IIF - The India Fund: Still A Compelling Play On The 'GDP Growth Champion'

2024-01-19 16:41:27 ET

Summary

- Investing in the Indian growth story remains as attractive as ever.

- Unlike most other listed alternatives, the abrdn-managed India Fund offers a unique mix of capital growth and distributions.

- Alongside the many other boxes it checks, the India Fund is well worth its premium.

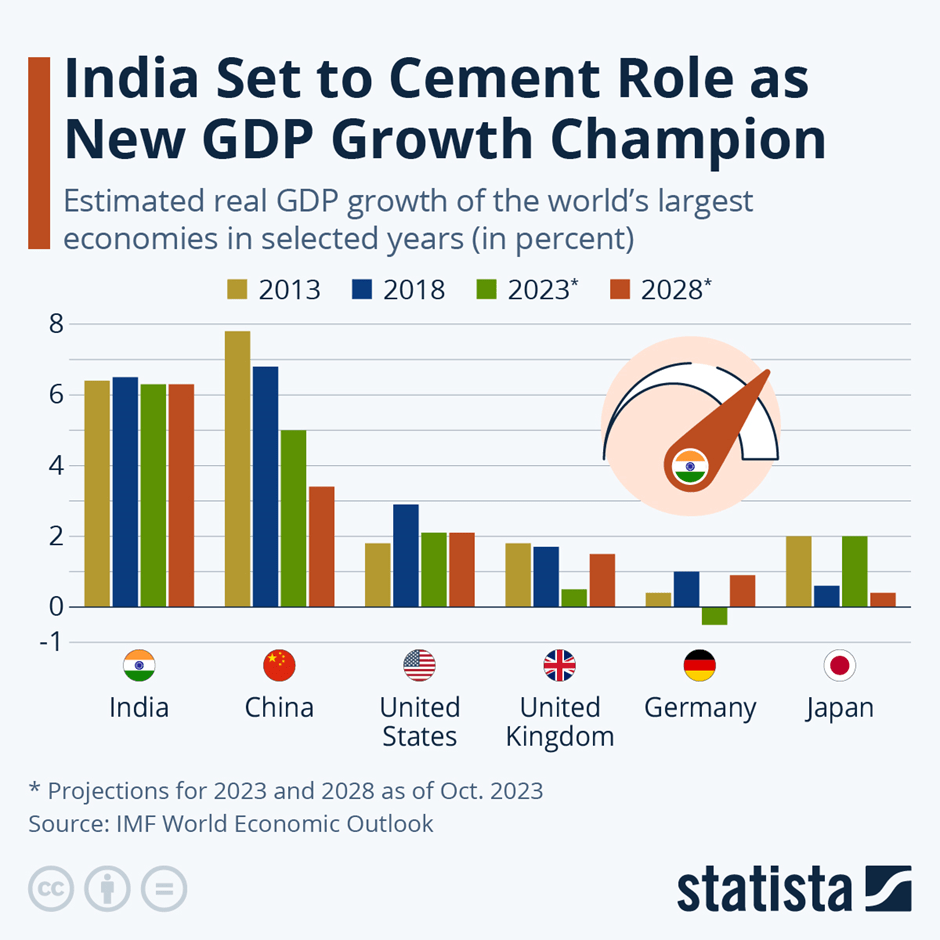

Consecutive quarters of above-consensus GDP growth puts India firmly in pole position to remain the fastest-growing major economy into 2024. Note that this has come against a weaker external backdrop, as well as significant monetary policy tightening throughout last year. If decelerating inflation prints are anything to go by, however, India could soon benefit from a central bank 'pivot', adding further legs to the near-term equity rally. As for the mid to long-term, the country remains well-placed to benefit from a wealth of growth drivers, including a capex upcycle , digitization , and an increasingly formalized economy - on top of its structural 'demographic dividend' tailwind. All told, predictions of India emerging as the world's 'new GDP growth champion' and the #3 global economic force by 2030 seem very realistic.

