EQR - The Looming Crash In Multifamily Rents: Is A Hard Landing Inbound?

2023-07-05 09:21:45 ET

Summary

- The US rental market is experiencing a downturn, with more people ending leases than starting them overall. Apartment vacancy rates just matched the COVID-19 high of 7.2% and are rising.

- Meanwhile, multifamily housing construction just hit an all-time high.

- This trend could negatively impact landlords and investors, particularly those invested in rental-heavy funds such as the iShares Residential and Multisector Real Estate ETF.

- The decline in rent is most pronounced in Sunbelt markets, with the concurrent "Airbnbust" doubly affecting hot markets such as Austin and Phoenix.

- The rapid shift in the rental market is another data point indicating the probability of an economic hard landing.

You oughta know by now (oughta know)

Who needs a house out in Hackensack

Is that what you get for your money?

It seems such a waste of time

If that's what it's all about

Mama if that's movin' up

Then I'm movin' out!

- Movin' Out (1977), Billy Joel .

Rents surged to unprecedented levels during the pandemic, fueled by government stimulus boosting demand and eviction moratoriums restricting supply. There's an old saying in economics that " the cure for high prices is high prices ," and in this case, the surge in sales prices and rents has sparked a massive construction boom in the United States. If you really think about it, it was a bit strange to have a construction boom when the overall population had flatlined due to the pandemic , only to return to very sluggish growth afterward! But after an epic surge, however, the data now shows that more people are ending leases than starting them, just as multifamily units under construction hits an all-time high. Real-time data on vacancies shows that the rate of apartment vacancy just matched the COVID high of 7.2% and is now rising by 21 bps per month. Falling rents will be cheered by consumers, but it's bad news for landlords and investors, especially large corporate landlords that have made big money over the past few years. This trend has a slew of implications for investors in rental-specific funds like the dedicated iShares Residential and Multisector Real Estate ETF ( REZ ), and also for broader ETFs like Vanguard's Real Estate ETF ( VNQ ).

The Wild Ride Of 21st-Century Housing

How did the pandemic affect demand for real estate? Fortunately, there is extensive data to guide us . Americans generally love real estate when it's expensive and going up, and hate it when it's cheap and going down. Massive booms and busts have defined American economic history for hundreds of years, and the 21st century has been no exception.

