OXY - The Growth Bug Bites Occidental Petroleum

2024-01-16 04:53:40 ET

Summary

- Occidental Petroleum has announced its second large acquisition in recent years, despite previous statements that they were unlikely to make further acquisitions.

- Shareholders have yet to see the benefits of the last acquisition in the form of a higher share price and raised dividends.

- The success of these acquisitions may be necessary for Occidental to return to former stock price levels in a "lower for longer" environment.

- CrownRock shows far superior free cash flow to just about any public company I follow whether adjusting production and cash flow or just comparing.

- The dividend will increase in conjunction with the acquisition. Free cash flow per share will also benefit.

The last article about Occidental Petroleum ( OXY ) mentioned that management stated they were unlikely to make an acquisition. But the "ink did not dry" on that one before the CrownRock acquisition was announced. This is the second large acquisition that was announced in the last few years. Shareholders have yet to see the benefits of the last acquisition in the form of a higher share price and higher dividends (compared to what existed before the Anadarko acquisition). The major question: will long-term shareholders see those proposed benefits or has stock has now become a trading opportunity only?

Some of us remember the Occidental stock price before the pandemic and before the Anadarko acquisition. I personally remember seeing one broker report after another stating some great future stock prices for Occidental as it was before the acquisition binge. Acquisitions are supposed to improve upon that outlook. But Occidental stock has yet to get back to those "older prices". This appears to be due to a combination of an industrywide price-earnings ratio collapse that has yet to reverse during this recovery, and lower oil and gas prices that have yet to get back to pre-pandemic levels. Oil and gas prices are definitely comfortable for the industry. But they are really nothing close to the levels of 2014 and before.

It is therefore possible that these acquisitions are needed for the company to return to former stock price levels (while maintaining its competitive position in the industry) in a "lower for longer" environment. I regularly report how production costs keep declining. This not only adds more Tier one acreage but also points towards higher future production levels. Occidental management discussed in the latest conference call (referenced in the opening paragraph) how accomplished the company has been in adding Tier 1 acreage in the past. That has been repeated throughout the industry. But that kind of success likely points towards lower commodity prices in the future.

