SPXN - The January PCE Report Unleashes A Giant Inflation Shockwave

Summary

- The January PCE report was a blowout and much hotter than expected.

- The market is now pricing in even more rate hikes, and higher terminal rate.

- Fantasyland and story time for the bulls is over.

Inflation returned with a vengeance in January as the PCE report was much hotter than expected. This sent shockwaves through the bond market as expectations built for more rate hikes and a much higher Fed terminal rate.

More importantly, the fantasy that the Fed would cut rates in 2023 has faded away, as only ten basis points separate the terminal rate and the December Fed Fund Futures contract. This is horrible news for the bulls because, at this point, stocks are overvalued relative to bonds and offer no earnings growth.

Hot PCE

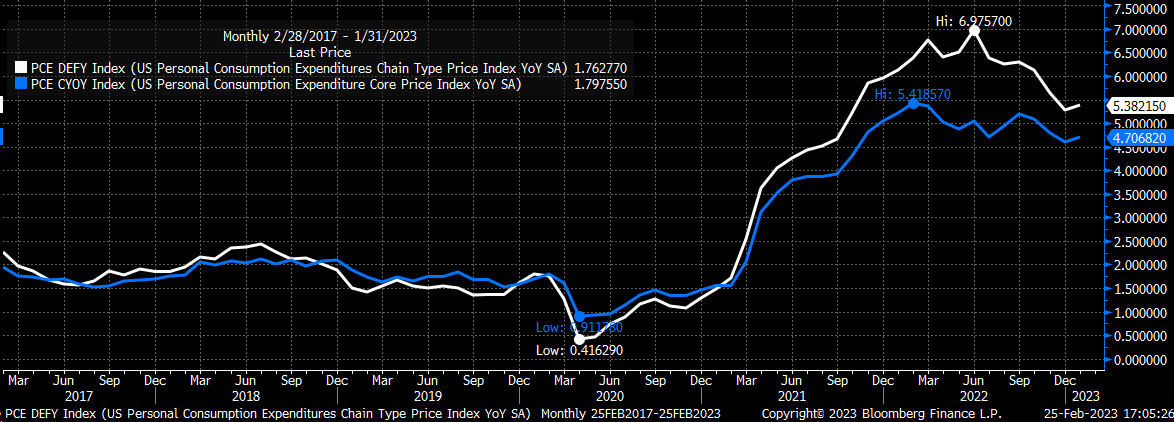

For January, the PCE increased by 0.6% month-over-month versus estimates of 0.5% and rose by 5.4% year-over-year versus forecasts of 5.0%. Meanwhile, core PCE rose by 0.6% versus estimates of 0.4% and climbed by 4.7% year-over-year versus forecasts of 4.3%.

Anyone that thinks this number wasn't a massive beat has no idea what the implication will be and is likely living in some fantasyland. Not only did this reverse a disinflation trend for both headline and core PCE but it also means that more rate hikes are coming because the recent rate hikes have had almost no impact on inflation or slowing the economy.

{kind=link}

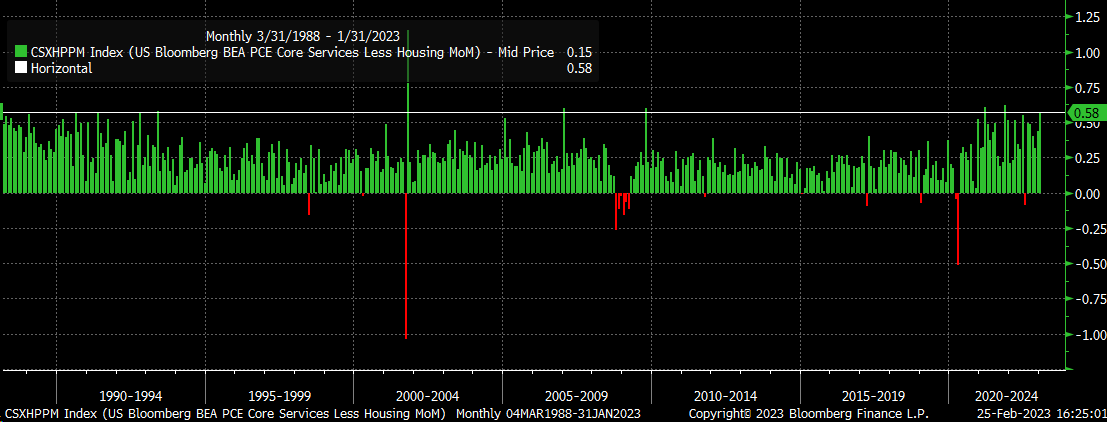

Even worse is that PCE core services less housing, a metric the Fed has talked about repeatedly, posted one of its most significant month-over-month increases in 35 years, rising by 0.58%.

