HIG - The Hartford Financial: Strong And Stable Earnings Grower

2024-01-17 12:24:44 ET

Summary

- The Hartford Financial downgraded slightly from Strong Buy last year to Buy. This is in line with today's consensus from SA analysts and Wall Street.

- Growth in dividends, earnings, revenue, and equity, but also bullish share price growth by double-digit percentages vs autumn lows.

- An asset portfolio with diversified exposure, however 30% tied to corporates.

- Q4 results in a few weeks expected to meet or beat estimates, driven by growth in policies (premiums income) and fee-based assets (fee income).

Stock & Industry Snapshot

Today's coverage returns to one of my favorite sectors to cover as both an analyst and investor, and that is insurance .

We'll be revisiting The Hartford Financial Services Group, Inc. ( HIG ) , which I last covered in September, and prior to that in June .

Since my June rating where I called it a strong buy , the share price is up nearly 17%, and since my September rating where I reaffirmed my strong buy it is up now nearly +15%.

The Hartford - price since last rating (Seeking Alpha)

Explaining the insurance business model is straightforward: they bring in a ton of cash from customer policy premiums, manage risk so that a lot more is left than has to be paid out in claims, and after business expenses they invest all the extra cash in an asset portfolio.. to earn even more cash.

And, what's better, this model has worked for over a century.

From this firm's profile on Seeking Alpha, we know some quick facts on this firm are that its roots go back to 1810, its named after its namesake city and headquarters of Hartford, and it covers diversified segments such as commercial lines (workers comp, property, liability), personal lines (auto, home), property and casualty, and group benefits.

As for the overall financials sector, of which insurance is a part of, we know from key market data that although this sector has been flat so far in the new year, it has up almost +20% in 3 years, and nearly up +5% in 1 year. This sector bullishness last month in particular also could have had an effect on this stock's price.

key market data (Seeking Alpha)

Although some of the earnings data we will discuss today came out in late October, our forward-looking sentiment relates to their Q4 results due out in a few weeks on Feb. 1st.

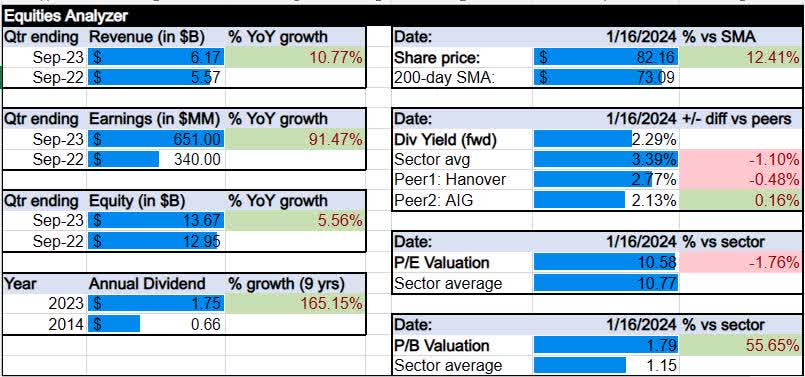

Equities Analyzer

New for 2024, we introduced our Equities Analyzer , which looks at this stock across 8 metrics such as revenue and earnings growth, equity and dividend growth, dividend yield vs peers, and valuations (P/E and P/B ratios).

Here are our results for this stock:

Hartford - equities analyzer (author)

{kind=link}

Revenue Growth

From the income statement as well as the most recent earnings results that came out in late October (the next one expected in a few weeks on Feb. 1st), we can paint a data story about this company's recent growth.

Hartford - rev growth (author)

For instance, top-line revenue grew nearly 11% on a YoY basis.

We can see from the statement that key drivers were growth to nearly $5.3B in their core business of collecting policy premiums, but also they saw growth in interest income on their assets, and a smaller loss on sale of assets than in the year prior.

Two insurance segments that were drivers, according to their press release , were property/casualty and group benefits:

Property & Casualty (P&C) written premiums rose 8% in third quarter 2023 compared with third quarter 2022, driven by both Commercial Lines and Personal Lines. Group Benefits fully insured ongoing premium growth of 8% in third quarter 2023.