{kind=link}

Statista

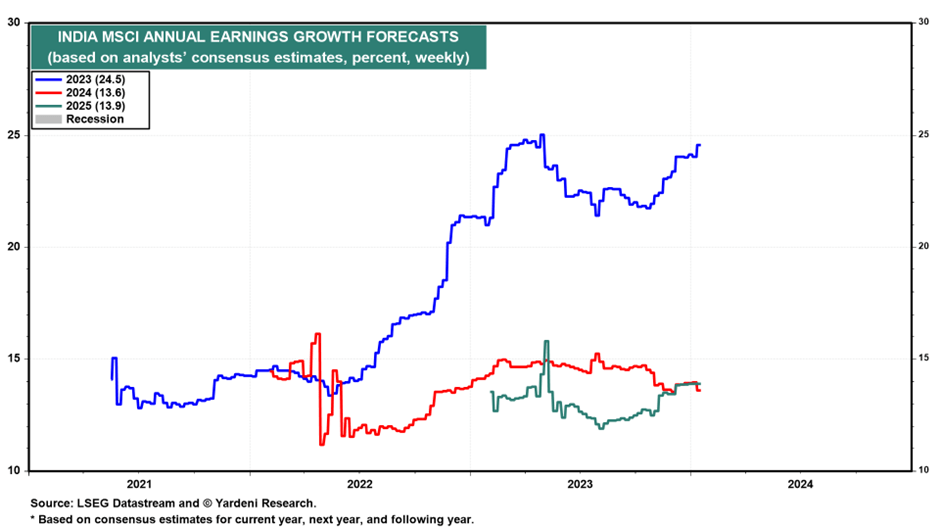

That said, there is a familiar catch to investing in India – high valuation multiples. Following last year's rally, the MSCI India benchmark is now priced at a wider premium to the rest of Asia at ~22x forward earnings. Yet, Indian equities have also delivered on earnings growth (consensus at +25% for 2023 and low-teens in 2024/2025), and thus, current valuations aren't unwarranted, in my view. There are also near-term catalysts here, from future index inclusions ( Bloomberg being the latest after JPMorgan (JPM) last year) to lower real rates (from a likely RBI and Fed pivot later this year).

{kind=link}

Yardeni

While the India Fund ( IFN ) offers less fund-specific optionality vs its key peer, Morgan Stanley's India Investment Fund ( IIF ) now that it's been re-priced to an NAV ('net asset value') premium, there are mitigating factors. For one, the manager's demonstrated willingness to enact shareholder-friendly policy changes is an uncommon one in the closed-end fund space. So is the fund's track record of outperformance vs MSCI India and best-in-class distribution. Ahead of an upcoming general election, where a policy continuity scenario now appears to be on the cards, investors looking for active Indian exposure should still find a lot to like in IFN.

India Fund Overview – A Competitively Priced Active Vehicle

The abrdn-managed India Fund, benchmarked against the MSCI India Index, continues to see impressive net asset growth. As of year-end 2023, the fund managed $549m, making it by far the largest US-listed Indian active manager. Despite the expanded asset base, IFN maintains a ~1.1% net expense ratio (~1.4% gross) per its latest factsheet – still competitive at a ~20bps discount to its closest active comparable, IIF. While fees are above passive alternatives like the ~70bps charged by iShares' MSCI India ETF ( INDA ), the IFN expense structure still screens very competitively when you factor in the added 'costs' associated with INDA's wide tracking error.

{kind=link}

abrdn

In line with previous quarters, the fund maintains its borderline 'closet indexer' active share (i.e., the portfolio composition difference vs. MSCI India). No surprises on the allocation breakdown either – per IFN's year-end disclosure , Financials still come out on top, with HDFC Bank ( HDB ) and ICICI Bank ( IBN ) at 7.6% and 7.5%, respectively. The absence of Reliance Industries continues to be IFN's largest delta vs MSCI India, while the most notable new overweight is cement leader UltraTech Cement ( OTC:UCLQF ) at 5.0%. While IFN remains relatively concentrated, the reduced contribution of its top ten holdings to ~49% is a positive development.

| Security Long Name |

| Shares/Par Value |

| Base Market Value |

| Percent of Fund |

| HDFC BANK LIMITED COMMON STOCK INR1.0 |

| 2,150,542 |

| 44,019,083 |

| 7.6% |

| ICICI BANK LTD COMMON STOCK INR2.0 |

| 3,647,684 |

| 43,667,817 |

| 7.5% |

| ULTRATECH CEMENT LTD COMMON STOCK INR10.0 |

| 231,610 |

| 29,160,297 |

| 5.0% |

| HINDUSTAN UNILEVER LTD COMMON STOCK INR1.0 |

| 901,805 |

| 28,809,319 |

| 5.0% |

| INFOSYS LTD COMMON STOCK INR5.0 |

| 1,528,732 |

| 28,292,978 |

| 4.9% |

Source: abrdn India Fund Disclosures (Year-End 2023)

India Fund Performance – Keeping Pace with MSCI India; Hefty Distributions

IFN hasn't released its year-end factsheet yet, but Morningstar numbers show the fund ended 2023 on a high, up +36.7% in market price terms. Even after adjusting for the market price-NAV swing, returns would have still been very strong at +21.4% - well above the largest and most liquid passive MSCI India tracker INDA (+17.5%). The fund's longer-term track record is stellar as well, producing a low teen percentage annualized return (including distributions) over the last decade. While only just above its MSCI India benchmark, it's worth noting the elevated 'hidden' costs (capital gains taxes, transaction costs, etc.) associated with deploying capital in India; in this context, IFN has done exceptionally well through the cycles.

