JYNT - The Joint Corp.: Cracking Upside Bet Or Creaking Business Model?

2023-08-03 15:31:26 ET

Summary

- Joint Corp. will report earnings on Aug. 10.

- The company's stock is down >70% in the past two years.

- The business model may lack punch, but even so the low valuation may be unjustified.

Investment Overview - Joint's Pain

It has been a while since I have covered The Joint Corp ( JYNT ) for Seeking Alpha.

I gave the company - whose principal business is to "develop, own, operate, support and manage chiropractic clinics through direct ownership, management arrangements, franchising and regional developers throughout the United States," according to its Q1 2023 10Q submission (quarterly report) - a "Buy" recommendation back in August 2020 , when shares traded at $14.

The next time I covered the company , in April 2021, the stock price had risen to $48 per share - up >240% in less than 12 months. This time, I was much more cautious on the company, issuing a "Hold" recommendation and concluding:

I would wait a couple more quarters before considering an investment, to see what the cash flow generation and growth is like in 2021. I think Joint more or less has the share price it merits at the current time and its growth prospects are not quite compelling enough to support much more upside.

Although I was no longer bullish on Joint, owing to the share price apparently growing disproportionately faster than the business model itself, by September 2021 its stock price had risen >$100, valuing the company >$1.5bn market cap.

Nevertheless, two years on, the share price has declined by >70%, trading at $13.4 at the time of writing, and the market cap has fallen to a measly $196m. What happened to this apparently promising business and investment opportunity?

Why Has Joint's Rise And Fall Been So Pronounced? Slow Growth And Lack Of Profits An Issue

As I wrote in my August 2021 note on The Joint Corp:

Joint describes itself as a "franchisor and operator of chiropractic clinics that uses a private pay, non-insurance, cash-based model" and its ambition is to become the "most recognized brand in our industry through the rapid and focused expansion of chiropractic clinics in key markets."

The company's clinics are no frills operations, whereby patients arrive, are escorted to an open bay area, remove outer clothing only and are attended to for 15-20 minutes by a licensed practitioner if on a first visit, and 5-7 minutes thereafter. There are no add-on services, devices or chronic care services.

Back then, Joint's stated ambition was to operate 1,000 clinics by the end of 2023, and it almost on track to achieve that figure - according to the company's Q1 2023 10Q :

As of March 31, 2023, we and our franchisees operated or managed 870 clinics, of which 740 were operated or managed by franchisees and 130 were operated as company-owned or managed clinics. Of the 130 company-owned or managed clinics, 61 were constructed and developed by us, and 69 were acquired from franchisees.

That appears to represent quite encouraging growth, although Joint's last quarterly report also reveals that:

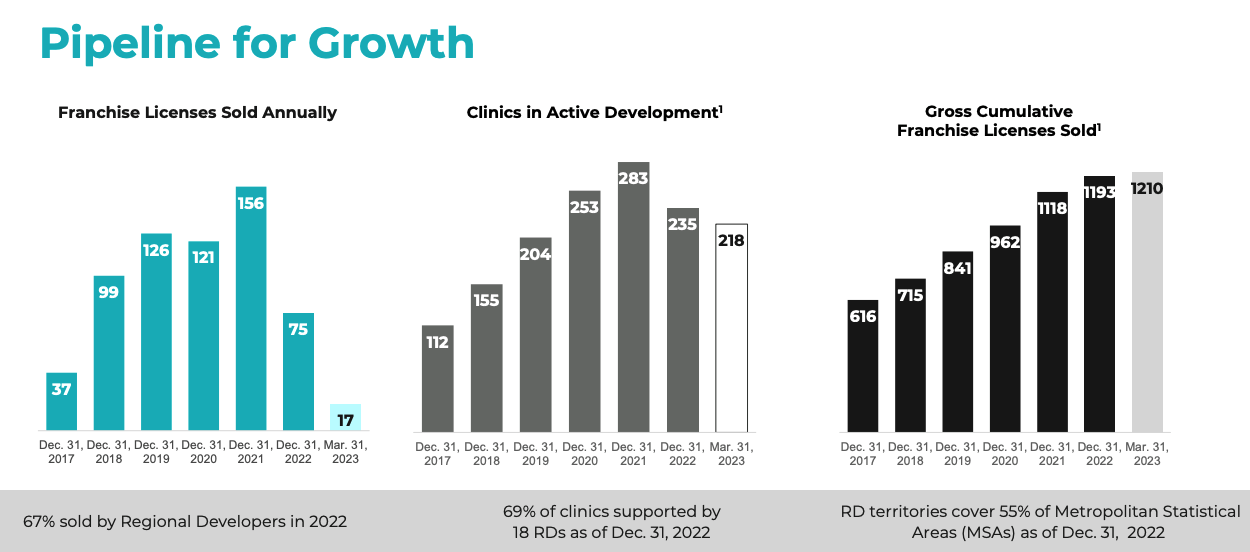

The number of franchise licenses sold for the year ended December 31, 2022 was 75, compared with 156 and 121 licenses for the years ended December 31, 2021 and 2020, respectively.