In the insurance business, besides earning from steady customers they also track new business coming in as well. In terms of new customer growth, the company mentioned "an increase in homeowners' new business."

Besides insurance, Hartford also has a funds business called Hartford Funds, and it too saw YoY growth in assets under management ((AUM)) which indicates to me that fee-income from managing these assets could also grow in 2024 especially if the AUM growth trend continues:

Hartford Funds - AUM growth (company presentation q3)

From the evidence, my outlook for Q4 results in a few weeks as well as 2024 outlook overall is a positive one on the basis of growth in both insurance policies as well as AUM, and also the added benefit of continuation of the high interest-rate environment driving higher income on fixed-income assets.

Unlike a bank, which has to deal with net interest margins since it pays interest on customer deposits, an insurance company does not have depositors but policyholders.

This category of revenue presents a buy case, in my opinion, supported by the evidence above.

Earnings Growth

From the same income statement and quarterly results, we can see even better figures on the bottom-line, with a +91% YoY growth in net income (earnings):

Hartford - earnings growth (author)

The earnings growth does not appear to be a one-time item, but indicates a longer trend since Sept 2022 of positive earnings growth:

Hartford - earnings growth since sep 2022 (Seeking Alpha)

{kind=link}

In fact, it may be that the market analysts were a bit overly cautious on this sector since it appears Hartford beat earnings estimates in 3 of the last 4 quarters. I expect this trend to continue for Q4.

In this type of business, a significant expense I want to point out would be having to pay out policy benefits, and if a certain quarter was particularly tough in terms of weather or other calamities, it could mean higher payouts.

We can see that benefit payouts only grew +4% on a YoY basis, so nothing too significant.

In this business also, a metric called combined ratio is used to gauge the profitability of the insurance policies, with a good ratio being below 100.

For instance, from their Q3 presentation we see that the commercial lines business saw a much better combined ratio than the personal lines, which were likely were impacted by higher claims paid out on auto losses:

Hartford - commercial lines - combined ratio (company q3 presentation) Hartford - combined ratio personal lines (company q3 presentation)

Looking forward, because we cannot with certainty predict all the different weather events, wildfires, floods and so on that could happen in 2024, it is difficult with certainty to know if a certain quarter will result in higher claims and therefore higher expenses hitting the bottom line.

What we do know is from the past several years is this company continues to show positive net income despite all the various weather events of the last few years, and has shown earnings growth since Sept 2022.

For this reason, along with decent combined ratios in its largest business which is commercial lines insurance, I call it a buy in this category, and I think the firm will meet or exceed earnings estimates for Q4.

Equity Growth

We can get a sense of this company's book value (positive equity) from its balance sheet , as well as equity growth which shows nearly +6% YoY growth.

Hartford - equity growth (author)

One thing that impacts equity is debt, and we know many companies take on corporate debt as does Hartford, but I am looking for trends in whether that debt is growing or coming down. In this case, their long-term debt on a YoY basis is practically flat ($4.36B vs $4.35B).

We also can see that since Sept 2022 equity has grown in 2 of the last 4 quarters since then.

Another item to mention that impacts equity, is the increase in the value of whatever is on the asset side of the equation. We know that bonds go up in value if interest rates go down, and so going forward since there is a high probability of Fed rate cuts this year (according to CME Fedwatch ), it could eventually boost the value of fixed-income securities held by Hartford. Of course, it could also decrease the potential interest-income earned on those assets.

Hartford - growth in securities (Seeking Alpha)

{kind=link}

We can see on a YoY basis, the company's fixed-income (debt securities) book has already increased in value.

Although an increase in equities markets in 2024 could boost their equities book, it is a much smaller part of their asset portfolio than fixed-income, so perhaps will have a smaller impact.

My sentiment for 2024 is a positive one, and in this category I think the evidence points to a buy case. For Q4, I expect continued positive equity growth driven by increasing market values on their asset side (both fixed-income and equity assets).

Dividend Growth

Next, this section is more tuned to dividend-income investors however for all other investors it could paint a picture of financial strength since a company in a better financial position is more likely to grow dividends, I would say.

Hartford - dividend growth (author)

From dividend growth data , we can see that over the last decade this company has growth dividends by +165%.