{kind=link}

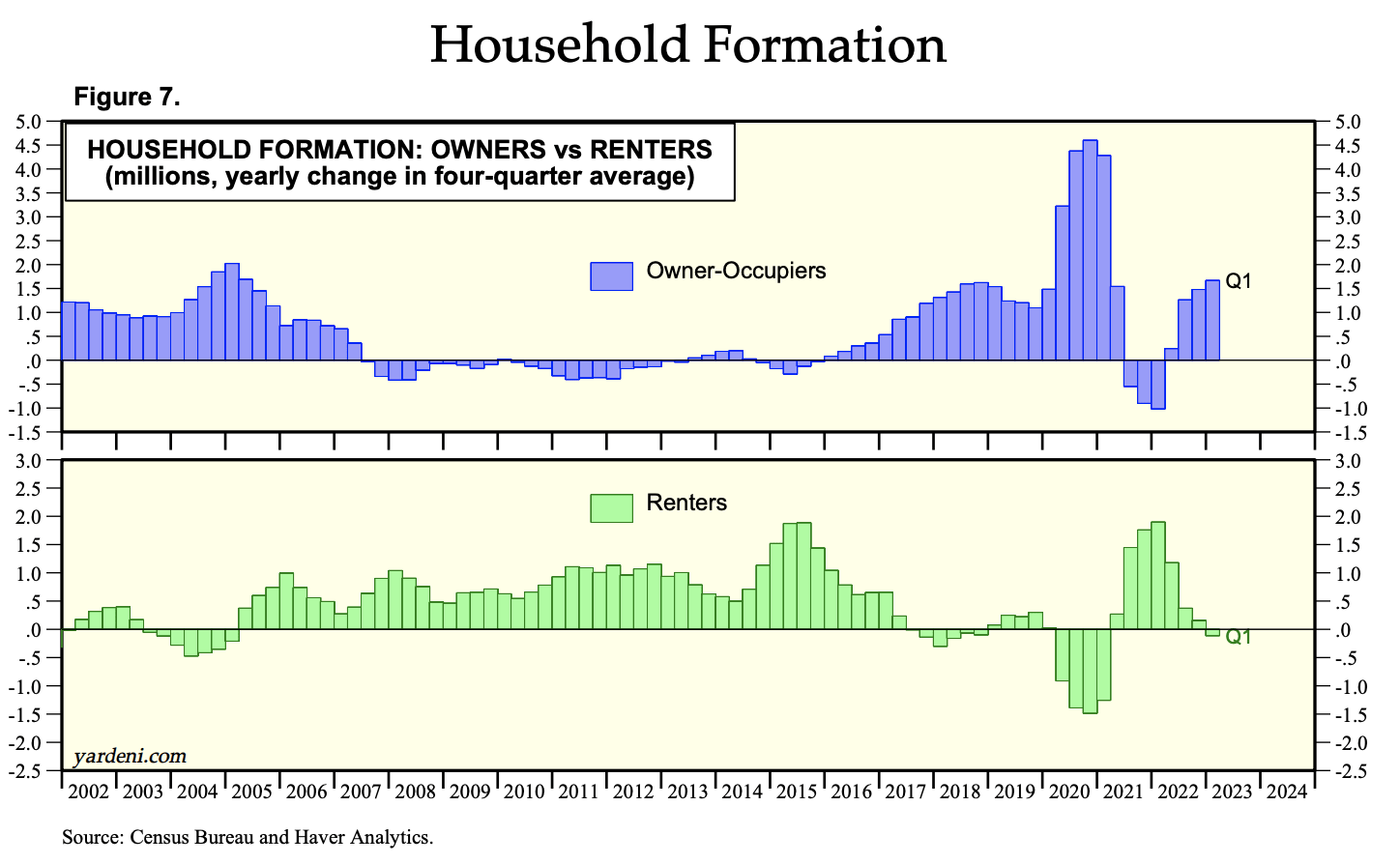

Rental vs. Ownership Demand (Yardeni Research)

2002-2007- here we see a steady pace of household formation, with the high point being in 2004-2005 when Americans last went wild for housing.

2008-2011- a huge bust in owner-occupied real estate as demand for housing goes down, despite healthy population growth.

2012-2016– the recovery started rather weak, for example in 2015 we see Americans largely moving into rentals despite mortgages being incredibly cheap at the time.

2017-2019- the overall economy is healthy, supply and demand are well balanced, and a few million people who were renting finally found the ability to buy. There's some trouble in areas like California, but the national housing market is really good at this point.

2020- Chaos ensues as nearly 1.5 million households flee rentals (mainly in cities) and roughly 2.5 households more people than expected buy homes. Rent falls and home prices rise, but there's nothing too crazy going on yet. Those who are willing to work during the pandemic are rewarded with inflation-adjusted wages that are higher than before.

2021- More chaos–well-intentioned government policies such as the federal eviction ban and stimulus checks redistribute income and wealth for political gain. Overall, living standards fall about 3.1% in 2021 amidst runaway inflation. The boom in home prices induces roughly a million households to sell and rent. At the same time, many people who fled cities begin to return, and rents soar after crashing. Reopening also brings an Airbnb ( ABNB ) boom as listings on the site soar to take advantage of the gap between long-term rental rates and demand for travel.

2022- Conventional mortgage rates skyrocket from 3% to 7% as the Fed recognizes the inflation problem and starts to fight it. Combined with previous price increases, this means that the typical mortgage payment for buying a house is often triple what it was five years ago. Many people think this is crazy and refuse to participate in the madness, but as buying a home is partly emotional and partly an investment, sales volumes fall about 35-40% from the peak rather than totally plummeting. The situation is better at the high end as other high-income consumers continue to take adjustable-rate mortgages from banks like First Republic ( OTCPK:FRCB ).

2023- People are sick of renting (or at least the data shows they're ending more leases than they're starting). With the economy at full employment, people are earning and banks are willing to lend, albeit at fairly punitive rates. However, beneath the surface, jumbo mortgage rates continue to march higher and banks get increasingly cautious about lending standards. As of my writing this, jumbo mortgages are exactly at their post-2008 high of just under 7%, with more increases likely to come if the economy weakens, the Fed raises rates higher, or both.

