CAT - The Hunt For Potential 10x Returns: Will Caterpillar Stock Continue To Climb?

2023-10-03 13:09:36 ET

Summary

- I examine whether Caterpillar has the potential to appreciate ten times over with its current valuation as part of 'The Hunt For Potential 10x Returns' series.

- As previously done, I use a rating system based on factors such as returns on invested capital, insider ownership, share repurchases, gross profit margin, and intangibles to evaluate the company.

- CAT scored 33.67/50 on the 10-bagger scale, supported by its high profitability, stable profit margins, and strong industry potential as a market share leader in a growing market.

- The strong operating performance is built on a strong customer focus as well as attention to new technological capabilities.

Introduction

Caterpillar ( CAT ) stock has experienced a run-up of nearly 14% year-to-date due to really strong top and bottom line growth. In this series, I evaluate whether a company is worth owning for the long term based on the 10-bagger rating list below. Hence, I will be going through the fundamentals of Caterpillar's operations, its future market potential, and whether the company is a buy, sell, or hold at its current valuation.

Check out how Caterpillar fairs against the latest companies that I've run through the 10-bagger rating list:

The 10-Bagger Rating List

Check out the start of this series in " The Hunt For Potential 10x Returns: 2 Software Giants " where I have calculated the required annualized return to gain 10x returns over different time horizons. The power and influence 10x returns can have on your portfolio is immense, and I believe there are certain factors that correlate with this outcome. In short, this is what the series is all about:

In this series, I will be rating one/two companies based on pre-determined criteria which have been found to increase the chance of a stock becoming a 10-bagger. My goal in this series is hence to give investors a quick checklist of 10-bagger factors for a multitude of different companies to compare with over time. Furthermore, I will be cumulatively adding to a scatterplot each company's 10-bagger rating and Seeking Alpha Quant rating which we can track over time.

With inspiration from Christopher Mayer and Peter Lynch, as well as my own experience with investing, I have created the following rating list, which ranges from 1-10, with what I believe are the most important factors that contribute to a potential 10-bagger status.

Rating List

- Profitability ("ROIC"), ("ROE") or ("ROCE").

- Insider Ownership.

- Share Repurchases.

- Gross Profit Margin.

- Intangibles.

Profitability: Ex. Returns on Invested Capital ("ROIC"), Return on Equity ("ROE"), Return on Capital Employed ("ROCE").

| Rating |

| Level |

| 1-2 |

| 0-5% |

| 3-4 |

| 5-10% |

| 5-6 |

| 10-25% |

| 7-8 |

| 25-50% |

| 9-10 |

| 50%+ |

Share Repurchase (yearly % purchase of outstanding shares)

| Rating |

| Level |

| 1-2 |

| Compressing |

| 3-6 |

| Steady |

| 7-10 |

| Expanding |

Intangibles

| Rating |

| Intangible Asset |

| Returns on Invested Capital ("ROIC") |

| 26.46% |

| 10 |

| Insider Ownership |

| 0.15% |

| 1 |

| Share Repurchases |

| 2.21% |

| 7 |

| Gross Profit Margin |

| Slightly Expanding |

| 7 |

| Intangibles |

| Exceptional |

| 8.67 |

Total Points: 33.67/50

Returns on Invested Capital ("ROIC")

Caterpillar, similar to John Deere ( DE ), sells its products under leasing agreements and the company finances its leases with debt. During the most recent quarter, CAT had debt attributable to financing leases amounting to $8.1 billion which is equivalent to 25% of the company's total debt load. The remaining 75% of debt is attributable to the operations of the company.

An interesting dynamic that is now occurring given the higher cost of borrowing is that Caterpillar's financial services arm seems to be facing headwinds. While revenues in this segment grew by 19% "YoY", operating profits only grew by 3% ( Caterpillar Financial, Q2 Report ). The increase in revenues was due to higher leasing rates, while the slow growth in operating profit was attributable to higher general and administrative costs as well as negative foreign currency impacts. However, another contributing factor is the growth in financial expenses. While leasing revenue has grown by 19%, the interest expense on financial products has increased by slightly over 50% "YoY" which is a reflection of the high-interest environment ( Caterpillar Q2 Report ).

Despite the additional costs of borrowing, which can be seen as a headwind to Caterpillar, the company has a solid cash and equity position to weather any storm. On top of that, the company has actually been thriving in an environment with extremely high demand for many of its products (especially in North America).

