SJM - The J. M. Smucker: Historically Strong Performance But Costly

2023-04-17 02:51:48 ET

Summary

- The J. M. Smucker Company has strong brand loyalty and pricing power in American staples with leading brands, such as Jif peanut butter, Dunkin', and Milk-Bone.

- The company is divesting in low-margin products and focusing on high-growth products, aiming to grow its uncrustables, coffee, and dog snacks segments into billion-dollar businesses.

- We are cautious of decreasing FCF, high capex, rising staple food costs, and impact on gross profit margins.

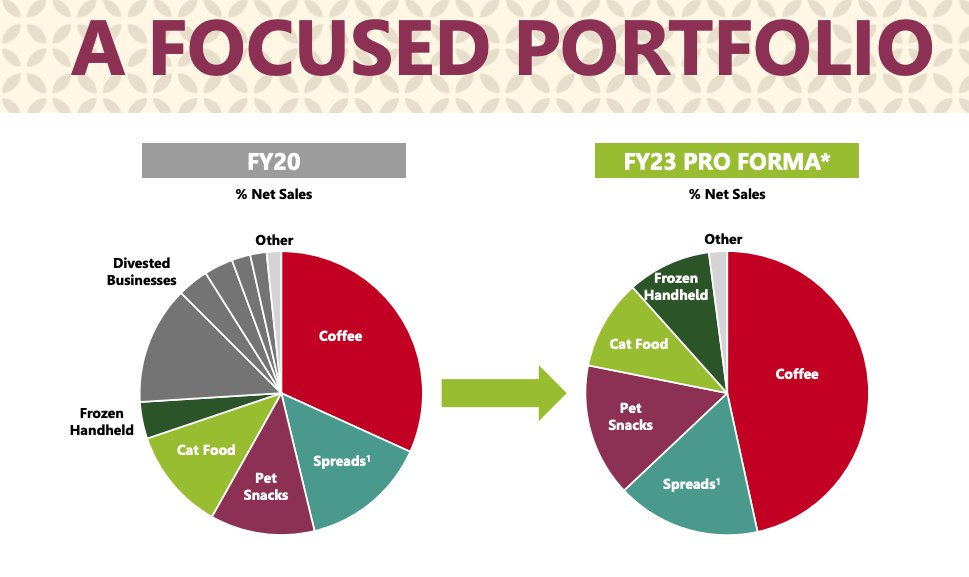

The J. M. Smucker Company ( SJM ) is a dividend-rewarding consumer staples stock at a large market cap of $16.40 billion. SJM is a mixed bag; on the one hand, it is attractive due to its long and robust performance history dating back to the 1800s, in which we have seen the company grow due to acquiring strong market-leading brands in American staples, such as its core peanut butter and jelly offerings which bring a timeless sense of customer loyalty. However, the company is recovering from an acquisition frenzy, which left it with several costly underperforming products. Over the last few years, SJM has been refocusing its efforts by divesting low-margin products and investing in growth products.

Major divesting efforts (Investor Presentation 2023)

{kind=link}

Its business strategy looks set to bring long-term top and bottom-line growth. However, in the short term, these actions are predicted to negatively impact its annual EPS for FY2023 and underperform on its annual Free cash flow target of $1 billion due to rising CapEx. While it is positive to see top-line growth across its coffee and pet snack businesses, the stock price is currently above the average analysts' stock price of $152,36. Therefore, I recommend a hold rating while waiting on a better entry price.

