MLI - The Gorman-Rupp Company: Shares Need To Fall Further To Justify Action

Summary

- Shares of The Gorman-Rupp Company have taken a beating in recent months, with downside coming in greater than what the market experienced.

- This is peculiar when you look at the relatively strong fundamental performance generated by management's actions and by strong demand.

- Even so, shares are pricey compared to similar firms, and they likely need to fall a bit further to be worth serious consideration.

Although many investors love to talk about their exciting investments, some of the more interesting opportunities are actually the boring companies. And what could get more boring than a business dedicated to the production and sale of pumps and pump systems? These are products that are used in water, wastewater, construction, dewatering, industrial, petroleum, agriculture, fire protection, and other miscellaneous areas and activities. The company in question is The Gorman-Rupp Company ( GRC ). In recent years, the financial trajectory of the company has been rather volatile. But the most recent data provided by management is more promising. On an absolute basis, shares of the company do look quite attractive at this time. But it's also true that, relative to similar firms, GRC stock is a bit on the pricey side. Given this relative valuation and the historical volatility of the business, I do still think that shares make a better ‘hold’ candidate than a ‘buy’ candidate. But they are getting closer to an upgrade based on my assessment.

A victim of downward pressure

A little over a year ago, in the middle of January of 2022, I wrote an article discussing the investment worthiness of Gorman-Rupp. In that article, I described the company's business model and talked about its mixed financial results over the prior few years. All things considered, I felt as though the company, given its past performance, looked to be more or less fairly valued. As a result, I assigned it a ‘hold’ rating to reflect my view that shares should generate upside or downside that would be more or less in line with what the broader market would experience. Unfortunately, that call has not played out exactly as I thought it would. While the S&P 500 is down 11.7% since the publication of that article, shares of Gorman-Rupp have seen downside of 31.1%.