The Author

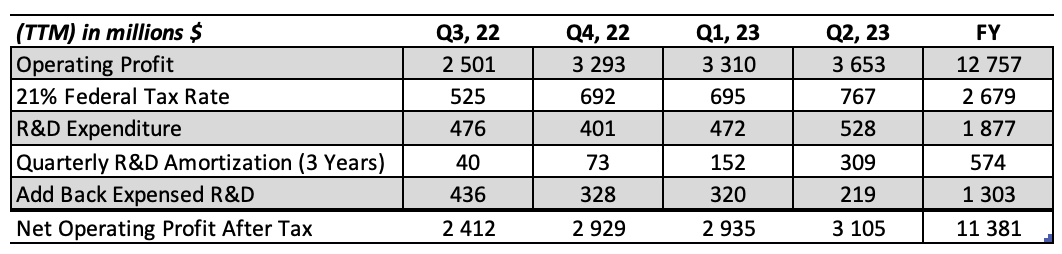

When adjusting "NOPAT" by capitalizing R&D costs for an assumed three years, and subtracting a 21% federal tax rate on profits, I find that CAT achieved $11.381 billion in net operating profit after tax for the "TTM". CAT had an impressive R&D budget of $528 million in the most recent quarter or 3.2% of revenue. This is in line with Deere which spent around 3.3% of revenues on R&D investments during the latest quarter.

{kind=link}

In general, Caterpillar had a strong operating margin and high sales during the "TTM" which attributed to the company earning a 26.46% return on invested capital.

The Author

As you can see in the graph below, Caterpillar's quarterly revenue has been extremely correlated with its operating margin during the past five years. Most likely, this means that CAT can grow its revenues without increasing fixed operating costs as much. This is of course positive during periods of strong growth, however, during periods similar to COVID, operating margins decline just as much as sales. This is likely due to an underutilization of the factories that CAT uses to produce its products. Despite the huge shock that the company experienced in sales volumes during 2020, it still managed to retain a relatively strong margin of 8%.

In all, due to the strong performance of CAT and its ability to mitigate external risks as they did for example during the pandemic, I rate the company with a 10/10 with regard to profitability.

Insider Ownership

Caterpillar is by no means a founder-driven company. During the late 1800's two competitors, Benjamin Holt and C.L Best drew an alliance to found Caterpillar. At the time, the company produced a steam tractor for farmers which was invented by Holt. One unique invention that the company coupled with the steam tractor was replacing the rear wheels of the tractor with a pair of tracks so that farmers could navigate in soft soil. Interestingly, this invention is what gave way to the company's name "Caterpillar":

"In 1904, Benjamin Holt replaced the rear wheels from a Holt steam tractor with a pair of tracks to help Caterpillar farmers deal with soft soil. During a field test in 1905, the company photographer exclaimed that the machine crawled like a big … Caterpillar. "

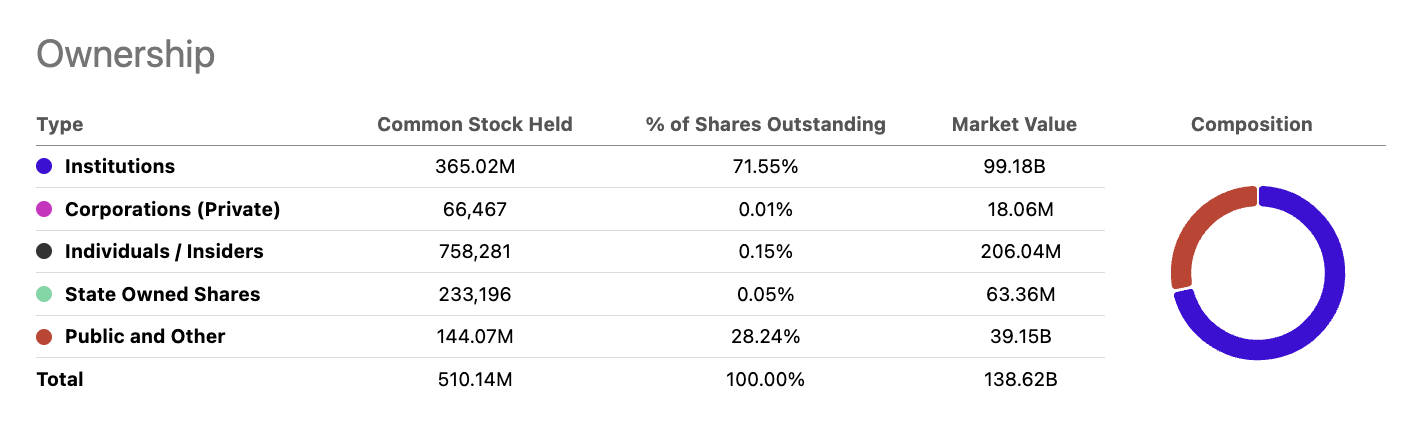

Now Caterpillar is primarily owned by financial institutions. Given the significant appreciation in stock price, CAT has likely become a favorite for several asset managers who are excited about the strong momentum and performance of the stock during the past few years. Currently, the largest owner of the stock is Vanguard Group followed by State Street Corp. and BlackRock. Due to the extremely low insider ownership at Caterpillar, I rate the company a 1/10 with regard to insider ownership.

{kind=link}

Share Repurchases

During the past 10 years, CAT has had a relatively consistent share repurchase program, save during the period 2016-2018. In all, CAT has reduced its shares outstanding by around 21% during the past 10 years. This equates to an average annual share repurchase of 2.1% per annum.