Company overview

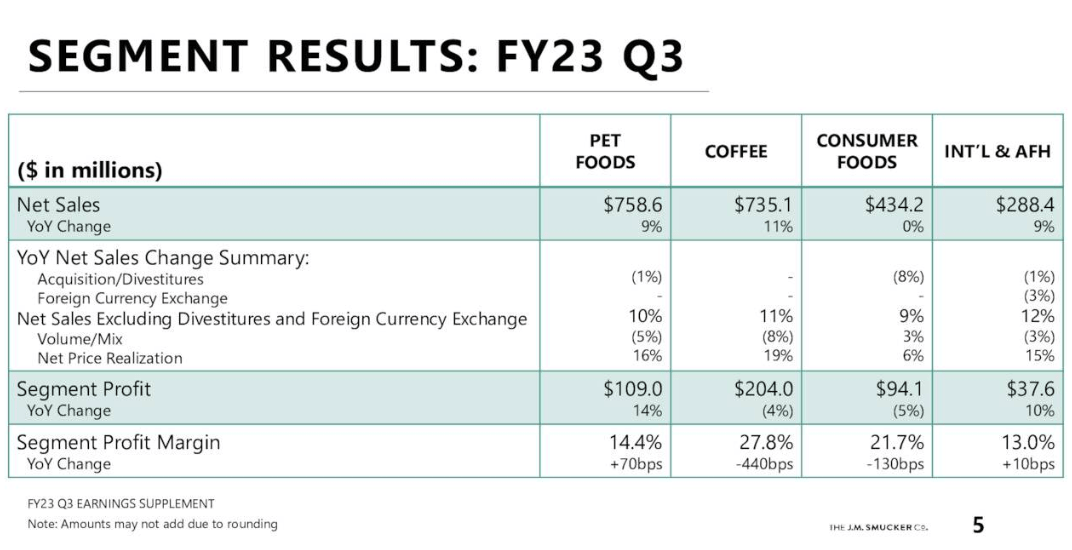

SJM is a company with a long history in the United States and globally founded in 1897 in Ohio, USA. A significant growth driver for the company has been its inorganic growth by acquiring successful brands such as Jif peanut butter in 2001. We saw SJM go on a considerable acquisition frenzy, particularly in the pet food industry, which left them with low-margin-producing brands that negatively impacted the business. SJM has been working on refocusing its portfolio by selling off underperforming businesses. SJM reports on three main revenue-generating segments: Pet Foods, Coffee and Consumer Foods. Its international revenue and away-from-home products are combined in its smallest fourth segment. We can see that over the last nine months, while total net sales have increased YoY, the whole segment profit has decreased due to increased costs.

Q3 2023 Sales versus Profit per segment (sec.gov)

Growth drivers but costs creep in

There are some impressive tailwinds for SJM's top line in its essential coffee and pet foods business if we look at the YoY results generated in its Q3 2023 results. However, increasing staple costs have particularly hit the coffee business, negatively impacting the segment's profit.

Q3 2023 Segment results (Investor presentation 2023)

{kind=link}

However, coffee remains a compelling long-term segment; post-pandemic, 68% of coffee cups are still consumed at home , and there is a trend to replicate high-quality coffee in the comfort of your home. SJM has a diverse range of coffee brands to meet many consumer needs.

Diverse coffee brand portfolio (Finance Yahoo)

{kind=link}

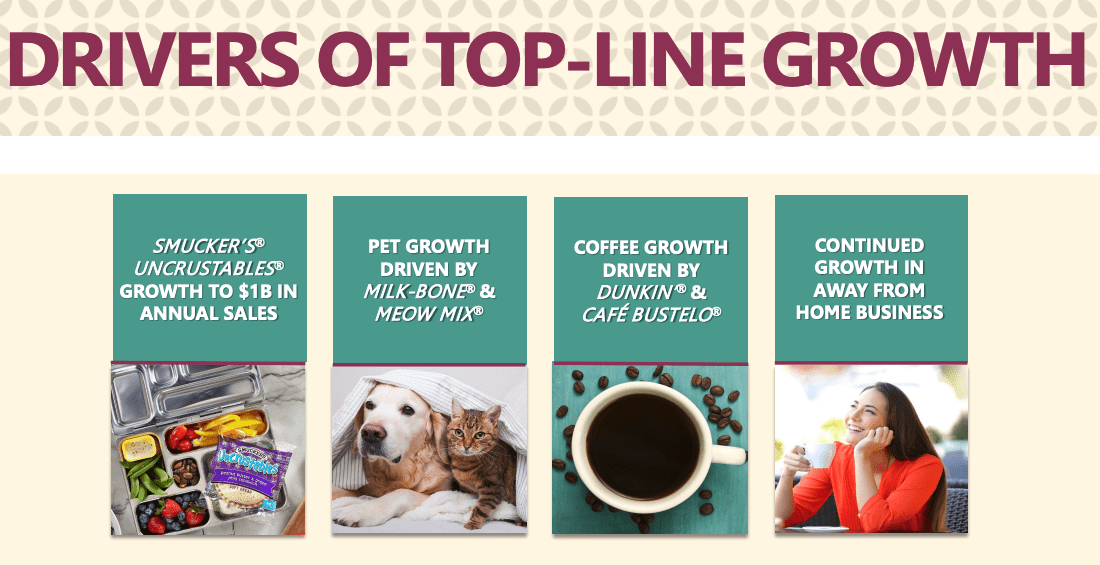

Furthermore, within the pet business, SJM sold off its lower margin brands within its dog and cat food business to Post Holdings for $1.2 billion. At the same time, it taps into pet snacks' growth momentum through its Milk-Bine and Meow Mix brands.

Top-line growth drivers (Investor presentation 2023)

{kind=link}

SJM continues to benefit from at-home consumption trends if we look at its double-digit growth numbers in its coffee business. This trend is influenced by the slowing economy, high inflation and consumers reducing their eating-out budgets. As consumers remain cautious in fear of a looming recession, SJM benefits as they provide various value products across a diverse brand portfolio. However, the cost of divesting, the increase in staple food costs and refocusing on growth products are proving costly for the business and cut into earning potential for the upcoming FY2023 results.