However, there's one piece in the data that's more important than all the others, and that's the fact that people are moving out of rentals. Multifamily construction has long lead times and the supply isn't super flexible in the short run. Multifamily housing starts just hit an all-time high:

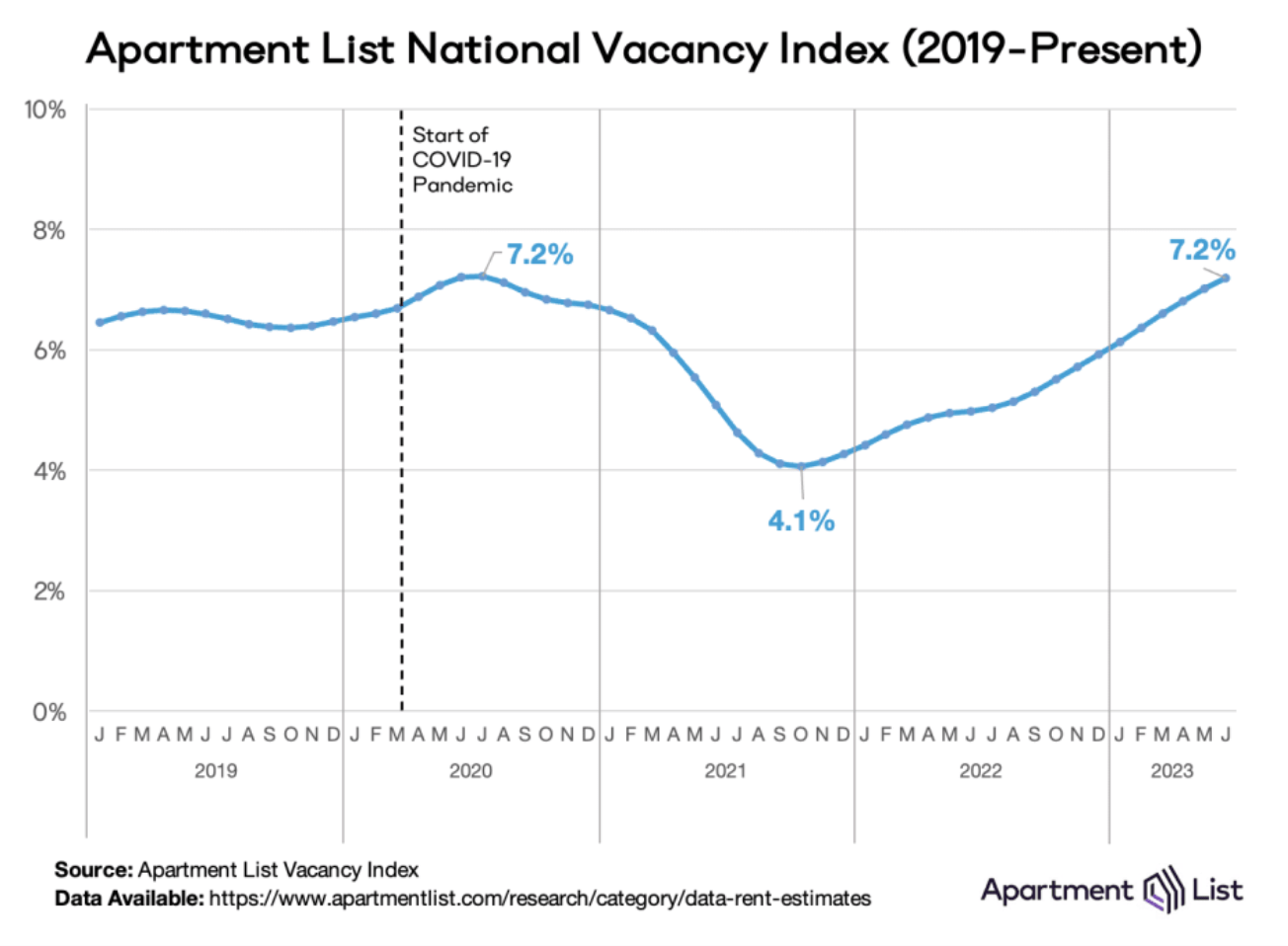

Just as vacancy rates have begun to top the peak of COVID-19.

