JRE - The Housing Recession Isn't Over Yet

2023-03-08 10:37:00 ET

Summary

- When analysing the business cycle, there are few sectors and areas within the economy of more importance and influence than the housing market.

- Housing is both a cyclical and interest rates sensitive market. Thus, at the heart of the housing market lies mortgage rates.

- House prices are likely going to continue to be pressured, while the lags through to the economic growth cycle are seemingly going to be more impactful from here. The US housing market recession may not yet be over.

When analysing the business cycle, there are few sectors and areas within the economy of more importance and influence than the housing market. With housing contributing to around 15-20% of GDP through housing-related investment and consumption, understanding the outlook for the housing market will provide investors with a significant edge in determining where the business cycle is headed. Understanding the cyclical outlook for the business cycle is key to risk management and asset allocation.

As such, it is time I underwent a check-up of the US housing market and assess the implications for not only house prices themselves, but the implications for the business cycle as well as homebuilding stocks and related equities.

Housing activity continues to trend down

Within my most recent deep-dive into the US housing market , the outlook appeared bleak. So much so I opined it a 'bad time to be a house', though in jest. Unfortunately, little has changed since. Although it is doing so at a slower pace than we have seen over the past six months, housing-related data continues to trend lower.

Housing is both a cyclical and interest rates sensitive market. Thus, at the heart of the housing market lies mortgage rates. While it is likely this move higher in mortgage rates is nearing a peak, much of the damage has yet to be felt. The Fed will get exactly what it wants; the housing market will be the release valve.

When mortgage rates rise, housing affordability falls. Housing affordability is now at its worst point in 40 years. Yikes. (And hey, I live in Melbourne, Australia - one of the most expensive housing markets in the world - so I feel your pain).

National Association of Realtors via Bloomberg When affordability falls, so does sentiment. This is true of both homebuyers and homebuilders. Again, while both look to have put in their lows, they still remain significantly depressed.

Unaffordable housing means a lack of buyers, which in turn means falling home sales.

And as a result, supply for new houses on the market remains well above levels seen at any time since pre-GFC, as we can see below (note, this chart focuses on the supply of new housing, as it is the construction activity associated with building that drives much of the cyclicality of the business cycle, and as such is my focus). New houses simply are not being sold.

More than anyone, first home buyers are taking the brunt of these dynamics as they are being priced out of the market. The rise in borrowing costs is vastly outweighing the fall in house prices, a dynamic with which many existing homeowners are being shielded given the fixed nature of most US mortgages. New home buyers and prospective buyers as a whole are not afforded such luxuries, and as such, mortgage applications to purchase are at decade lows.

With a lack of demand, excess in supply and plummeting house prices, there is simply no appetite to build. Thus, we are seeing building permits collapse. Building permits are one of the best hard data points that provide a good lead on economic activity.

Generally, mortgage applications lead to building permits, which lead construction and thus economic activity. As we shall see in further detail below, the housing market remains a significant drag on the business cycle moving forward.

Taking this all in, we should not be surprised to see house price growth within the US as a whole see its swiftest decline since the GFC.

But, more importantly, what is the outlook for house prices? Let's dig in.

Headwinds remain for house prices

There are a number of factors that go into determining the trajectory of house price growth on a cyclical basis. These include; the cost of housing, supply, demand, liquidity and of course, speculation.

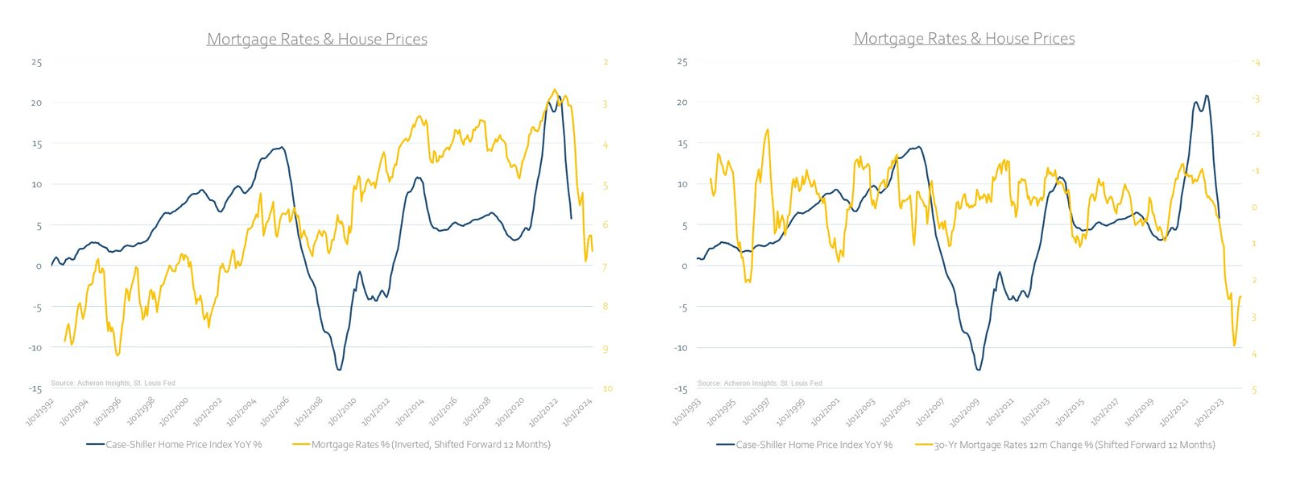

Beginning with mortgage rates, the largest and swiftest rise in mortgage rates in half a century was always going to impact prices. We have seen that play out over the past 12 months, and, unless mortgage rates move lower to a material degree, they are likely to continue to pressure prices lower, at least to some extent.