CAT is a shareholder-friendly company that has the goal of returning substantially all free cash flows to shareholders in the form of dividends and share repurchases. During the period 2019-2021, CAT returned $15 billion to shareholders which represents almost 11% of the company's current market cap. While this is a reflection of the company's financial strength and the company actively catering to investors who enjoy secure returns, it also reflects the company's secondhand focus on reinvesting cash into the business. In all, however, based on this rate of share repurchases, I rate the company a 7/10 on the share repurchase scale.

{kind=link}

Gross Profit Margins

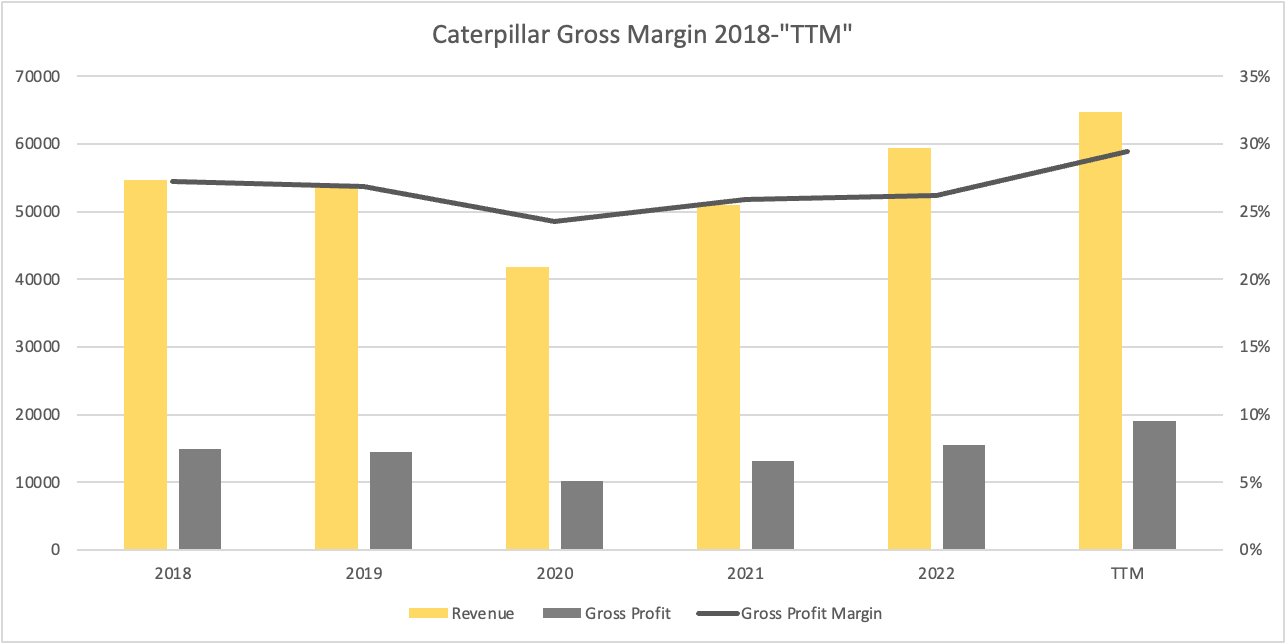

As we can see in the graph below, gross margins have been relatively stable/slightly growing throughout the past five years. In 2018, the company achieved a gross margin of 27.2% which has increased to 29.4% in the TTM. The margins have grown in recent periods as a result of increasing price realization on products sold and lagging cost increases within the business.

{kind=link}

Although gross margins are important, it seems that the company focuses a great deal on adjusted operating margin instead of gross margin. This measure takes into account all overhead and variable costs that are involved in generating revenue. While gross profit margins have only slightly increased over the past five years, the company's operating margins have generally improved and stabilized since a shaky 2014-2017. As of yet, it is unclear whether Caterpillar will be able to continue driving this operating margin. Costs are lagging, as management has mentioned, which means that the cost of labor and inputs will increase over time as prices on the products sold will remain level or slightly increase. In essence, this should decrease gross and operating margins. Despite previous downturns in the company's operating margin, gross margins have remained stable which implies that the company has pricing power. Hence, I rate CAT with a 7/10 for slightly expanding gross margins.

Intangibles

| Intangible Asset |

| Rating |

| Company Culture |

| 9 |

| Industry Potential |

| 10 |

| Operating Leverage |

| 7 |

Average Points: 8.67

1. Company Culture

Caterpillar has a simple goal: Delivering profitable growth . This means that the company is not simply focused on driving revenue growth, it must drive revenue growth that translates to strong bottom-line performance.

CAT is able to deliver this through the values that it strives to put into action and these " Values In Action " are provided on CAT's corporate website:

- Integrity - we believe in the power of honesty.

- Excellence - we set and achieve ambitious goals.

- Teamwork - we help each other succeed.

- Commitment - we embrace our responsibilities.

- Sustainability - we are committed to building a better world.

Furthermore, the company aims to upfill its strategy of driving profitable growth by focusing on four key objectives.

- The first is to provide the best services in the industry. Services comprise everything that CAT does for the customer after the sale of its equipment. Services range "from aftermarket parts to maintenance agreements to financing - with a goal of delivering a superior customer experience." This is one of the company's main initiatives to retain stable revenues throughout volatile demand cycles.

