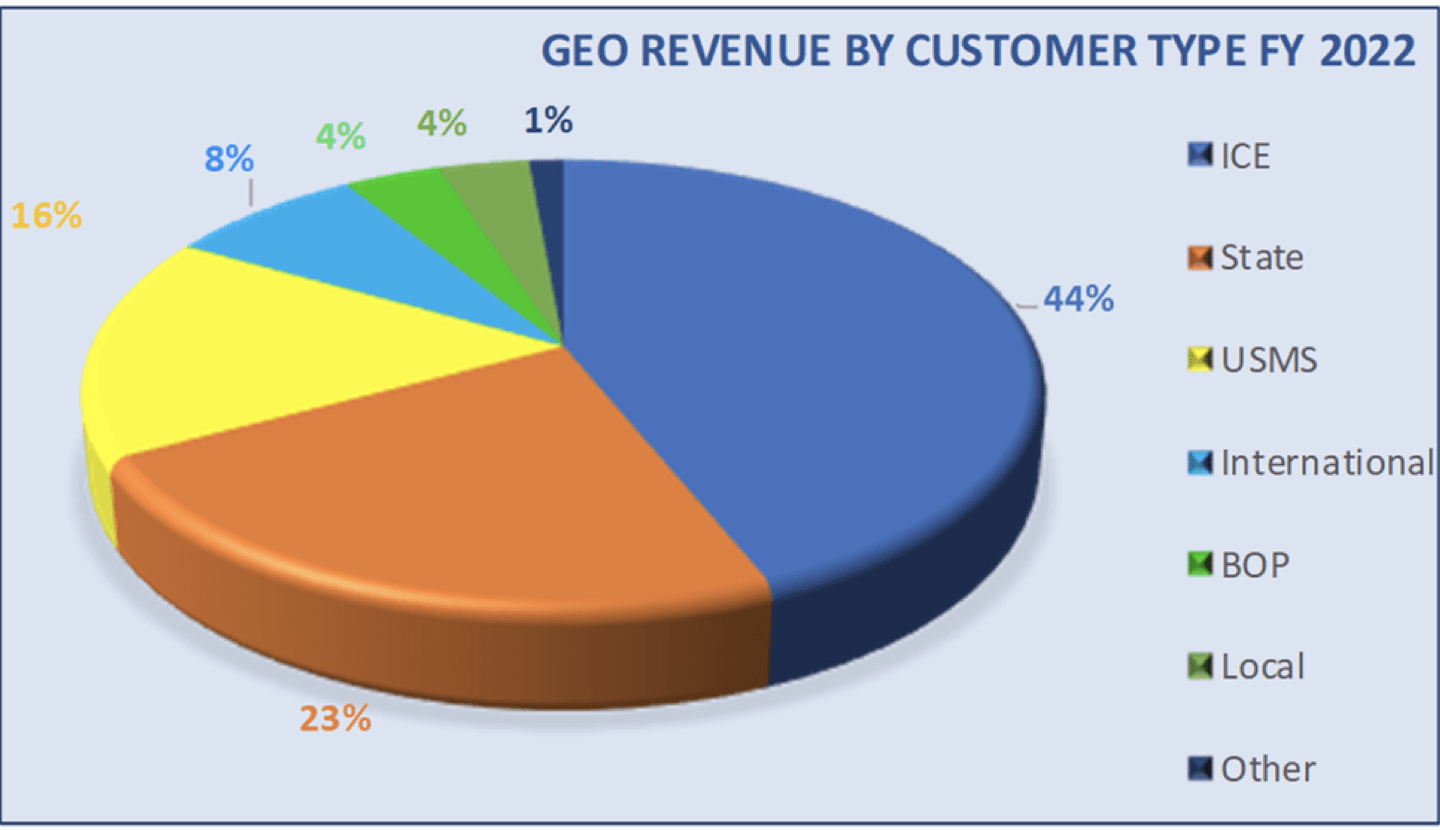

GEO’s largest customer is U.S. Immigration and Customs Enforcement, or ICE, which accounts for about 44% of its revenue and 29% of its beds. U.S. Marshal Services make up another 16% of revenue and 18% of beds, while the Federal Bureau of Prisons represents nearly 4% of revenue and less than 3% of beds.

States make up 23% of GEO’s revenue with Arizona and Florida the biggest contributors at 4.4% of revenue and 3.5% revenue in 2022, respectively. International is about 8% of GEO’s revenue, with Australia accounting for 7% by itself. Local U.S. facilities are about 4% of revenue.

{kind=link}

Risk and Opportunities

Illegal immigration and the laws and enforcement surrounding this hot-button issue are a big driver for GEO, with ICE representing nearly 45% of its revenue in 2022. Thus, the end of Title 42 regulations could be a big boost to the company.