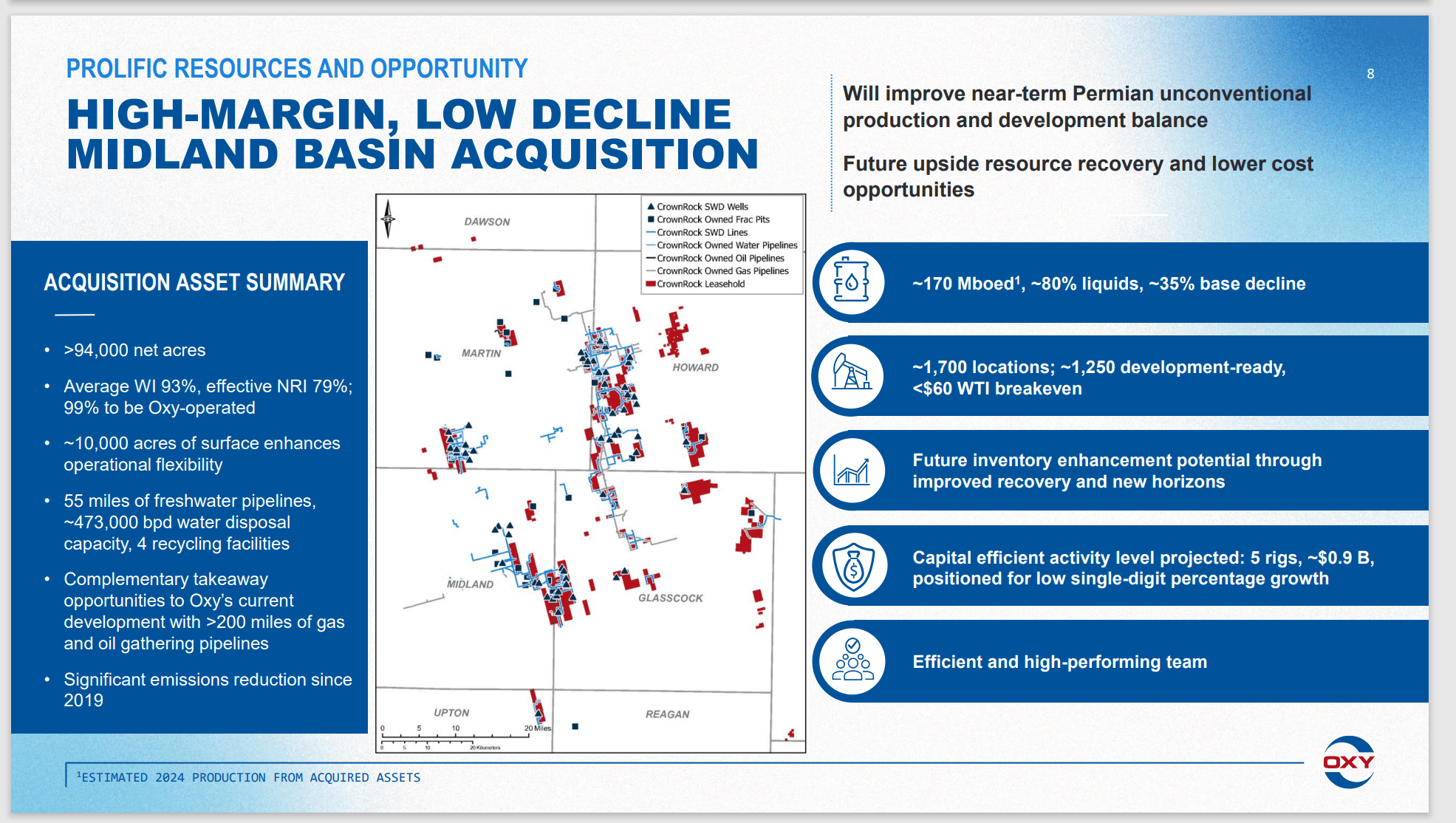

CrownRock Acquisition Proposal

Management disclosed the following terms and conditions:

Occidental Petroleum Summary Of CrownRock Acquisition (Occidental Petroleum Corporate Presentation Third Quarter 2023)

{kind=link}

Management expects $1 billion in free cash flow subject to commodity price expectations. However, this company generally does not hedge. To survive with that strategy, the company needs very low production costs (which it appears to have). Even then, something like fiscal year 2020 where the oil price went negative will strain a company like this if it lasts.

For comparison purposes to roughly check on management's statements, Baytex Energy ( BTE ), which I follow regularly, does not show anything close to that $1 billion of free cash flow using similar assumptions. Vital Energy ( VTLE ) is another company where you can adjust the production levels and free cash flow to get roughly the production listed here of 170,000 BOED and still not show that kind of free cash flow.

That makes this acreage premium acreage with the results management stated. Oftentimes management knows some things to improve and technology keeps advancing. So, there is an excellent chance of even more free cash flow at various pricing assumptions in the future. In fact, if technology continues to advance, then management can grow profitability over time. Management stated in the conference call they have been adding to Tier 1 acreage. Therefore, this deal will improve over time.

Next is the statement about lower capital costs. But that is very much implied by that very high free cash flow figure. It gets backed up by managements like Diamondback Energy ( FANG ) management stating this acreage has slowed or even stopped at times production cost increases reported by the company. Vital Energy management notes that Howard County (for example) has some of the best cash flows and free cash flows in the company portfolio.

I have long noted that the Midland Basin often produces profitability similar to the Delaware Basin without the cost (at least until this transaction). Management would not be making this transaction using due diligence if they did not see a benefit.

The whole thing comes down to if shareholders will see the advantages in the stock price. If this acreage delivers benefits fast enough and material enough for investors to see that on quarterly reports, then there is that possibility. On the other hand, if the acquisition delivers benefits over time, the slowing of cost increases and smaller profitability increases to the corporate average may not be as apparent to the individual investor because it would have to be compared to the company before the acquisition was made. Fluctuating commodity prices can make such a comparison difficult or even impossible.