{kind=link}

Morningstar

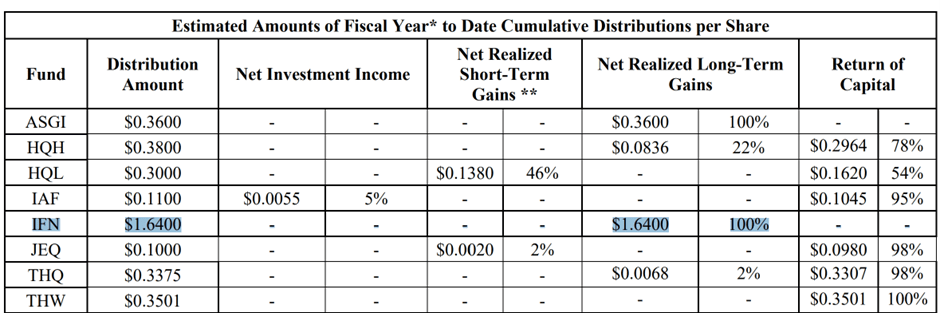

Where IFN really shines, though, is its generous distribution policy - a key reason behind the narrowing NAV discount last year (in fact, IFN now trades at a premium). The ~10% rolling distribution rate (comprising both income and capital gains) and stock distribution policy are notably intact - last year, for instance, saw the fund distribute the equivalent of $1.64/share.

{kind=link}

abrdn

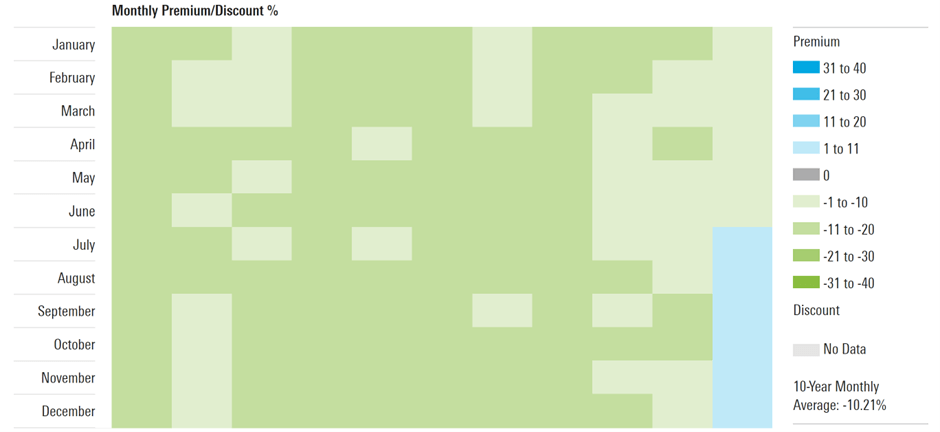

For now, the distribution is well-supported. As this yield is entirely funded by capital gains, though, investors should be mindful of the income stability should market gains run dry – an equity downturn, for instance, would likely see much lower payouts. The other potential risk is the market price-NAV delta, which now stands at a ~4% premium – rare in the closed-end fund universe, where shares typically trade at discounts on the secondary market. In this regard, key comparable IIF is probably the better pick, given its high teens discount implies upside optionality if the manager ever decides to follow the IFN roadmap. Still, investors who want the best of both worlds today (capital gains and distributions) will find a lot to like with IFN.

{kind=link}

Morningstar

Still a Compelling Play on the 'GDP Growth Champion'

2023 may have been a great year for India, but the next few years could well be even better. In an environment of decelerating GDP growth across Asia, India continues to stand out with consistent high-single-digit prints. This growth has been accompanied by more disinflation than inflation as well, and core is now well within target - positive signs for a monetary policy 'pivot' in the coming months. To be fair, valuations are also elevated, but justified by underlying fundamentals; foreign participation is also recovering and thus, the path of least resistance is likely higher, not lower. IFN is as good as any US-listed vehicle for Indian exposure, in my view – even after factoring in the NAV premium, IFN's performance and peer-leading distributions remain compelling reasons to own the fund.

For further details see:

The India Fund: Still A Compelling Play On The 'GDP Growth Champion'