Title 42 itself is actually a health law that can be used to prohibit a person from entering the country when there is the danger of spreading a communicable disease into the U.S. The Trump Administration used the law during Covid to immediately be able to send back immigrants trying to cross the border without detention, processing, or being able to seek asylum. The rule has led to ICE detainee populations being well below historical levels.

CFO David Garfinkle, of rival CoreCivic (CXW), summed up the opportunity for private prisons on its Q3 call , saying:

“Whenever Title 42 is terminated, such action may result in an increase in the number of undocumented people permitted to enter the United States claiming asylum and could result in an increase in the number of people apprehended and detained by ICE. With the press occupancy levels, we are in a position to significantly grow earnings whenever the impact of Covid-19 restrictions subsides.”

In April 2022, the CDC said it would stop authorizing Title 42 due to Covid, but several states took the matter to the courts, and in December, the Supreme Court ruled that the restrictions should remain in place as legal challenges work their way through the courts. The Biden Administration said it was ready for the policy to end , but in January the administration actually expanded the program to include immigrants from Cuba and Nicaragua.

At this point, it’s still unknown if and when Title 42 will end. If it does and it leads to more ICE detainees, it would be a huge boost to GEO. Given that the Covid pandemic has ended by government standards, it seems difficult that the Title 42 border controls would be allowed to remain in place for too much longer. That said, when dealing with the government and political risk, it's often best to throw logical assumptions out the window.

Other Covid-era policies have also negatively impacted GEO’s reentry business, as the pandemic led government agencies to consider alternatives, including home confinement, furloughs, and day reporting programs. Reentry occupancy, as a result, has also been way below historical levels. The company does have some day programs that have done well, but it would benefit more with its reentry centers if things return to pre-Covid levels.

The company has also seen ISAP participants decline at the start of this year due to what the company described as “changes in immigration policies and budgetary pressures.” The program peaked at over 300,000 participants in 2022, but is down to 290,000.

Also on the political front, one of President Biden’s first moves was an executive order banning new federal private prison contracts . Thus far, private prison operators such as GEO have been able to avoid the impact of this in two ways. One way is to turn the facilities into immigration detention centers, as the executive order did not apply to ICE facilities. The other is that states and local governments have taken federal funds to manage prisons and then just turned around and given them to private prison operators.

At the end of 2022, GEO had 47 contracts up for renewal before the end of 2023 representing 29% of its revenue. While some contracts have been renewed, that’s a lot of contract risk for this year, especially given Biden's executive order. It also has 11 facility management contracts up for re-bid, representing 6% of its revenue. The company has already said two U.S. Marshal facility contracts would be renewed - and U.S. Marshal Services would fall under that contract ban - and that no U.S. Marshal contracts are up for renewal in 2024.

Outside of politics, GEO does have a fair amount of variable-interest debt that will cause its interest expenses to rise. Its leverage is also fairly high at 3.7x given some of the uncertainties it faces.

Valuation

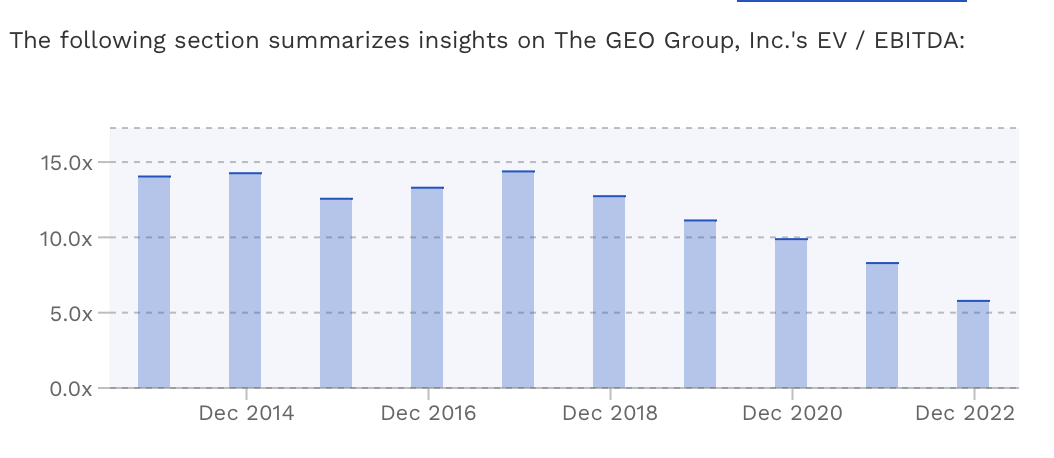

GEO trades at a 5.6x EV/EBITDA multiple based on the 2023 EBITDA consensus of $531.5 million. Based off of the 2024 EBITDA consensus of $555.2 million, it trades at around 5.4x.