Joint - historical growth (Joint Q123 earnings presentation)

{kind=link}

As we can see above - in a slide from Joint's Q1 2023 earnings presentation - the rate of franchise license sales has slowed, and could fall again this year based on Q1 performance, while the number of clinics in active development is falling, and gross licenses sold is not growing as it once was.

That's not necessarily a problem, given that a plateau in the growth trajectory is often a feature of a company that has been scaling rapidly, and marks a transition to a more mature company - after all, even if growth has slowed, cumulatively the company is earning more revenues than ever before.

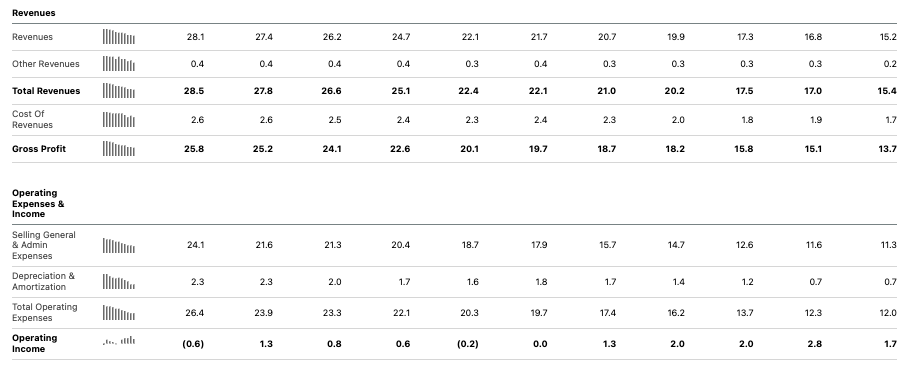

When Joint launched its initial public offering ("IPO") in 2014, selling 3 million shares at a price of $6.50 to raise $17.1m, the company drove just $6.9m revenues in that year, making a net loss of $3m. Last year, the company posted revenues of $100.5m, which represents a CAGR of 35% for the top line, but net income came in at $1.2m, for earnings per share of $0.08.

As such, we can conclude that Joint has not met the market's expectations around continual growth, or profitability - two good reasons for a share price correction - although low growth and negligible profits from a young and growing company do not normally drag a stock price down from >$100, to <$15 in less than seven months, which is what happened to Joint stock between November 2021 and June 2022.

Doubts Around Joint's Business Model

To have slipped so far in such a short space of time seems to suggest the market had a complete change of opinion about Joint and its business model - the market will usually forgive a couple of quarters of slow growth if it believes a business has long term credibility - as the market certainly seemed to believe was the case with Joint in early 2021.

Joint's guidance for FY23 is for revenues of $123m - $128m, adjusted EBITDA of $12.5 - $14m, and 100-120 new franchised clinic openings, with 8-12 new Greenfield clinics. The top line growth rate is still a solid 24% year-on-year at the midpoint of guidance, although one issue may be that Joint started from such a low bar - just $7m revenues in 2014 - and that the market was expecting growth in the triple-digit percentages annually, with revenues perhaps climbing towards $500m by 2023, not ~$125m.

Another issue to consider is that Joint's franchise model may be slightly broken.