{kind=link}

Apartment Vacancy US (Apartment List)

Summer is seasonally the strongest time of the year for real estate, so the vacancy rate rising by ~21 bps per month during this time is really surprising. If autumn ends up being weak for rental demand for the existing rental stock plus the roughly one million units under construction, it's not inconceivable for vacancies to hit 10% by spring. This is pure demographics, and there's no way out of it besides cutting prices or abandoning half-finished construction projects. The previous peak in vacancies was roughly 11% in 2009. Residential and multifamily REITs like Equity Residential ( EQR ), Invitation Homes ( INVH ), and Mid-America Apartment Communities ( MAA ) might actually be in some non-obvious economic trouble from this.

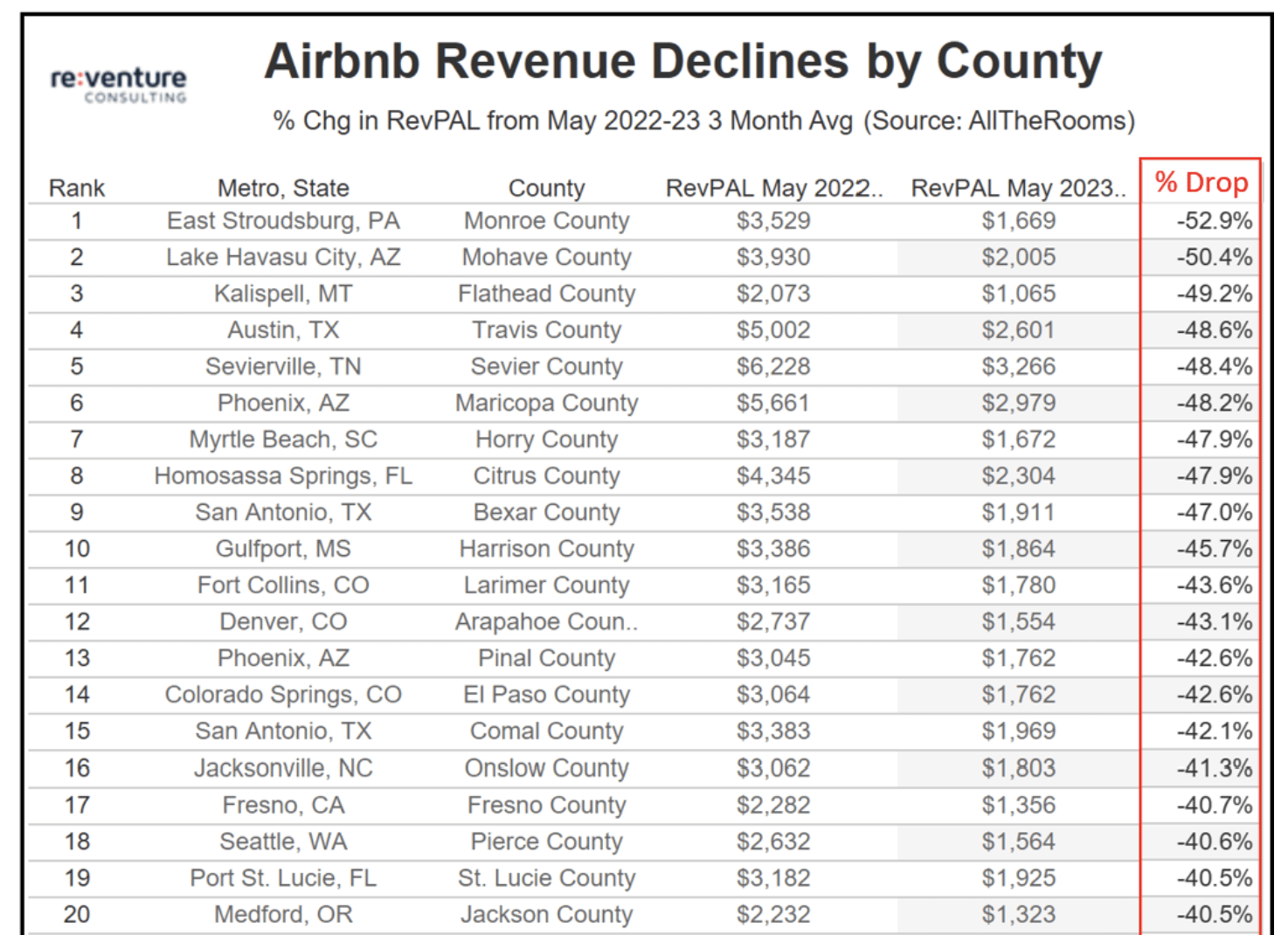

And in case you were wondering, the biggest declines in rent are occurring in Sunbelt markets like Austin and Phoenix and not in New York or California at this time. There was also an explosion in speculators renting apartments and turning them into Airbnb in Florida, Texas, and Arizona. Now that boom has soured into the so-called "Airbnbust," in many markets. If you look at the markets where Airbnb operators are seeing the sharpest revenue declines , you'll again find Austin and Phoenix near the top of the list.