It trades at 8.5x forward EPS, with analysts projecting 2023 EPS of 99 cents.

It’s projected to grow revenue 3.5% in 2023, slightly accelerating to 3.7% growth in 2024.

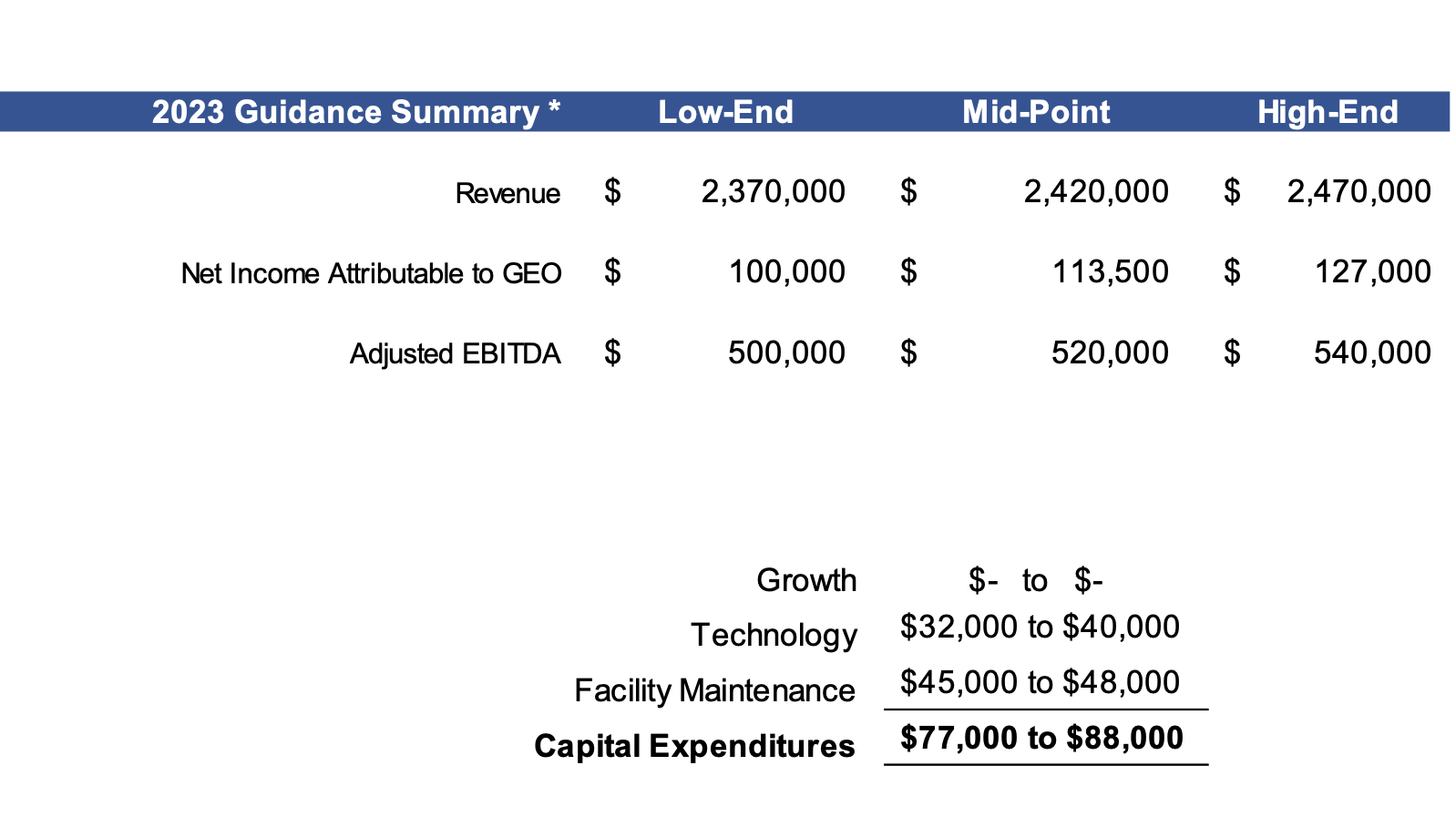

For its part, GEO forecast 2023 revenue of between $2.37-$2.47 billion. It guided for 2023 EBITDA of between $500-$540 million.