Additionally, more recently the company's q3 release indicates they "increased the quarterly common dividend per share by 11%, to $0.47, payable Jan. 3, 2024 to shareholders of record at the close of business on Dec. 1, 2023."

So, the prior dividend growth along with recent dividend hikes presents a buy case for me.

Looking out at 2024 I also expect a higher likelihood of more dividend hikes since earnings have grown but also this is a company having positive cash flow as well. For instance, their cash flow statement shows +$1B in both levered and unlevered positive cash flow.

After Q4 when I expect them to meet or exceed earnings estimates, I think it sets the stage for another dividend hike in H1 of 2024, as they try to return some of that profit back to shareholders.

Share Price vs Moving Average

Here, we will consider the most recent share price pulled from yCharts.

The latest as of this article's writing shows a share price of $82.16, which has grown +12% vs its 200-day SMA.

Hartford - share price vs sma (author)

In addition, the chart tell us the price is about $12/share higher now than its autumn low around $70, for a +17% growth since then.

By itself, this chart may scream "sell" at this price, but let's combine it with the earnings, revenue, and equity data.

We know that the share price is 12% above its SMA and 17% above its autumn low, but also that earnings and revenue have both grown by double digits and equity has grown by single digits, while dividends also continue to grow.

That is not a company I would just sell off, even at this price, so I think the price bullishness is justified (not simply because the larger financials sector is also bullish).

It is also not a great "buy" at this price either, because if the larger financials sector takes a hit this year due to let's say media headlines of major office properties defaulting on loans, it could cause an investor to pull back a bit on financials.

I think the case here is for a hold for this stock, with expectations of at least some volatility in financials stocks this year.

Since I expect them to meet or beat Q4 estimates in a few weeks, this could add some more bullishness to the share price, for a short while at least. It will mostly come from experienced investors who are not looking for a hyped-up Silicon Valley startup but a long-established insurance company stock to park their capital at, with an eye towards greater long-term security, despite short term volatility.

With that said, Q4 results whether great or not are still a short-term result and this company to me seems the type of stock I would look at as a longer-term play, looking at its results over many quarters and years.

Dividend Yield vs Peers

Though we already talked about dividend growth, here we want to touch upon the type of yield we are getting from dividends on the capital we invest, and compared to peers, so we can pick the best yield.

Hartford - div yield (author)

Using dividend yield data , we can see that Hartford currently has a forward yield of 2.29%.

We are comparing to the sector and two insurance peers, The Hanover Insurance Group ( THG ) and AIG ( AIG ).

Hartford comes short vs its sector, beats AIG but comes short vs Hanover which has a little better yield.

Though they were not part of this comparison, since they have significate life insurance businesses that Hartford does not have, Prudential Financial ( PRU ) has a much better yield at 4.84% and so does Canada-based Sun Life Financial ( SLF ) at 4.33%.

So, if I was only looking to add any insurance stock to my portfolio to gain exposure to that sector, and wanted the best yield, I would not go with Hartford. Therefore, it gets a sell from me in this category.

Since I expect some more bullishness on the share price after positive Q4 results, it could drive the dividend yield even lower for a while.

Valuation: P/E Ratio

A key valuation metric I look at is the forward price-to-earnings ratio (P/E), which often can be the most cumbersome to get a grip on.

Hartford - P/E ratio (author)

What the data tells us is that Hartford has a forward PE of 10.58, slightly lower than its sector.

Now, it being lower than its sector average does not necessarily mean a great valuation, as we need to place it in the context of share price vs earnings.

From what we already discussed, we know the share price has grown by double digit percentages vs its autumn lows as well as its 200-day average. At the same time, earnings have grown +91% on a YoY basis.

That to me presents a buy case, in my opinion, as the percentage of earnings growth exceeds the percent growth in the share price, so the gap between the two is tight.

Valuation: P/B Ratio

Besides the P/E, I care about the gap between price and book value as well.

Hartford - P/B ratio (author)

From valuation data we also see a forward P/B ratio of 1.79, somewhat higher than its sector average.

Again, in the context of share price growth vs equity growth, we know that share price grew double digit percentages while equity only grew about +6%.