{kind=link}

Airbnb Revenues (Reventure Consulting)

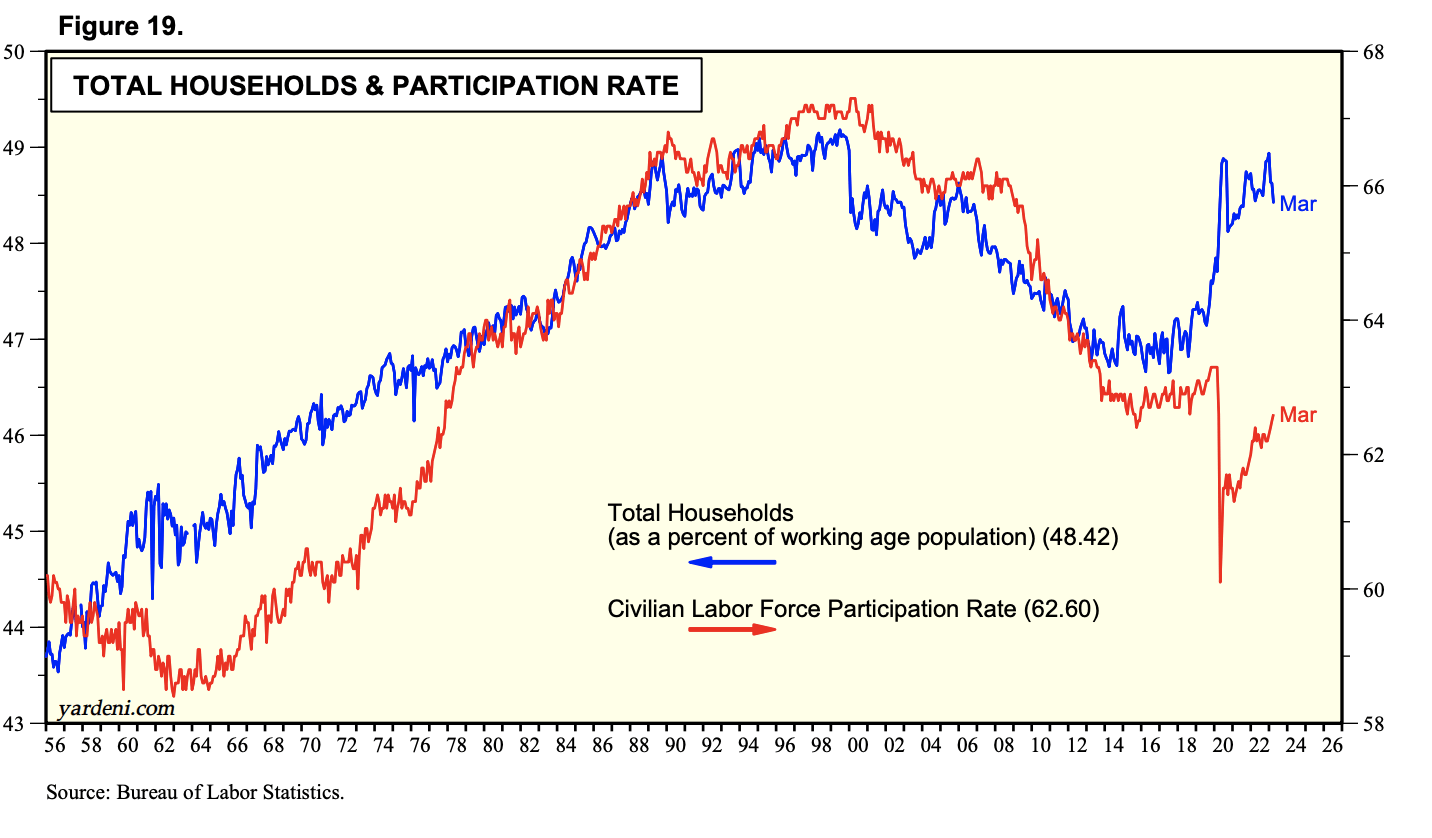

In 2008, much of the leverage in the system was explicit. Banks made bad loans to people who couldn't pay them back. Now, much of the leverage in the system is implicit– with low savings rates and high fixed expenses for consumers. As far as the business cycle is concerned–it's six of one and a half dozen of the other. I've tracked Yardeni Research's housing data for a while, and I've always been fascinated by the ratio of those owning or renting housing (right) with those who work (right). These correlate very highly historically but sharply diverged during the pandemic.

{kind=link}

Total Households vs. Labor Force Participation (Yardeni Research)

The implication here is that a rise in the unemployment rate could flood the housing market with millions of units held by those living off of investment income. Similarly, people moving out of housing could slow the construction sector of the economy, leading to a negative feedback loop. If you're owning or renting a house and aren't independently wealthy, history shows you really need a job! With the median 401k balance sitting at about $70,000 for those 55-64 years old, this divergence won't fly in the long run.

Throw on a roughly 1% reduction in consumer disposable income from student loans resuming , and I think you have the match that will light the tinderbox. The Fed will likely hike at least once more and hold rates there, but the action in the rental market is showing a serious slowdown in consumer demand coming down the pike.

The Business Cycle Is Alive And Well

Market pros and retail investors alike have been surprised to see that economic growth has held up despite rapid tightening from the Federal Reserve and global central banks. It has certainly surprised me. I personally don't care much if I only make 6% this year and someone else doubles their money by going all-in on speculative stocks. Easy come, easy go. The popular opinion now is that the Fed hiking rates and shrinking the money supply doesn't matter anymore.

However, leading economic indicators continue to worsen. Officials at the Fed always say that monetary policy works with long and variable lags of about a year on average . Meanwhile, investors think the Fed doesn't matter, loading up on risk like tourists eating a third edible in Amsterdam because the first two didn't kick in.