- The second objective is to expand the company's product offering. The company does this by being reactive to what customers need and want. Through tight collaboration with customers, CAT is able to deliver products at a reasonable price that are actually needed. Furthermore, CAT aims to go above and beyond the customer's needs by delivering products with advanced technological capabilities.

- The third objective is operational excellence. Caterpillar is focused on being lean in operations as well as having a competitive and flexible cost structure.

- The final objective is to deliver sustainable products and a sustainable value chain. Caterpillar sees this as a long-term growth opportunity. The company is very focused on refurbishing its existing machines to expand the available life of each machine. Furthermore, the company is seeking to expand its product offering into machines that run on more sustainable energy sources.

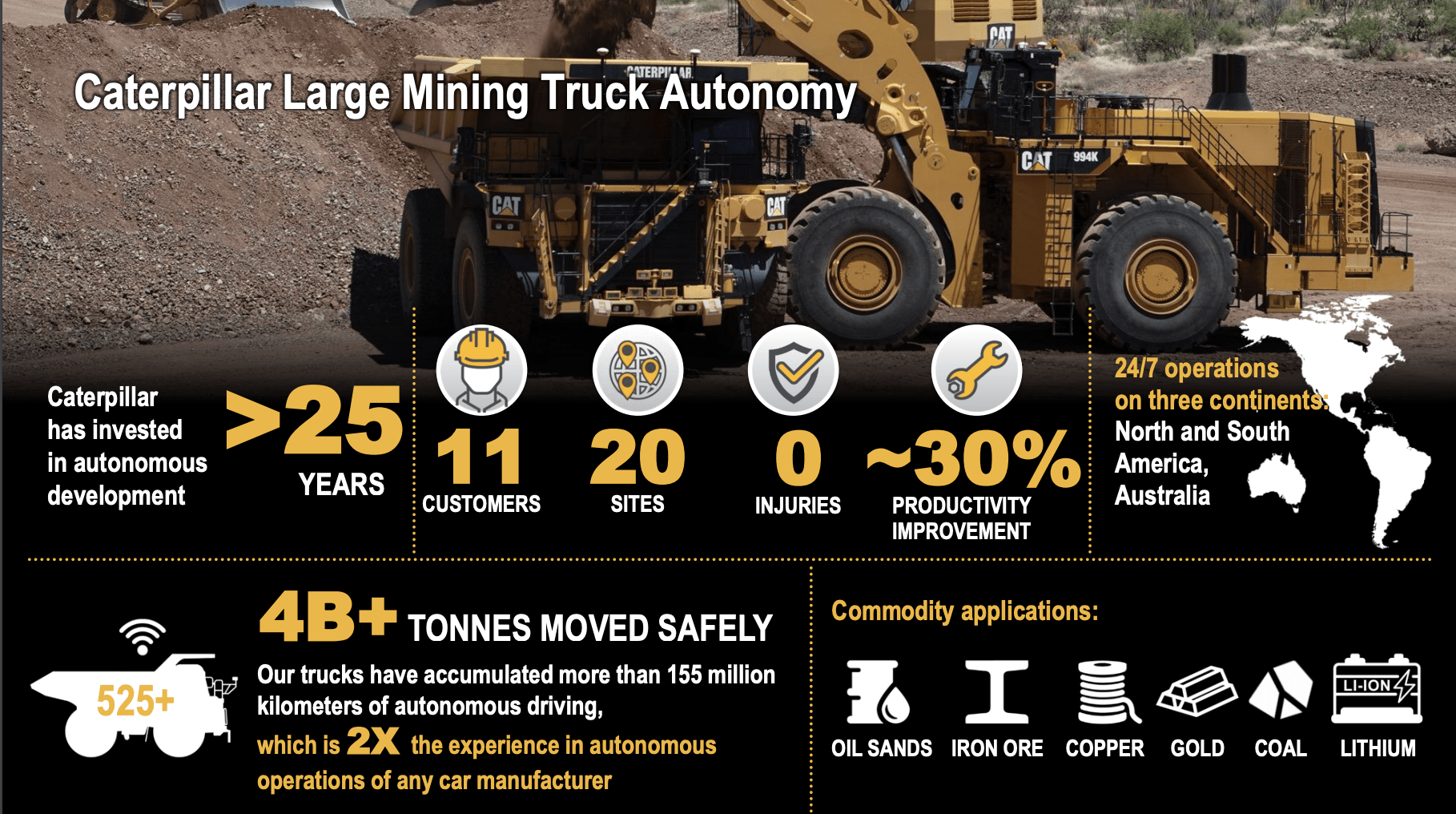

In all, Caterpillar has set a clear and comprehensive strategy for why their customers and stakeholders should participate with them. This, in turn, should support the company's ambition to deliver profitable growth. Another important pillar that Caterpillar is focusing on is automation. The focus on automation is not unique per se, but an important long-term growth initiative and differentiator. For large equipment companies like John Deere and Caterpillar, one of the best ways to limit the cyclicality in sales for the equipment industry overall is to offer SaaS-like services such as automation. Although recurring revenues are not expected to come to fruition at a high rate until 2027 and beyond for Deere, I believe it is important for equipment manufacturers such as Caterpillar to begin investing in technology like this. For these reasons, I give the company culture a rating of 9/10 .