{kind=link}

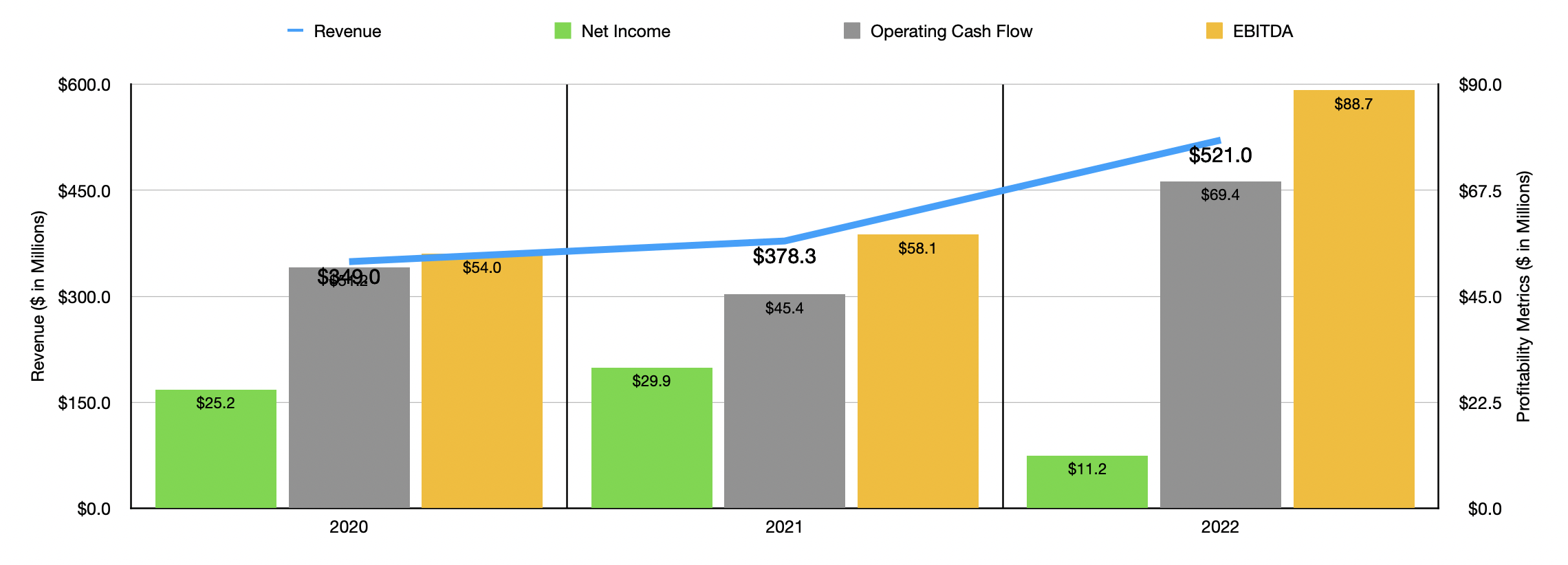

What's really interesting about this return disparity to me is that there doesn't seem to be much of a fundamental justification for the push lower. Consider, for instance, how the company performed during 2021. Sales of $378.3 million beat out the $349 million reported one year earlier. Net income inched up from $25.2 million to $29.9 million. It is true that operating cash flow fell year over year, dropping from $51.2 million to $45.4 million. But on the other hand, EBITDA rose from roughly $54 million to $58.1 million.

Given this mixed performance, particularly when it comes to operating cash flow, I guess I could imagine a scenario where the market might push the stock lower. But when you look at data for the 2022 fiscal year, you end up with a different impression. Sales for that year came in strong at $521 million. That's 37.7% higher than in the 2021 fiscal year. To be fully transparent, it's important to note that the lion’s share of this sales increase came from the company's acquisition of Fill-Rite in May Of 2022. For those who don't know, Fill-Rite is a producer of pumps and meters that the company paid $525 million for. But after adjusting for $80 million in tax benefits, the net price paid by the company was $445 million. Even if we exclude the aforementioned acquisition, sales for the company would have risen by 14.6% year over year. With the exception of the agricultural and petroleum markets, the company experienced robust sales growth across the board. On top of this, the company ended the year with backlog of $267.4 million. That's up significantly compared to the $186 million reported for the end of the 2021 fiscal year. Interestingly, the aforementioned acquisition added only $13 million to this backlog figure. So the rest of the increase was due to high demand for the firm's offerings.

On the bottom line, the picture was slightly more complicated. Net income did manage to fall year over year, plunging from $29.9 million to only $11.2 million. But the other profitability metrics were positive. The one that management has reported so far is EBITDA. That came in during 2022 at $88.7 million. By comparison, in 2021, the metric was $58.1 million. Operating cash flow has not yet been reported. While the company has announced data covering all of 2022, they have not yet filed their annual report or supplementary financials that reveal operating cash flow. If we assume that it increased at the same rate that EBITDA did, then a reading of $69.4 million, up from the $45.4 million reported one year earlier, would not be unrealistic. For the purpose of the rest of this article, any reference to operating cash flow in any way, shape, or form, assumes that this estimate is what the company ultimately generated last year. The actual picture could change to some degree once their annual report is made public.

