THG - The Hanover Insurance: 3% Dividend Yield And Modest Buy Rating

2023-09-11 23:28:04 ET

Summary

- The Hanover Insurance Group gets modest Buy Rating today, agreeing with Wall Street consensus.

- Positives: revenue YoY growth, share price 16% below 200-day SMA, 3% dividend yield, company financial health.

- Headwinds: overvaluation vs its sector.

- Risk of asset exposure discussed, investment portfolio appears diversified and investment-grade.

- Catastrophe losses in Q2 attributed to unusual storm activity.

Research Summary

Today I'll be rating The Hanover Insurance Group ( THG ) , in the financials sector, insurance subsector.

The firm had its FY2023 Q2 earnings result on Aug. 2nd and I will do a deep dive into some of that data that I think is relevant to readers.

For readers less familiar with this company, here are a few relevant points from their website : roots go back to 1852, diversified insurance segments across personal / commercial / specialty lines. Trades on the NYSE. Headquartered in Massachusetts US. Its financial services / investment advisory is through its Opus Investment Management division.

Two key peers of this company, according to Seeking Alpha, are Selective Insurance ( SIGI ), and Kemper Corp ( KMPR ).

Rating Methodology

Using a process similar to 5 project phases in project management, I break down my overall holistic rating of this stock into 5 categories I rank individually and of equal weight: dividends, valuation, share price, earnings growth, financial health.

If I recommend this stock on at least 3 of 5 categories, it gets a hold rating. 4 of 5 gets a buy, and less than 3 gets a sell rating. Then I compare my rating to the consensus from analysts, Wall Street, and the quant system.

Dividends

In this category, I will analyze the dividends of this stock and whether I think they present an opportunity for dividend-income investors. The data comes from official dividend info from Seeking Alpha.

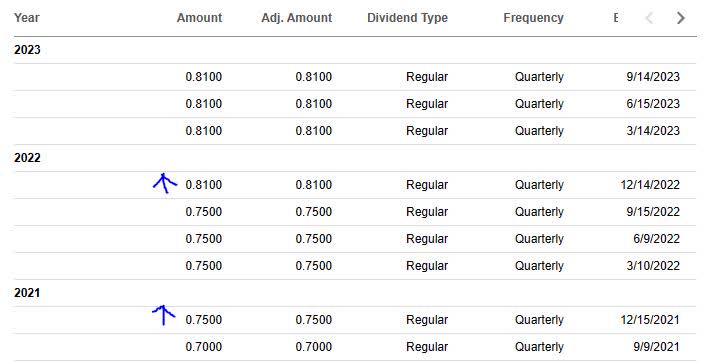

As of the writing of this analysis, the forward dividend yield is 3.10% , with a payout of $0.81 per share on a quarterly basis, with another ex-date coming up very soon on Sept. 14th.

Although I consider this a relatively attractive yield, it will require comparison to its overall sector.

Hanover - div yield (Seeking Alpha)

{kind=link}

When comparing to its sector average, this dividend yield is nearly 20% below its sector average. I believe this is a only a moderately negative point to consider for dividend investors who are comparing multiple stocks in which to invest, as I think that a yield within 1% of the average is reasonable, which would put my target at 3% - 5% dividend yield. In this case, Hanover's yield falls within that range.

Keep in mind that, in my opinion, a yield much higher than average may at first glance look attractive but it may indicate some other reason driving a share price drop recently.

Hanover - div yield vs sector (Seeking Alpha)

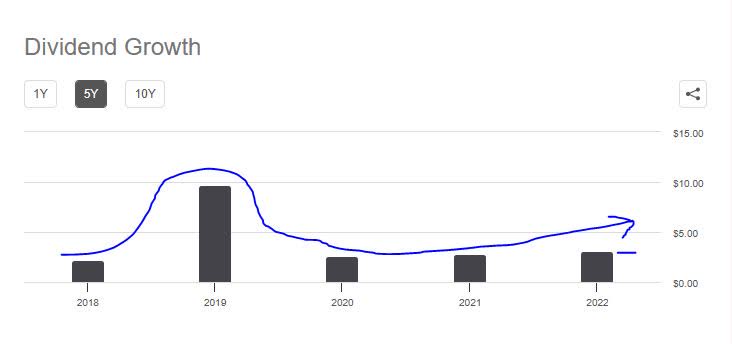

In looking at the 5-year dividend growth for this stock, it has shown a lopsided growth trend with more recent improvement and growth since 2020. This is, in my opinion, a moderately positive point for dividend investors and a sign of this firm's capacity to return capital back to shareholders, which I think is a sign of capital strength.