A smaller company like Diamondback Energy did show some corporate and operating cost declines from acquisitions in the Midland Basin. But that was because the company was small enough that the acquisitions were material enough to have an effect on the quarterly reports from time to time. Here, that may not be the case.

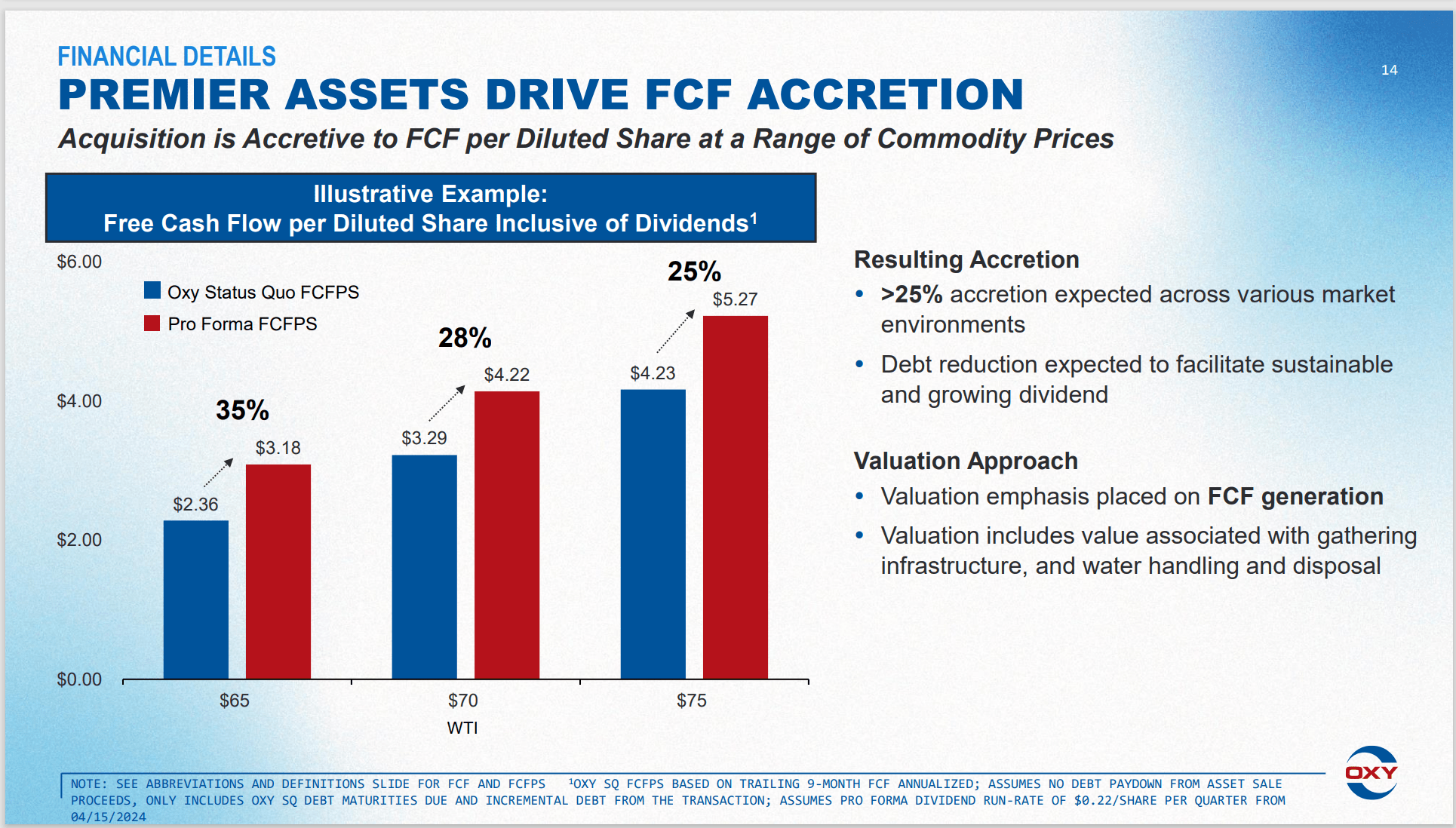

Management Free Cash Flow Selling Point

Management is telling shareholders that the following will happen as a result of the acquisition. This helps. But investors also have to trust management about the statements made.