{kind=link}

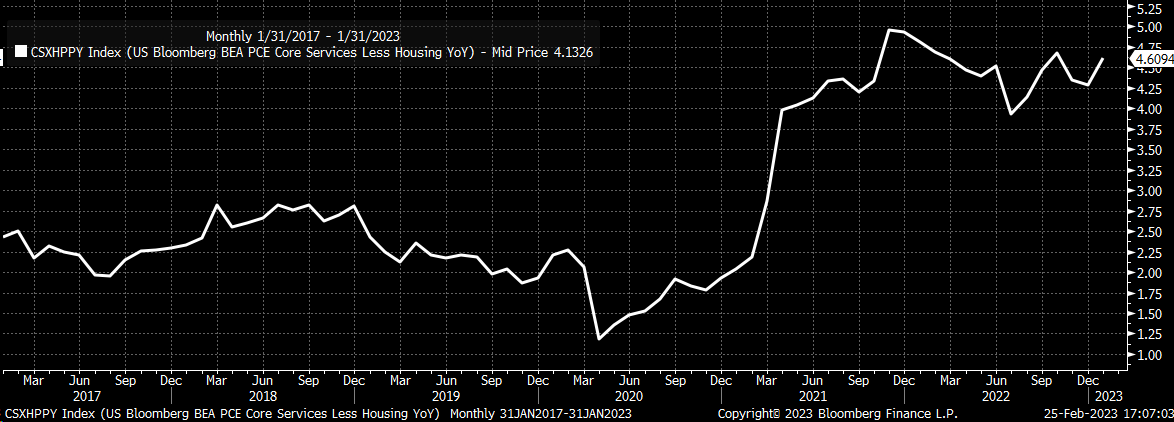

Additionally, PCE core service less housing increased by 4.61% year-over-year, and it also shows stickiness, as the Fed has been barely able to make a meaningful impact.

{kind=link}

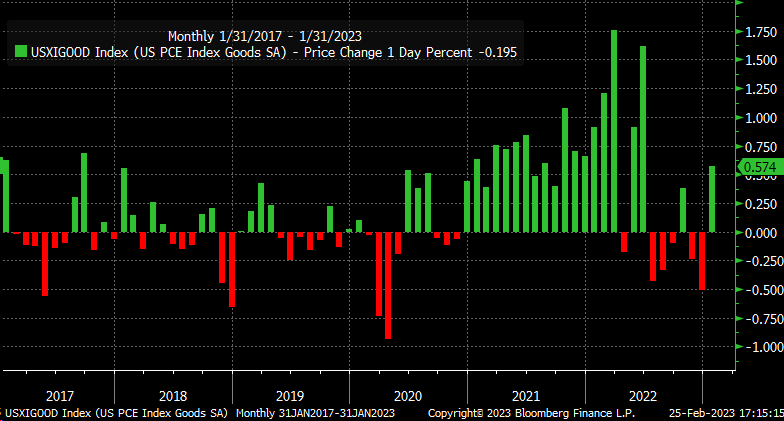

On top of that, goods inflation came back in a big way in January, rising by almost 0.6% month over month. That was the most significant increase since June, reversing much of the decline in the last two months.

{kind=link}

Massive Impacts On Monetary Policy

The impacts are clear; the market now sees 3 or 4 more rate hikes in 2023. That is not only a massive change from prior expectations, but that would be well above the Fed's December summary of economic projections.