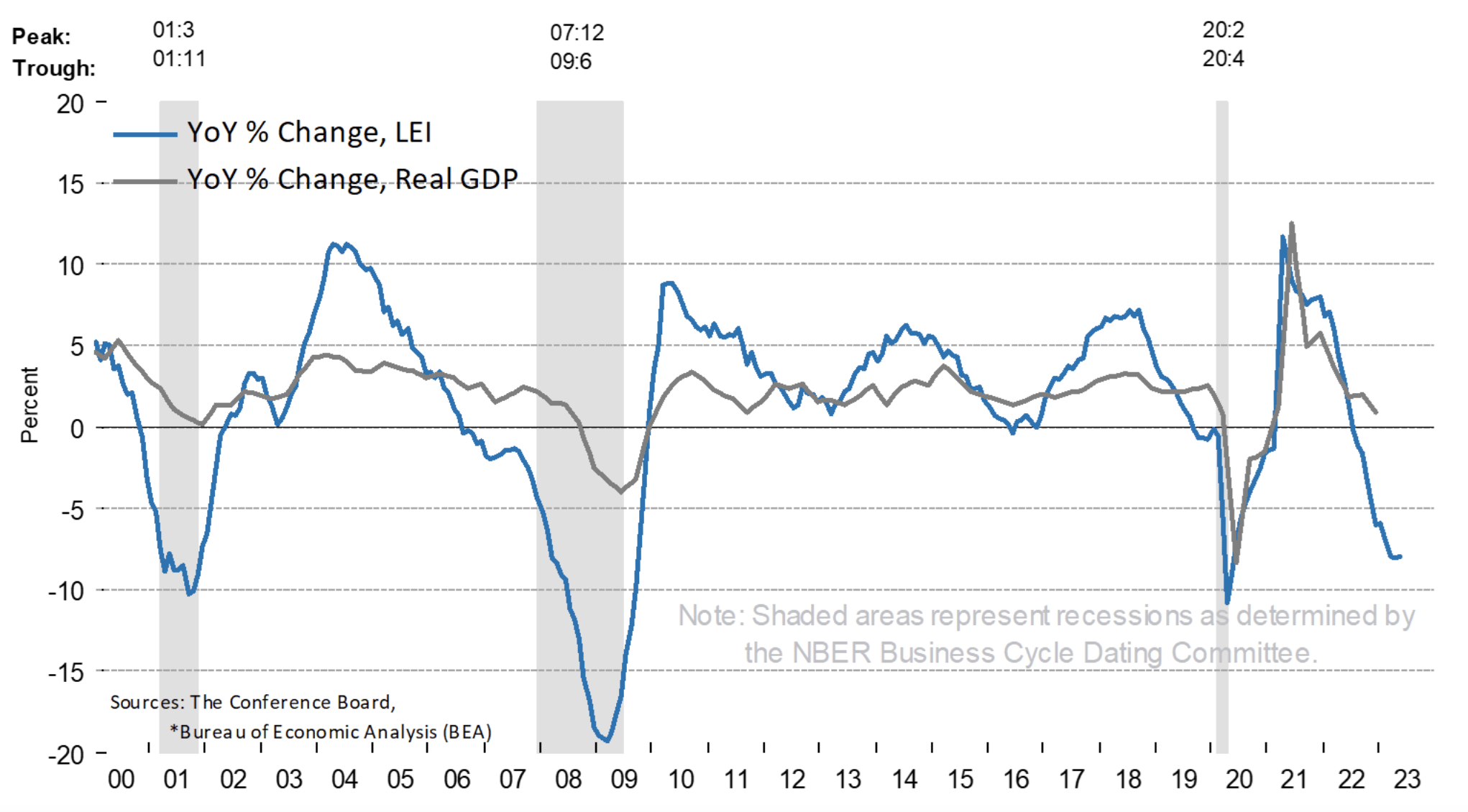

I've shared the leading economic indicators before, and I'll share them again.

{kind=link}

Leading Economic Indicators (Conference Board)

The business cycle does exist, and rapid rate hikes from the Fed are hitting the leading sectors of the economy. Credit is quickly tightening ( look no further than jumbo mortgages vs. Fannie/Freddie mortgages for proof). The yield curve remains highly inverted, both disincentivizing lending further and signaling a recession ahead. Consumer and small business confidence is still negative (this correlates with hiring and large purchases such as houses, cars, and furniture). Manufacturing continues to weaken. Finally, weekly jobless claims are rising, but it's hard to see exactly how much with three holidays over the past six weeks. The only leading indicators that are positive are stock prices and building permits, which don't have the same pull in forecasting the economy.

Manufacturing continues to decline (anything below 50 is contracting).

But services are holding steady.

There are a few different data providers for service PMI numbers, some have the services sector of the economy in expansion and some have it holding steady. The methodology is definitely a factor– for example, before the pandemic, I routinely would book trips the week before. This summer, availability is much worse, so now I've already booked all my summer travel. Will I spend more for the whole summer? I'm not. All I did was book travel sooner than I would have because the media goaded everyone into doing the same.