{kind=link}

This is true of both mortgage rates on an absolute basis and on a rate-of-change basis, as we can see above, but it is also true of the spread between 30-year mortgage rates and the 30-year Treasury yield. The latter also suggests prices may continue to correct still.

In terms of supply, the forecast is much the same. The oversupply in the months' supply of housing remains a material headwind for prices. Again, unless we see supply roll over as swiftly as it has risen over the past couple of years, the supply dynamic continues to suggest lower house price growth ahead.

Perhaps more important than just supply however is the interplay between the demand and supply dynamics within the housing market. Using building permits as a proxy for demand and months' supply of housing for supply, the relative movements between the two tend to provide a solid read on the direction of prices. As we can see, both demand and supply continue to suggest house prices are yet to find a bottom.

Another important determinant is liquidity. If we measure liquidity via the growth of the money supply adjusted for inflation in excess of economic growth, with the idea being the excess money supply will feed through to asset price inflation and speculation, we generally see excess liquidity lead most asset prices by around 12 months. Once again, the outlook for house prices appears unfavourable.

While all of these forward-looking indicators of house price growth suggest further downside ahead, it should be noted it seems likely the bulk of the decline in house prices is behind us. This does not mean prices will not continue to fall further, but the momentum in house price depreciation is likely to continue to improve from here, particularly if we do see mortgage rates find a cyclical top in the coming months. Still, it remains a bad time to be a house.

This does not bode well for economic growth

Unfortunately, until house price growth does manage to find a bottom, we are unlikely to see an uptick in construction activity and thus the cyclical impact from housing will continue to drag growth lower. Monetary policy lags are long and variable, and housing seems the area to which we may ultimately begin to see the economic consequences of the Fed's tightening fully felt in the months and quarters ahead.

Remember, capital investment follows price.

And capital investment leads the business cycle. This is true of residential investment as a percentage of total fixed investment…

As well as housing starts.

Both provide a solid and reliable lead for the direction of the business cycle, highlighting the housing markets importance as a cyclical driver of economic growth.

It is not just through capital investment, construction activity and housing-related consumption that these impacts are felt. It is also true of the wealth effect associated with house prices. Consumption and spending activities are largely derived from changes in net wealth, which itself is largely driven by changes in house prices given one's house is by far the largest asset of most US citizens, which is why changes in net wealth have a material impact on changes in economic growth.

Clearly, the trends in play within the US housing market do not bode well for economic growth in 2023.

What about housing stocks?

It will be of no surprise for me to tell you housing stocks are driven largely by the dynamics within the housing market. Just as mortgage rates lie at the heart of house prices and housing investment, they too are a key determinant of the absolute and relative performance of homebuilder stocks. Mortgage rates continue to suggest underperformance of homebuilder stocks is likely in the coming months.

This relationship can also be seen by assessing moves in Treasury yields themselves. Either way, it seems the recent outperformance of homebuilders relative to the broad stock market was not fundamentally supported or representative of economic reality.

This notion is also being confirmed via the NAHB Index…

And residential investment, both of which also tend to track the relative performance of homebuilder stocks and the broad market and again, are not supportive of the recent relative outperformance of homebuilder stocks.

BCA Research

From a technical perspective, we can see just how well homebuilding stocks have performed since the lows of October last year. Through both a short-squeeze and overly bearish positioned market, the ITB homebuilder ETF is up around 40% during this period. We now appear to be forming somewhat of a bearish flag pattern, suggesting that homebuilder stocks could correct once again should we break this pattern to the downside, as the fundamentals suggest may occur.

However, while fundamental headwinds are present in the sector for sure, we appear to be slowly unlocking some value in homebuilding stocks. The market is (somewhat) forward-looking after all. The ITB ETF is currently trading at a P/E ratio of around 7.4, which is on the cheap side, both on an absolute basis and relative to most other sectors (whilst also being 40% below its median P/E ratio for the past 10 years). Furthermore, short homebuilders has been a pretty consensus trade (which we can infer by the significant level of short interest relative to other major sector ETFs), likely explaining why much of the recent price action can be attributed to a short-squeeze.

However, now is not yet the time to be overweight homebuilder stocks, but to begin scouring the marketplace for attractive business's one may wish to own for the foreseeable future may be a prudent idea, given the increasingly attractive valuations within the sector.

Patience is key here. House prices are likely going to continue to be pressured, while the lags through to the economic growth cycle are seemingly going to be more impactful from here. The US housing market recession may not yet be over.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Housing Recession Isn't Over Yet