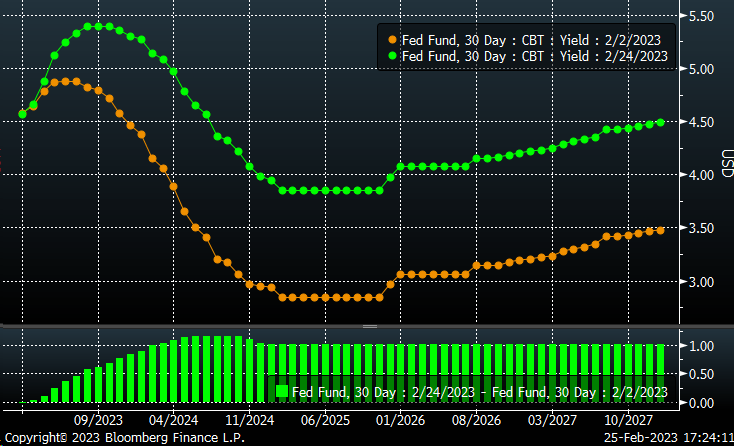

Fed Funds Futures contract shows a terminal rate of 5.4% by August. It was on February 2 that the market saw a terminal rate of 4.88%. Now not even a month later, that terminal rate has risen by more than 50 bps. On top of that, the futures now show rates falling to just 5.3% by December, suggesting no rate cuts in 2023. This is a significant reversal from February 2, when the market saw the December contract at 4.46%, priced in more than one rate cut in 2023. The market now thinks the first Fed rate cut rate doesn't happen until February 2024.

{kind=link}

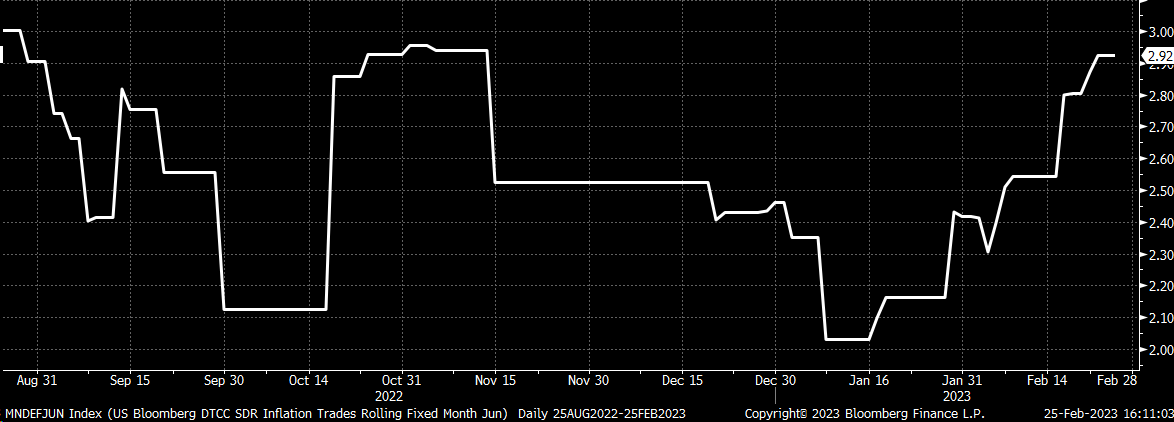

Additionally, expectations are for inflation to run hotter for longer, as the market prices higher inflation over the next several months. For example, the June CPI inflation swap was pricing in 2% inflation back at the beginning of the year; now, that same inflation swap is pricing in 3%.

{kind=link}

Massive Market Impacts

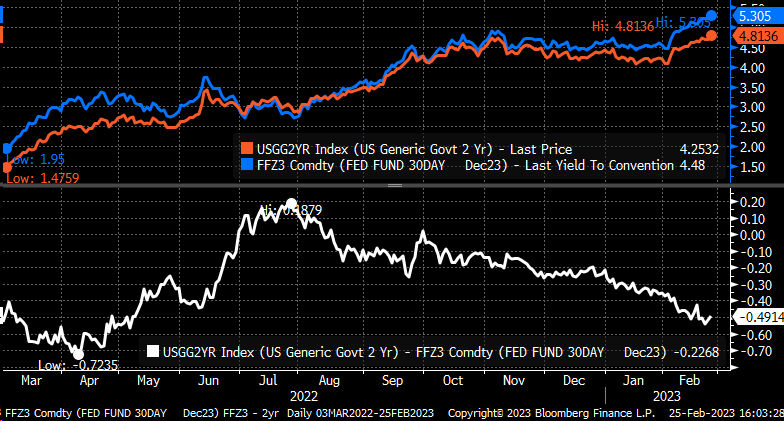

With the December Fed Funds Futures now trading at 5.3%, the 2-year nominal rate is trading at 4.82% and is probably on its way above 5% in the not-too-distant future. The spread between the 2-year and the December contract is now almost 50 bps. The longer the December contract stays elevated, the more likely the 2-year Treasury drifts higher towards that December in the near term.