So, equity is growing but not as fast as the share price. This appears to be a hold in my opinion. Had it been a case of double-digit share price growth along with declining equity, I would have called it a sell and overvalued.

Key Risks

Up until now, holistically this stock is pivoting towards the buy range, so let's talk about a key risk to see if that changes things.

Because an insurance company is exposed to the asset risk of whatever is in its asset portfolio, I am looking for asset diversification in Hartford's portfolio.

Here is what it looks like:

Hartford - investment portfolio (company q3 presentation)

{kind=link}

It appears +96% of their portfolio is investment grade. We see about half of their exposure is tied to corporates and securitized products. Although there is no mention of exposure to commercial real estate or office property, only about 11% of the portfolio is made up of mortgage loans.

US Treasuries make up only about 4% of the portfolio.

Although there is diversification, in my opinion (and I welcome readers comments on this topic for sure) I think they are a bit too exposed to corporate bonds and not enough to govt bonds, which are traditionally a safer bet due to being backed by the full faith of the federal government.

I will take a cautious one here and say in terms of risk it appears a hold rather than a buy or sell. On a positive note, in the event there is an uptick in office loan defaults in 2024, some investors in the financials sector may flock away from banks with heavy office exposure and towards insurance companies like this one that do not have that type of risk.

I think this company should make a clear statement on their very low office loan exposure in their Q4 results commentary in a few weeks, as it is certainly a relevant topic.

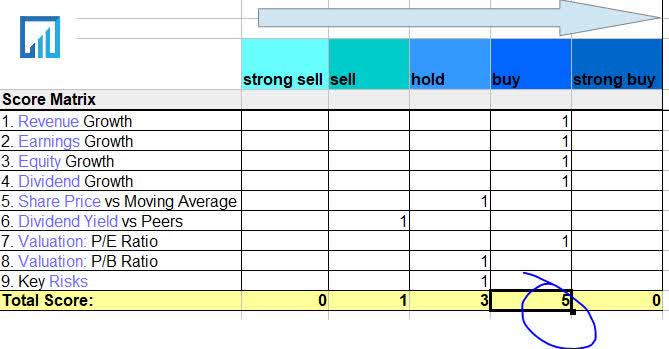

Summary and Rating

Here is a holistic summary using my score matrix:

Hartford - score matrix (author)

{kind=link}

From this score matrix, we see that from a holistic overall standpoint the company gets a buy rating, despite the skyrocketing share price above its average.

This is a slight downgrade from my prior two strong buy ratings last year, which also used a slightly different rating methodology than I use now.

Compared to today's consensus on Seeking Alpha, my rating matches the consensus from analysts and Wall Street who both appear bullish on this stock, as is the quant system, despite the surge in the share price.

To summarize, the company saw positive growth in earnings, dividends, revenue and equity. Its dividend yield is unremarkable vs peers, and its valuation is reasonable. Its asset risk exposure is diversified, but heavily into corporates and not enough into govt bonds/treasuries, although not showing major exposure to office loans.

My portfolio strategy here, if I was buying, would be continue buying up a bit more of this stock, but as a longer-term move (several years) and part of a dividend-income portfolio I am building and not looking to sell off soon to take short term capital gains.

In the short term, after a boost due to Q4 positive results this strategy could see some downside from volatility in financials stocks this year since the overall sector is impacted by Fed decisions on interest rates but also headlines about major office property loan defaults. I think in the long term it presents a strong case to own such a long-established insurance company like this one who has stood the test of time.

Should the company happen to miss Q4 estimates and they come in a little worse than expected, we could see a slight pullback on the share price however in the bigger picture I think the case I presented today supports being long on this one and I expect any price dips will be scooped up by opportune investors who will drive up the price again.

As for the insurance sector overall, those opportune investors like me will continue to see this industry as a necessary component of the economy and a way to transfer risk to a third party, since for many families and companies having to assume the full cost of a catastrophic property loss could be financially debilitating without insurance.

Since there are many insurance company stocks to choose from, this is one of those as they have already proven themselves many times over and the data I showed supports this.

For further details see:

The Hartford Financial: Strong And Stable Earnings Grower