Hanover - div 5 yr growth (Seeking Alpha)

{kind=link}

Additionally, I am looking for stability with dividend payouts, and this stock has shown regular dividend payment history lately, which is a positive point to think about. However, since 2019 it has not paid a "special/other" dividend in addition to its regular quarterly ones. You can see in the above chart the reflection of this in the 2019 spike vs the other years.

So far I have only seen a handle of firms in this sector that do special dividends, so I try to highlight them out here when possible.

Hanover - div history (Seeking Alpha)

{kind=link}

On the whole, I would recommend this company on the category of dividends. Later in the section on share price, I will show how this dividend income can be used in an investment idea for this stock.

Valuation

In this category, I will analyze the valuation of this stock. The data comes from official valuation info on Seeking Alpha, specifically the forward P/E ratio and forward P/B ratio, the key metrics I look at.

This stock has a forward P/E ratio of 43.36, which is a whopping 341% above its sector average. Attention grabbing, to say the least. I think that a reasonable forward price to earnings for this stock in relation to the average of 9.6x earnings would be between 8x earnings and 11x earnings, to stay within a reasonable 1 to 2 point range of the average. In this case, on this metric the stock appears extremely overvalued vs its overall sector.

In fact, Seeking Alpha gave it an "F" grade so that is worth calling out too.

Hanover - PE ratio (Seeking Alpha)

This stock has a forward P/B ratio of 1.59 , which is 61% above its sector average . I think that a reasonable price-to-book value for this stock would be between 0.5x book value and 1.5x book value, to stay within a 1/2 point range of the average. In this situation, this stock appears modestly overvalued vs its overall sector.

Hanover - PB ratio (Seeking Alpha)

Based on the examples I gave, I would not recommend this stock on the basis of valuation, and would wait on more normalization of those ratios in relation to the sector it is in.

Share Price

In this category, I will use a simple investment idea to determine if the current share price presents a value buying opportunity right now or not, in relation to my goal for return on capital and my tolerance for capital loss, assuming both can occur.

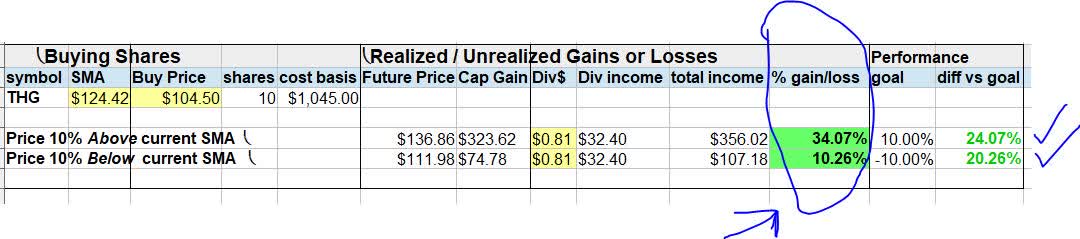

Take a look at the yChart (as of the writing of this article, so the price shown is not real time!) which shows a share price of $104.50, compared to its 200-day simple moving average "SMA" of $124.42 , over the last 1 year period.

I use the 200-day SMA as it is a common long-term trend indicator to track in charts, smoothing out the trend nicely. In the chart, that longer trend appears to have been downward since early this year.

The investing idea I am "simulating" below is to buy 10 shares at the current price, hold 1 year, earn both dividend income and capital gains by selling the shares in Aug. 2024.

The profit goal is to generate a +10% positive return on capital in 1 year, and the maximum loss tolerance is a -10% negative return on capital (unrealized loss) on this investment in 1 year.

After plugging in the current moving average, share price, and dividend per share, as well as assuming the future share price in 1 year will either be +10% above the moving average or -10% below, the following is the result:

Hanover - investing idea (author analysis)

{kind=link}

In the above example, I exceeded my goal for total gains by 24% and also stayed within my loss tolerance since the 2nd scenario shown also generates a positive gain.

With that said, the current share price presents a buy opportunity and in my opinion I would recommend it. Readers should still run their own simulations, however, since everyone does not have the same profit & loss goals or risk tolerance.

In the comments section, I welcome a productive discussion on why you agree or don't agree that this share price presents a great buying opportunity?

Earnings Growth

In this category, I examine the earnings trends comparing the most recent quarterly results to the same quarter a year ago.