{kind=link}

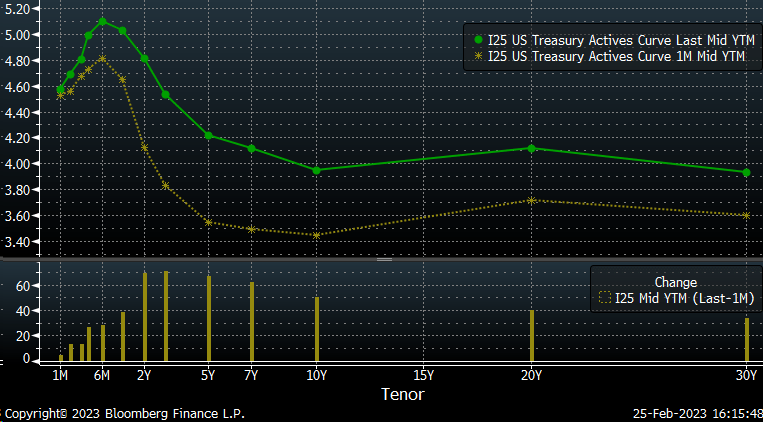

Expectations for higher inflation, a higher Fed terminal rate, and a higher 2-year Treasury have pushed nominal rates across the curve higher. The most significant changes in rates have come between the two and 10-year Treasury rates.

{kind=link}

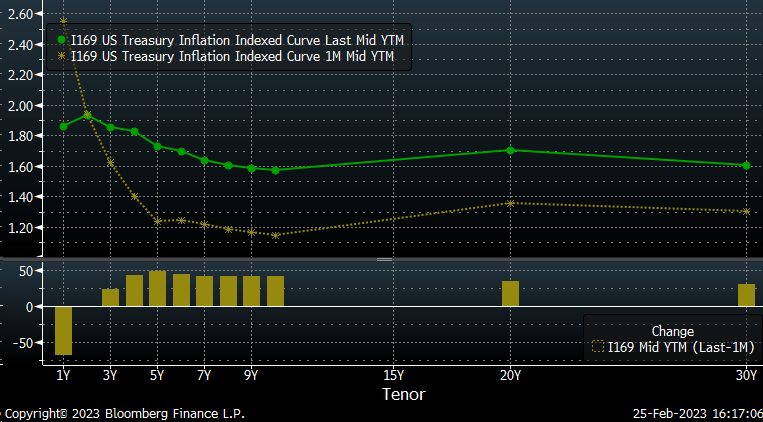

Additionally, real rates have exploded higher as well. For example, the five- and 10-year real yields have risen by more than 40 bps over the past month.

{kind=link}

Expectations for higher rates from the Fed have resulted in the dollar index breaking out and heading higher. The combination of higher rates and a stronger dollar will tighten financial conditions, and tighter financial conditions will work against rising equities.

Stocks Are Overvalued and Offer No Growth

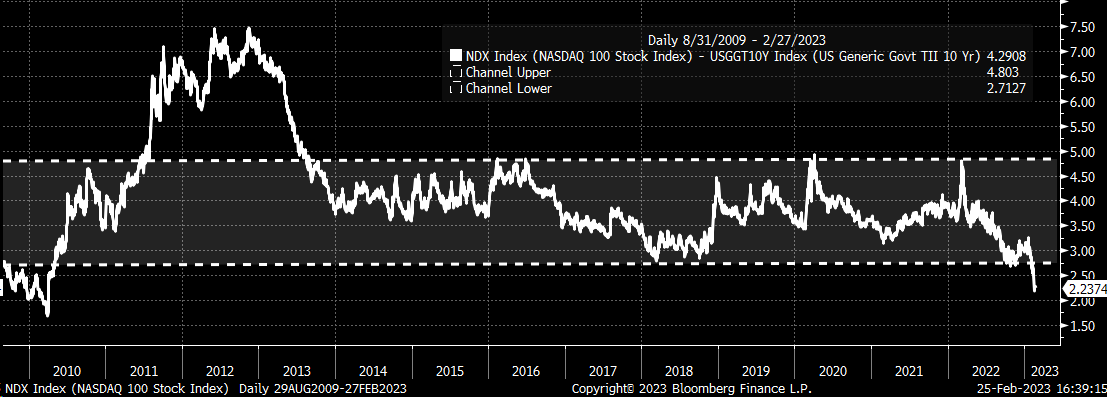

Additionally, valuations for stocks are stretched, with the NASDAQ 100's current earnings yield now trading just 2.23% above the 10-year real yield. That means that on a relative basis, the NASDAQ 100 is at its most expensive point relative to real rates since 2010. Since 2013, the NASDAQ 100's current earnings yield minus the 10-year real yield has been between 2.75% and 4.85%. However, in 2023, that spread has become more narrow, suggesting that NASDAQ earnings yield needs to rise as rates generally rise, meaning NASDAQ prices need to fall.