Occidental Petroleum Free Cash Flow Accretion From CrownRock Acquisition (Occidental Petroleum Corporate Presentation Third Quarter 2023)

{kind=link}

Management stated that even given the relatively high valuation of the purchase price, it would benefit free cash flow immediately per share. Left out of the discussion is the risk of higher debt which management agrees to pay down fast.

In a "status quo" situation, this would definitely benefit the stock price and the dividend eventually. The question remains: if the whole industry duplicates this achievement one way or another, would this end up being a maintenance exercise due to "lower for longer" commodity prices?

This is where potential upside opportunities become important because then it is possible to change the company production mix with lower cost opportunities if they are significant to the company. Management mentioned the Barnett formation as an upside for this acreage. But there is no guarantee that the formation or any other ideas would be material for Occidental even if they prove to make the purchase a good one.

Management also mentioned that the unconventional business is largely in the Delaware while the EOR business is largely in the Midland basin. The size of the Midland unconventional business would become more optimal with the acquisition to also add value to the purchase. That of course implies lower costs for the Midland operation. Whether this benefit actually becomes obvious to shareholders is another matter.

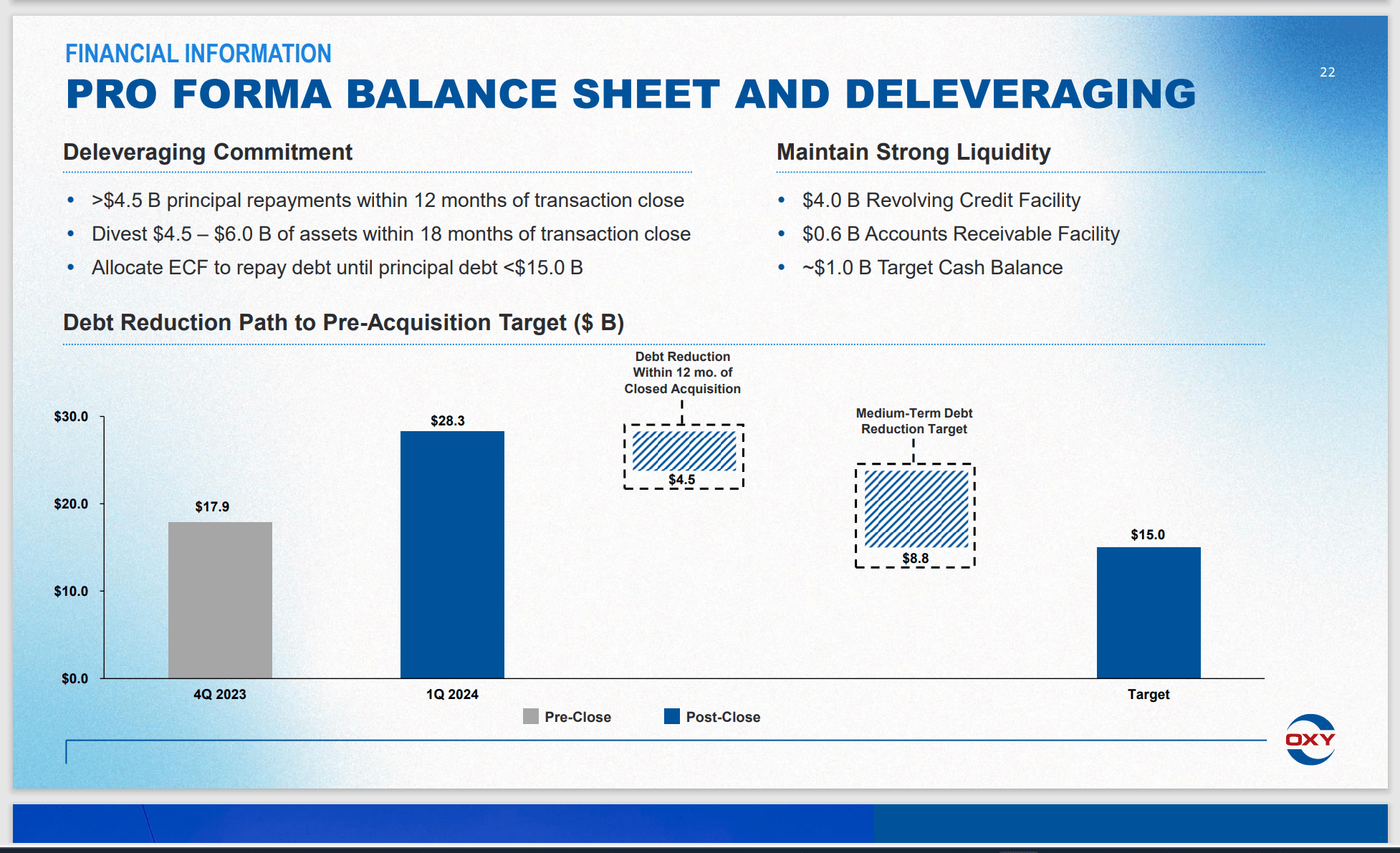

The Debt Plan

Management plans to magnify the effect of the acquisition by disposing of noncore assets that are higher cost to the company while repaying debt at an accelerated rate.

Occidental Petroleum ProForma Debt Structure And Future Debt Strategy (Occidental Petroleum Corporate Presentation Third Quarter 2023)

{kind=link}

Management has overlapping goals in the asset sales and debt repayments. That could well mean that management wants to repay this debt faster than the guidance given above. But the timing of asset sales can be variable enough that management gave a conservative guideline "just in case".

The experience with the Anadarko acquisition probably demonstrated to both management and to investors just how conservative the plans had to be because that acquisition occurred just before the pandemic challenges. Management was able to meet the divestiture goals in terms of dollars even if more properties had to be sold than anticipated.

Of course, the commodity price rises of fiscal year 2022 helped the debt repayment process tremendously. There is always a risk of a fiscal year 2020 which was loaded with challenges without the benefits of a fiscal year 2022 that was pretty much at the opposite end to put the company back on track.

What This All Means