{kind=link}

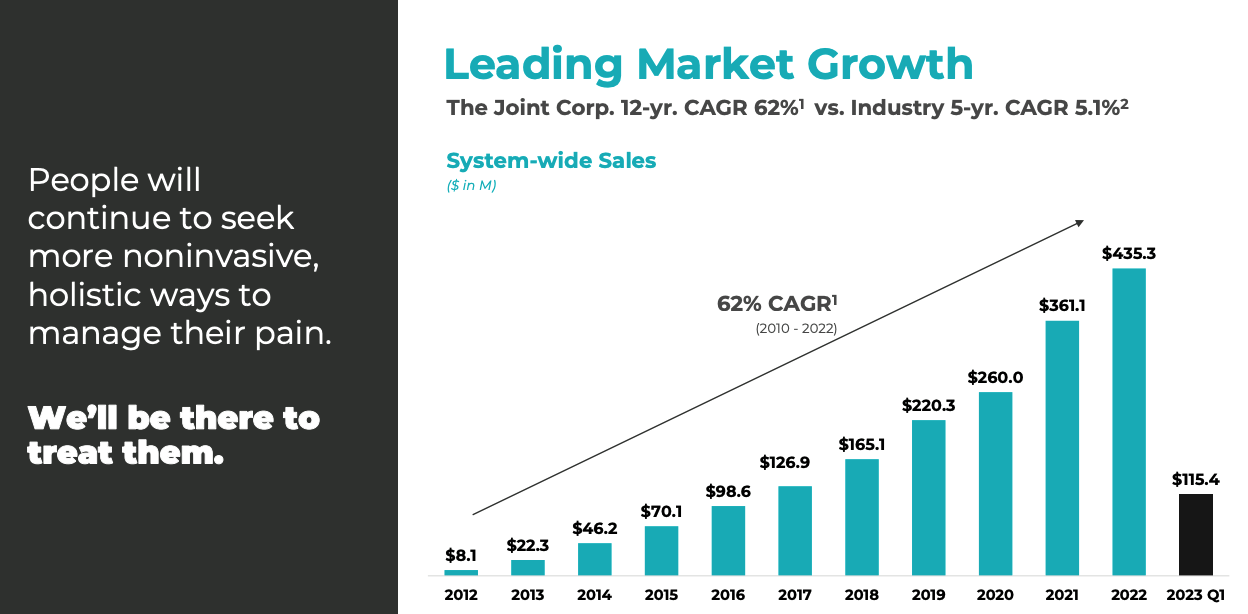

As we can see above, in terms of system wide sales, Joint's CAGR of 62% is nearly double its top line CAGR, but its franchise operations generated just $11.3m of revenues in Q1 2023, vs. $9.8m in the prior year period, while corporate clinics generated $17.1m. The corporate clinics segment recorded an operating loss of $(550k), however, while the franchise segment made an operating profit of $4.6m.

Joint presumably wants the majority of its business to be franchise based - the corporate segment is losing money owing to higher costs and depreciation of assets - but even though this part of the business is profitable, it is, arguably, not nearly profitable enough to support business growth. If Joint doubled its number of franchise clinics in 2023, it would only earn ~$44m more revenues, and ~$20m in profit, based on Q1 2023 segment reporting.

That growth is not going to happen, but even if it did, although it might trigger some share price upside, it would certainly not justify the company's former market cap of $1.5bn, although it wouldn't be unreasonable (in my view) for a profitable company with close to $200m revenues per annum, and no significant debt would justify a market cap valuation ~$500m, at least.

Joints says - in a corporate presentation - that only 4.9% of franchise concepts have 500-plus units. Depending on how you look at it, that could either mean that Joint is in rarefied air among franchise owners, or that its franchise has a profitability problem, and the company ought to be earning substantially more per unit.

Joint's CEO is a franchise specialist - former companies include Tasti D-Lite, Planet Smoothie, and Mail Boxes - while almost the entire management team has franchise experience - could management simply have misjudged the economics of the business?

{kind=link}

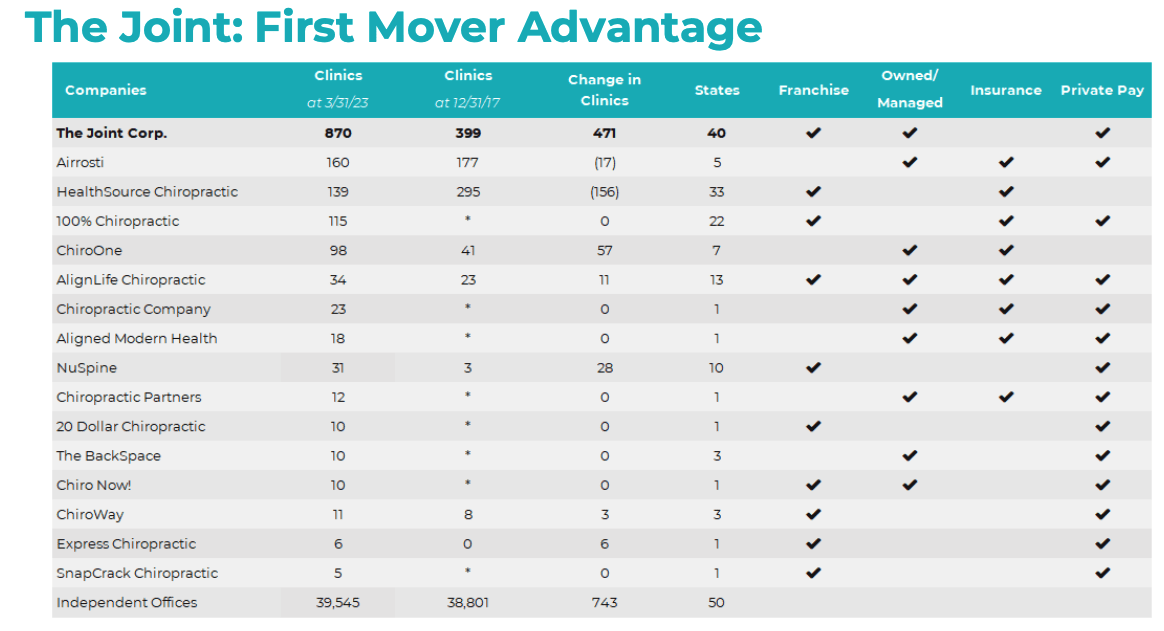

As we can see above, Joint has a dominant presence in its market, but a dominant market share is only strictly a good thing if it can be translated into profitability. As we can see below, Joint is barely squeezing a $1m operating profit from its giant portfolio, and after a decade, the market is probably right to be asking if this is an industry profitable enough to invest in?