It's not clear how PMI numbers would handle this, but my guess is that it will lead to a lot of spending early on in the summer that rapidly drops off. Services spending tends to hold steady in all but the worst economic environments. Services held firm in 2008 until the unemployment rate blew up and even then only dropped a couple of percent. This is typical for the business cycle. Meanwhile, new car sales plunged from over 16 million to under 10 million in the 2008 recession. That's why it's worth paying attention to what's going on in the markets for housing, used cars, and manufacturing in general. Durables goods and housing are the business cycle .

Key Takeaways

- After an epic surge during the pandemic, rent is now falling on a seasonally adjusted basis in the US, and falling outright in many markets. Vacancies are rising at a rapid clip, just as a huge amount of construction is underway. The pandemic housing bubble pulled forward years of demand, and the early signs are that much of that projected demand may be going away.

- This is another sign that a hard landing is still coming, despite boundless investor optimism for buying call options.

- Just because there's a long lag from the economic effects of the Fed's rapid tightening campaign, it does not mean that a sharp slowdown and fall in asset prices are not coming.

- That the Fed is likely forced to continue to hike into weakening economic conditions makes a soft landing less likely, not more. It's up to you whether you'd prefer to earn 5.5% in Treasury bills or take a flier on stocks, but I'm quite comfortable with the former.

For further details see:

The Looming Crash In Multifamily Rents: Is A Hard Landing Inbound?