Financials and valuation

SJM is a well-established business with a long-standing history of delivering steady top and bottom-line results and rewarding investors with a consistent and growing dividend program. However, the business has been dealing with recovering profit margins due to an accumulation of low-margin products over the years. Divestment and increased CapEx into growth, such as new facilities, have been cutting into EPS and free cash flow.

Annual income statement (Marketscreener.com)

{kind=link}

This past year, gross profit margins have been impacted by an increase in staple product costs, particularly in their growing coffee segment. We can see that the TTM gross profit margin is 32.23% compared to 39.26% two years prior. However, we can see that since FY16, the company has made significant improvements through its divestment strategy of underperforming businesses, such as its canned milk operations in 2015.

Annual gross profit margins (Seeking Alpha)

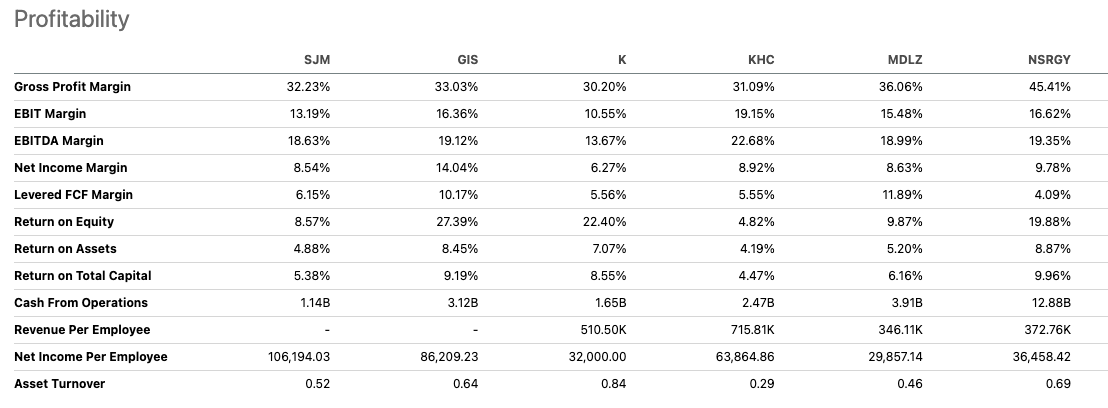

Gross profit margin is critical in understanding the strength of brands within the consumer staple food industry. If we compare SJM to its peers, we can see that its gross profit margin falls under a few of its key larger consumer staple peers.

Peer comparison (Seeking Alpha)

{kind=link}

SJM has a positive levered free cash flow of $511.83 million TTM and saw an improved cash flow generation in the prior quarter of Q3 2023. However, although the company generates positive cash flow, it is expected to decrease for FY2023 to $550 million, under the company's target of $1 billion annually. This has been connected to a product recall in their Jiff product, increased capital expenditure related to building Uncrustable facilities and tax payments. In the Q3 2023 earnings call, the management indicated that although $1 billion in free cash flow is their target, this may not be achieved in 24 due to continued CapEx costs.

Annual levered free cash flow (Seeking Alpha)

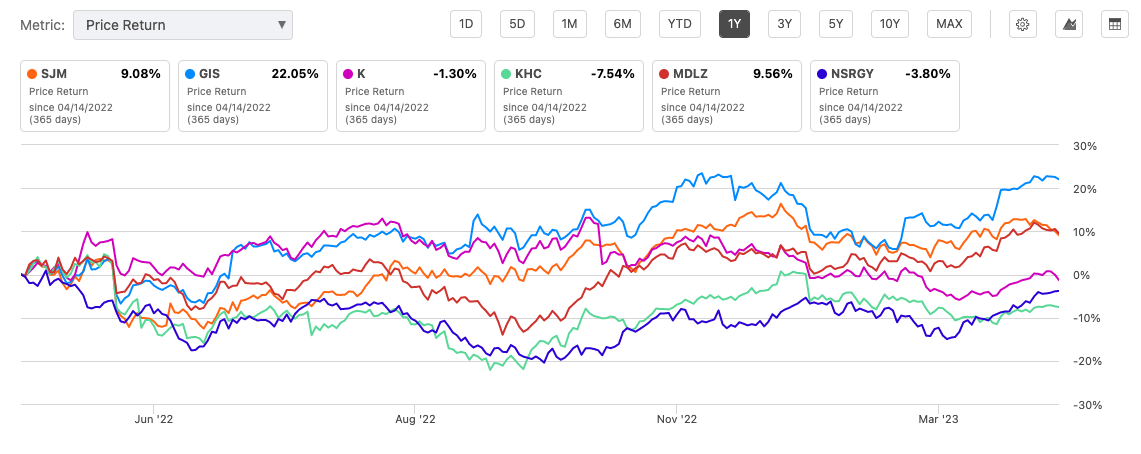

SJM has recently been upgraded to a Buy by analyst Argus due to predicted profit improvements. However, these improvements are not expected for FY2023 if we look at the expected YoY decrease in EPS by 2.19% $ YoY to $8.69. The stock is rated a Hold by various analysts, and it has an average target price of $152.36, according to Market Screener. We can see that SJM has been rewarding to hold as a stock over the last year compared to some of its peers at a price return of 9.08%, and over the previous ten years, investors have been rewarded with returns of 49.17%.