I like to say that you are not just buying shares of a 100+ year old insurance firm, you are investing into an existing revenue stream that is already there, not having to do the work of launching a business from scratch!

When it comes to Hanover, I am pleased to say that its top-line revenue saw YoY growth after the Q2 results, and in breaking that down further they saw an impressive yoY growth in its core business of generating insurance premiums from clients but also interest income from their investment portfolio and a decreased loss on selling some of those investments, from the same quarter a year prior.

Hanover - revenue YoY (Seeking Alpha)

{kind=link}

But what about the bottom line?

Unfortunately, I don't have good news there, as the company posted a net loss again in Q2. In fact, more disappointingly I think is 3 straight quarters of net losses.

Hanover - net loss YoY (Seeking Alpha)

{kind=link}

To make sense of these losses, I turned to the company Q2 earnings commentary.

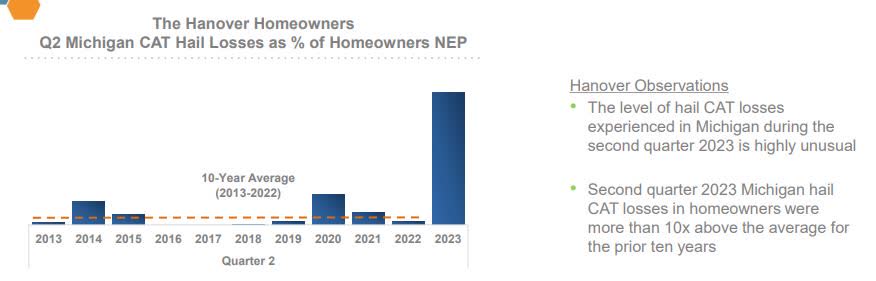

It appears the tailwind came from storm-related catastrophe losses that hit this insurance company hard, specifically the personal lines segment.

According to the earnings release ,

Catastrophe losses in the second quarter of 2023 were $219.2MM, or 38.0 points of the combined ratio, driven primarily by hail damage that significantly impacted the company’s homeowners book of business, particularly in Michigan. This compared to catastrophe losses of $53MM, or 10.2 points of the combined ratio, in the prior-year quarter.

It is important to note that the storms driving insurance policy losses seemed to be unusually above average and not an indicator of any longer-term trend, according to the chart & data below the company provided:

Hanover - hail trends (company q2 presentation)

{kind=link}

Based on this evidence, in my opinion when considering the strong top-line revenue growth and the fact that catastrophe losses tied to storms may not become an all-year event, I would recommend Hanover in the category of earnings growth, despite the 3 quarters of net losses, as looking forward I think it will overcome storm-related headwinds and improve the bottom line for Q3 & Q4.

Financial Health

In this category, I will discuss whether this stock's parent company shows strong financial fundamentals by looking at items like capital & liquidity.

We already mentioned that this firm pays out regular dividends, and when it comes to share repurchases it seems to have put that on hold for the moment, according to Q2 earnings comments.

During the quarter, the company did not repurchase any shares of common stock in the open market. The company has approximately $330MM of remaining capacity under its existing share repurchase program.

On June 30, 2023, operating subsidiary’s statutory capital and surplus was $2.51B, after payment of a $100MM statutory dividend to its parent company.

As I mentioned in some prior articles, the business model of insurance is to "invest" excess cash it gets from premiums into an investment portfolio, with the goal of earning income on those assets.

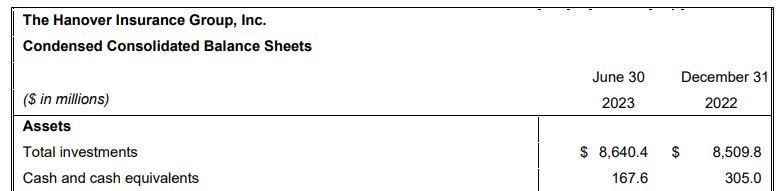

As the table below shows, at the end of Q2 the overall company had $168MM in cash, a good sign I think, and total investments worth $8.6B.

Keep in mind, that is $8.6B not just sitting in a lockbox but is actively earning income for the company, so it is being put to work. A certain percent of those investments also get sold, to generate cash.

Hanover - assets (company Q2 earnings)

{kind=link}

Another point to call out is the positive cashflow which has also improved on a YoY basis, as the table shows. I think free cashflow is an important indicator, and in the case of Hanover it has had a positive free cashflow per share for several quarters, in addition to positive levered & unlevered free cash flow.