Autonomous Experience in Mining (Caterpillar Investor Relations)

{kind=link}

2. Industry Potential

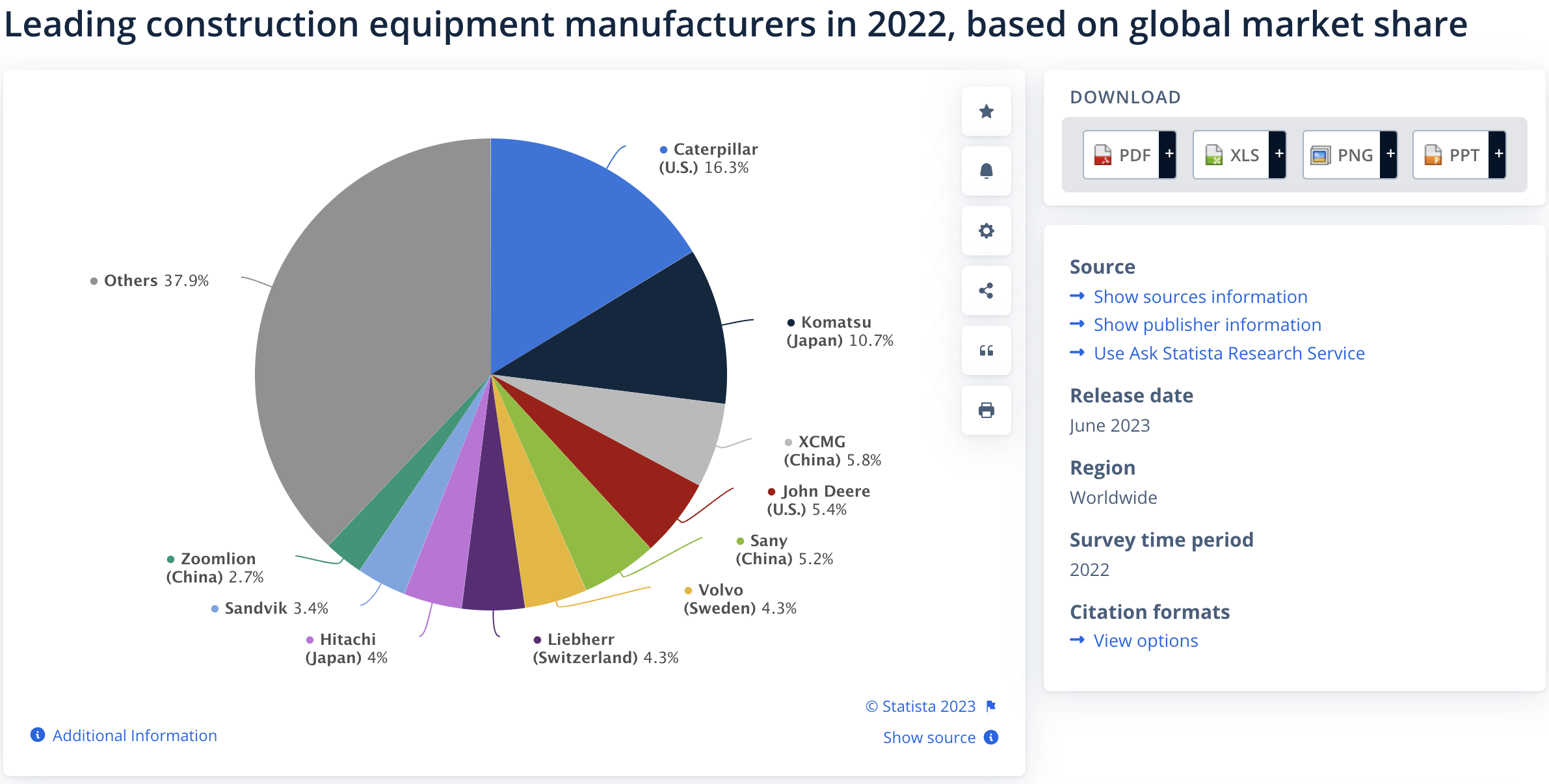

Caterpillar is impressively leading in the global market share for equipment manufacturers. As of 2022, the company had a global market share of 16.3%, which is well beyond the closest competitor Komatsu, with a 10.7% market share. Being an industry leader is a clear reflection of the quality of products and services that Caterpillar is able to provide to its customers.

{kind=link}

Allied Market Research estimates that the global construction equipment market, including services, was worth around $195 billion in 2022. The research firm expects the market to grow with a CAGR of 4.8% to $313.9 billion by 2031. This provides Caterpillar with an ample tailwind for growth going forward.

The direct growth drivers for the construction equipment industry are:

- Energy transition increases the demand for key mining commodities.