Management is trying to get across the benefits to investors with a chart showing the accretive nature per share of free cash flow and by increasing the dividend after the acquisition (or with the acquisition announcement).

This is kind of important because costs are decreasing throughout the industry on a regular basis. While such cost improvements could "stop tomorrow" that does not appear to be likely. It is far more likely that costs improve at a pace where the Tier 1 acreage definition gradually changes through lower costs over time to the point where commodity prices are "lower for longer". Tier 1 acreage when I grew up was a vertical well of (for example) 3,000 feet that flowed at least 200 BOD without suddenly drying up. It is therefore very clear that Tier 1 acreage has changed the definition to evolve with the industry over time.

This risk of industrywide cost improvement could keep shareholders from seeing the benefits of the acquisition. It may also keep the stock price from reaching previous levels while slowing the rate of dividend increases. Occidental is an upstream operator and therefore is best analyzed by investors as a variable distribution entity rather than one that can consistently raise the dividend like a dividend king or "SWAN".

Nonetheless, management presents a compelling case for making the acquisition. The company future appears to be better regardless of the future of commodity price projections. That is probably the key for any commodity industry.

The company therefore remains a strong buy as the acquisition reinforces (or even increases) the company profitability at various pricing levels. The industry itself is still buying in what is essentially a buyers' market (even though prices are increasing). As long as insiders are buying, then it is very likely that a purchase like this one signal better times ahead. We still appear to be at the beginning of the cyclical recovery cycle where purchases overall are cheap (even with this one in the equation because some may not consider this one cheap).

A lot can happen in the future. Insiders can certainly be wrong. However, insiders often have a much more knowledgeable view of the industry than many investors. All of this purchasing of production rather than growing production is something seen early in the business cycle.

What will happen at a market top is a lot of companies going public as we saw in the auto industry not too long ago. Speculative money generally pours in to make some fantastic acquisitions at sky high prices while also lending for projects with less-than-ideal returns. This money generally loses big time when years like 2015 and again in 2020 saw a lot of bankruptcies. But that money is nowhere in sight. Therefore, the current recovery still has a runway.

For further details see:

The Growth Bug Bites Occidental Petroleum