Hanover - cashflow (Seeking Alpha)

{kind=link}

Based on the whole picture, I would recommend Hanover in this category, and I expect similar or better results for Q3.

Rating Score

Today, this stock was recommended in 4 of my 5 rating categories, earning a modest buy rating from me today. Although I am disagreeing with the consensus from SA analysts and the quant system, my rating is in line with the Wall Street consensus.

Hanover - rating consensus (Seeking Alpha)

My Rating vs Downside Risk

My bullish rating can face a downside risk as follows:

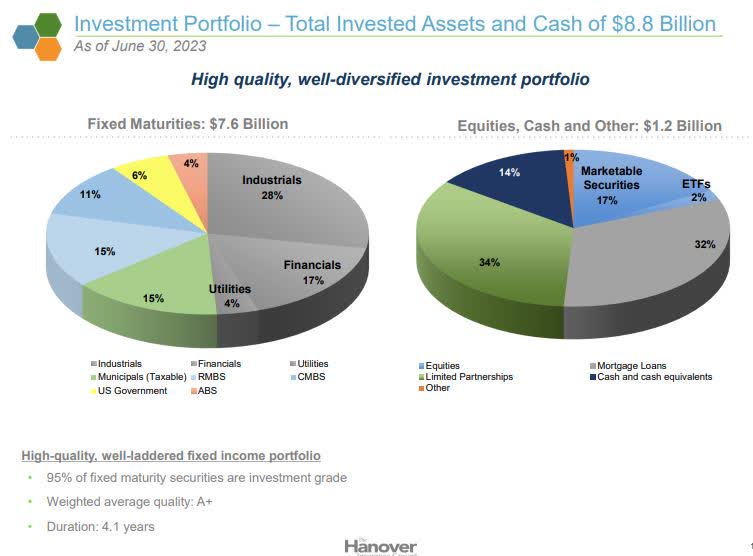

Analysts and investors concerned about asset risk exposure may be bearish on insurance-sector stocks as well as some banks, pushing this share price even further down.

However, this is why I think my buy rating should stand: This company does not mention exposure to assets like commercial real estate /office property, and its $7.6B of fixed-income assets (likely bonds, etc.) are diversified across a plethora of sectors, most of which being investment-grade.

Hanover - investment portfolio (company q2 presentation)

{kind=link}

Further, net investment income on their asset portfolio has only been growing, as the chart below shows, which in my opinion is a positive sign to consider.

Hanover - net investment income (company Q2 presentation)

...

Analysis Wrapup

To wrap up today's discussion, here are the key points we went over:

This stock got a buy rating today.

Its positive points are: dividends, share price, financial health of company, earnings growth.

The headwinds it faces are: valuation.

Downside risks to my rating have been addressed.

In closing, I recommend adding this stock to a watchlist of financial sector, insurance subsector stocks.

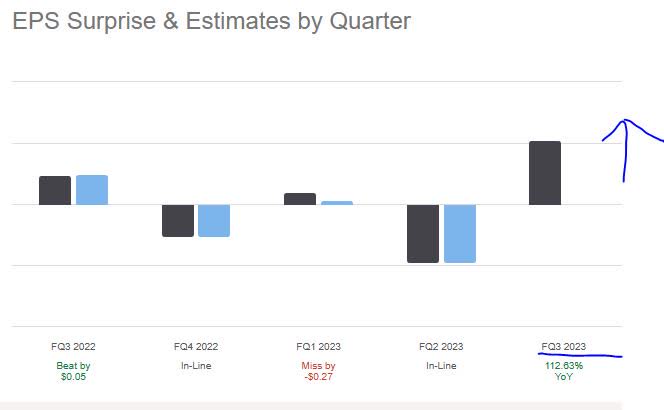

Though sometimes I agree with the rating consensus, this time I am going against the grain, despite the overinflated valuation, and on the whole seeing a moderately decent buy opportunity with this stock right now, for someone looking to pick up a smaller position as part of an overall financial stocks portfolio that is diversified. In addition, the 3% dividend yield can't hurt, either.

In addition, the consensus is already predicting a turnaround on earnings for Q3, as the chart below shows, so I think the company has strong potential to at least meet that estimate if not slightly beat it.

Hanover - earnings beats (Seeking Alpha)

{kind=link}

For further details see:

The Hanover Insurance: 3% Dividend Yield And Modest Buy Rating