- Steady and growing demand for oil and natural gas.

- Large infrastructure spend.

Caterpillar wants to leverage its position as the market leader in mining and construction equipment and sees these areas as focus areas going forward. Furthermore, Caterpillar develops industrial engines for boats, vehicles, oil and gas facilities, and factories in general. Hence, the company believes that it will be able to develop more efficient and sustainable engines to meet the growing demand for such products.

The unique caterpillar yellow can be seen in almost any part of the world and based on its current market position as well as its strategy to lead going forward, I believe Caterpillar deserves a 10/10 with regard to industry potential.

3. Operating Leverage

As we can see from the historical data, CAT clearly has a great deal of operating leverage baked into its business model. It is clear that the company has been able to grow revenues significantly without expanding the fixed costs of the business nearly as much. Currently, quarterly revenue is around 8x as large as the company's quarterly expenses. One aspect however is that when sales dip, as they did in 2014-2016 CAT was not able to lower its operating expenses to adjust for the change in demand.

However, the lack of flexibility can be seen as a result of having operating leverage built into the business. If we take a closer look at the past five years we see that while revenues have grown by nearly 21%, operating expenses have only grown by 3.2%. This re-affirms the company's ability to drive operating leverage, which is the reason why the stock price has been performing so well recently. In all, I rate the company's operating leverage level with a 7/10 due to the incredible outpacing of sales to operating expenditures though weighed down by the lack of flexibility.

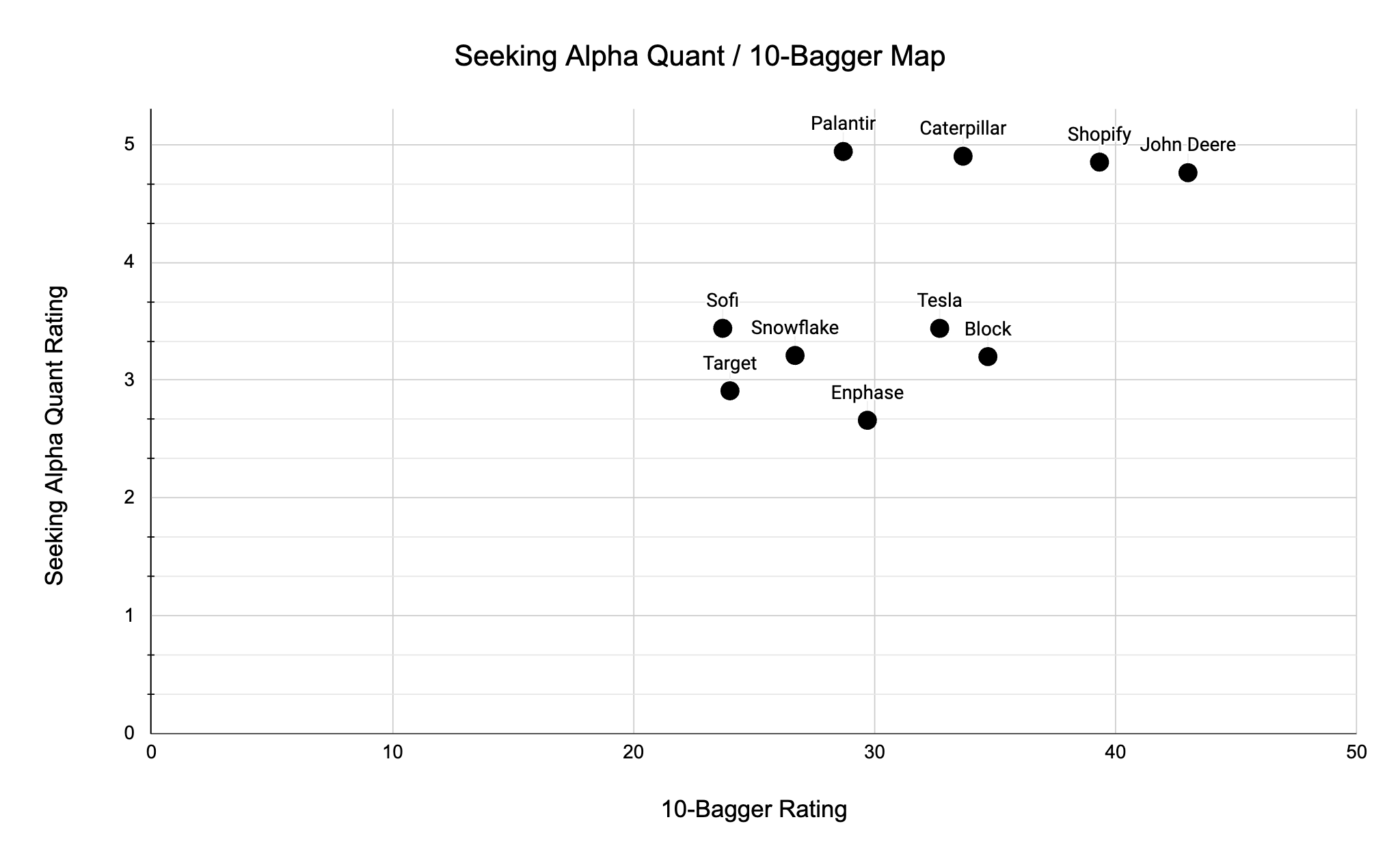

10-Bagger Rating & Seeking Alpha Quant Map

What follows now is a map continuously plotting the companies I analyze based on my 10-bagger rating and Seeking Alpha's quant rating. This allows us to gauge the performance of different companies over time.