{kind=link}

Joint says it treated 1.6m unique patients in 2022 (theoretically earning ~$62.5 per patient per annum), and says that the chiropractic industry is worth $19.5bn, and growing as more and more Americans learn about its benefits. As such, Joint has a tiny theoretical share of the market of ~2%, with independent practices dominating the landscape.

There are a couple of potential flaws in Joint's approach that may significantly restrict its ability to grow however. Firstly, Joint's franchises don't work with people covered by insurance - meaning that if your physician detects you have back pain, and you have insurance, you may well opt to go to a chiropractor that works with your health insurer as opposed to joining Joint.

Secondly, perhaps the "bare bones," "no frills" approach does not strike much of a chord with patients - sessions can last just five minutes - and the lack of any potential for add-on services again limits potential for profitability. Thirdly, Joints says chiropractors working at its centers earn an average annual salary of ~$85,000, higher than the industry average of $81,240.

Is Joint being too generous to its franchisees, impacting its profits, or is this the rate the company must pay to attract staff? Whichever way you look at it, it's a difficult problem to resolve, as it's difficult to walk back salaries whilst attempting to persuade more people to consider a career as a chiropractor.

Joint says it has developed software that allows it to provide administrative services for all franchisees that gives it unique insight into where to develop new franchises, although there's limited evidence to suggest it has been deployed usefully to date - and as the business grows more geographically diverse, it may become significantly more expensive to oversee, due to differences in state laws, demographics, and cultural and behavioral differences.

Concluding Thoughts - Is The Joint Corp A Buy, Sell, Or Hold

It's strange to return to reviewing a company whose business model and ambition is nearly identical to what it was two years ago, and, after two years of >20% top line revenue growth, finding that company's share price has decline in value by >70%.

The pandemic era threw up some incredible, anomalous valuations, although in the main, the companies with sky-rocketing share prices had exposure to the COVID testing and treatment market, and those whose share prices were tumbling were set to be disrupted in the absence of a Business As Usual ("BAU") operating environment.

In Joint's case, the situation seems to have been reversed. Riding high at the height of the pandemic, even with access to its centers restricted, the company's share price has apparently been devastated by BAU market conditions. Could it have been that Joint's franchise model looked better on paper than it does in real life? Was the market expecting growth to explode in a BAU environment, only to sell-off when the anticipated explosion in revenues did not materialize?

Although I may have been critical of Joint in this post, this is still a business that will - if guidance is met - drive >$120m of revenues in 2023 - up >20% year-on-year - and generate positive EBITDA, as the business grows in size. Usually, such figures and outlook would support a company valuation substantially higher than $194m, which is <2x FY23 sales.

Net income generation may not be especially impressive, and perhaps the market is right to have reservations about how successful a chiropractics franchise business can be - after all, if it was a strong business model, wouldn't there be more such businesses in evidence? - but even so, you can make a good case that Joint is oversold.

In light of all this, 2023 and 2024 strike me as critical years for Joint, with a great deal at stake. Joint's business model is now mature enough - with nearly 1k clinics in operation - to be judged as a mature business, and the conclusion is inescapable - this is not a very profitable model.

With that said, can management now begin to use its business intelligence, collected over a long period, and begin to pull the right levers to make the business more profitable?

The company has warned against over-extending itself, which is a good thing as it has very little cash, just under $15m as of Q1 2023, and if management's math has been just a little off, the business could lurch toward net losses, which could have a domino-like effect as every franchise has a similar economic possibility.

That presents a conundrum for management - keep growing an unprofitable business, or retreat, and suffer the economic consequences of a move that the market will judge negatively.

The investment case is built around Joint finding and fixing the elements of its business model that are unprofitable - in my view, a couple of good earnings quarters could easily increase the company valuation by >100%, given that would imply a P/S ratio of barely more than 2x, and perhaps reduce the price to earnings ratio to a more competitive figure. The price to forward EBITDA in 2023 is a fairly attractive 15x.

Things are finely balanced heading into Q2 2023 reporting season - Joint reports on Aug. 10 - but on balance, I believe management's chances of turning very minor profits into more major ones may be higher than the chances of the business model unravelling completely, and as such, for me, Joint stock represents an intriguing buy and hold, for a 12- 18-month period.

For further details see:

The Joint Corp.: Cracking Upside Bet, Or Creaking Business Model?