{kind=link}

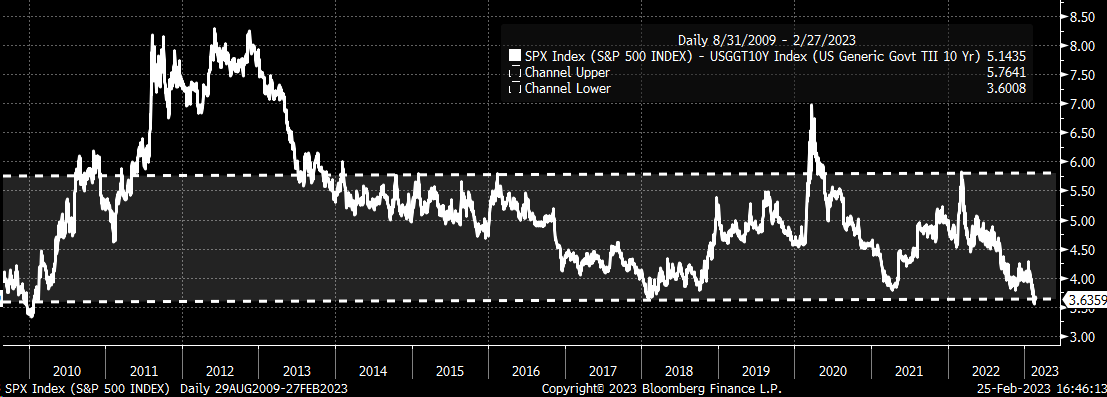

It isn't much better for the S&P 500 either, with the current earnings yield minus the 10-year TIP rate at the lower end of the trading range, since 2010, again suggesting that stocks are overvalued as a group versus bonds.

{kind=link}

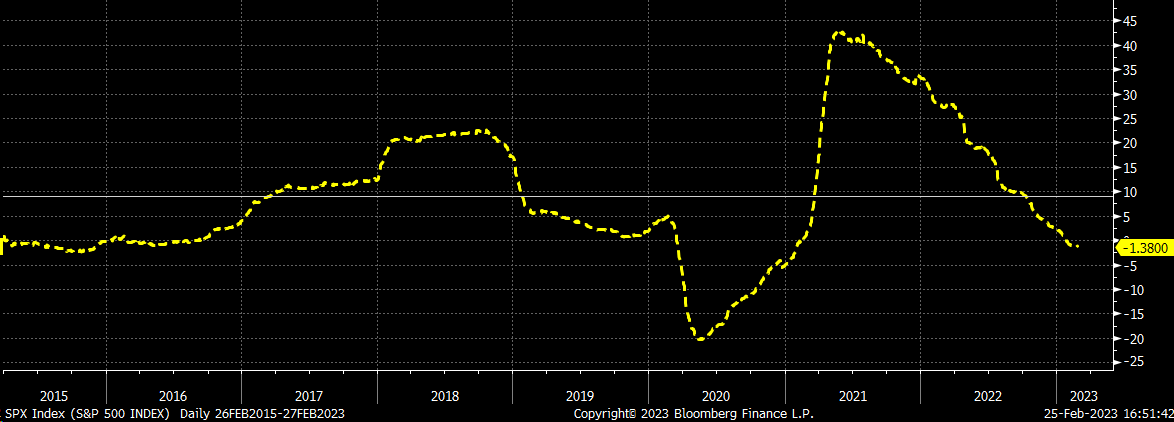

On top of stocks being expensive relative to bonds, stocks offer no earnings growth in 2023. The S&P 500 is expected to see its 1-year blended earnings fall 1.4% this year. So not only is the S&P 500 expensive relative to bonds, it is expensive relative to its forecasted earnings growth rate, with the index currently trading at more than 18 times earnings.

{kind=link}

So as long as inflation stays hot and expectations are for rates to go higher, the pressure will remain on equities, which means that stocks will continue to decline over the near term or until stock and bond valuations come to some agreement.

Based on this last PCE report, the Fed won't be finished raising rates any time soon, and that means yields are probably heading higher, and stocks need to give back all of their 2023 gains, and probably more.

For further details see:

The January PCE Report Unleashes A Giant Inflation Shockwave