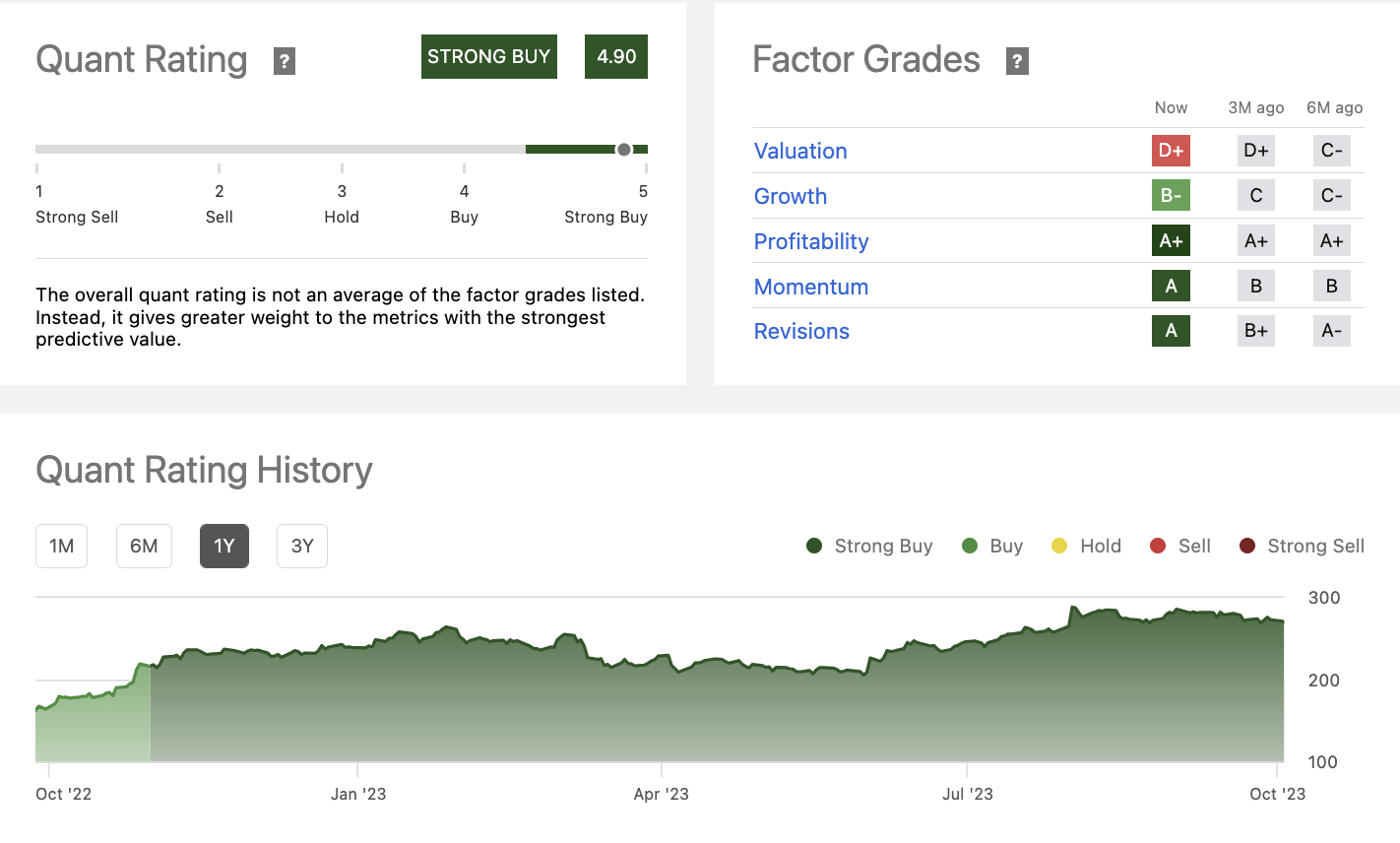

Caterpillar Q uant Rating: 4.9/5.00

{kind=link}

Rating Map

In this analysis, I find that Caterpillar scores 33.67/50 on the 10-bagger scale and 4.9/5.00 on Seeking Alpha's quant rating. This is one of Seeking Alpha's highest conviction strong buys that I have seen throughout this series. CAT has been rated a strong buy for almost a whole year due to incredible profitability, strong momentum, large revisions, and good growth.

{kind=link}

Will CAT Stock Go Down?

Evidently, the company's strong performance is attributable to being in a period of strong demand during the sales cycle. Deere has forecasted that the cycle for road construction equipment may be prolonged into 2025 due to large infrastructure spend - which would surely benefit CAT as well. However, given that the strong momentum tampers down, is CAT still fairly priced today?