{kind=link}

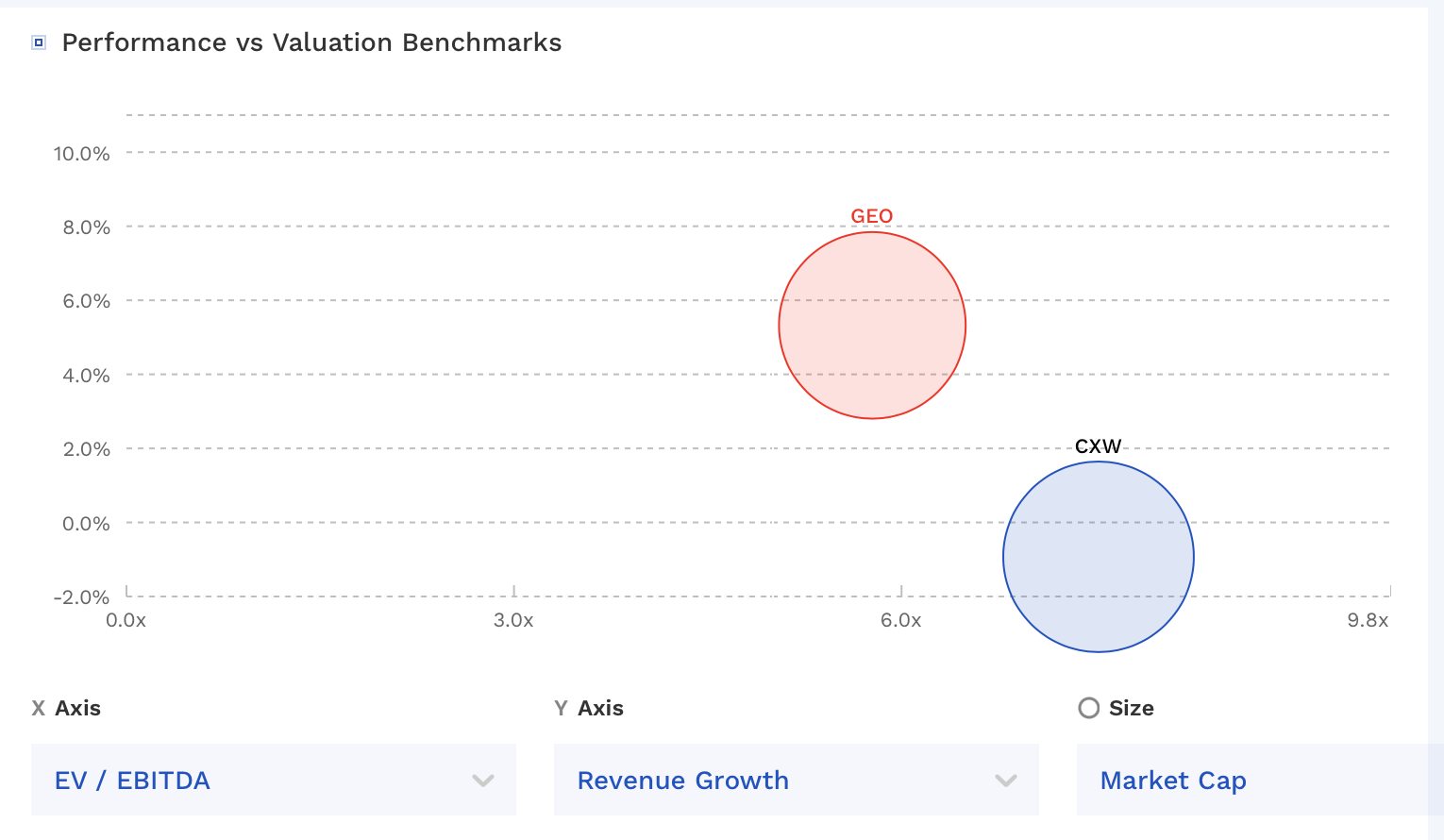

The stock trades at a discount to its competitor CXW. Both companies are in the same industry facing the same trends, although GEO is actually growing a little faster and they have similar leverage. CXW has less BOP and U.S. Marshal exposure and has been buying back shares, which is likely the reason for the discount.

{kind=link}

Conclusion

GEO carries an interesting combination of opportunities and risks, and most of it is political in nature. Despite what would appear to be headwinds in its business, the company has grown its EBITDA nicely the last three years (from $385 million to $516 million). At the same time, it has a pretty nice opportunity in front of it if Title 42 border restrictions are lifted.

If the Title 42 border restrictions are lifted, the stock could have upside to over $20, which is an under 8x multiple based on 2024 EBITDA. The stock has traded between a 10-15x multiple in the past.

{kind=link}

For further details see:

The GEO Group: The Stock Looks Cheap With Title 42 Upside Optionality