One-year price return versus peers (Seeking Alpha)

{kind=link}

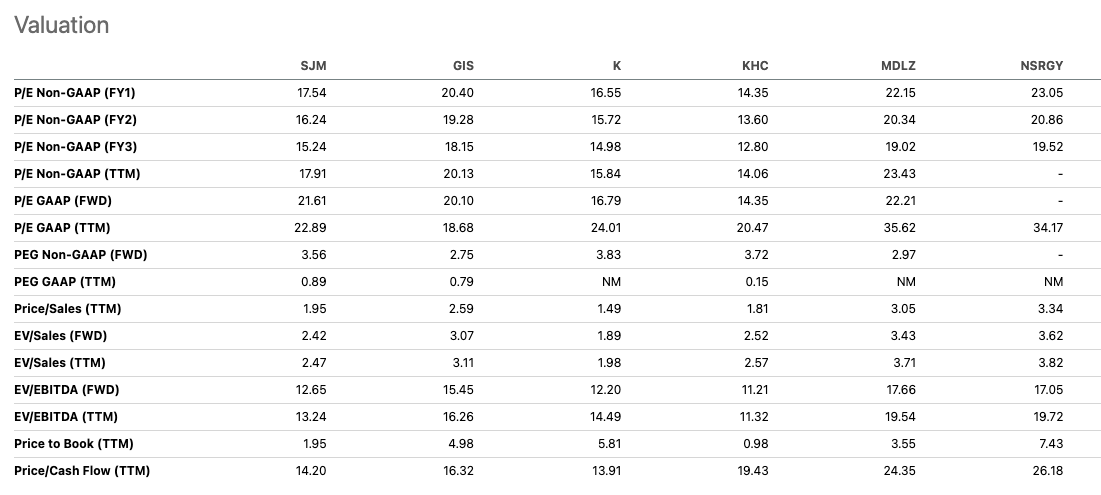

If we look at SJM's price-to-earnings ratio, we can see that it has a high FWD price-to-earnings ratio of 21.61 compared to its peers. Therefore the stock may be overvalued at this point. We can also see that its price-to-sales ratio of 1.95 indicates that investors are paying more than one dollar for every dollar earned.

Relative peer valuation (Seeking Alpha)

{kind=link}

Final thoughts

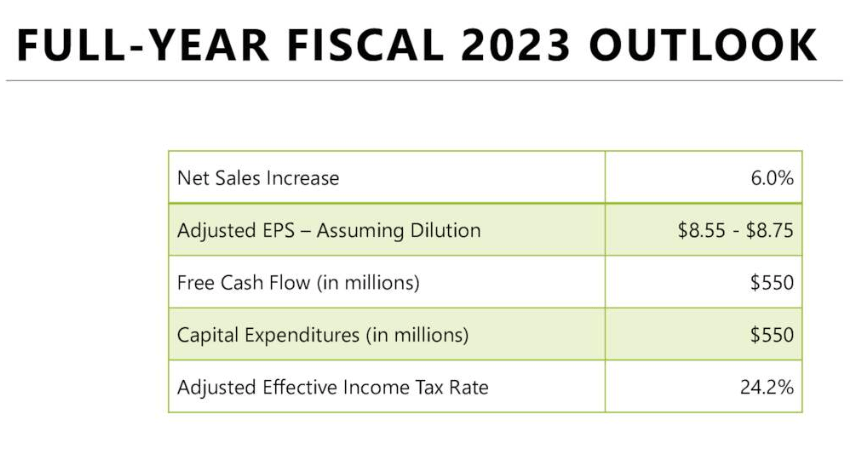

SJM is focused on its growing coffee and dog snacks & cat food segments which are all experiencing impressive year-on-year growth numbers. Investing and divesting in these businesses is taking a toll on the company's FCF, which will fall well below its usual annual target of $1 billion, and this trend will likely continue into FY2024. EPS is expected to decrease by 2.19% YoY to $8.69. While I am optimistic about the company's actions, the stock price is unattractive at this point, and therefore recommend a Hold and waiting for a better entry price.

Full year 2023 outlook (Investor Presentation 2023)

{kind=link}

For further details see:

The J. M. Smucker: Historically Strong Performance, But Costly