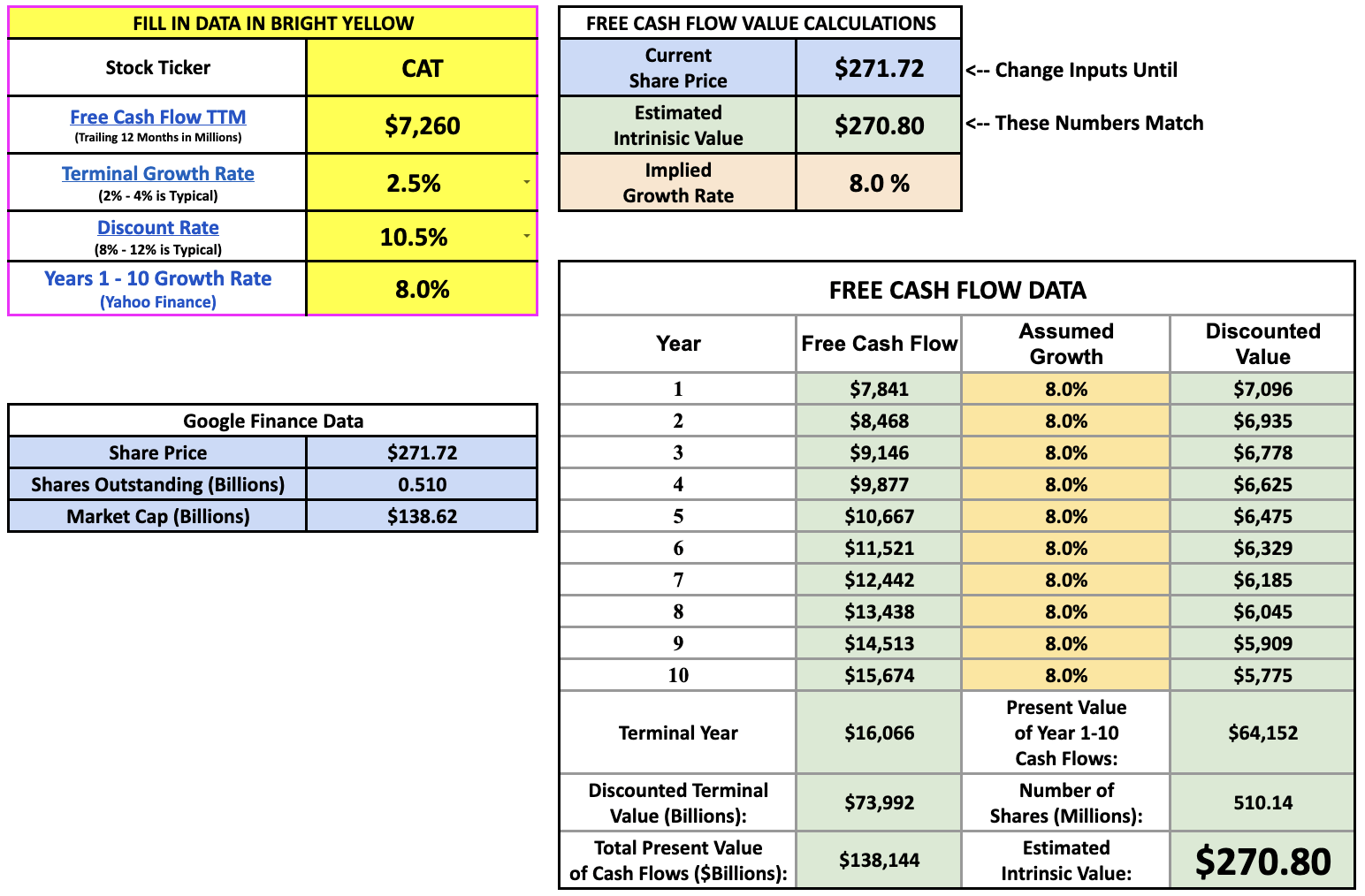

Given the current historically high free cash flow generation of the company, CAT only needs to grow its free cash flows by 8% to justify its valuation. The tricky part here however is that the free cash flows of this company after a market boom period sink to around $5 billion. This is in line with what happened after the booming 2013 period. Free cash flows steadily declined and averaged about $5 billion per year in "FCF" for the period. Given that cash flows revert to this level, the company will need to grow its cash flows by about 15% per year in order to justify the valuation.

The takeaway from this is that the market capitalization will likely decline given that the demand cycle dampens and cash flows weaken. However, the company is building up recurring revenue streams to dampen the effects of this cycle which could be a catalyst for continued high cash flows. Since this series is about the long-term potential of companies, I don't think it's useful to focus too much on the short/medium term. Clearly, CAT is an extraordinary company with strong management principles, which I believe justify it as a long-term buy.

{kind=link}

For further details see:

The Hunt For Potential 10x Returns: Will Caterpillar Stock Continue To Climb?