{kind=link}

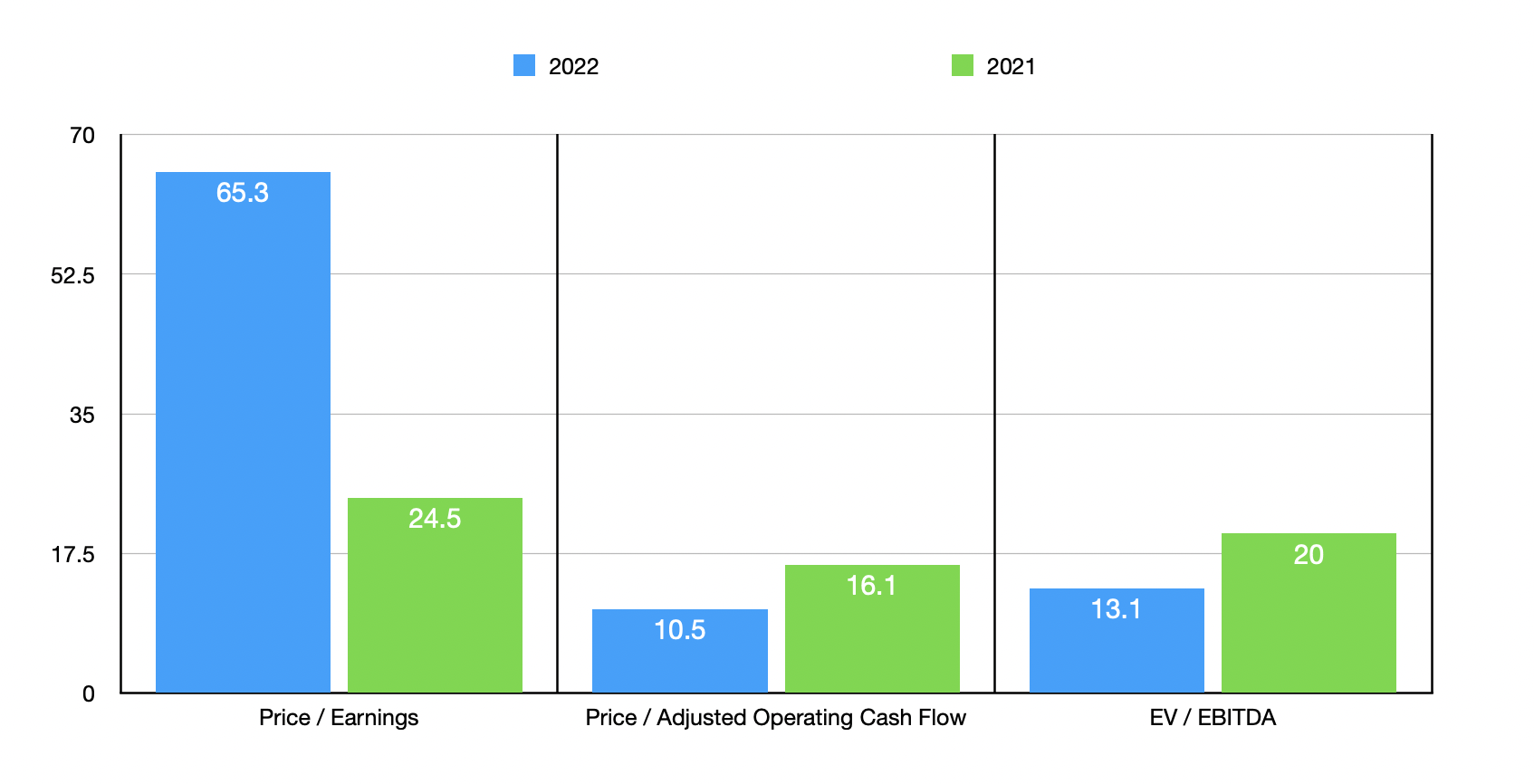

If we take these reported numbers, as well as the aforementioned estimate for operating cash flow, we can easily value the company. Using the price-to-earnings approach, the company does look rather lofty with a multiple of 65.3. That's almost triple the 24.5 reading that we would get using data from its 2021 fiscal year. On a price to adjusted operating cash flow basis, shares to the business or trading at a multiple of 10.5. This is down considerably from the 16.1 reading that we would get using data from 2021. Meanwhile, the EV to EBITDA multiple for the firm was 13.1. That compares nicely to the 20 reading that we get using data from the year prior. As I do with most other companies that I analyze, I decided to compare Gorman-Rupp to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 5.7 to a high of 20.5. In this case, only one of the five firms was cheaper than our target. But this is the only way in which shares of the business look cheap. Using the price-to-earnings approach, the range for the five firms was between 6.2 and 36. In this case, our prospect was the most expensive of the group. When it comes to the EV to EBITDA approach, the range was from 3.8 to 22. Four of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Gorman-Rupp Company |

| 65.3 |

| 10.5 |

| 13.1 |

| Mueller Industries ( MLI ) |

| 6.2 |

| 5.7 |

| 3.8 |

| Parker-Hannifin ( PH ) |

| 36.0 |

| 18.1 |

| 22.0 |

| Crane Holdings Co ( CR ) |

| 16.6 |

| 15.0 |

| 9.9 |

| EnPro Industries ( NPO ) |

| 13.3 |

| 14.4 |

| 8.5 |

| Standex International ( SXI ) |

| 20.2 |

| 20.5 |

| 11.8 |

Takeaway

Thanks to the acquisition of Fill-Rite, combined with strong organic growth, Gorman-Rupp is definitely looking better than it had in the past. Shares are looking cheaper from a cash flow perspective, though they are pricey relative to similar firms. In truth, I am getting closer to upgrading the company based on these improvements and the likelihood, thanks to backlog, that robust results will continue moving forward. But until I see more evidence that the firm's days of volatility are behind it and until the stock falls perhaps a bit more, I believe that a ‘hold’ rating is still appropriate.

For further details see:

The Gorman-Rupp Company: Shares Need To Fall Further To Justify Action